Street Calls of the Week

Introduction & Market Context

Laurentian Bank of Canada (TSX:LB) presented its third-quarter 2025 financial results on August 29, 2025, revealing a mixed performance with some positive indicators alongside ongoing challenges. The bank’s stock closed at $31.68 on August 28, 2025, representing a modest gain of 0.6% or $0.19, and remains near its 52-week high of $31.74.

The Q3 results come after a challenging second quarter where the bank missed analyst expectations but still saw its stock price rise nearly 6% on investor optimism about its strategic direction. The third-quarter presentation demonstrates the bank’s continued focus on strengthening its capital position while navigating revenue pressures.

Quarterly Performance Highlights

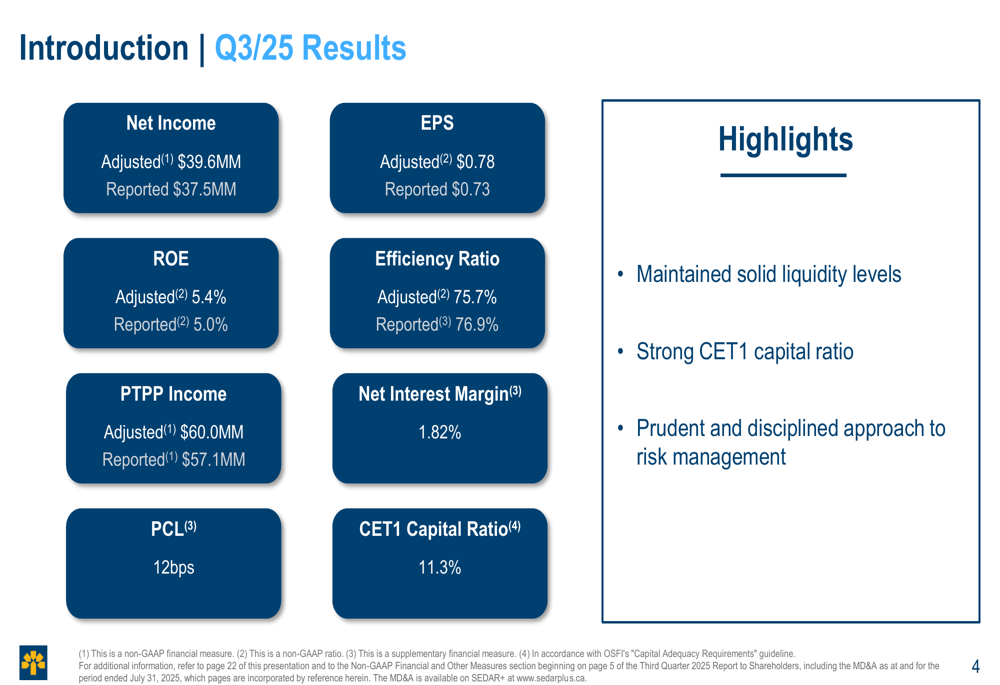

Laurentian Bank reported adjusted net income of $39.6 million for Q3 2025, with adjusted earnings per share of $0.78. On a reported basis, net income was $37.5 million with EPS of $0.73. The bank’s adjusted return on equity stood at 5.4%, while its reported ROE was 5.0%.

As shown in the following summary of key Q3 2025 metrics:

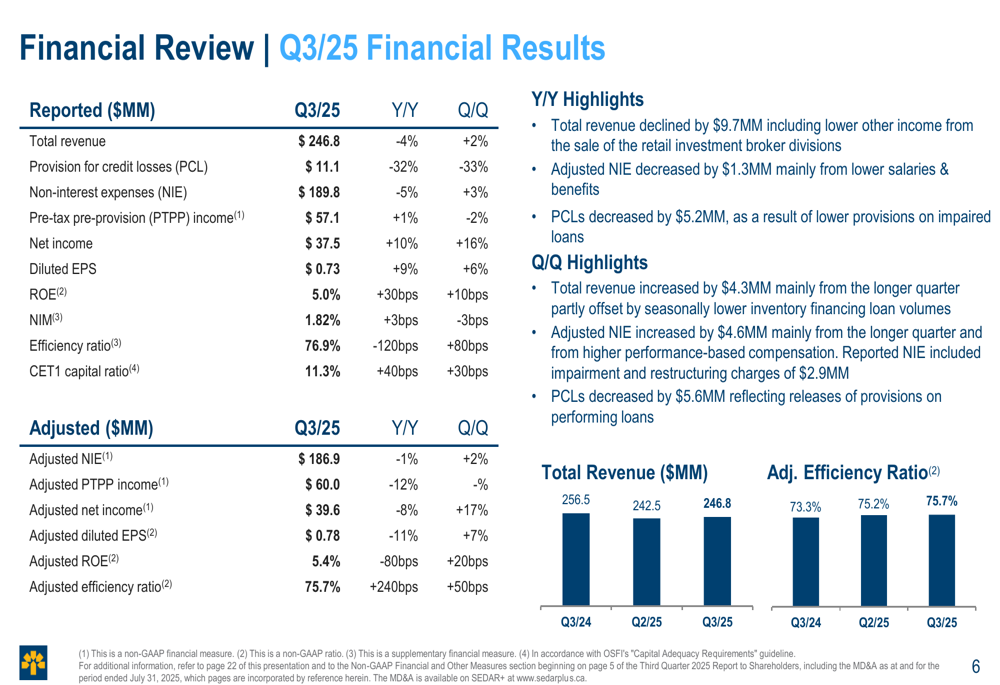

Total revenue for the quarter was $246.8 million, representing a 4% decrease year-over-year but a 2% increase compared to the previous quarter. The bank’s efficiency ratio, a key measure of operational effectiveness, was 76.9% on a reported basis and 75.7% on an adjusted basis, indicating ongoing challenges in cost management.

The detailed financial results reveal mixed performance across various metrics:

Detailed Financial Analysis

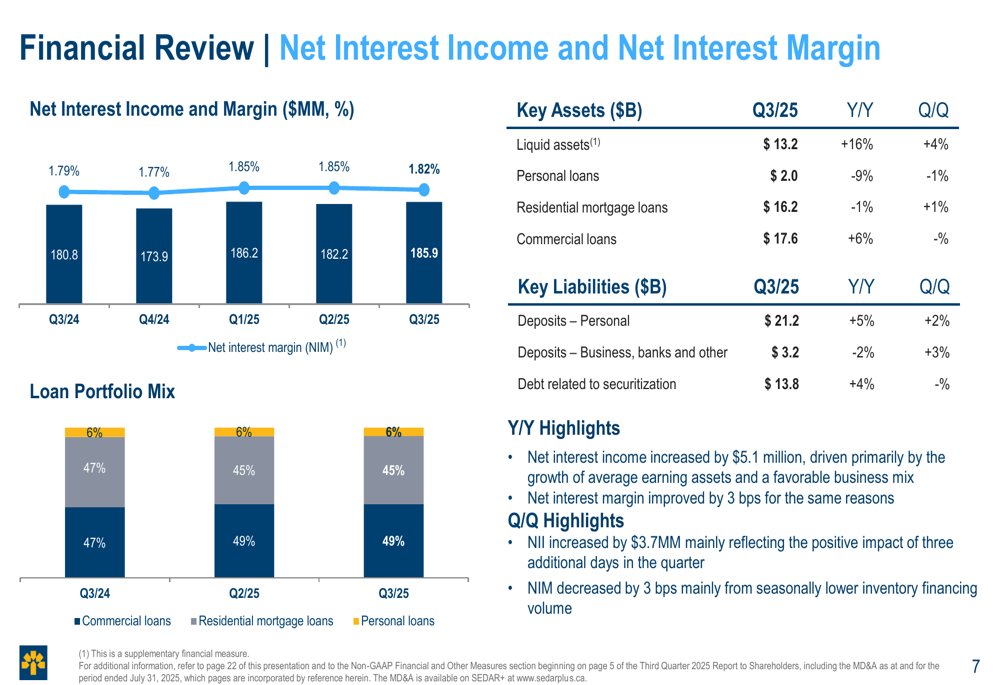

Net interest income, a crucial revenue driver for the bank, increased to $185.9 million in Q3 2025, up from $180.8 million in the same quarter last year. The net interest margin improved slightly to 1.82%, up 3 basis points year-over-year, though it decreased by 3 basis points compared to the previous quarter.

The following chart illustrates the trend in net interest income and margin:

Other income, however, showed significant weakness, declining by 20% year-over-year to $60.9 million. This decrease was primarily driven by lower fees and securities brokerage commissions following the sale of the retail investment broker divisions in the prior fiscal year, as well as reduced income from financial instruments and lower lending fees.

Non-interest expenses decreased by 5% year-over-year to $189.8 million, largely due to lower impairment and restructuring charges compared to the prior year. On an adjusted basis, non-interest expenses decreased by 1% year-over-year to $186.9 million.

Capital Position and Risk Management

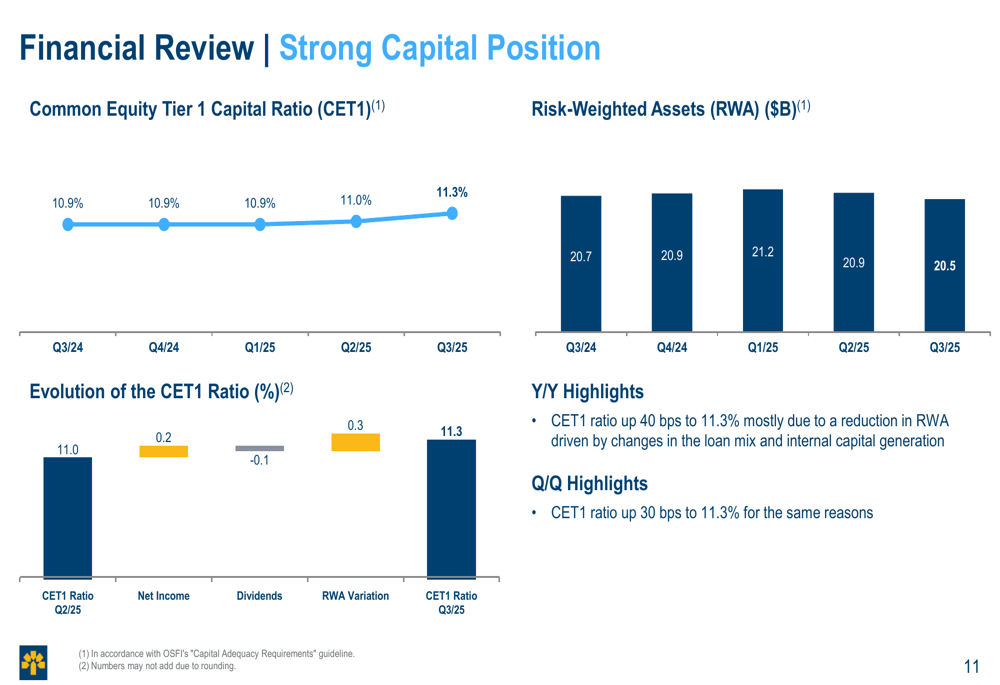

A notable strength in Laurentian Bank’s Q3 results was its robust capital position. The Common Equity Tier 1 (CET1) capital ratio improved to 11.3%, up 40 basis points from the previous year and 30 basis points from the previous quarter. This improvement was primarily driven by a reduction in risk-weighted assets and internal capital generation.

The following chart demonstrates the bank’s strengthening capital position:

The bank’s provision for credit losses (PCL) decreased by 32% year-over-year to $11.1 million, representing 12 basis points of average loans and acceptances. This reduction was mainly due to lower provisions on impaired loans.

However, there are some concerning trends in the bank’s credit quality. Gross impaired loans increased by $41.9 million, primarily due to credit migration in commercial loans. Net impaired loans also rose by $55.2 million compared to the previous year.

Strategic Initiatives & Portfolio Composition

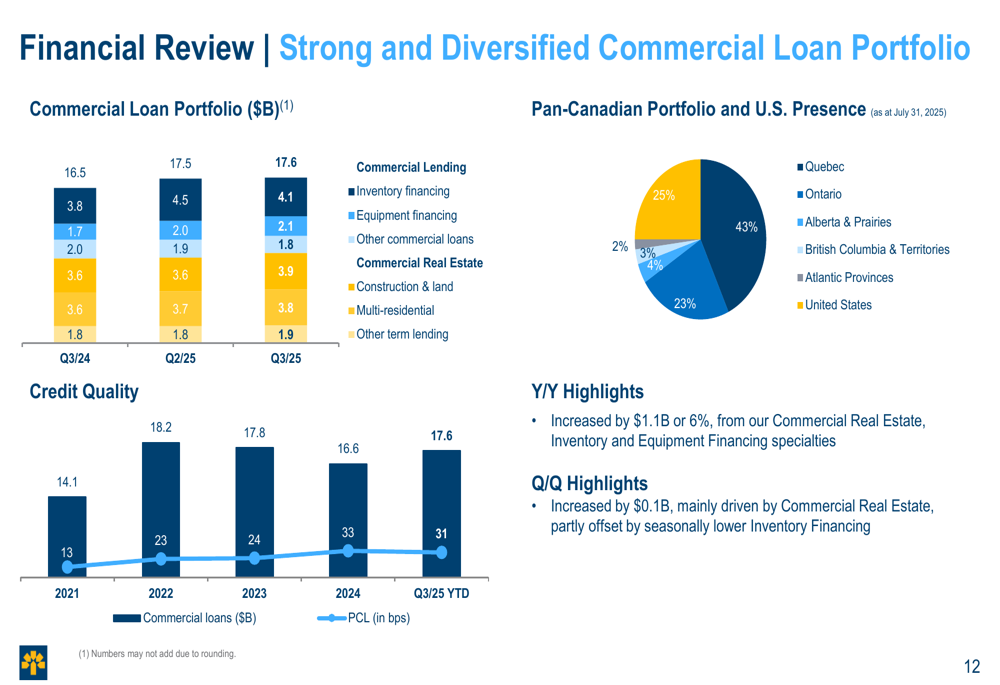

Laurentian Bank continues to focus on growing its commercial loan portfolio, which increased by 6% year-over-year to $17.6 billion. This growth was primarily driven by the bank’s commercial real estate, inventory financing, and equipment financing specialties.

The following chart provides a breakdown of the commercial loan portfolio:

The bank’s inventory financing business represents a key strategic focus, with a portfolio of $4.1 billion serving over 6,500 dealers across the United States and Canada. This diversified portfolio spans multiple sectors including power sports (35%), manufactured housing (17%), marine (13%), and recreational vehicles (7%).

Laurentian Bank’s commercial real estate portfolio also shows strong diversification, with over 67% concentrated in residential properties (57% multi-residential and 10% condos). This focus on residential real estate helps mitigate risk in the commercial property segment.

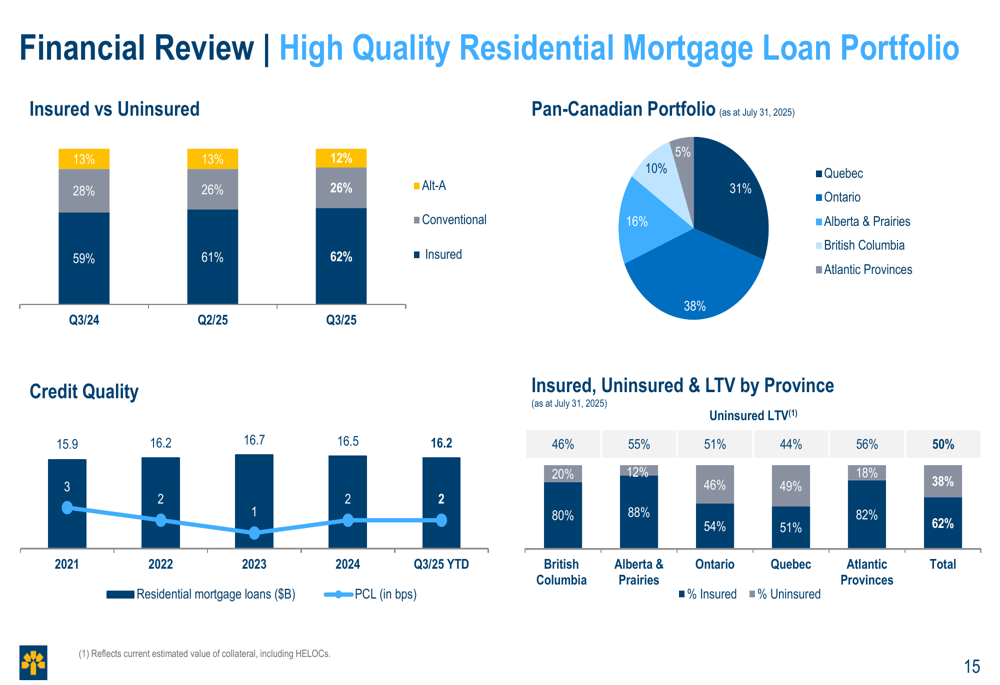

The residential mortgage loan portfolio, valued at $16.2 billion, remains high-quality with 62% of loans insured and a conservative loan-to-value ratio of 50% for uninsured mortgages. The geographic distribution of this portfolio is well-diversified across Canada:

Forward-Looking Statements

While the presentation doesn’t provide explicit forward guidance, Laurentian Bank’s focus on maintaining strong capital and liquidity positions suggests a continued conservative approach to growth and risk management. The bank’s emphasis on commercial lending specialties, particularly inventory financing and commercial real estate, indicates these will remain strategic priorities.

The declining trend in the efficiency ratio (higher is worse) presents an ongoing challenge that management will need to address. At 75.7% on an adjusted basis, this metric has deteriorated by 240 basis points year-over-year, suggesting pressure on operational efficiency.

The bank’s funding structure shows increased reliance on deposits from advisors and brokers, which grew year-over-year, while partnership deposits declined as customers reallocated funds to market activities. This shift in funding sources may impact the bank’s cost of funds going forward.

In conclusion, Laurentian Bank’s Q3 2025 results demonstrate resilience in its capital position and commercial lending business, but challenges remain in improving operational efficiency and managing the quality of the loan portfolio. Investors will be watching closely to see if the bank can leverage its strong capital position to drive improved performance in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.