One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

L.B. Foster Company (NASDAQ:FSTR) presented its second quarter 2025 earnings on August 11, showing a significant recovery from its disappointing first quarter performance. The infrastructure solutions provider, which saw its stock drop nearly 11% following its Q1 earnings miss, delivered substantial improvement in profitability metrics despite mixed segment results.

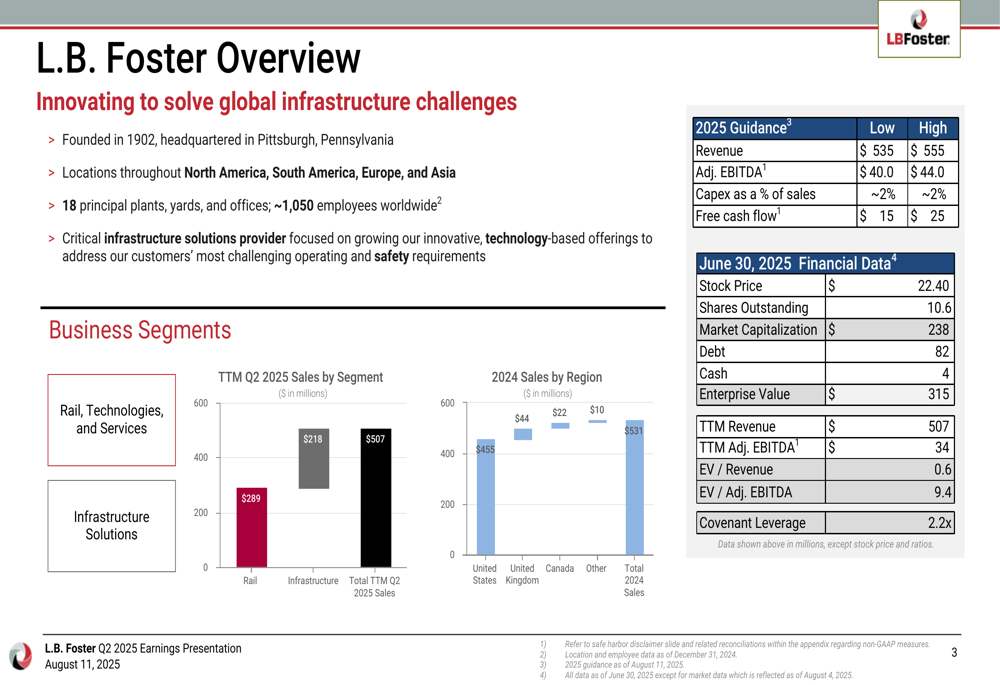

The company’s Q2 presentation highlighted its strategic positioning as a critical infrastructure solutions provider, with operations spanning North America, South America, Europe, and Asia. With approximately 1,050 employees worldwide and 18 principal facilities, L.B. Foster continues to focus on innovative, technology-based solutions for infrastructure challenges.

As shown in the following overview of the company’s key financial data:

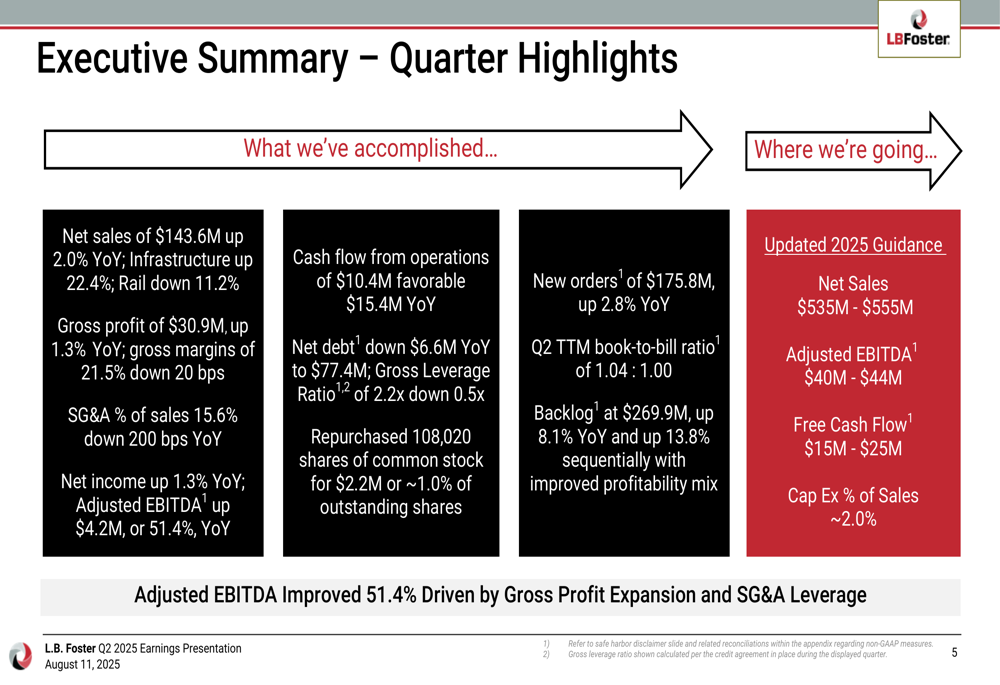

Executive Summary

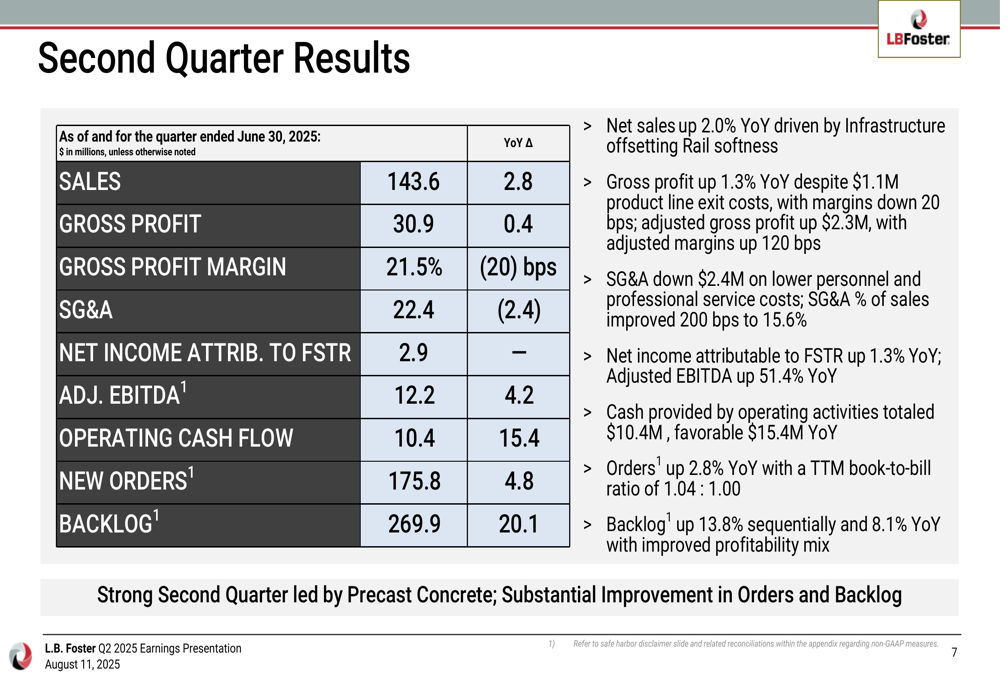

L.B. Foster reported Q2 2025 net sales of $143.6 million, up 2.0% year-over-year, with gross profit increasing 1.3% to $30.9 million. The most notable improvement came in Adjusted EBITDA, which surged 51.4% to $12.2 million compared to the same period last year.

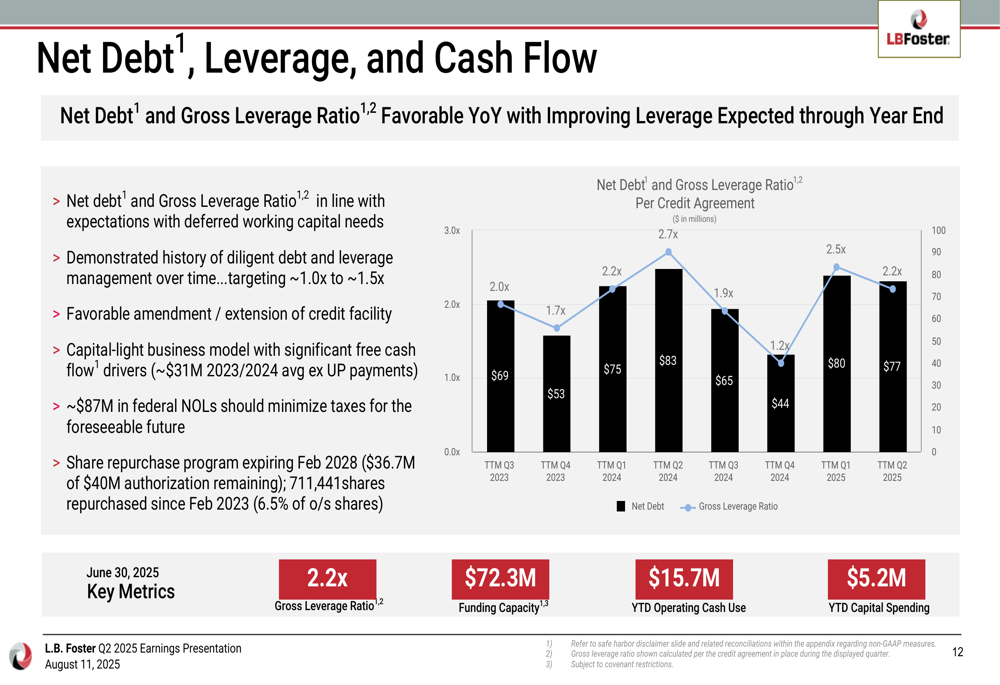

The company’s cash flow from operations showed remarkable improvement at $10.4 million, representing a $15.4 million favorable change year-over-year. Net debt decreased by $6.6 million to $77.4 million, with the gross leverage ratio improving to 2.2x from 2.7x in the prior year.

These results mark a substantial turnaround from Q1 2025, when the company reported an EPS of -0.2 against a forecast of 0.12, with revenue falling short at $97.79 million compared to the expected $109.24 million.

The executive summary highlights the company’s key quarterly achievements:

Quarterly Performance Highlights

L.B. Foster’s second quarter results showed notable improvement across several key financial metrics. Net income attributable to the company increased 1.3% year-over-year to $2.9 million, with diluted earnings per share rising 3.8% to $0.27. SG&A expenses as a percentage of sales improved by 200 basis points year-over-year.

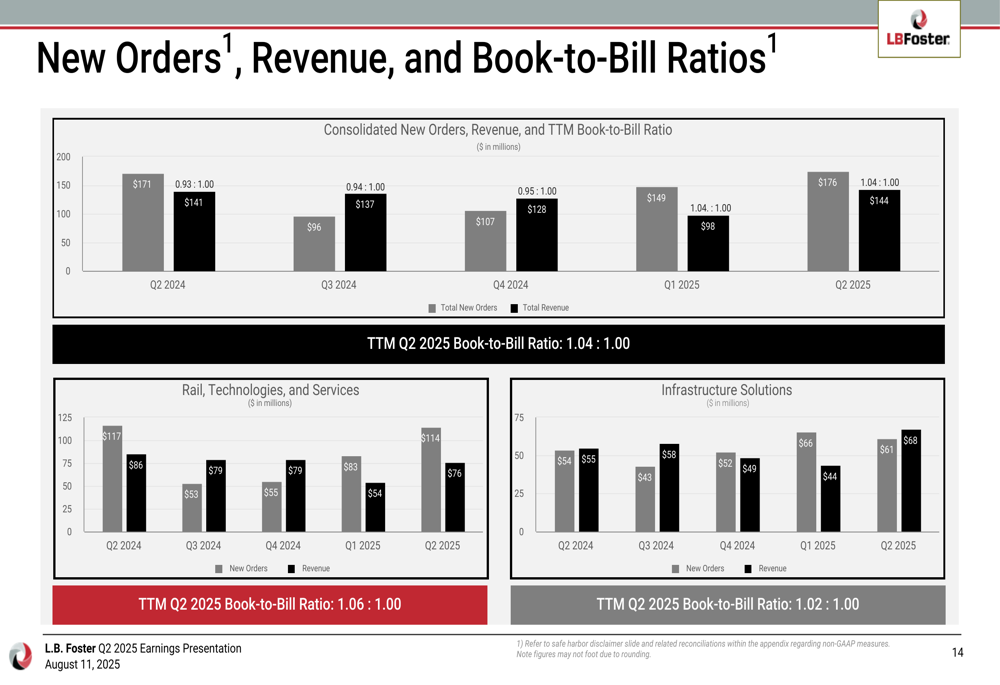

The company also reported strong order intake, with new orders of $175.8 million representing a 2.8% increase from Q2 2024. This contributed to a backlog of $269.9 million, up 8.1% year-over-year and 13.8% sequentially, indicating potential for continued growth in the coming quarters.

The detailed quarterly results are presented in the following slide:

Segment Analysis

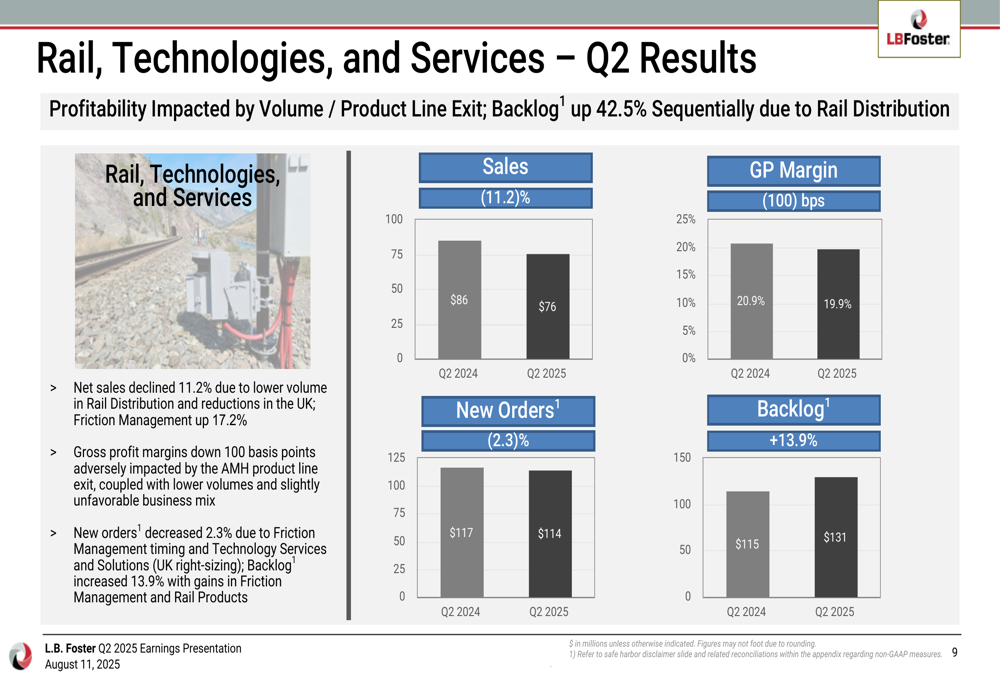

L.B. Foster’s performance showed significant divergence between its two main business segments. The Rail, Technologies, and Services segment experienced an 11.2% decline in net sales to $76 million, with gross profit margins contracting by 100 basis points to 19.9%. This decline was attributed to lower volume in Rail Distribution and reductions in the UK market.

As shown in the following segment breakdown:

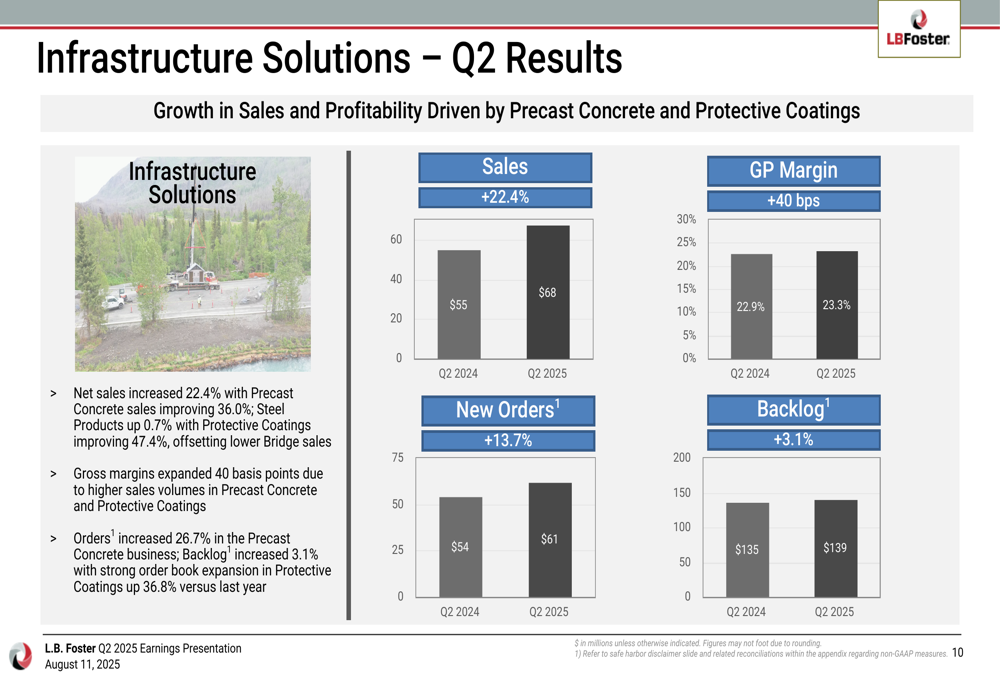

In contrast, the Infrastructure Solutions segment delivered robust growth, with net sales increasing 22.4% to $68 million. This growth was driven by a 36.0% improvement in Precast Concrete sales and a 47.4% increase in Protective Coatings. Gross margins in this segment expanded by 40 basis points to 23.3%.

The Infrastructure segment’s strong performance is detailed in this slide:

Management noted that renewed interest in domestic energy production has translated into a strong order book for Protective Coatings, while the company’s new Precast facility in Florida delivered its first order in Q2. Government funding for large-scale infrastructure investments also improved during the quarter, benefiting the Infrastructure Solutions segment.

Financial Position and Outlook

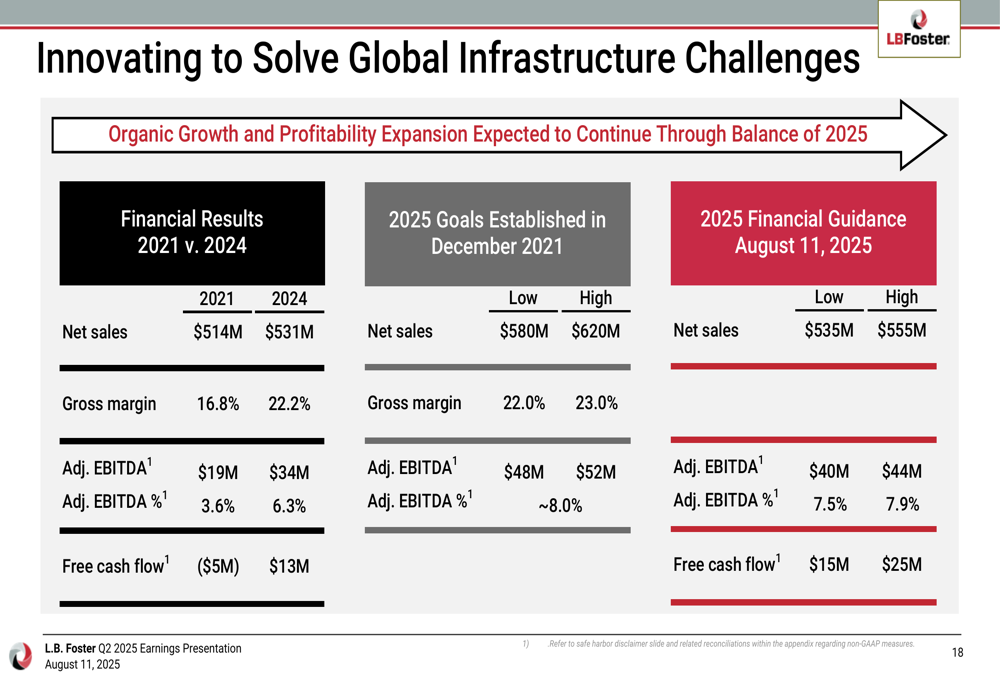

Despite the strong Q2 performance, L.B. Foster’s year-to-date results still reflect challenges, with net income for the first six months of 2025 at $0.8 million, down 89.4% from $7.3 million in the same period of 2024. However, the company has maintained its 2025 financial guidance, projecting net sales of $535-555 million, Adjusted EBITDA of $40-44 million, and free cash flow of $15-25 million.

The company’s debt management and leverage position have improved, as illustrated in the following chart:

L.B. Foster’s capital allocation priorities remain focused on debt reduction, targeting a gross leverage ratio between 1.0x and 1.5x. The company is also allocating approximately 2.0% of sales for maintenance and organic growth capital expenditures, while continuing its share repurchase program and evaluating strategic tuck-in acquisitions.

The company’s progress toward its 2025 financial goals is shown in this comparative analysis:

Strategic Initiatives

Looking ahead, L.B. Foster is focusing on several strategic initiatives to drive growth. The company highlighted that government funding of large-scale investments in infrastructure improved in the second quarter, which should benefit its Infrastructure Solutions segment. Additionally, continuing focus on and funding of railroad customer safety and operating ratio initiatives is expected to support long-term growth for Rail Technologies.

The company’s new orders and backlog trends indicate potential for continued growth, with a book-to-bill ratio of 1.04:1.00 for the trailing twelve months ending Q2 2025. The following chart illustrates the company’s order trends:

Management noted that sales and adjusted EBITDA follow construction season cycles, with peak levels typically occurring in Q2 and Q3. Free cash flow generation is expected to be strongest in the second half of the year due to seasonal working capital needs, a pattern that is anticipated to continue in 2025.

L.B. Foster’s CEO John Kasel expressed optimism about the company’s trajectory, emphasizing the strong performance in precast concrete and the substantial improvement in orders and backlog. The company appears well-positioned to capitalize on infrastructure spending and energy sector growth, though challenges remain in the Rail segment that will require continued attention.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.