EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

LATAM Airlines Group (NYSE:LTM) presented its first quarter 2025 results on April 29, showcasing record profitability and strong operational performance. The Latin American carrier transported over 21 million passengers during the quarter while maintaining healthy load factors despite significant capacity expansion. LATAM’s stock closed at $27.36 on April 28, near its 52-week high, reflecting investor confidence ahead of the earnings release.

The airline continues to strengthen its competitive position in the region, having received recognition as a SkyTrax World Airline Awards Winner and an APEX+ Five Star Airline for 2024, credentials that underscore its focus on service quality and customer experience.

Quarterly Performance Highlights

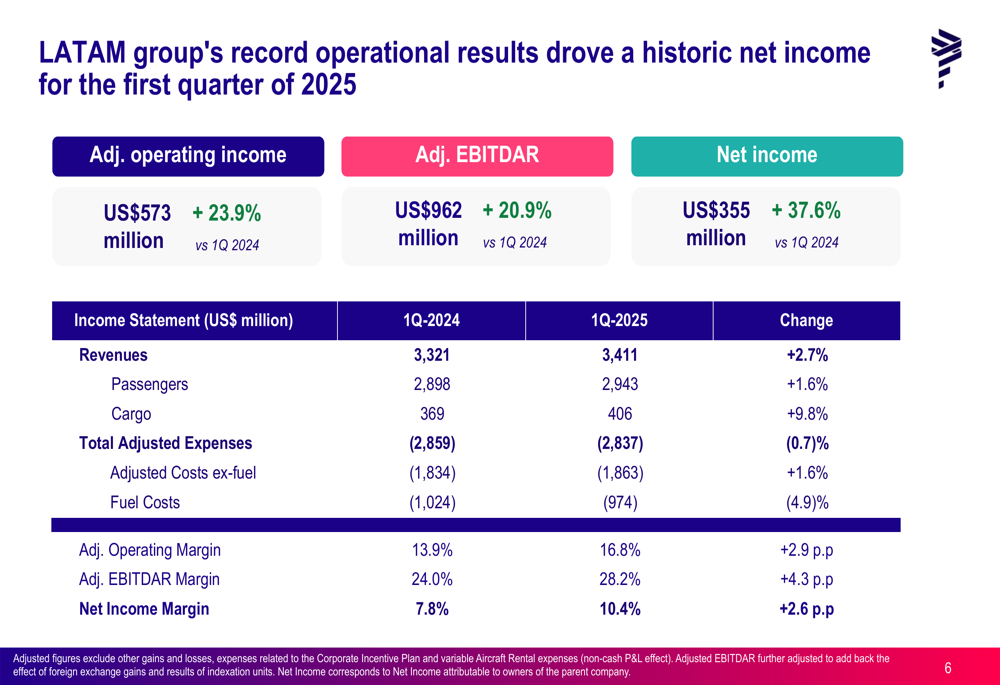

LATAM reported a 37.6% year-over-year increase in net income to $355 million for Q1 2025, driven by strong operational performance and effective cost management. The company achieved an adjusted operating margin of 16.8%, representing a 2.9 percentage point improvement compared to the same period last year.

As shown in the following summary of key operational and financial metrics:

The airline expanded capacity (measured in Available Seat Kilometers or ASK) by 7.3% compared to Q1 2024, while maintaining a solid consolidated load factor of 83.3%. Though this represents a slight decrease from the 84.4% load factor in Q1 2024, it remains strong considering the significant capacity expansion.

Revenue increased by 2.7% year-over-year to $3.41 billion, with passenger revenue growing 1.6% to $2.94 billion and cargo revenue showing robust growth of 9.8% to $406 million. The financial performance details demonstrate the company’s ability to grow profitably:

Detailed Financial Analysis

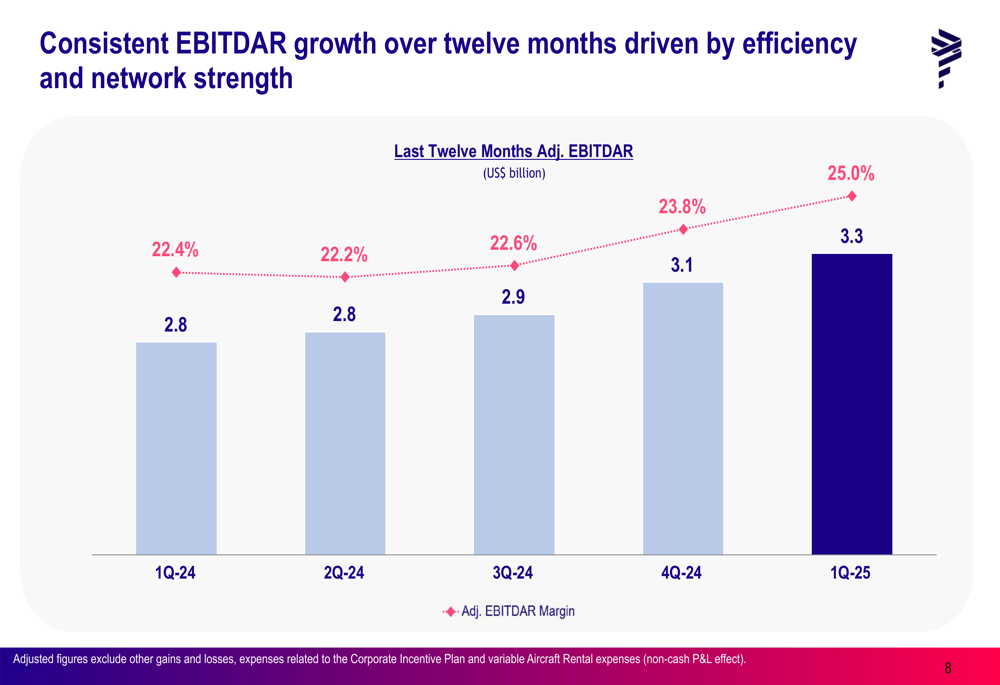

LATAM’s adjusted EBITDAR (Earnings Before Interest, Taxes, Depreciation, Amortization, and Restructuring or Rent costs) reached $962 million, a 20.9% increase from Q1 2024. The adjusted EBITDAR margin expanded by 4.3 percentage points to 28.2%, reflecting improved operational efficiency.

The company has maintained a consistent upward trajectory in its EBITDAR performance over the past year:

Cost containment remains a key focus area for LATAM. The airline has successfully kept its adjusted passenger CASK ex-fuel (Cost per Available Seat Kilometer excluding fuel) at competitive levels, decreasing from 4.2 cents in 2019 to 4.1 cents in the twelve months ending Q1 2025, demonstrating effective cost management despite inflationary pressures across the industry.

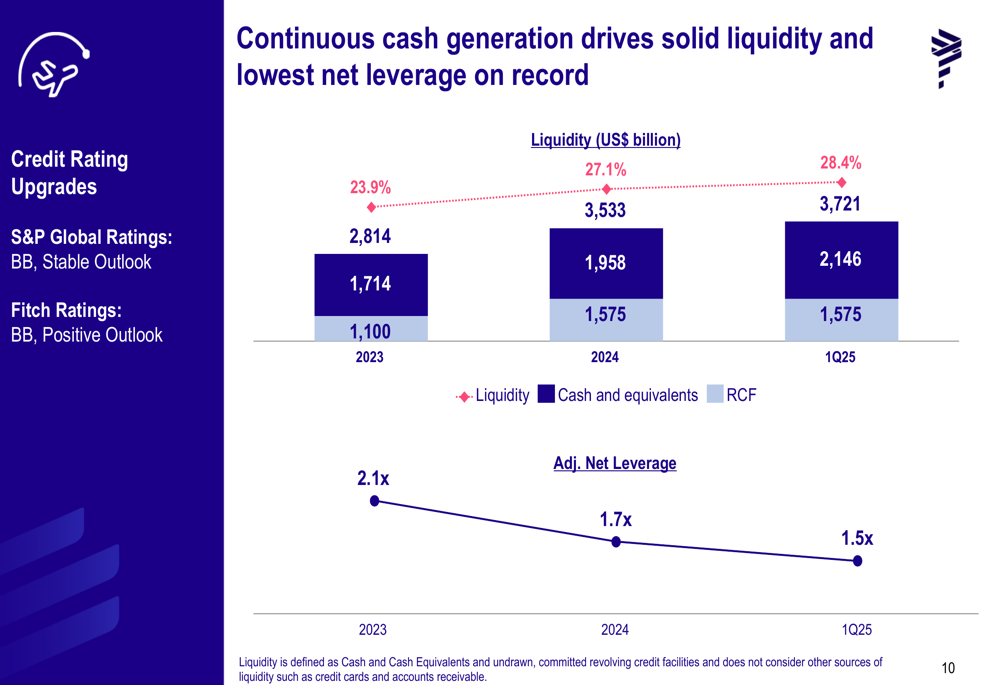

LATAM continues to strengthen its balance sheet, with liquidity increasing to $3.72 billion (28.4% of LTM revenue) in Q1 2025, up from $3.53 billion (27.1%) at the end of 2024. The adjusted net leverage ratio improved to 1.5x, down from 1.7x in 2024 and 2.1x in 2023, indicating a progressively stronger financial position.

Strategic Initiatives

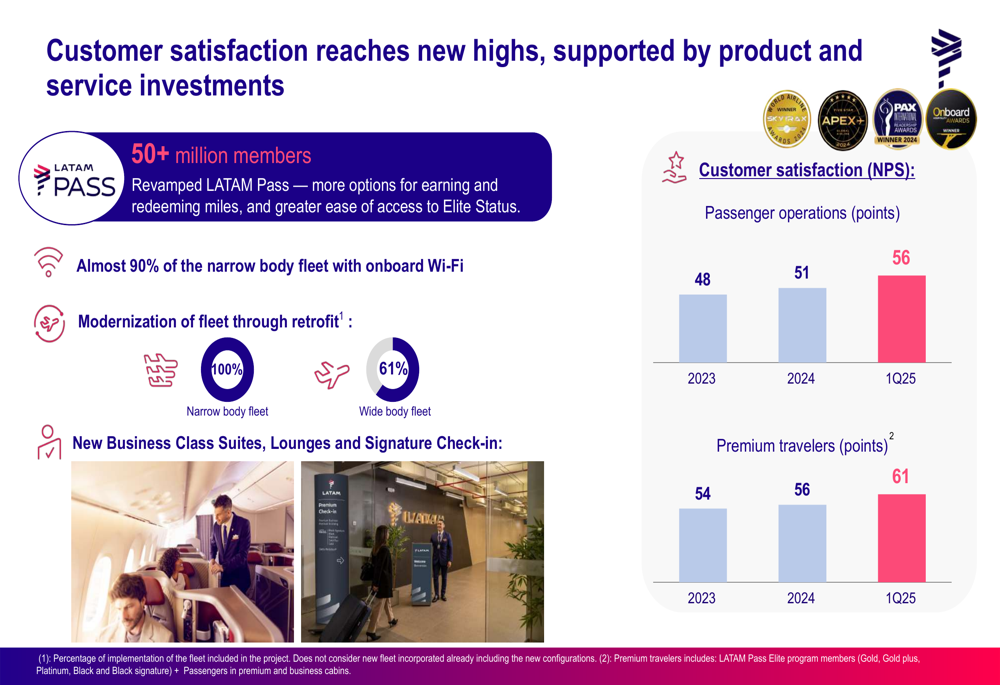

LATAM’s customer-centric strategy is yielding positive results, with customer satisfaction (Net Promoter Score) reaching 56 points in Q1 2025, up from 51 in 2024 and 48 in 2023. Premium travelers’ satisfaction has also improved significantly to 61 points.

The airline has invested in enhancing the passenger experience through fleet modernization, with 100% of its narrow-body fleet and 61% of its wide-body fleet now retrofitted. Almost 90% of the narrow-body fleet is equipped with onboard Wi-Fi, and the company has introduced new Business Class Suites, lounges, and signature check-in services.

As illustrated in the following customer satisfaction metrics:

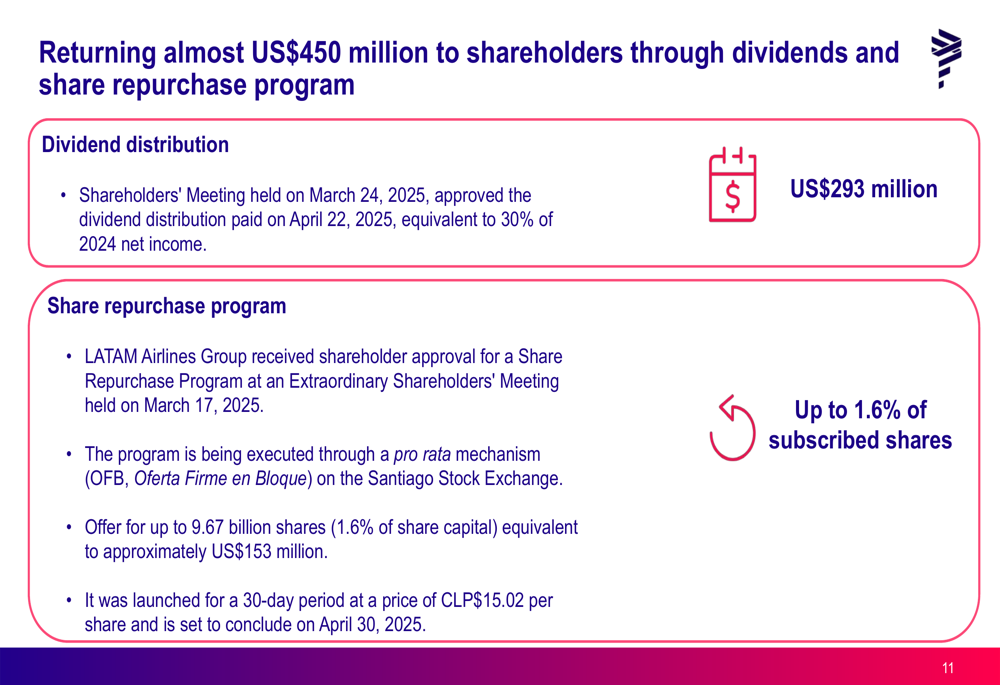

In a significant move to reward shareholders, LATAM announced capital return initiatives totaling nearly $450 million. This includes a dividend distribution of $293 million (equivalent to 30% of 2024 net income) paid on April 22, 2025, and a share repurchase program for up to 1.6% of subscribed shares, valued at approximately $153 million.

Forward-Looking Statements

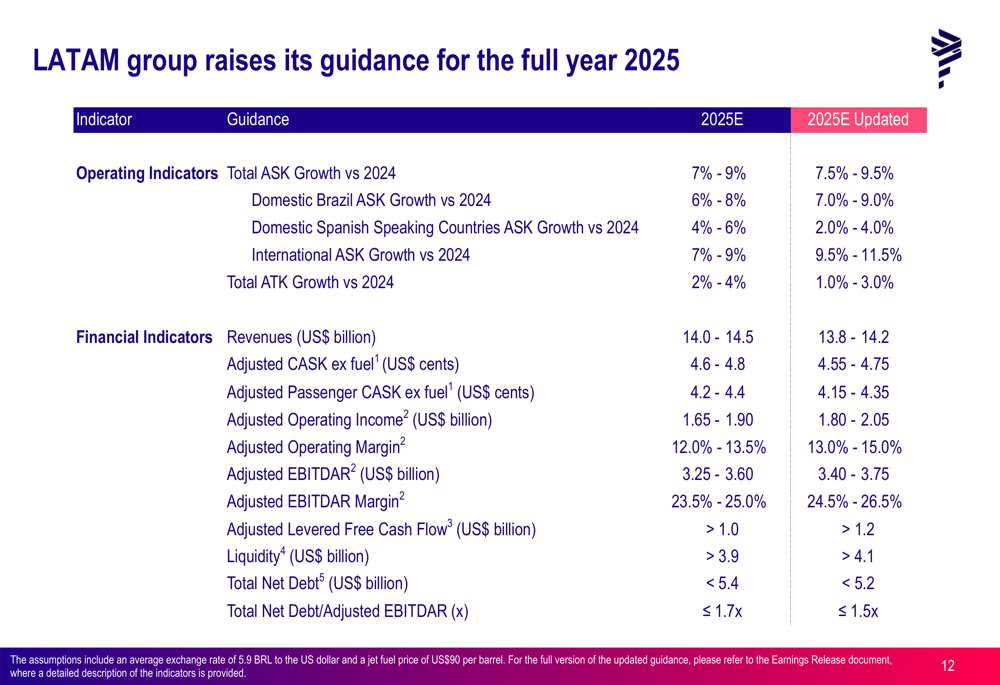

Based on its strong Q1 performance, LATAM has raised its full-year 2025 guidance. The company now expects an adjusted operating margin of 13.0% to 15.0% and adjusted EBITDAR of $3.40 to $3.75 billion.

The airline forecasts capacity growth of 7.5% to 9.5% for 2025 compared to 2024, with international routes showing the strongest expansion at 9.5% to 11.5%. Revenue is projected to reach $13.8 to $14.2 billion for the full year.

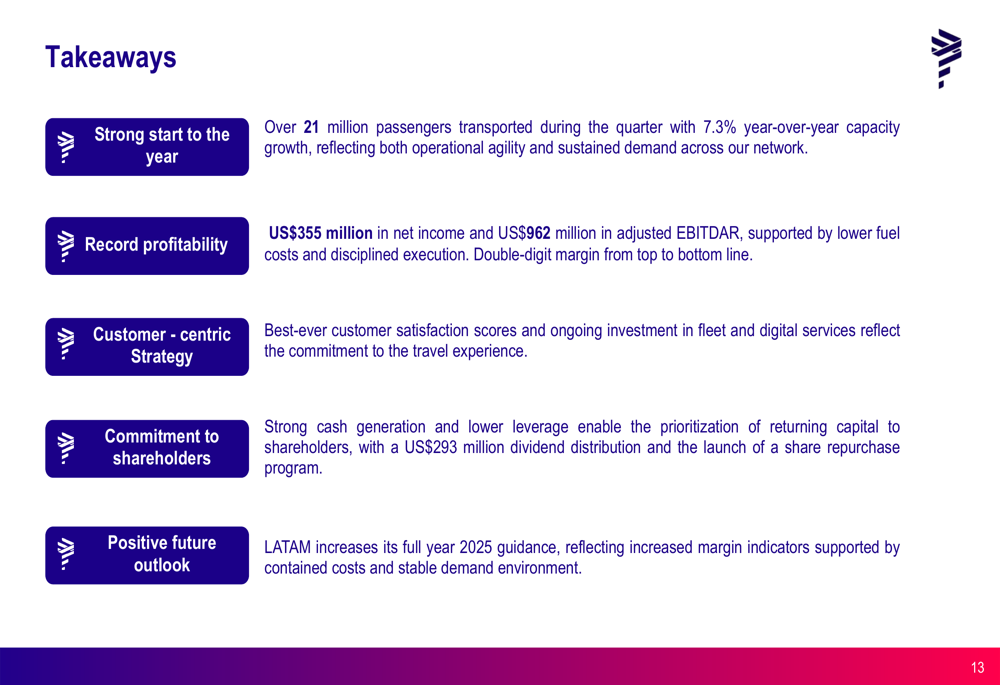

LATAM’s key takeaways from the quarter emphasize its strong start to 2025, record profitability, improving customer satisfaction, commitment to shareholder returns, and positive outlook:

The airline’s incorporation of Argentina into its Joint Venture Agreement with Delta Air Lines (NYSE:DAL) represents another strategic move to strengthen its network across the Americas, potentially opening new growth opportunities in the region’s third-largest aviation market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.