Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Lee Enterprises , Inc. (NASDAQ:LEE) presented its third quarter fiscal year 2025 earnings results on August 7, 2025, highlighting the company’s continued progress in its digital transformation strategy. The media company, which operates local news and information providers across 77 markets, reported that digital revenue now represents 55% of total revenue, marking a significant milestone in its transition from a traditional print publisher to a digital-first media company.

Lee’s stock closed at $4.97 on the day of the presentation, up 2.47% from the previous close, but still near its 52-week low of $4.46, reflecting ongoing investor concerns about the company’s transformation amid industry-wide challenges in the media sector.

Quarterly Performance Highlights

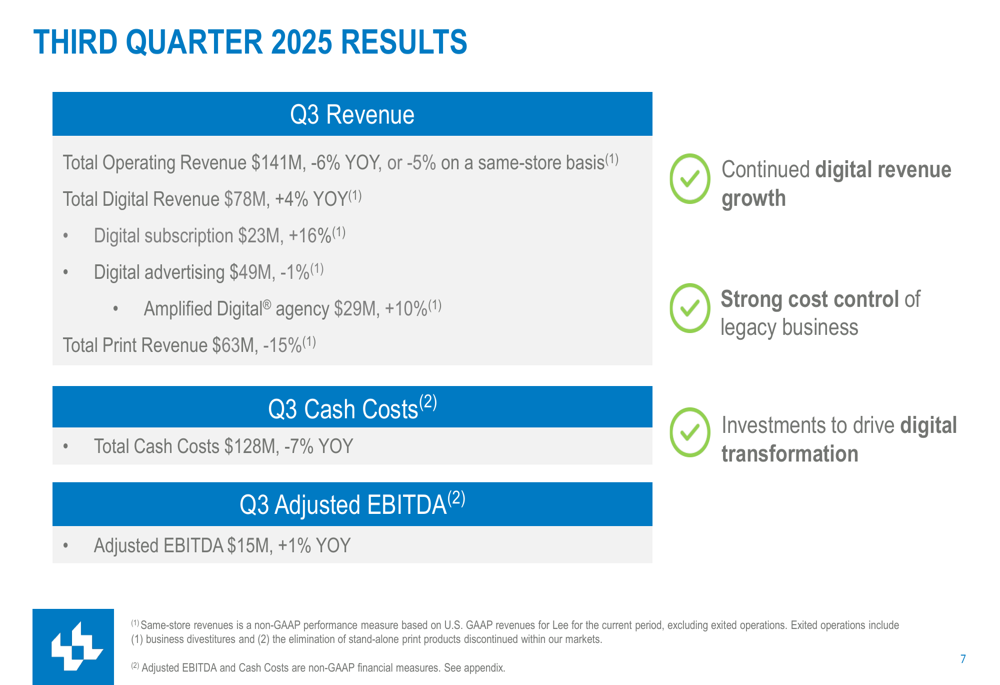

For Q3 FY2025, Lee reported total operating revenue of $141 million, down 6% year-over-year, or 5% on a same-store basis. Despite the overall decline, the company’s digital revenue showed positive momentum, reaching $78 million, a 4% increase year-over-year on a same-store basis.

The company’s adjusted EBITDA was $15 million, up 1% compared to the same period last year, supported by continued cost management efforts. Total (EPA:TTEF) cash costs decreased to $128 million, representing a 7% reduction year-over-year.

As shown in the following breakdown of quarterly results:

Digital subscription revenue was a particular bright spot, growing to $23 million, a 16% increase year-over-year on a same-store basis. The company’s Amplified Digital Agency revenue also performed well at $29 million, up 10% year-over-year on a same-store basis. However, digital advertising revenue declined slightly to $49 million, down 1% compared to the previous year.

Digital Transformation Progress

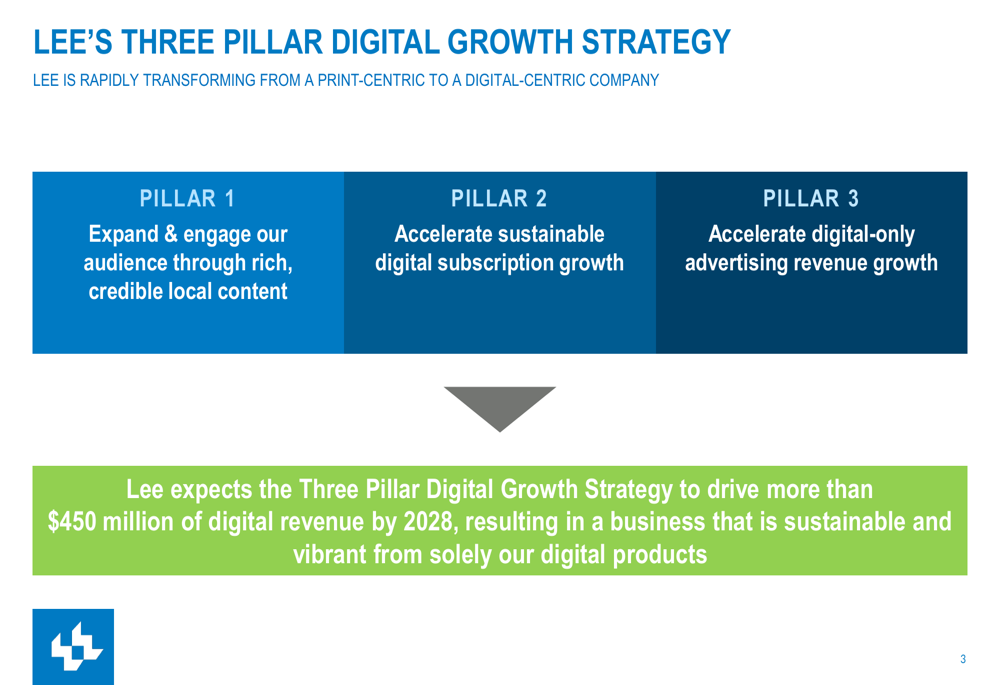

Lee’s digital transformation strategy is built around three core pillars aimed at driving sustainable growth. The company expects this strategy to generate more than $450 million in digital revenue by 2028.

The three pillars of Lee’s digital growth strategy are illustrated here:

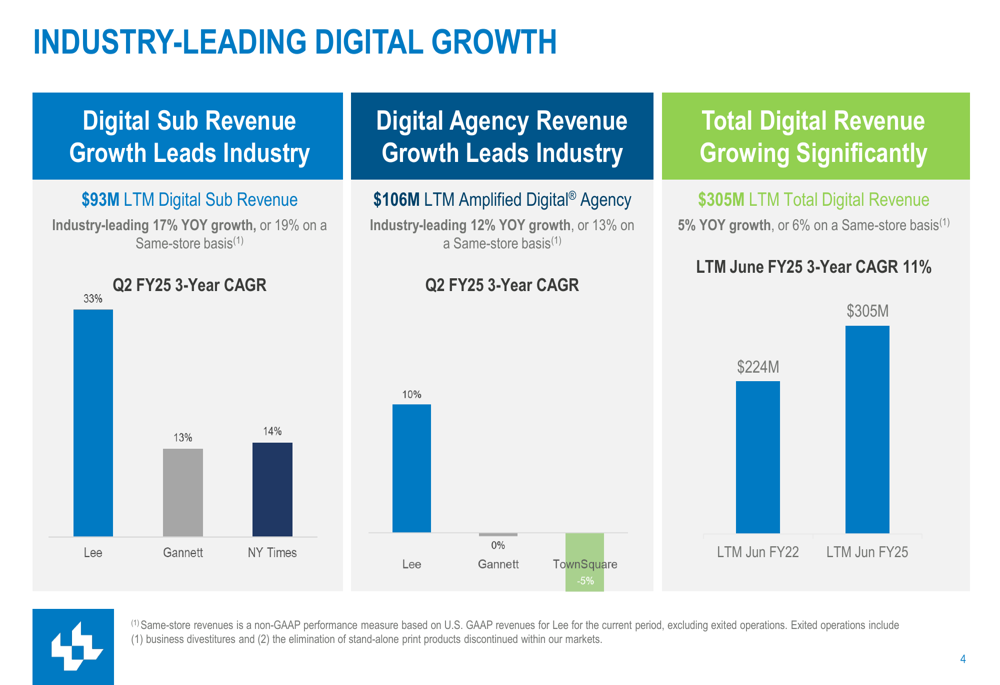

The company claims industry-leading digital growth compared to peers, particularly in digital subscription revenue, which has grown at a three-year CAGR of 33% through Q2 FY2025. This performance compares favorably to competitors like Gannett and The New York Times (NYSE:NYT), according to the company’s presentation.

The following chart highlights Lee’s competitive positioning in digital growth metrics:

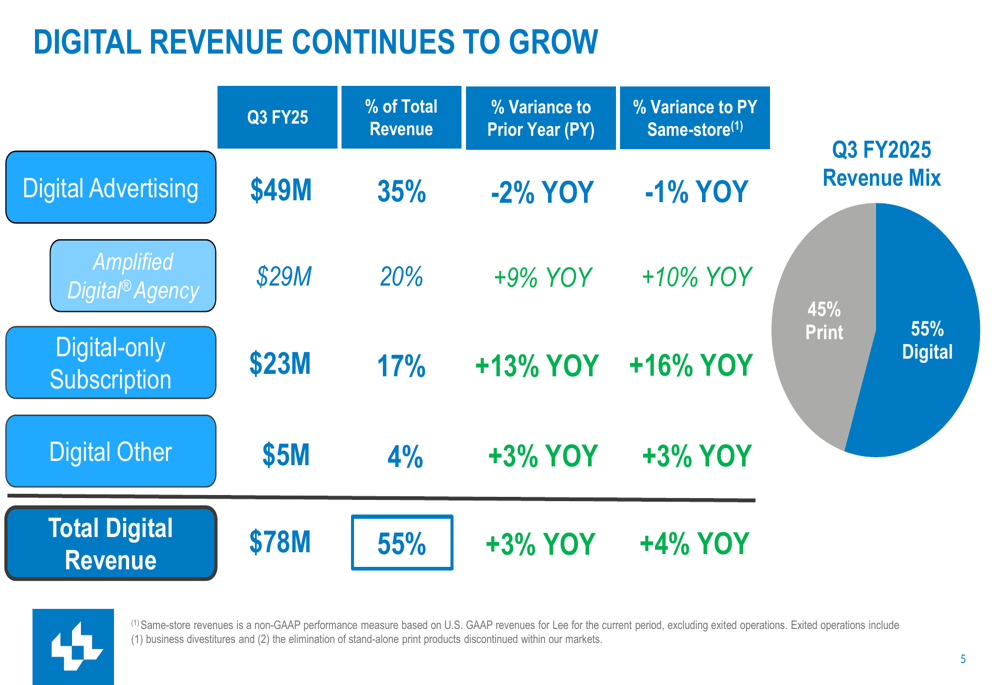

The composition of Lee’s revenue continues to shift toward digital, with the current mix showing digital revenue now exceeding print revenue for the first time:

Financial Challenges and Cost Management

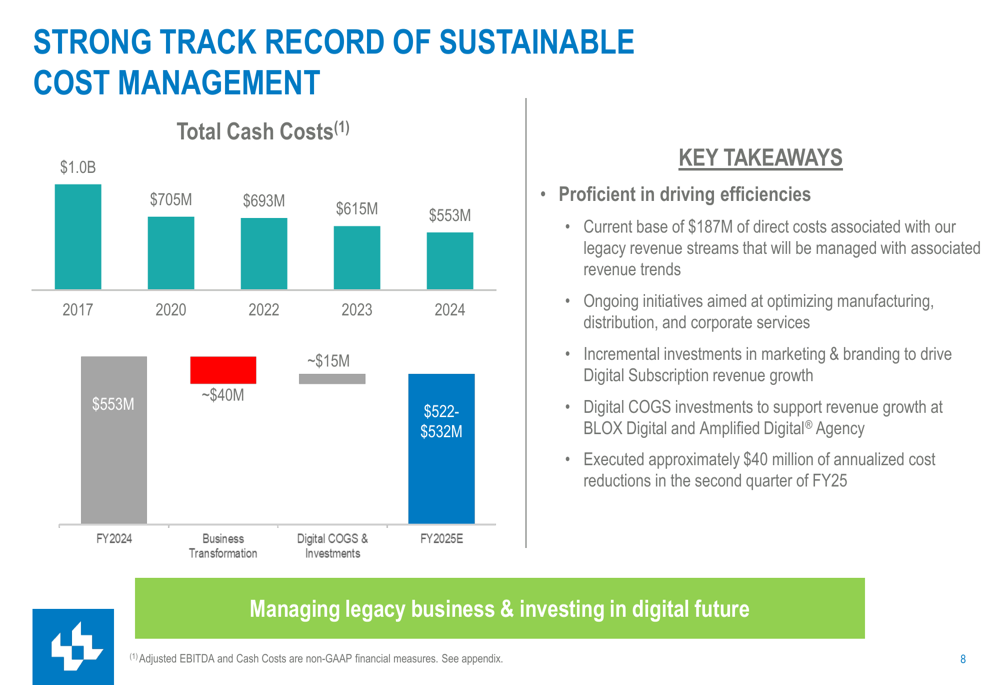

Despite progress in digital revenue growth, Lee continues to face financial challenges. The company has been actively managing costs, with a strong track record of reducing expenses while investing in digital capabilities. Since 2017, Lee has reduced its total cash costs from approximately $1 billion to $553 million in 2024.

The company’s cost management strategy is illustrated in this multi-year trend:

Lee executed approximately $40 million in annualized cost reductions during the second quarter of FY2025, focusing on optimizing manufacturing, distribution, and corporate services while continuing to invest in marketing and digital capabilities.

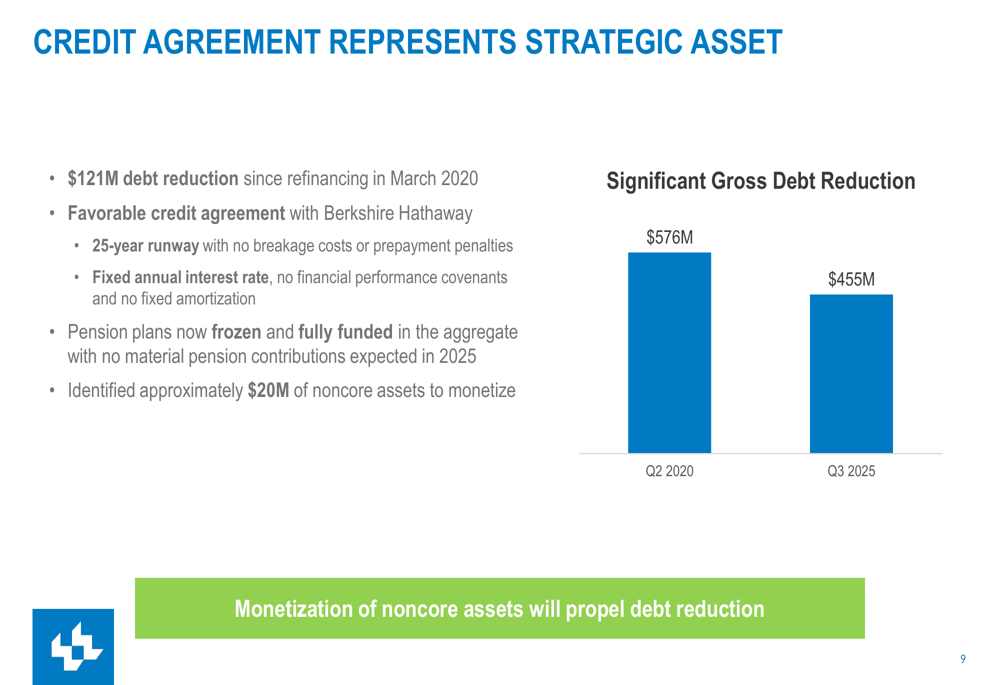

The company has also made progress in reducing its debt burden, decreasing gross debt by $121 million since refinancing with Berkshire Hathaway (NYSE:BRKa) in March 2020. Current debt stands at $455 million as of Q3 2025.

This debt reduction represents progress, but remains significant relative to the company’s market capitalization. The previous quarter’s earnings report revealed wider-than-expected losses, with an EPS of -$2.07 that missed analyst forecasts of -$1.48, leading to an 8.62% stock price drop at that time.

Strategic Outlook and Guidance

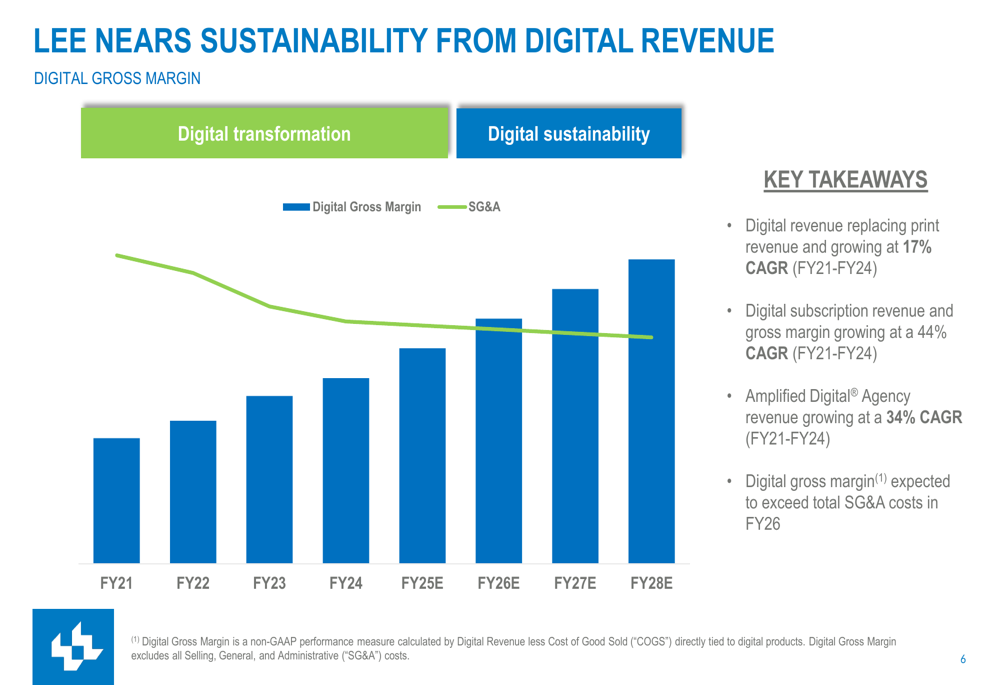

Lee is approaching what it describes as "digital sustainability," the point at which digital gross margin exceeds total SG&A costs, which the company projects will occur in FY2026. This milestone would represent a significant achievement in the company’s transformation journey.

The following chart illustrates Lee’s progress toward digital sustainability:

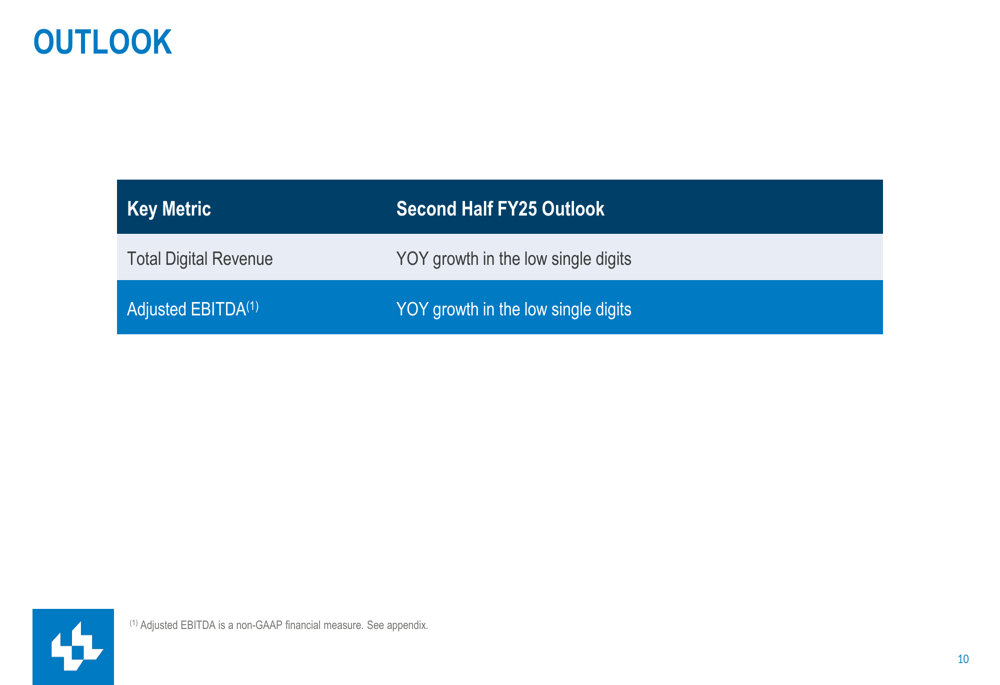

For the second half of FY2025, Lee provided a modest outlook, projecting low single-digit growth for both total digital revenue and adjusted EBITDA. The company remains focused on its three-pillar strategy to expand audience engagement, accelerate digital subscription growth, and increase digital advertising revenue.

While Lee’s presentation emphasizes the positive trajectory of its digital business, the company continues to navigate the challenging transition from print to digital media. The success of this transformation will depend on the company’s ability to accelerate digital revenue growth while managing the decline of its traditional print business and addressing its substantial debt obligations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.