EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

Laureate Education Inc (NASDAQ:LAUR) released its first quarter 2025 earnings presentation on May 1, revealing mixed financial results but an improved outlook for the full year. The company, which operates leading private universities in Mexico and Peru, reported significant revenue and EBITDA declines in Q1 but attributed these largely to academic calendar timing shifts rather than underlying business weakness.

Shares of Laureate were trading at $20.07 as of April 30, down 1.42% from the previous close but still near the upper end of its 52-week range of $13.26 to $21.73.

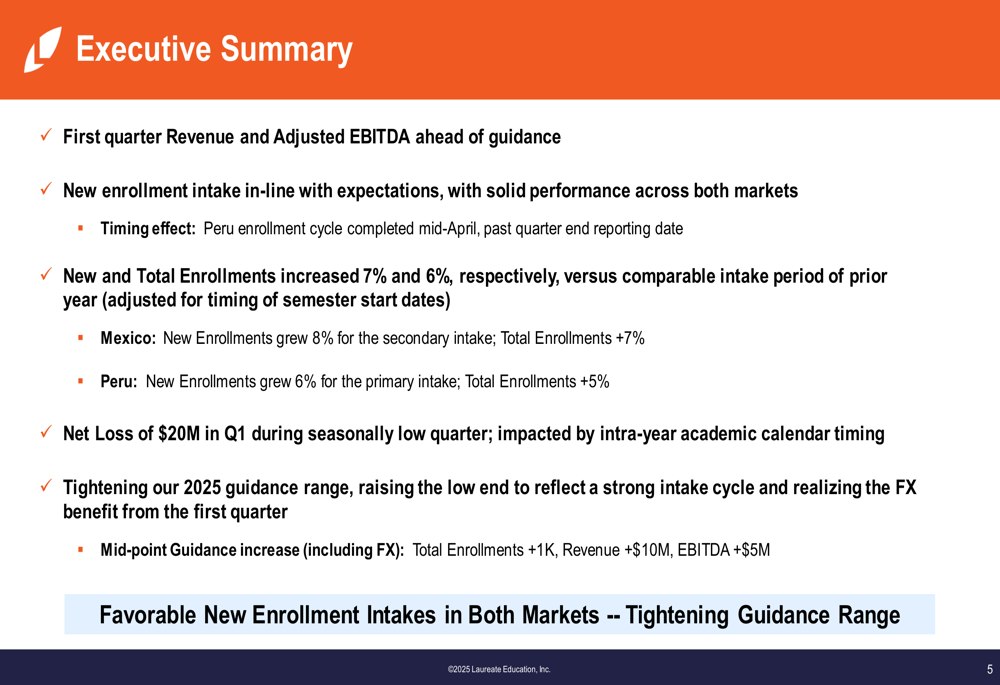

Executive Summary

Laureate reported Q1 2025 revenue of $236 million, down 14% as reported and 1% on an organic constant currency basis compared to the same period last year. Adjusted EBITDA fell more sharply to $5 million, representing an 82% decrease as reported and 45% on an organic constant currency basis. The company posted a net loss of $20 million for the quarter.

Despite these declines, management emphasized that both revenue and adjusted EBITDA were ahead of guidance, with new enrollment intake in line with expectations. The company also highlighted that when adjusted for academic calendar timing effects, organic constant currency revenue would have grown 10% and adjusted EBITDA by 132%.

As shown in the following executive summary from the presentation:

Total (EPA:TTEF) enrollment reached 477,000 students, up 4% year-over-year, while new enrollments were 94,000, down 2% compared to the prior year’s intake period. The company noted that Peru’s enrollment cycle completed in mid-April, which fell outside the quarter-end reporting date, impacting the results.

Segment Performance

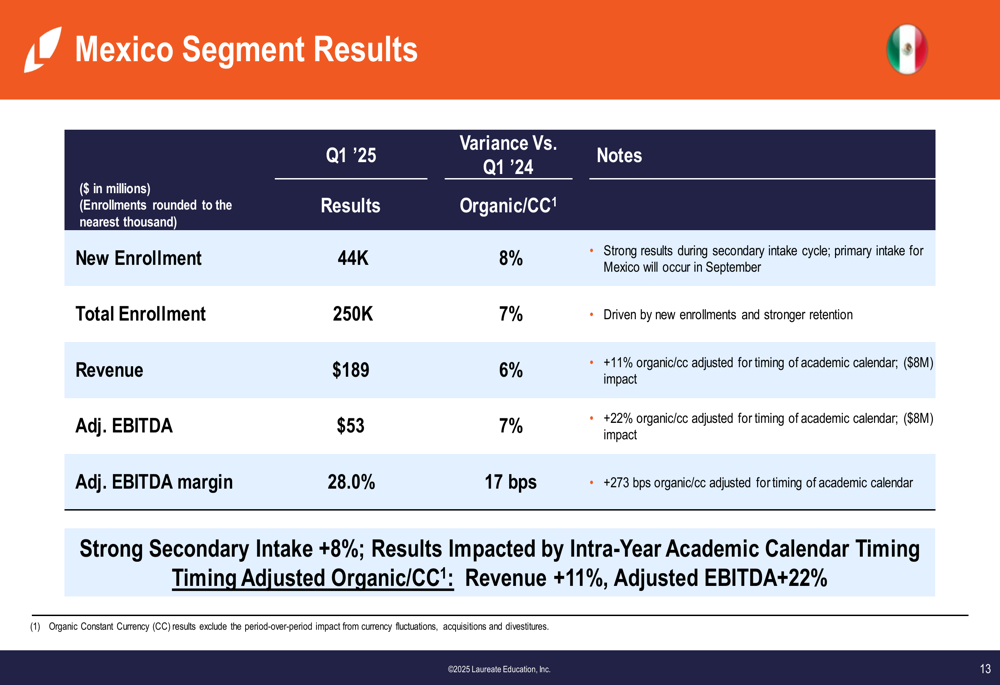

Laureate’s performance varied significantly between its two key markets. The Mexico segment showed strong results, with new enrollments up 8%, total enrollments up 7%, and revenue growth of 6% on an organic constant currency basis. Adjusted EBITDA for the Mexico segment reached $53 million, up 7% on an organic constant currency basis.

The following slide details Mexico’s performance:

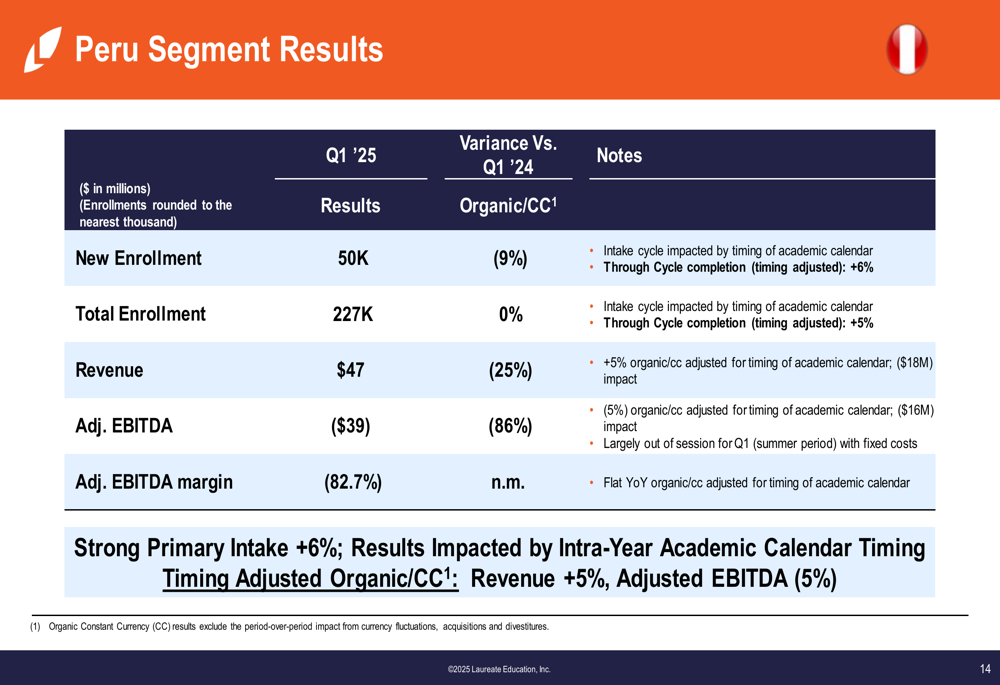

In contrast, Peru experienced challenges with new enrollments declining 9% and revenue dropping 25% on an organic constant currency basis. The segment reported a negative adjusted EBITDA of $39 million. However, management attributed much of this weakness to academic calendar timing, noting that the primary intake actually grew 6% when considering the full cycle that extended beyond the quarter end.

Peru’s segment results are illustrated here:

The company emphasized that intra-year academic calendar timing significantly impacted quarterly results, particularly in Peru. According to management, the timing shifts resulted in approximately $26 million of revenue moving out of Q1, with $18 million of that from Peru alone.

Market Position & Strategic Assets

Laureate continues to highlight its strong position in attractive education markets. The company serves a combined population of 162 million people across Mexico and Peru, with higher education gross participation rates of 36% in Mexico and 57% in Peru. Private institutions hold significant market share in both countries: 46% in Mexico and 76% in Peru.

The market opportunity is illustrated in this slide:

The company operates five major educational institutions across both countries, serving different market segments from premium/traditional to value/teaching and technical/vocational education. These institutions include Universidad del Valle de México (UVM) and Universidad Tecnológica de México (UNITEC) in Mexico, and Universidad Peruana de Ciencias Aplicadas (UPC), Universidad Privada del Norte (UPN), and CIBERTEC in Peru.

The following slide showcases Laureate’s institutional portfolio:

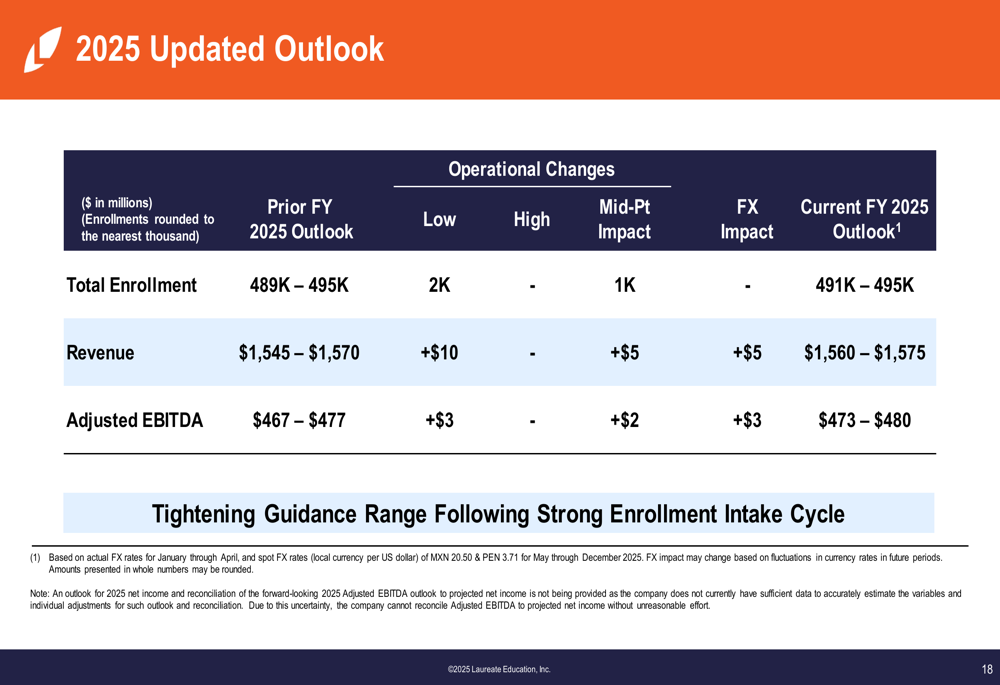

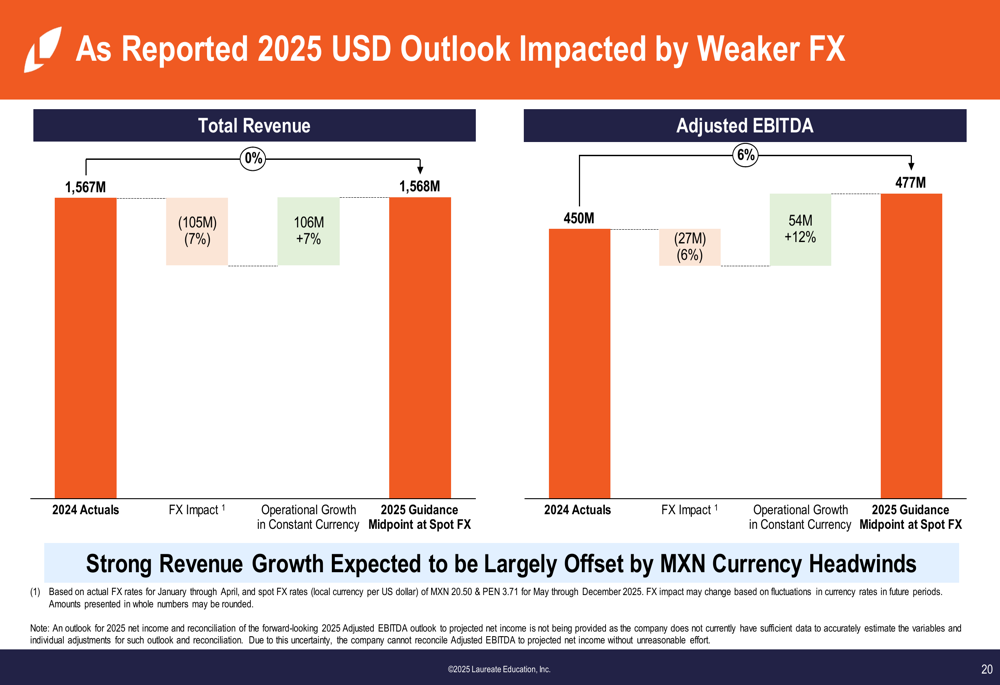

Updated Outlook & Guidance

Despite the mixed Q1 results, Laureate raised its full-year 2025 guidance. The company now expects:

- Total enrollment of 491,000-495,000 (up from 489,000-495,000 previously)

- Revenue of $1,560-$1,575 million (up from $1,545-$1,570 million)

- Adjusted EBITDA of $473-$480 million (up from $467-$477 million)

The updated guidance is detailed in this slide:

Management attributed the guidance increase to a strong intake cycle and favorable foreign exchange impacts from the first quarter. However, the company also noted that significant FX headwinds are anticipated for the remainder of 2025 due to the weakening Mexican Peso.

For the second quarter of 2025, Laureate expects revenue of $499-$504 million and adjusted EBITDA of $191-$194 million, based on April spot FX rates.

The following slide illustrates how FX impacts are affecting the 2025 outlook:

Financial Position & Capital Returns

Laureate maintains a strong balance sheet with gross debt of $115 million and cash and cash equivalents of $110 million, resulting in minimal net debt of $5 million as of March 31, 2025. The company continued its share repurchase program, buying back $42 million worth of shares in Q1 2025, with $56 million of authorization remaining.

The company highlighted its track record of returning capital to shareholders, noting that nearly $3 billion has been returned since the start of 2019 through share buybacks and cash distributions.

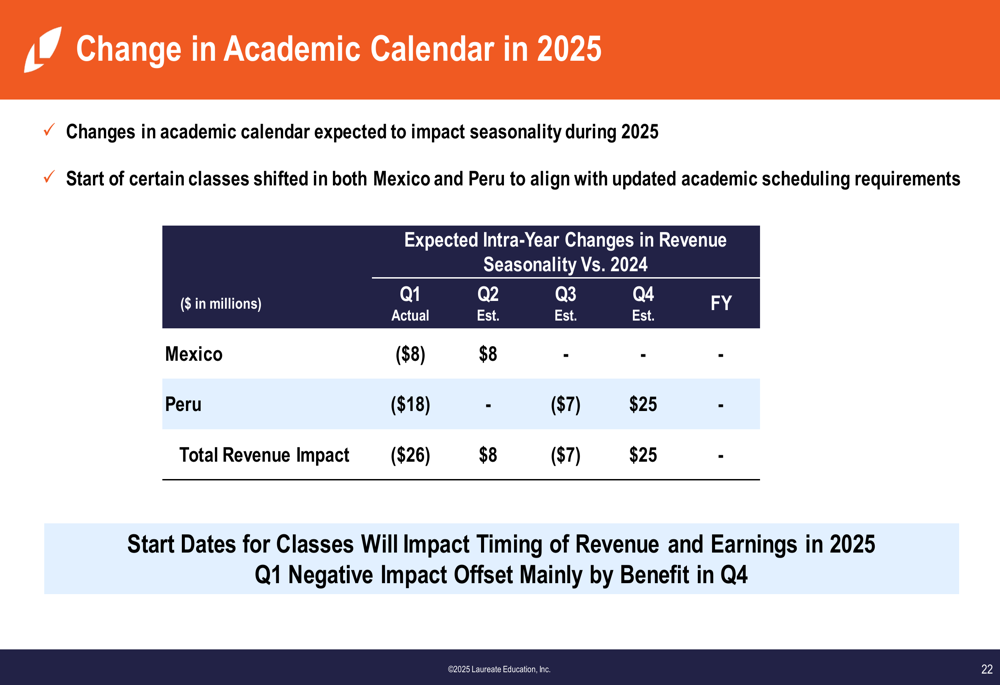

Academic Calendar Impact

A significant factor affecting Laureate’s quarterly results is the change in academic calendars in both Mexico and Peru. The company provided a detailed breakdown of how these changes are expected to impact revenue seasonality throughout 2025:

These timing shifts explain much of the apparent weakness in Q1 results, with revenue expected to shift between quarters but not affect the full-year outcome. The company expects these timing effects to normalize over the course of the year.

Forward-Looking Statements

Looking ahead, Laureate expects 2025 revenue growth of 0-1% versus 2024 on a USD reported basis, but 6-7% on an organic constant currency basis. Adjusted EBITDA is projected to grow 5-7% on a USD reported basis and 11-13% on an organic constant currency basis. The company anticipates adjusted EBITDA margin accretion of approximately 1.5 percentage points, driven by Mexico’s continued margin optimization and operating leverage from revenue growth.

Management remains confident in the company’s ability to generate strong cash flow, projecting adjusted EBITDA to unlevered free cash flow conversion of approximately 50% for 2025.

While Laureate faces challenges from foreign exchange headwinds and timing shifts, the underlying business appears to be performing in line with management’s expectations, particularly in the crucial Mexico market which continues to show strong enrollment growth and margin expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.