Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

L.B. Foster Company (NASDAQ:FSTR) reported a challenging first quarter for 2025, with significant revenue and profit declines, but pointed to encouraging signs of recovery in its May 6 earnings presentation. The infrastructure and rail solutions provider saw its stock trading at $20.20 in pre-market, down 1.37% following the results, adding to a 0.53% decline from the previous session.

The Pittsburgh-based company, which has been operating since 1902, highlighted that its weak Q1 performance was primarily due to softness in its Rail Distribution business, while its Infrastructure segment showed positive growth. Management emphasized that the results align with typical seasonal patterns, with stronger performance expected in the second and third quarters.

Quarterly Performance Highlights

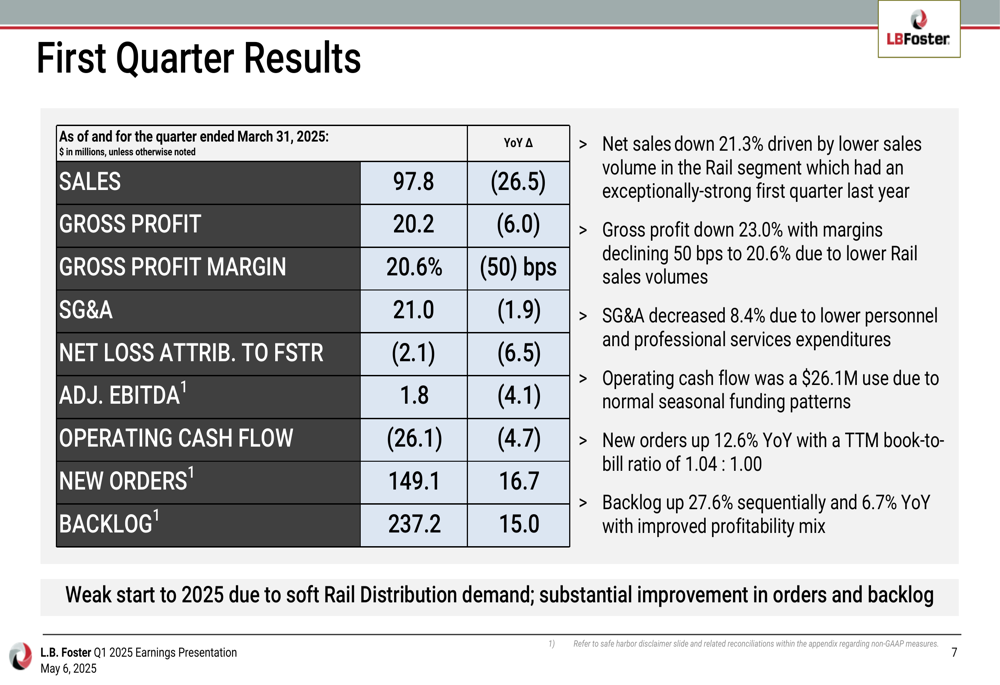

L.B. Foster reported net sales of $97.8 million for Q1 2025, a 21.3% decrease compared to the same period last year. Gross profit fell by 23.0% to $20.2 million, with gross margins contracting slightly to 20.6%, down 50 basis points year-over-year. The company recorded a net loss, which deteriorated by 148.1% compared to Q1 2024, while Adjusted EBITDA declined by 69.3% to $1.8 million.

As shown in the following chart of quarterly financial results:

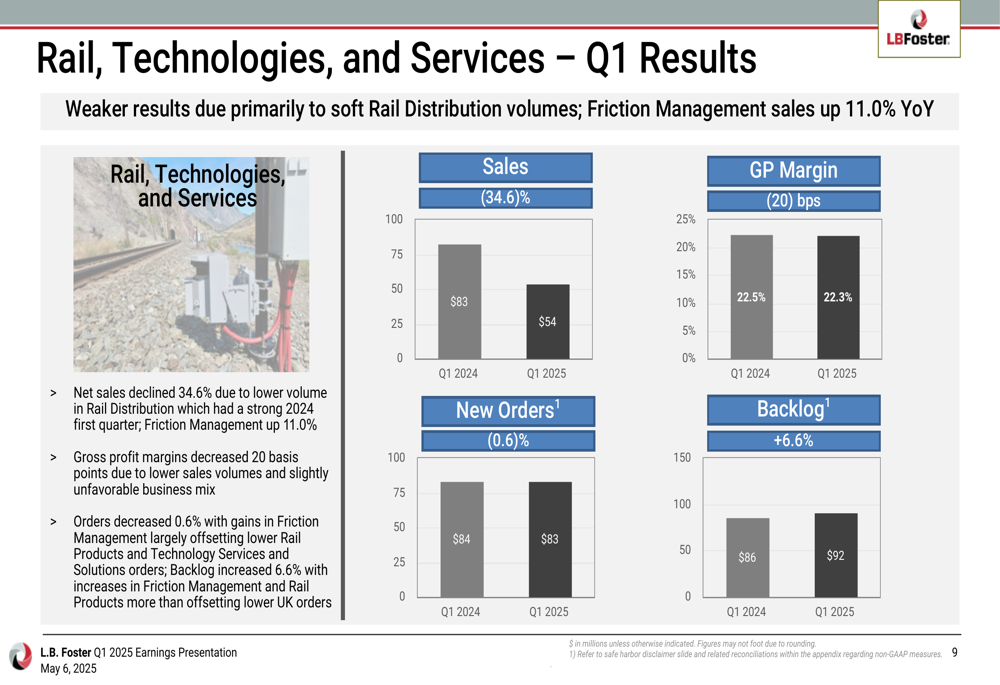

The company’s performance diverged significantly between its two main segments. The Rail, Technologies, and Services segment experienced a 34.6% decline in sales to $54 million, with gross profit margin decreasing slightly to 22.3%. This weakness was attributed primarily to soft Rail Distribution volumes, though the company noted that Friction Management sales increased by 11.0% year-over-year.

The segment breakdown is illustrated in this chart:

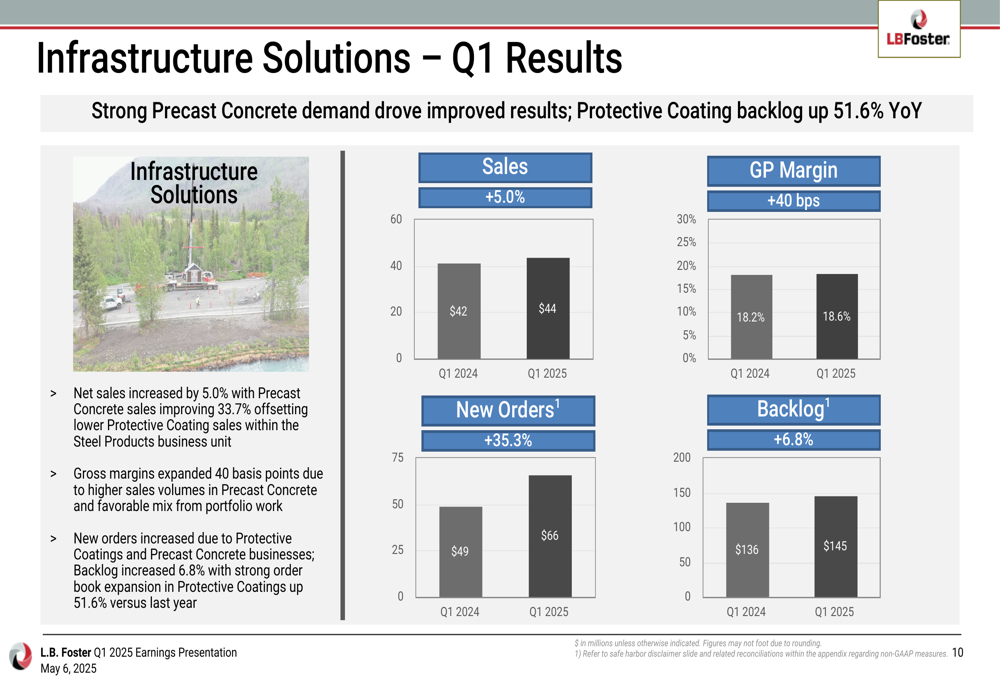

In contrast, the Infrastructure Solutions segment showed positive momentum with a 5.0% increase in sales to $44 million and a 40 basis point improvement in gross profit margin to 18.6%. Management highlighted strong demand for Precast Concrete products as a key driver of the improved results.

The Infrastructure segment’s performance is detailed in this chart:

Detailed Financial Analysis

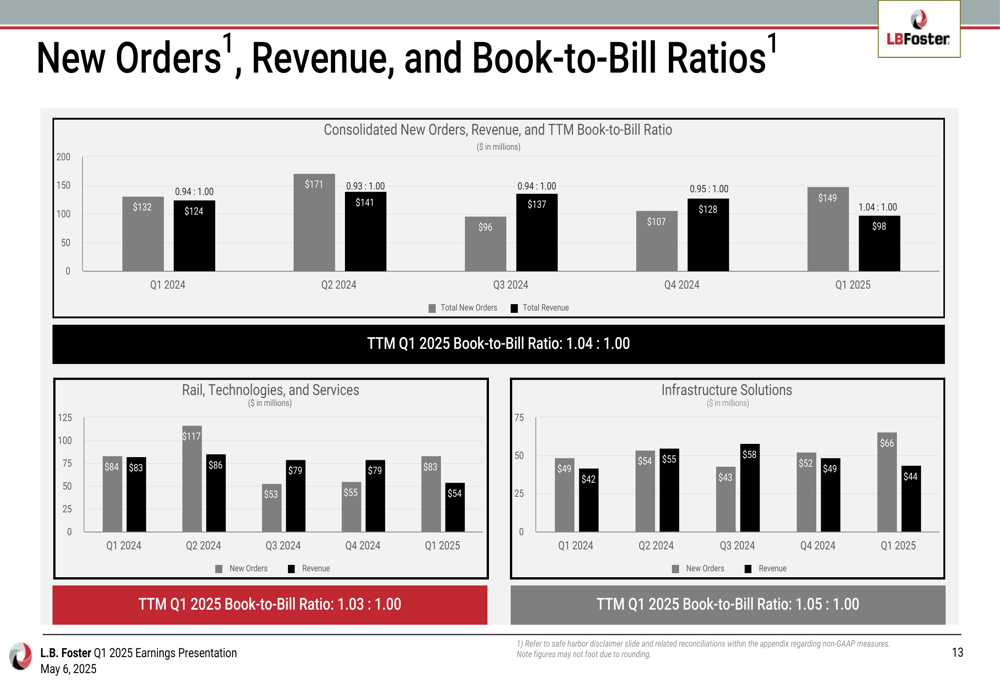

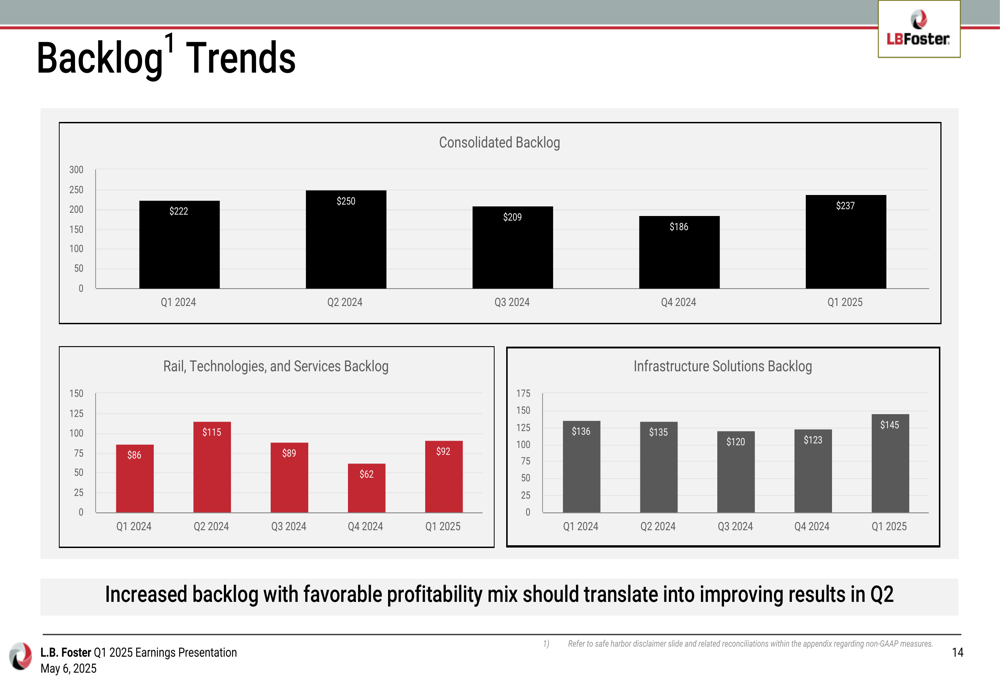

Despite the weak quarterly results, L.B. Foster reported several encouraging financial indicators. New orders reached $149.1 million, up 12.6% year-over-year and 39.1% sequentially. The company’s backlog grew to $237.2 million, representing increases of 6.7% year-over-year and 27.6% from the previous quarter. The trailing twelve-month book-to-bill ratio improved to 1.04:1.00, suggesting future revenue growth potential.

The company’s order and backlog trends are visualized in these charts:

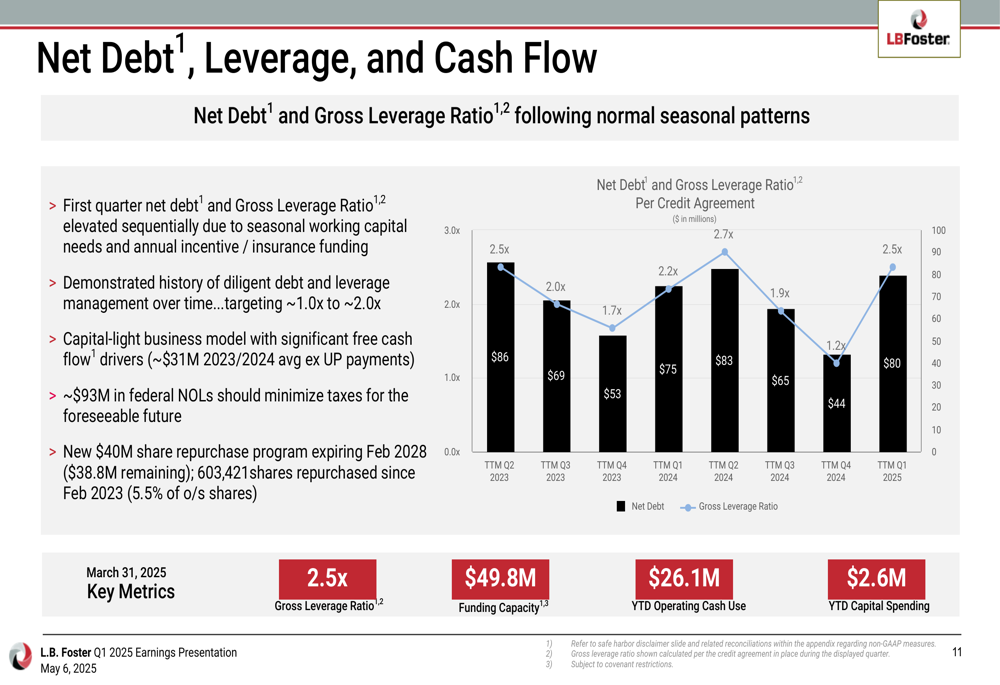

L.B. Foster’s net debt increased by $4.9 million year-over-year to $79.9 million, with a Gross Leverage Ratio of 2.5x, up 0.3x from the previous year. Management explained that the first quarter typically sees elevated debt levels due to seasonal working capital needs and annual incentive and insurance funding. The company targets a leverage ratio between 1.0x and 2.0x.

The following chart illustrates the company’s debt and leverage trends:

Strategic Initiatives

L.B. Foster outlined its capital allocation priorities, balancing debt reduction, shareholder returns, and growth investments. During Q1, the company repurchased 168,911 shares of common stock for $4.3 million, representing approximately 1.5% of outstanding shares. A new $40 million share repurchase program has been authorized through February 2028.

The company highlighted its capital-light business model, targeting capital expenditures at approximately 2.0% of sales for maintenance and organic growth initiatives. Management also noted that approximately $93 million in federal net operating loss carryforwards (NOLs) should minimize taxes for the foreseeable future.

On the growth front, L.B. Foster commissioned a new facility in Florida during Q1 to produce Envirocast® modular wall systems for commercial and residential real estate markets. The company also reported renewed interest in domestic energy production, which has translated into a strong order book for its Protective Coatings business, with backlog up 51.6% year-over-year.

Forward-Looking Statements

Despite the weak first quarter, L.B. Foster reaffirmed its full-year 2025 guidance, projecting:

- Net sales of $540-$580 million

- Adjusted EBITDA of $42-$48 million

- Free cash flow of $20-$30 million

- Capital expenditures of approximately 2.0% of sales

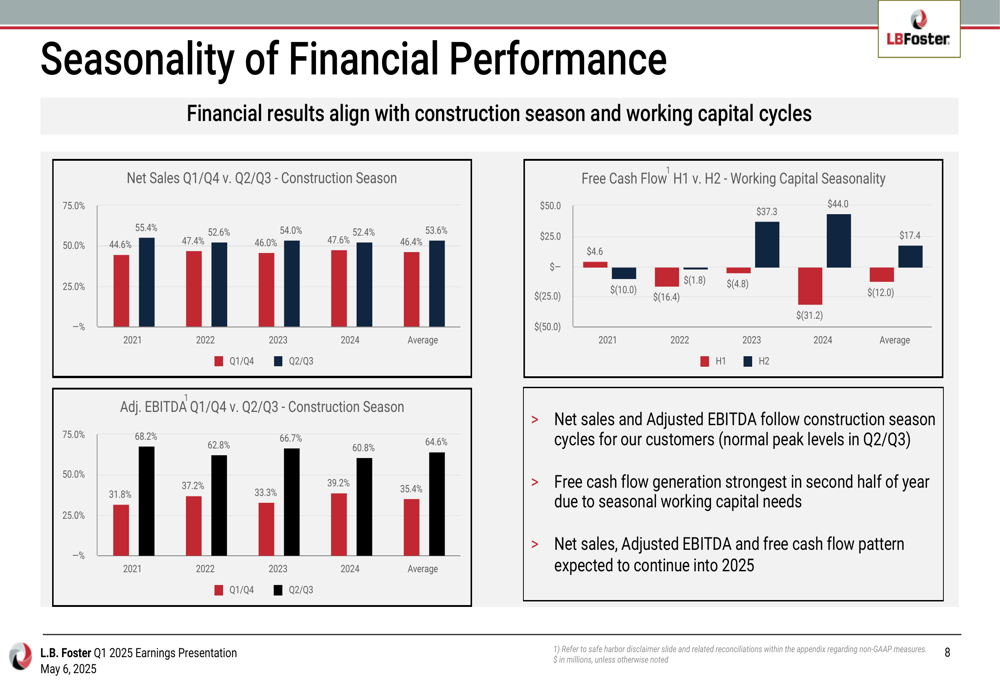

Management expressed confidence that the strong order book should translate to sales growth and profitability expansion as early as the second quarter. The company emphasized its historical seasonality pattern, with net sales and adjusted EBITDA typically stronger in Q2/Q3 (construction season) compared to Q1/Q4, and free cash flow generation stronger in the second half of the year.

This seasonal pattern is illustrated in the following chart:

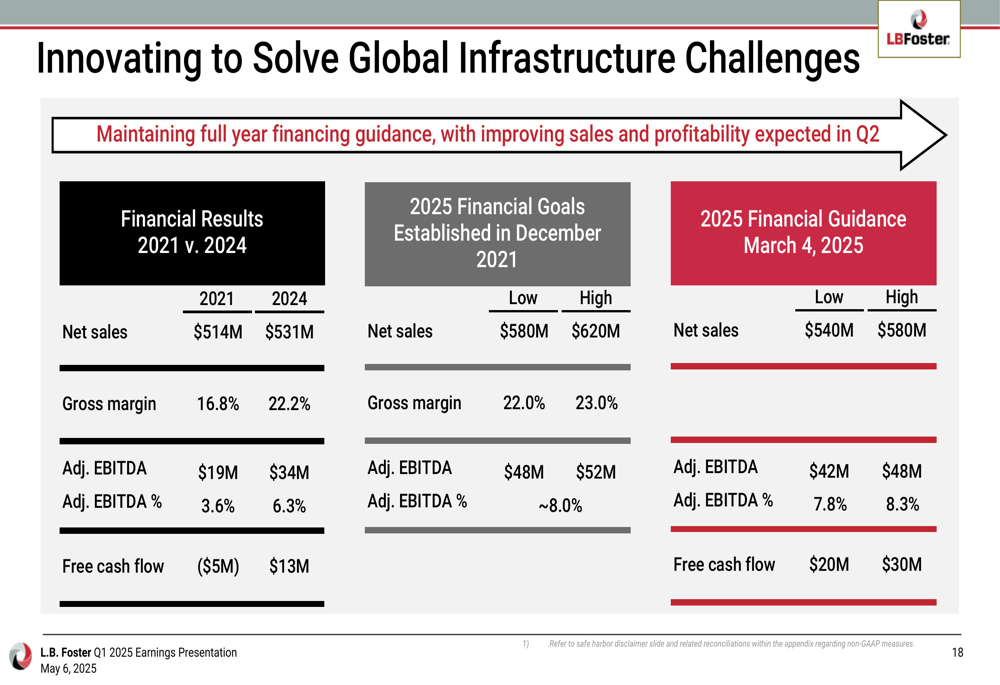

Looking at longer-term trends, L.B. Foster highlighted the progress made since 2021, with improvements in net sales, gross margin, adjusted EBITDA, and free cash flow. The company’s 2025 guidance represents significant growth from 2021 levels, though slightly below the financial goals established in December 2021.

The company’s financial progress and outlook are summarized in this chart:

L.B. Foster’s management emphasized that government funding for large-scale investments in freight rail, transit lines, and civil infrastructure is expected to remain largely intact given ongoing needs. The company also noted continuing focus on and funding of rail safety initiatives, which supports long-term growth for its Rail Technologies offerings.

As the company navigates through 2025, investors will be watching closely to see if the anticipated recovery materializes in the second quarter and whether L.B. Foster can achieve its full-year guidance despite the weak start to the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.