Futures turn lower; Musk’s $1 trn pay package approved - what’s moving markets

Introduction & Market Context

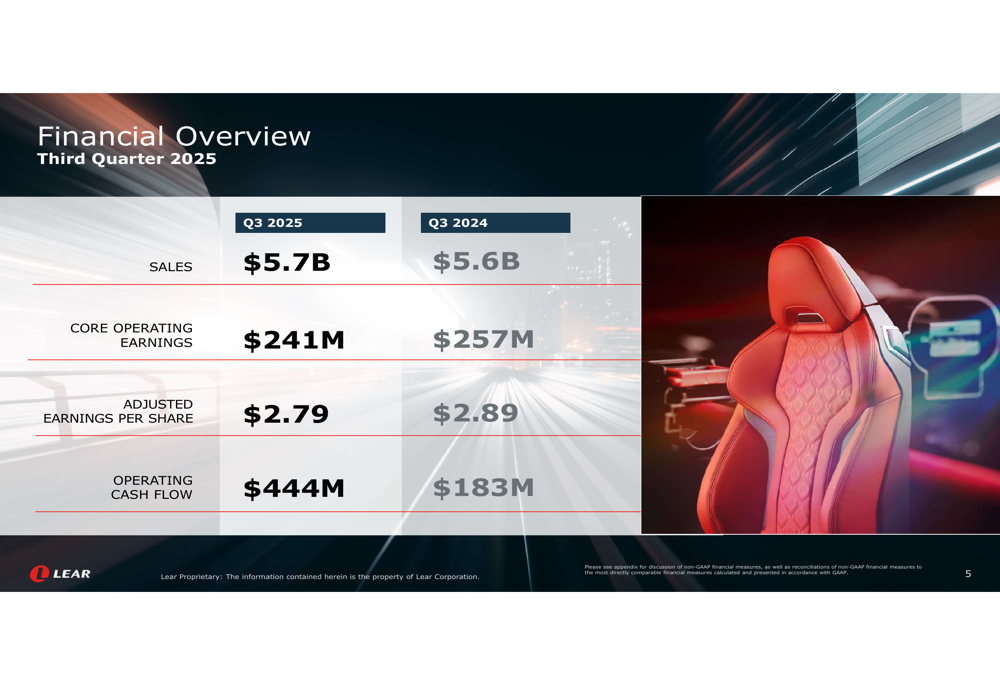

Lear Corporation (NYSE:LEA) released its third quarter 2025 financial results on October 31, showing modest revenue growth despite significant disruption from a cyberattack at key customer Jaguar Land Rover (JLR). The automotive supplier reported revenue of $5.7 billion, up 2% year-over-year, slightly exceeding analyst expectations of $5.64 billion. Adjusted earnings per share came in at $2.79, narrowly beating forecasts of $2.78.

Despite the positive earnings surprise, Lear’s stock traded down 1.14% at market open, reflecting investor concerns about margin pressure and ongoing industry challenges. The company’s presentation highlighted both achievements and headwinds faced during the quarter.

As shown in the following financial overview, Lear managed to grow sales while maintaining relatively stable earnings metrics despite several challenges:

Quarterly Performance Highlights

Lear’s third quarter showed mixed results across its two main business segments. The Seating segment generated $4.25 billion in sales, up from $4.11 billion in Q3 2024, while maintaining relatively stable adjusted earnings of $261 million compared to $262 million a year earlier. However, the segment’s margin contracted slightly to 6.14% from 6.37%.

The E-Systems segment faced more significant challenges, with sales declining to $1.43 billion from $1.47 billion and adjusted earnings dropping to $60 million from $74 million. The segment’s margin contracted more substantially to 4.20% from 5.02% a year earlier.

A major factor affecting both segments was the JLR production disruption caused by a cyberattack, which began on August 31 and significantly impacted production through mid-October. This disruption reduced Lear’s Q3 revenue by approximately $111 million and operating income by $31 million.

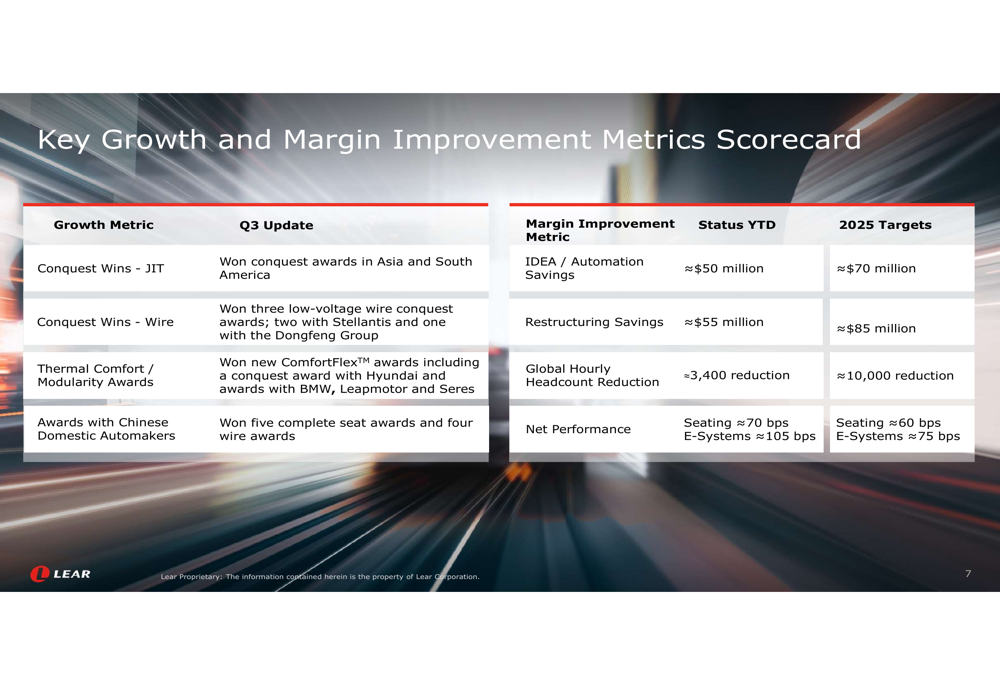

Despite these challenges, Lear highlighted several key achievements during the quarter, as illustrated in this comprehensive overview of the company’s progress:

The company’s operating cash flow showed remarkable improvement, reaching $444 million compared to $183 million in Q3 2024, representing a 142.6% increase year-over-year. This strong cash generation supported Lear’s capital allocation strategy, including share repurchases and dividend payments.

Strategic Initiatives

Lear is pursuing several strategic initiatives to drive future growth and margin improvement. The company has developed a detailed scorecard to track progress on key metrics:

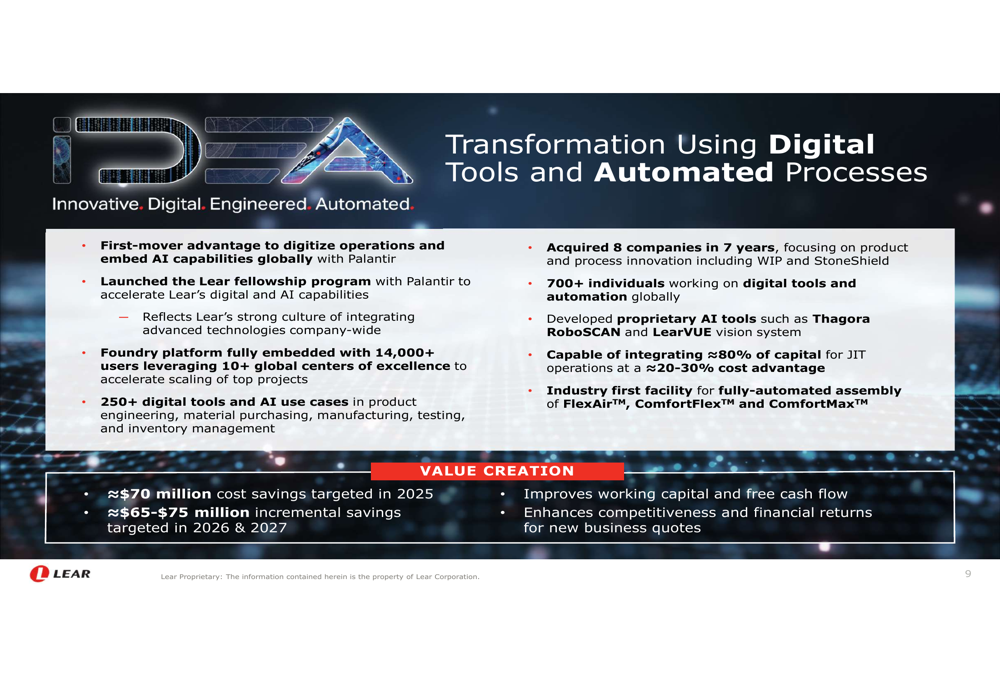

A central element of Lear’s strategy is its digital transformation and automation initiative, branded as "IDEA by Lear" (Innovative Digital Engineered Automated). The company has partnered with Palantir to embed AI capabilities across its global operations, with 14,000+ users leveraging digital tools through 10+ global centers of excellence.

As shown in the following slide, this transformation is expected to generate significant cost savings:

The company is also positioning itself to capitalize on the trend of manufacturing onshoring in the United States. Lear highlighted its competitive advantages, including a significant U.S. manufacturing footprint, extensive vertical integration capabilities, and industry-leading speed to launch. The company is in advanced discussions with several automakers about potential U.S. manufacturing opportunities.

Forward-Looking Statements

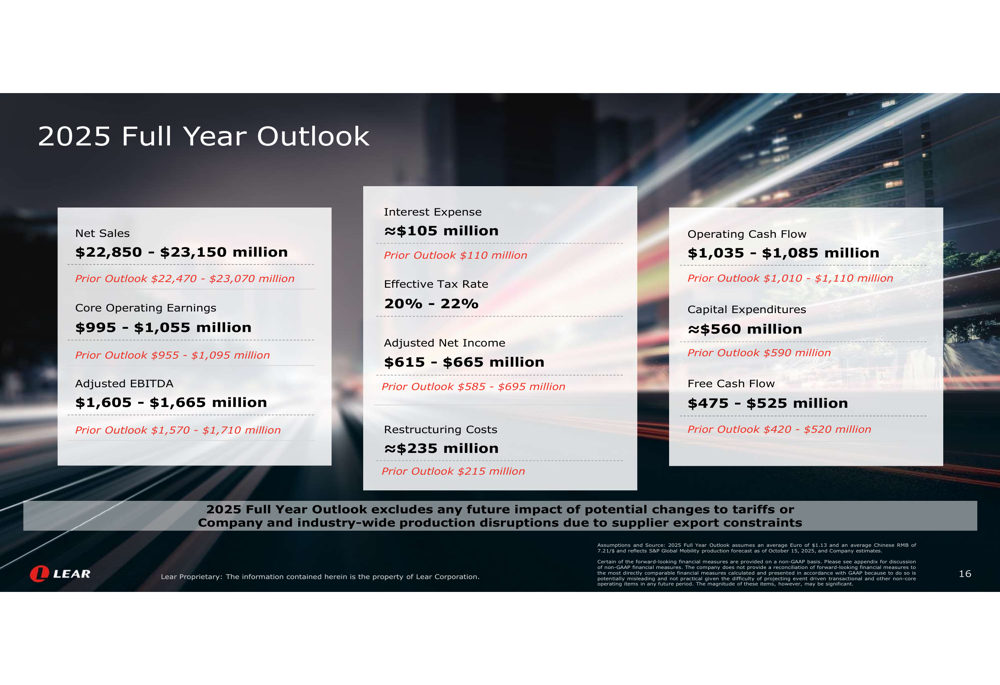

Lear provided a detailed outlook for the full year 2025, maintaining its core operating earnings guidance while slightly raising its sales forecast:

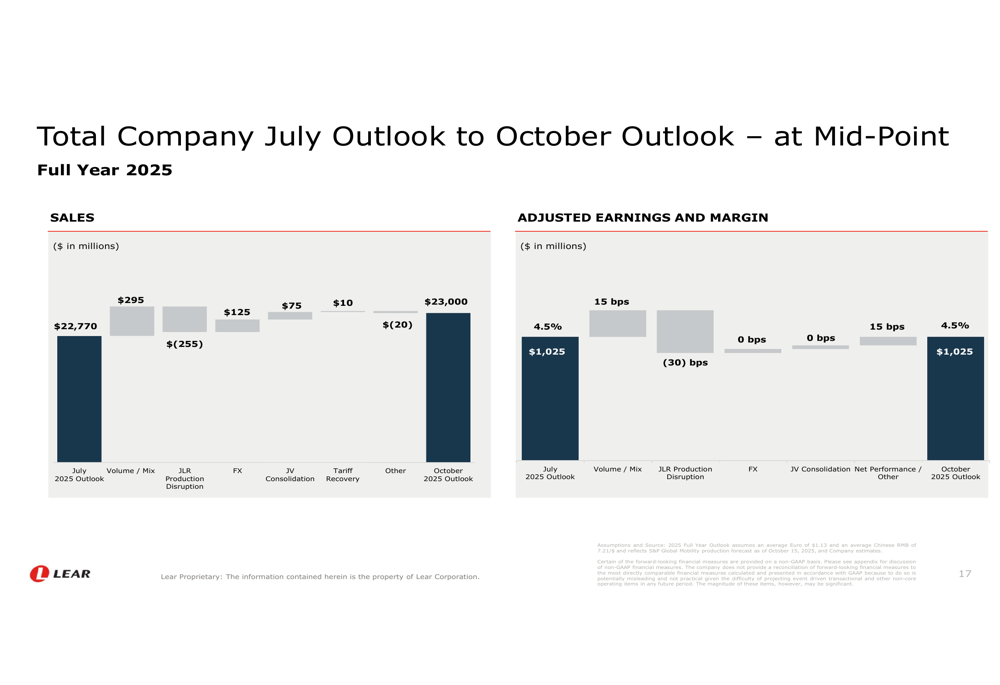

The company explained the changes in its outlook from July to October, highlighting how various factors affected both sales and margins:

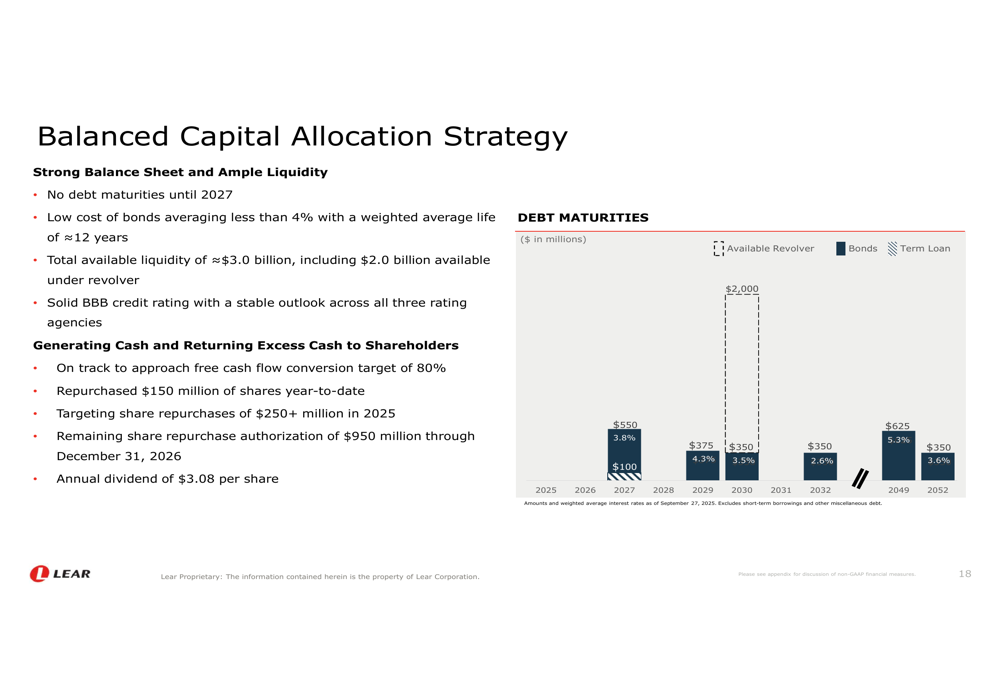

Lear also emphasized its balanced capital allocation strategy, which includes maintaining a strong balance sheet while returning cash to shareholders:

The JLR production disruption is expected to continue impacting results in Q4, with an estimated revenue impact of approximately $143 million and operating income impact of $40 million. For the full year 2025, the total estimated impact is projected to be $255 million in revenue and $71 million in operating income.

Competitive Industry Position

Lear continues to strengthen its competitive position through innovation and customer relationships. During the quarter, the company was recognized by Ferrari and Nissan for its performance and released its 2024 Sustainability Report.

The company secured approximately $1.1 billion in E-Systems business awards year-to-date and won several new seating programs, including five complete seat awards with Chinese domestic automakers. Lear also achieved seven top-four finishes in the J.D. Power 2025 U.S. Seat Quality and Satisfaction Study.

In his concluding remarks, CEO Ray Scott emphasized that Lear is "positioned for long-term success" by extending its global leadership in Seating, expanding margins in E-Systems, growing capabilities in operational excellence, and maintaining disciplined capital allocation.

While the company faces near-term challenges from the JLR disruption and margin pressures, its strong cash flow generation and strategic investments in digital transformation and automation provide a foundation for future growth and profitability improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.