JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Latham Group Inc (NASDAQ:SWIM), a leading manufacturer of in-ground residential swimming pools and accessories, presented its Q1 2025 earnings results on May 6, 2025, highlighting modest quarterly improvements and an optimistic outlook for the full year despite ongoing market challenges.

The company continues to navigate a challenging environment for new pool installations, with U.S. pool starts projected to remain flat year-over-year at approximately 72,000 units in 2025 – well below the long-term average of 100,000 annual installations. Despite these headwinds, Latham maintains its position as the market leader in fiberglass pools and is pursuing strategic initiatives to drive growth.

As shown in the following slide detailing the company’s long-term growth story:

Q1 2025 Performance Highlights

For the first quarter ended March 29, 2025, Latham reported net sales of $111.42 million, a slight increase from $110.63 million in the comparable period of 2024. The company posted a net loss of $5.96 million, an improvement from the $7.86 million loss recorded in Q1 2024.

However, Adjusted EBITDA declined to $11.14 million from $12.29 million in the prior-year quarter, with Adjusted EBITDA margin contracting to 10.0% from 11.1%. This performance reflects the ongoing market challenges in the residential pool sector, though the company’s ability to maintain revenue stability demonstrates resilience in a difficult environment.

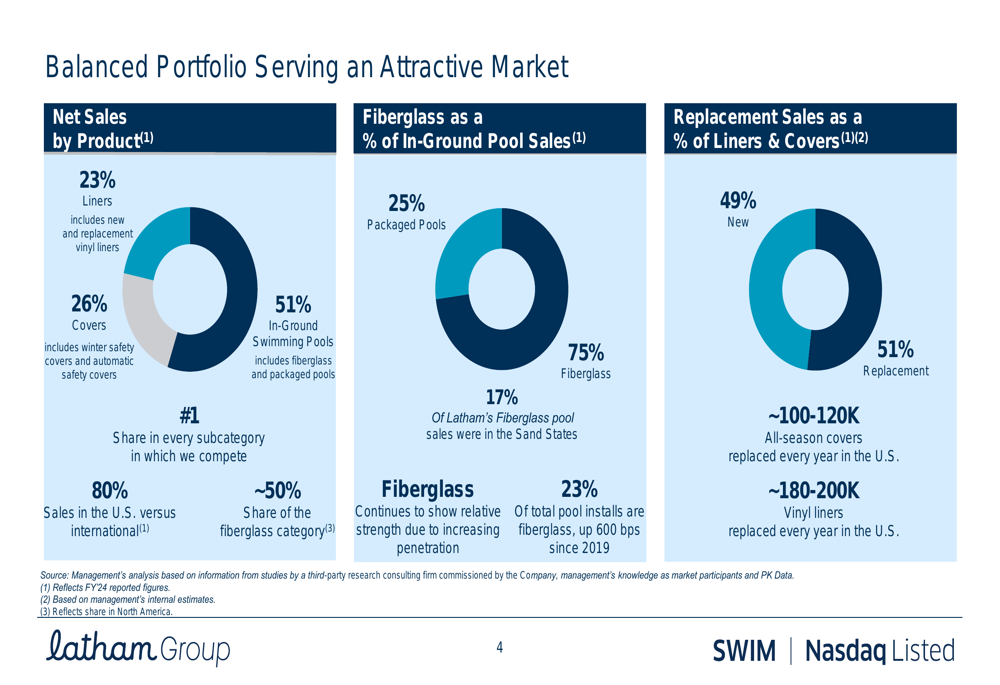

The company’s product portfolio remains well-balanced across multiple categories, providing diversification that helps buffer against market fluctuations. As illustrated in the following breakdown:

In-ground swimming pools represent the largest segment at 51% of net sales, with fiberglass pools accounting for 75% of that category. Covers (including winter safety covers and automatic safety covers) contribute 26% of sales, while liners make up 23%. Notably, approximately half of liner and cover sales come from replacement demand rather than new installations, providing a more stable revenue stream.

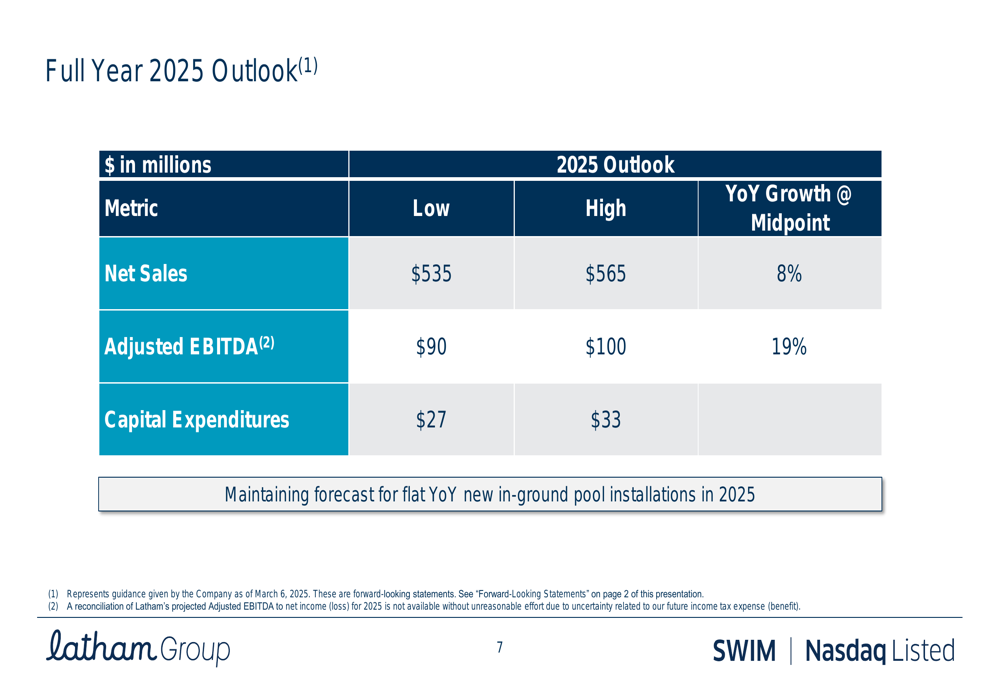

Full Year 2025 Outlook

Despite the challenging market conditions, Latham provided an optimistic outlook for the full year 2025, projecting growth that would outpace the broader pool market. The company’s detailed guidance is presented in the following slide:

Latham expects net sales between $535 million and $565 million for 2025, representing 8% year-over-year growth at the midpoint. Adjusted EBITDA is projected to reach $90-100 million, a 19% increase at the midpoint compared to 2024. Capital expenditures are forecast between $27-33 million.

This positive outlook is particularly notable given the company’s expectation for flat year-over-year new in-ground pool installations in 2025, suggesting that Latham anticipates gaining market share and increasing penetration of its higher-margin products.

Strategic Growth Initiatives

Latham’s growth strategy centers on three key drivers that the company believes will enable it to outperform the broader market in 2025, as outlined in this slide:

The company is particularly focused on expanding its presence in the "Sand States" (primarily Florida and Texas), which represent significant growth opportunities for fiberglass pools. Management highlighted that 75% of the largest master-planned communities are located in these two states, with approximately 30,000 new homes constructed in such communities in 2023.

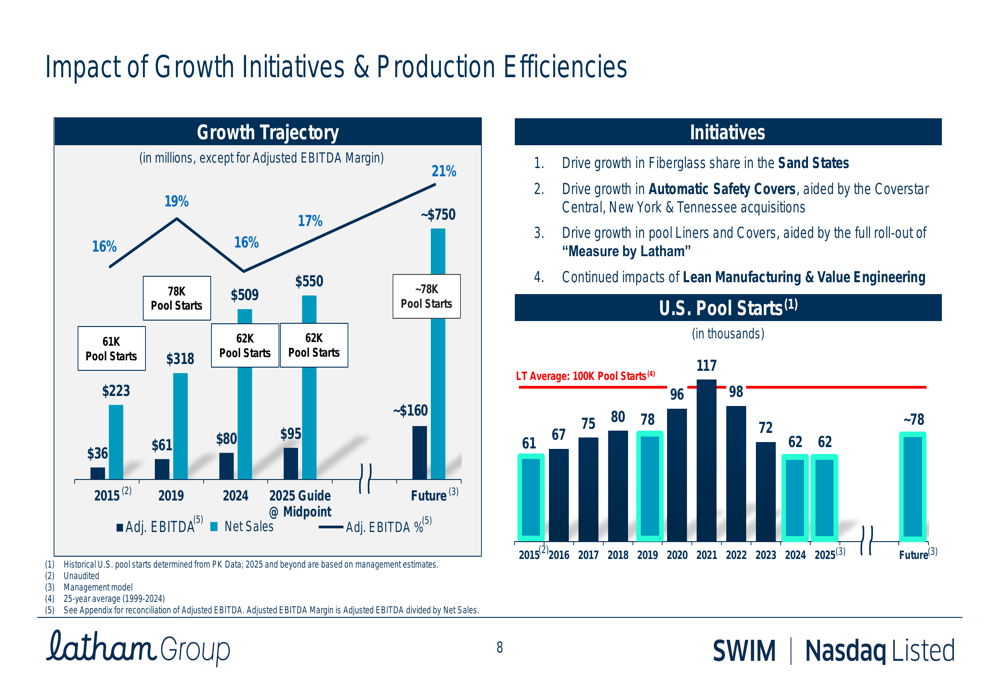

Latham’s long-term growth trajectory and the impact of its strategic initiatives are illustrated in the following chart:

The company envisions growing to approximately $750 million in net sales and $160 million in Adjusted EBITDA in the future, representing substantial growth from its 2024 results of $509 million and $80 million, respectively. This growth is expected to come despite U.S. pool starts remaining below historical averages, highlighting the company’s focus on market share gains and operational efficiencies.

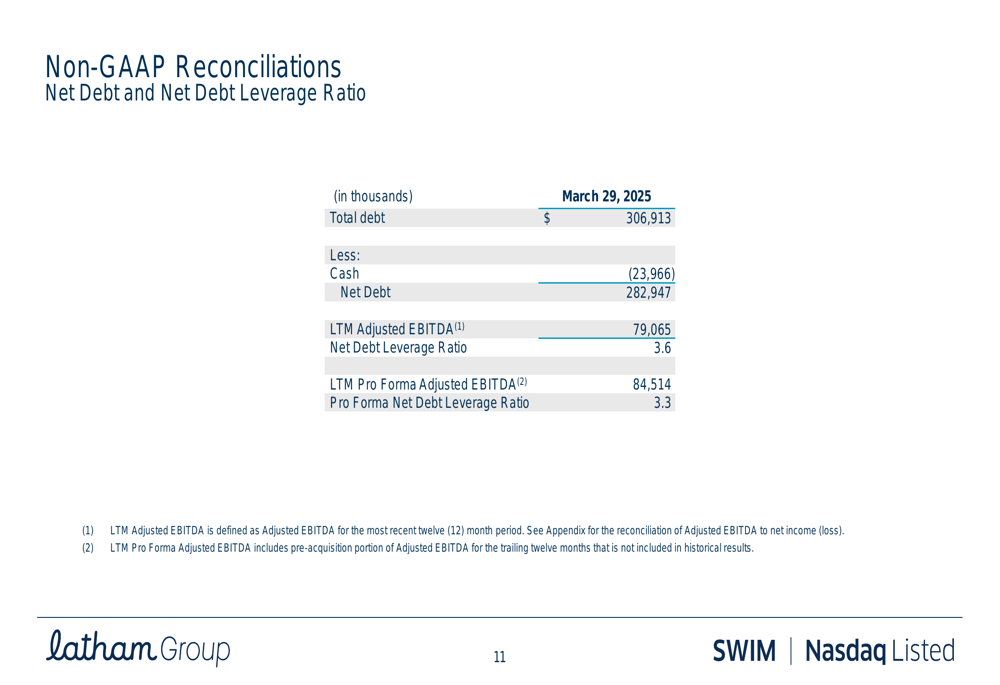

Financial Position and Debt Profile

As of March 29, 2025, Latham reported total debt of $306.91 million and cash of $23.97 million, resulting in net debt of $282.95 million. The company’s net debt leverage ratio stood at 3.6x based on last twelve months (LTM) Adjusted EBITDA of $79.07 million, or 3.3x on a pro forma basis.

The following slide details the company’s debt position:

While this leverage ratio remains somewhat elevated, it represents an improvement from previous quarters. The company’s projected EBITDA growth for 2025 should help further reduce this ratio if debt levels remain stable.

Market Reaction and Outlook

Despite the optimistic presentation, Latham’s stock has shown volatility. According to available data, the stock closed at $5.97 on May 6, 2025, and declined 2.68% in after-hours trading to $5.81. This follows a period of significant movement after the company’s Q4 2024 results, when the stock surged 18.32% despite an earnings miss.

Latham’s strategic focus on expanding fiberglass pool market share, particularly in the high-growth Sand States, positions the company to potentially outperform the broader market despite challenging conditions. However, investors appear to be taking a cautious approach, balancing the company’s growth initiatives against the reality of a pool market that remains well below historical averages.

As the company executes on its strategy throughout 2025, key metrics to watch will include its success in the Sand States expansion, the growth of its automatic safety cover business, and its ability to maintain or improve margins through operational efficiencies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.