Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

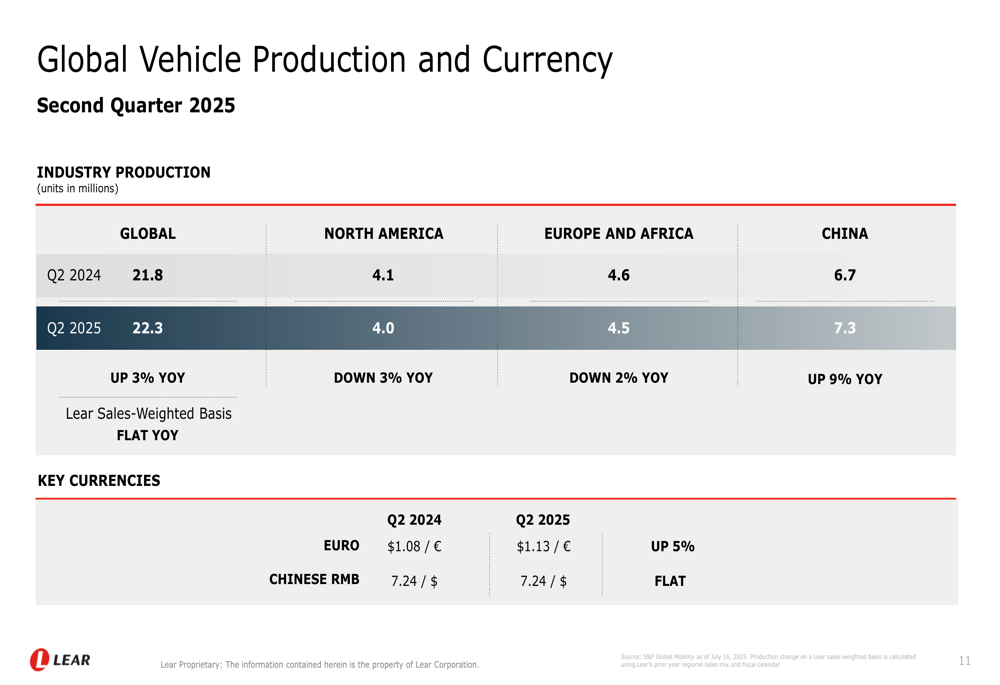

Lear Corporation (NYSE:LEA), a leading global automotive technology company specializing in seating and electrical systems, presented its second quarter 2025 financial results on July 25, 2025. The company maintained stable performance despite facing production challenges in key markets, with global vehicle production on a Lear sales-weighted basis remaining flat year-over-year.

While global production increased by 3% compared to Q2 2024, North America and Europe experienced declines of 3% and 2% respectively. China was the bright spot with a 9% increase in production volumes. These regional variations created a challenging operating environment for automotive suppliers like Lear.

As shown in the following chart of global vehicle production and currency exchange rates:

Quarterly Performance Highlights

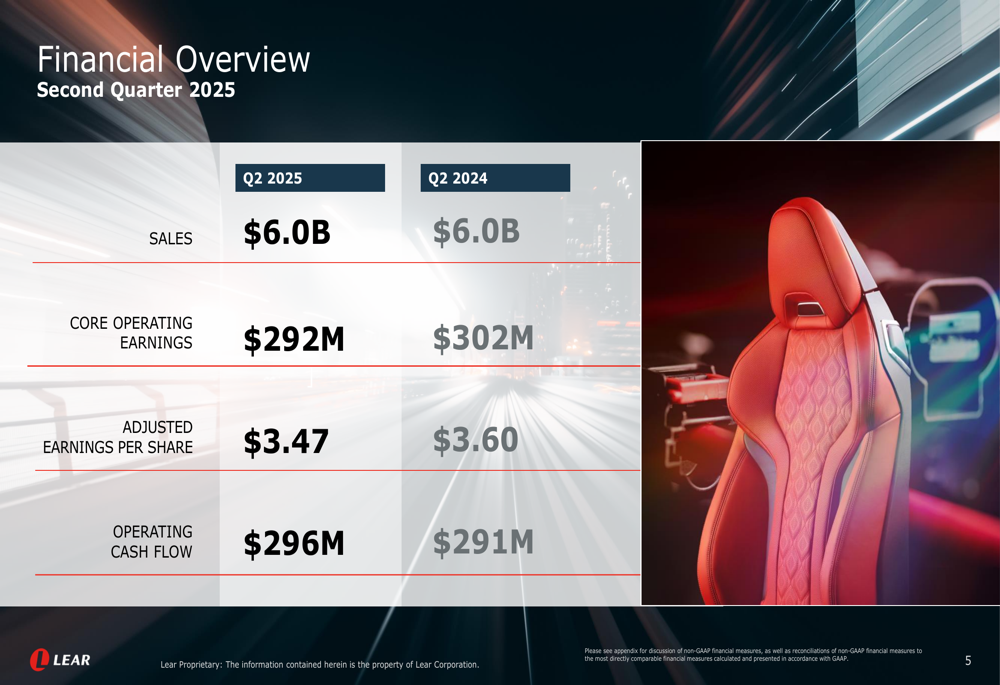

Lear reported sales of $6.0 billion in Q2 2025, unchanged from the same period last year. Core operating earnings decreased slightly to $292 million from $302 million in Q2 2024, while adjusted earnings per share declined to $3.47 from $3.60. Despite these challenges, the company improved its operating cash flow to $296 million, up from $291 million in the prior year.

The following slide provides a comprehensive overview of Lear’s second quarter financial performance:

The company achieved several significant milestones during the quarter, including strong net performance in both segments, generating approximately 45 basis points improvement in Seating and 70 basis points in E-Systems. Lear also announced it is restoring its full-year guidance and increasing total company full-year net performance by approximately $25 million.

As illustrated in this detailed breakdown of key Q2 highlights:

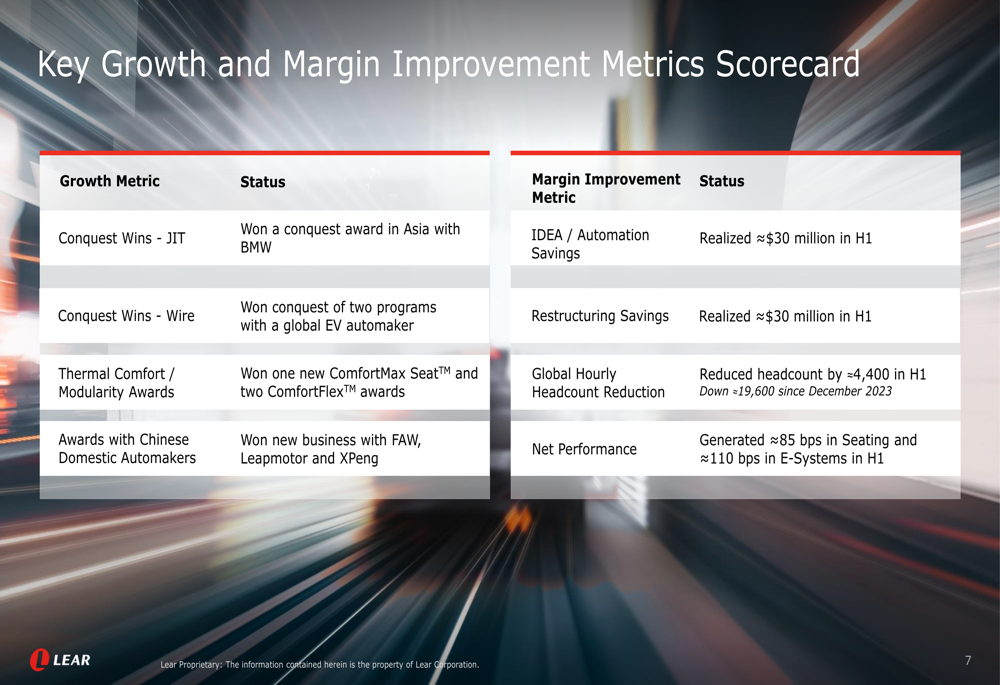

Lear’s scorecard of growth and margin improvement metrics demonstrates the company’s progress in winning new business while enhancing operational efficiency:

Segment Performance Analysis

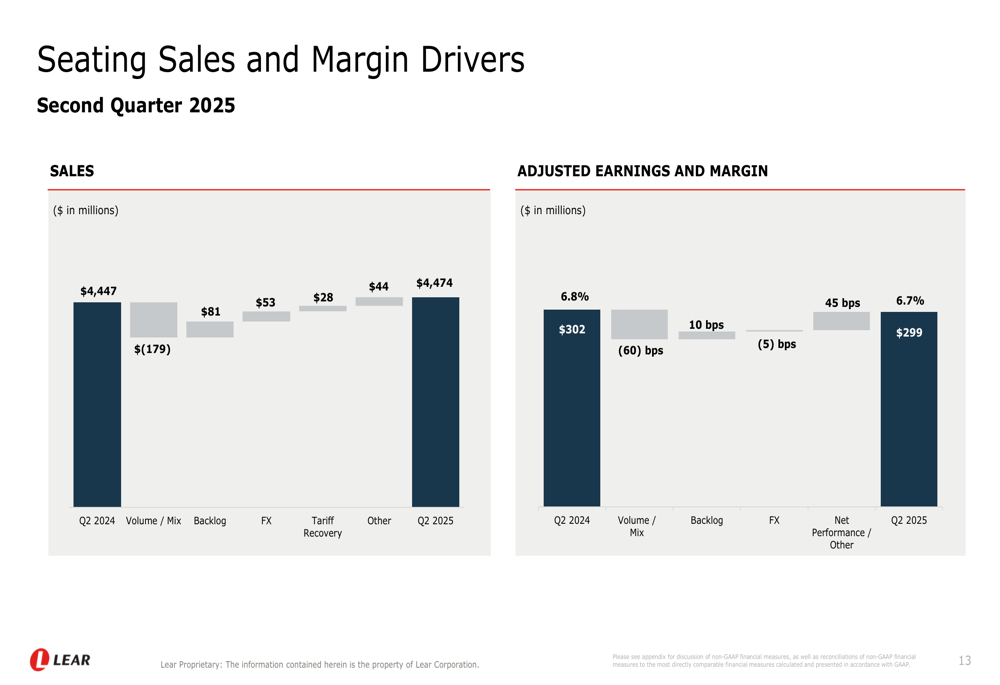

Lear’s Seating segment reported sales of $4.47 billion in Q2 2025, slightly higher than the $4.45 billion in Q2 2024. Despite positive contributions from backlog, foreign exchange, and tariff recovery, the segment faced headwinds from lower volume and mix. Adjusted earnings for the segment were $299 million with a margin of 6.7%, compared to $302 million and 6.8% in the prior year.

The following waterfall chart details the drivers of Seating segment sales and margins:

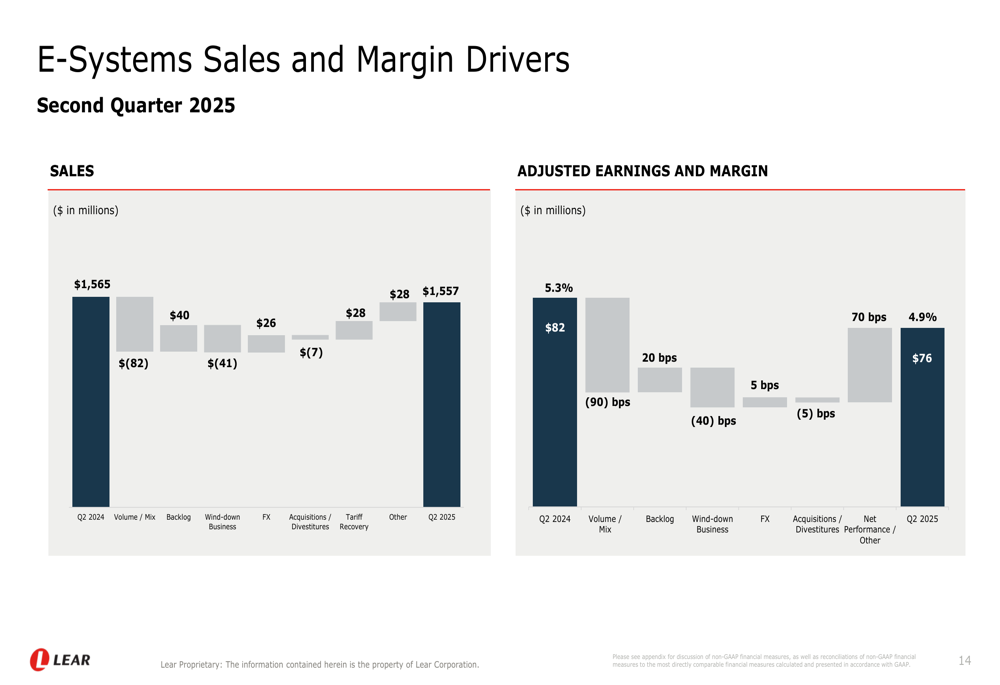

The E-Systems segment faced more significant challenges, with sales decreasing slightly to $1.56 billion from $1.57 billion in Q2 2024. The decline was primarily due to lower volume/mix and wind-down business, partially offset by backlog, acquisitions, and tariff recovery. Adjusted earnings decreased to $76 million with a margin of 4.9%, compared to $82 million and 5.3% in the prior year.

This detailed breakdown shows the factors affecting E-Systems performance:

Strategic Initiatives and Operational Improvements

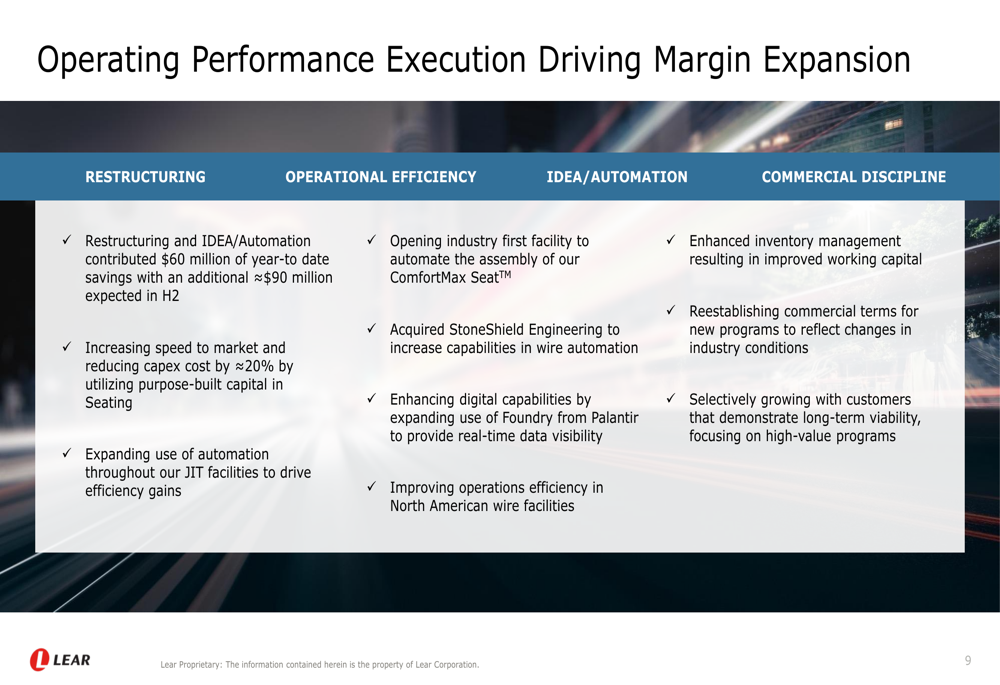

Lear is focusing on operational efficiency to drive margin expansion through four key initiatives: restructuring, operational efficiency, IDEA/automation, and commercial discipline. The company has realized approximately $30 million in IDEA/Automation savings and $30 million in restructuring savings in the first half of 2025.

The following slide illustrates Lear’s approach to operational performance improvement:

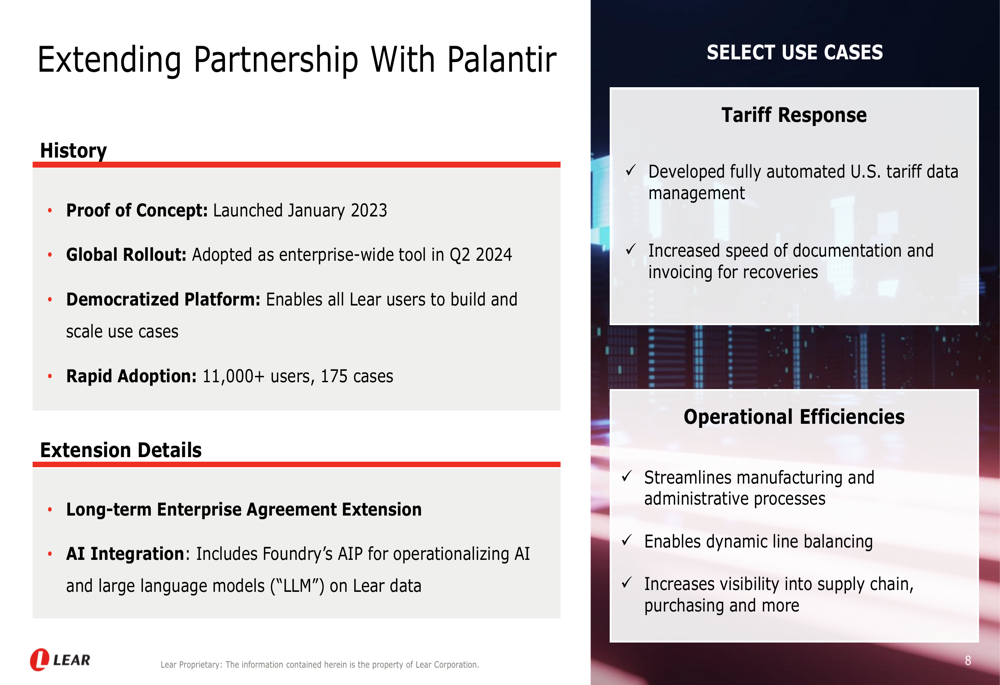

A significant strategic development is Lear’s extended partnership with Palantir Technologies to enhance its IDEA platform capabilities. The partnership, which began with a proof of concept in January 2023, has rapidly expanded to over 11,000 users with 175 use cases. The extension includes AI integration through Foundry’s AIP and has delivered tangible benefits in tariff response and operational efficiencies.

As shown in this overview of the Palantir partnership:

Tariff Exposure and Mitigation

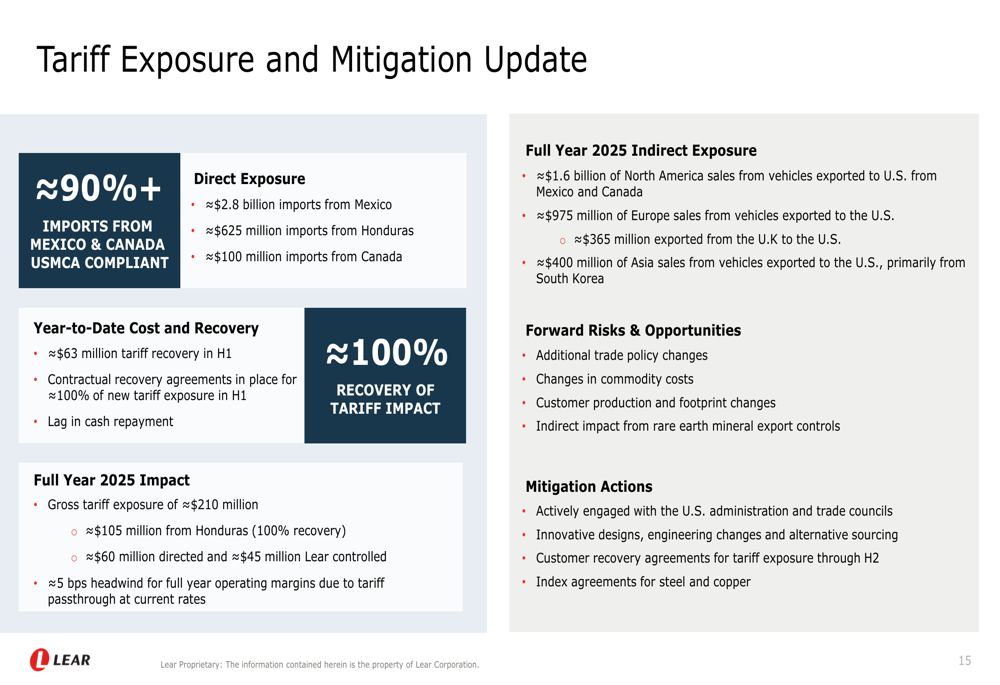

Lear provided a detailed update on its tariff exposure and mitigation strategies. The company has approximately $2.8 billion in imports from Mexico, $625 million from Honduras, and $100 million from Canada, with over 90% of imports from Mexico and Canada being USMCA compliant. Lear has secured contractual recovery agreements for approximately 100% of new tariff exposure in the first half of 2025.

The following slide details Lear’s tariff exposure and mitigation efforts:

2025 Outlook and Capital Allocation

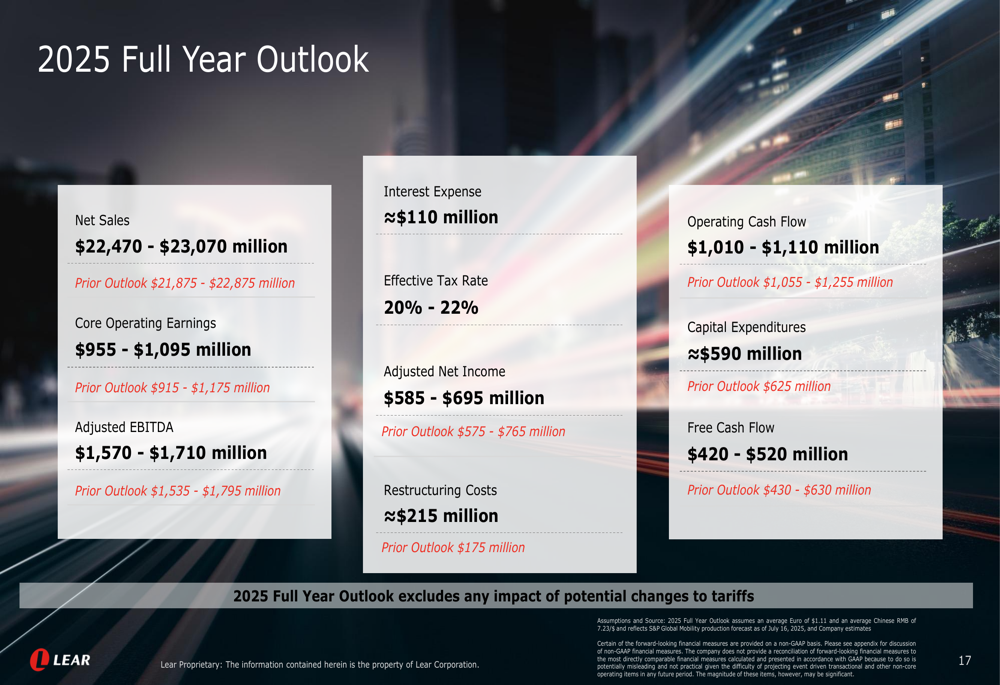

Lear has restored its full-year guidance for 2025, projecting net sales of $22,470 to $23,070 million and core operating earnings of $955 to $1,095 million. The company expects to generate free cash flow of $420 to $520 million for the year.

This comprehensive outlook for 2025 provides investors with clear expectations:

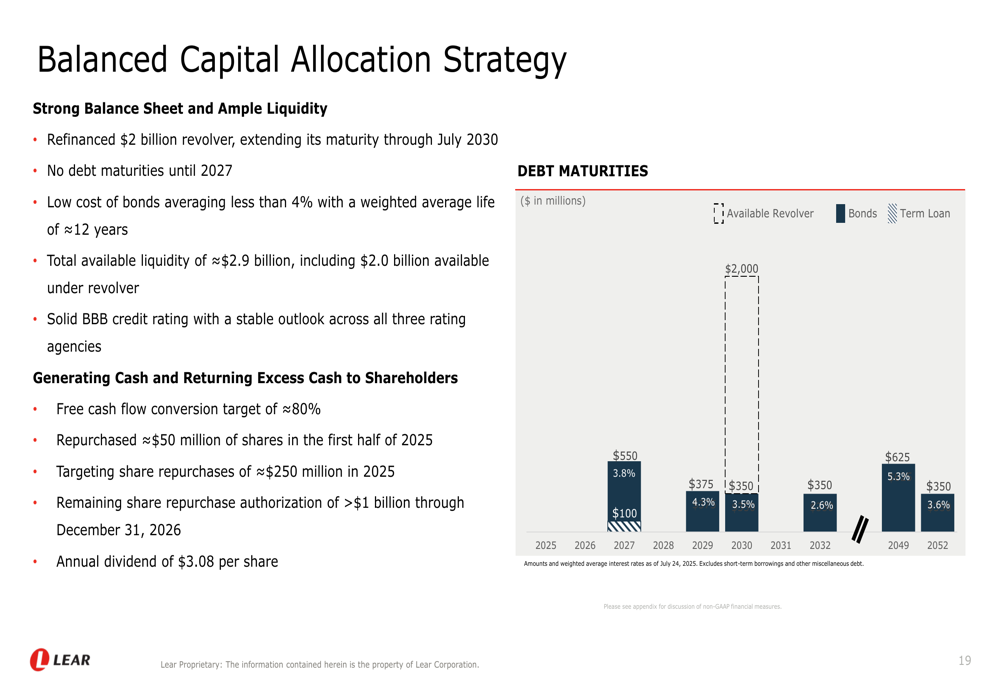

The company maintains a balanced capital allocation strategy, focusing on maintaining a strong balance sheet while returning excess cash to shareholders. Lear refinanced its $2 billion revolver, extending its maturity through July 2030, and has no debt maturities until 2027. The company is targeting share repurchases of approximately $250 million in 2025 and maintains an annual dividend of $3.08 per share.

As illustrated in the capital allocation strategy slide:

Looking at the transition from first half to second half of 2025, Lear expects some challenges with volume and mix, projecting a 90 basis point negative impact on margins. However, the company anticipates that net performance improvements will partially offset these headwinds, resulting in second-half adjusted earnings of $463 million with a margin of 4.1%, compared to $562 million and 4.9% in the first half.

Despite near-term challenges, Lear remains focused on its long-term strategy of extending global leadership in Seating, expanding margins in E-Systems, growing operational excellence capabilities through IDEA, and supporting sustainable value creation with disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.