Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Introduction & Market Context

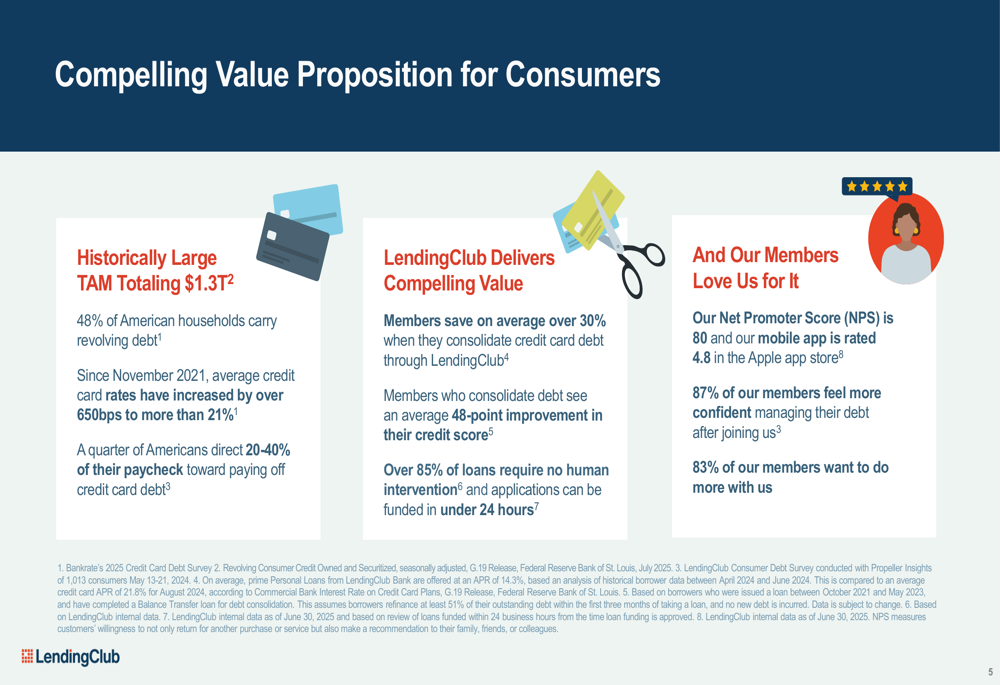

LendingClub Corporation (NYSE:LC) reported its second quarter 2025 financial results on July 29, 2025, showcasing substantial growth across key metrics. The company operates in a historically large total addressable market of $1.3 trillion in outstanding revolving consumer credit, with credit card interest rates reaching 21.2% as of May 2025. According to the presentation, 48% of American households carry revolving debt, with a quarter of Americans directing 20-40% of their paychecks toward paying off credit card debt.

The company’s stock closed at $12.95 before the earnings release and moved up slightly to $13.05 in aftermarket trading, reflecting positive investor sentiment about the results. This represents a significant improvement from the $11.01 aftermarket price following Q1 2025 results, when the company missed EPS forecasts despite beating revenue expectations.

Quarterly Performance Highlights

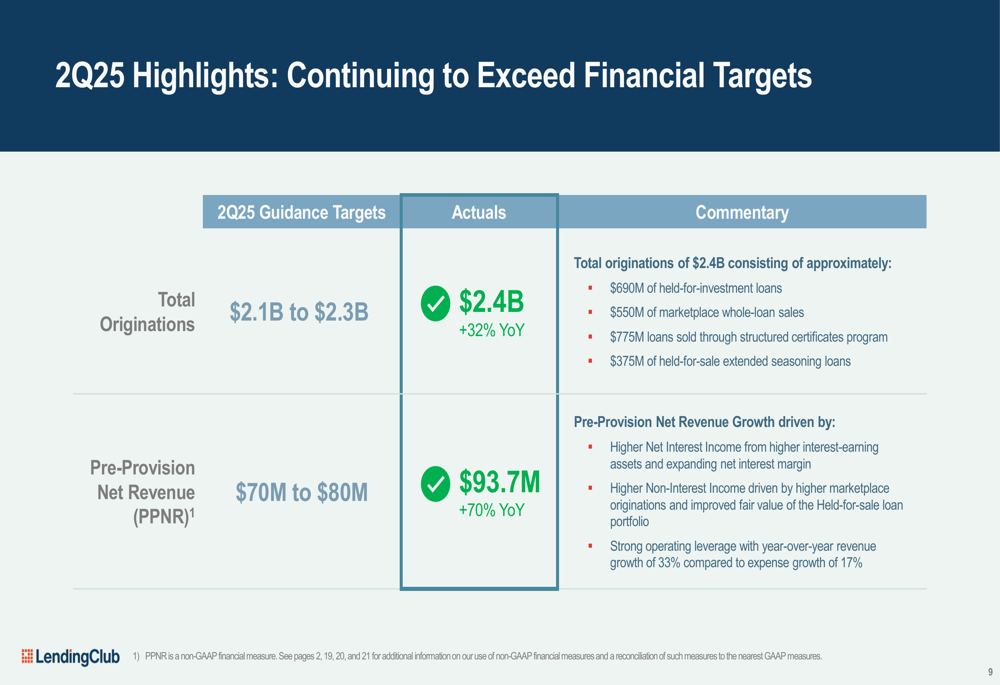

LendingClub significantly exceeded its financial targets for Q2 2025, with total originations reaching $2.4 billion, a 32% year-over-year increase and above the guidance range of $2.1-$2.3 billion. Pre-Provision Net Revenue (PPNR) came in at $93.7 million, growing 70% year-over-year and surpassing the guidance of $70-$80 million.

As shown in the following chart highlighting the company’s financial performance:

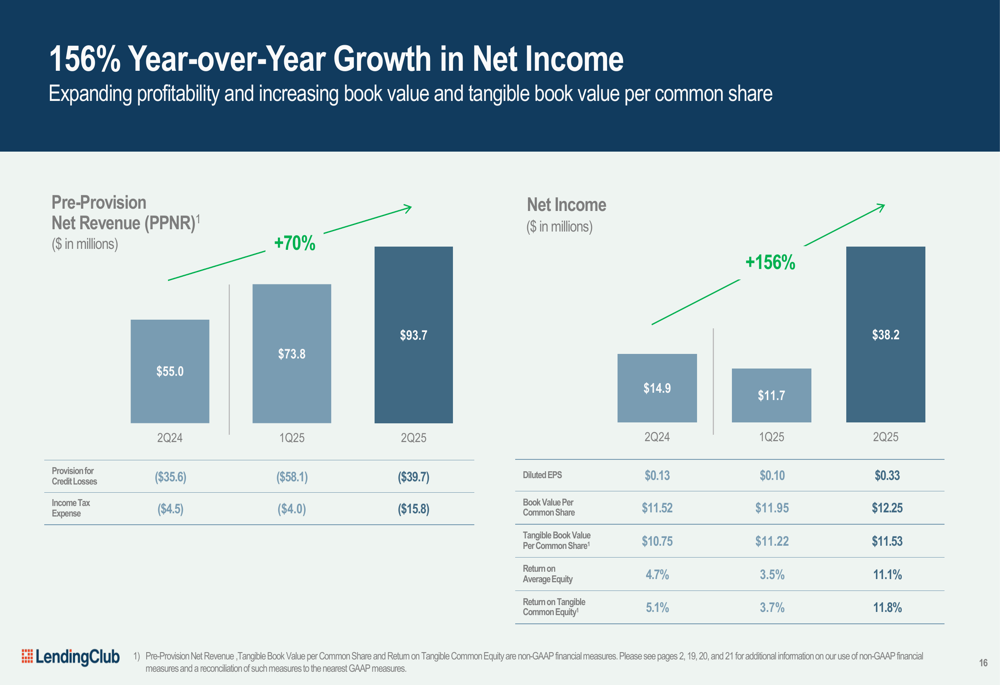

The company reported impressive net income of $38.2 million, representing a 156% year-over-year increase, with diluted earnings per share of $0.33. This marks a substantial improvement from Q1 2025, when the company reported EPS of $0.10, slightly below analyst expectations of $0.11. Return on Average Equity reached 11.1%, while Return on Tangible Common Equity was 11.8%.

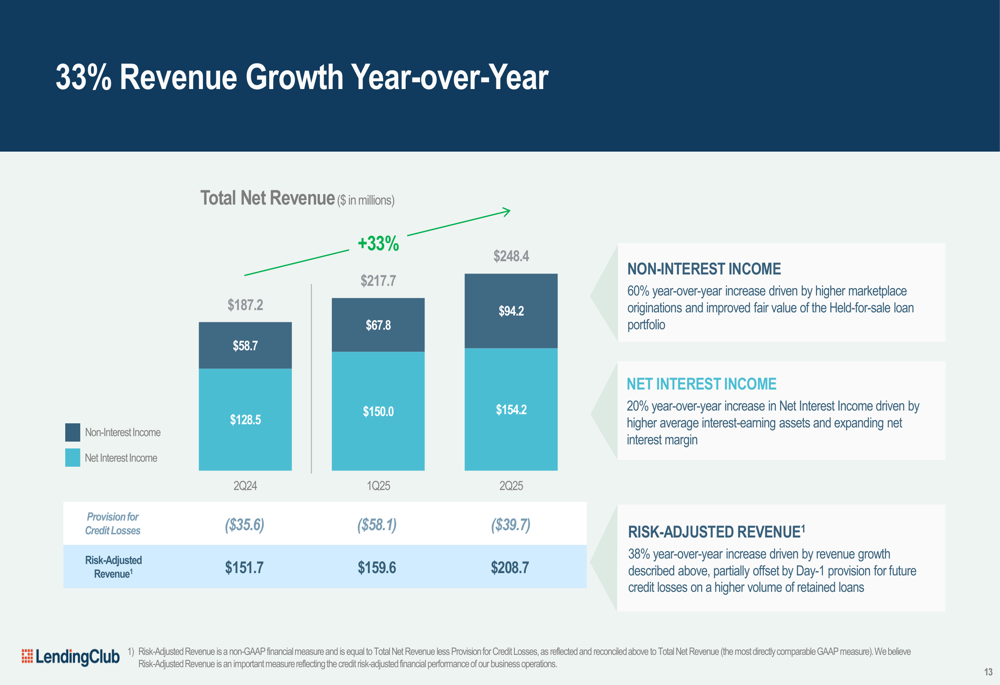

Revenue growth was equally strong, with total net revenue increasing 33% year-over-year. The growth was driven by a 60% increase in Non-Interest Income to $94.2 million and a 20% increase in Net Interest Income to $154.2 million. The following chart illustrates this growth:

LendingClub’s balance sheet grew 12% year-over-year, with the net interest margin expanding to 6.14% from 5.75% in Q2 2024. The company also improved its efficiency ratio by 8 percentage points year-over-year, demonstrating better operational leverage with revenue growth of 33% compared to expense growth of 17%.

Strategic Positioning and Competitive Advantages

LendingClub positions itself as a hybrid between traditional banks and fintechs, claiming to combine the advantages of both while avoiding their respective limitations. The company’s presentation highlighted its unique position in the market, with a capital-light, high-ROE marketplace earnings stream combined with profitable earnings via a high net interest margin loan portfolio.

The following chart illustrates LendingClub’s strategic positioning compared to fintechs and traditional banks:

The company’s credit performance continues to outperform its competitive set, with 30-day+ delinquencies and hardships showing significant improvements across all FICO score ranges. LendingClub utilizes multiple loan disposition channels to optimize earnings and return on capital, including whole loan sales, structured certificates, extended seasoning, and held-for-investment approaches.

LendingClub’s consumer value proposition includes helping members save on average over 30% when consolidating credit card debt and seeing an average 48-point improvement in their credit scores. The company boasts high customer satisfaction with a Net Promoter Score of 80 and an average customer review of 4.83 out of 5 stars.

New Product Initiatives

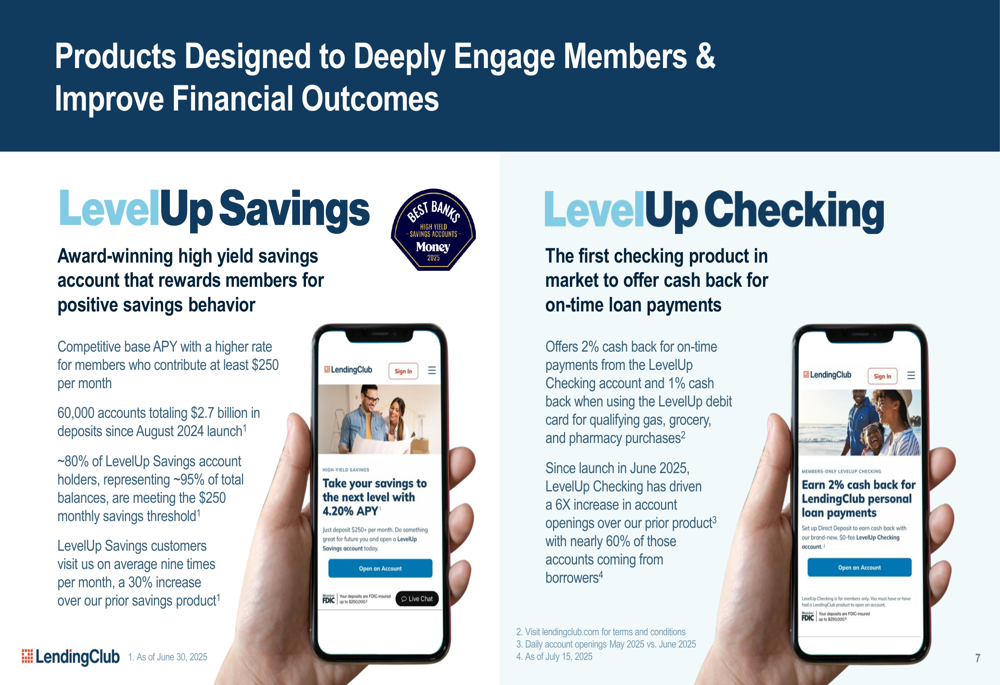

LendingClub is focusing on building lifetime lending relationships with its 5+ million members through new product initiatives. The company recently launched LevelUp Savings and LevelUp Checking products designed to deeply engage members and improve financial outcomes.

LevelUp Savings, an award-winning high-yield savings account, has attracted 60,000 accounts totaling $2.7 billion in deposits since its August 2024 launch. Approximately 80% of account holders, representing 95% of total balances, are meeting the $250 monthly savings threshold to earn higher interest rates. LevelUp Checking, launched in June 2025, offers cash back rewards and has driven a 6x increase in account openings compared to the prior product.

The following chart shows these new product initiatives:

Forward Guidance and Outlook

Looking ahead to Q3 2025, LendingClub provided guidance for total originations between $2.5 billion and $2.6 billion, representing 31% to 36% year-over-year growth. The company expects Pre-Provision Net Revenue between $90 million and $100 million, a 37% to 53% year-over-year increase, and projects Return on Tangible Common Equity between 10% and 11.5%, which would be a 111% to 143% year-over-year improvement.

The guidance assumes a stable economic operating environment and reflects continued positive momentum in originations. The company noted that Q3 2025 PPNR guidance assumes growing revenue partially offset by investment in marketing channel expansion.

LendingClub’s strong Q2 performance and optimistic Q3 outlook suggest that the company has successfully addressed the challenges it faced in Q1 2025, when it missed EPS forecasts despite beating revenue expectations. The hybrid business model combining marketplace lending with traditional banking appears to be delivering results, as evidenced by the substantial growth in net income, revenue, and originations.

The company’s focus on deepening customer relationships through new products and leveraging its digital marketplace bank model positions it well to continue capitalizing on the large addressable market of revolving consumer credit, particularly as credit card interest rates remain historically high.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.