Street Calls of the Week

Introduction & Market Context

Leonardo DRS (NASDAQ:DRS) presented its second quarter 2025 financial results on July 30, 2025, showcasing continued momentum with double-digit revenue growth and significant profit expansion. The defense technology company, which specializes in advanced sensing, computing, and integrated mission systems, demonstrated resilience in what it described as a "dynamic and complex operating environment."

Following a strong first quarter that saw 16% revenue growth, Leonardo DRS has maintained its growth trajectory while navigating challenges from higher R&D investments and elevated raw material costs, particularly germanium, a critical component in infrared sensing technologies.

Quarterly Performance Highlights

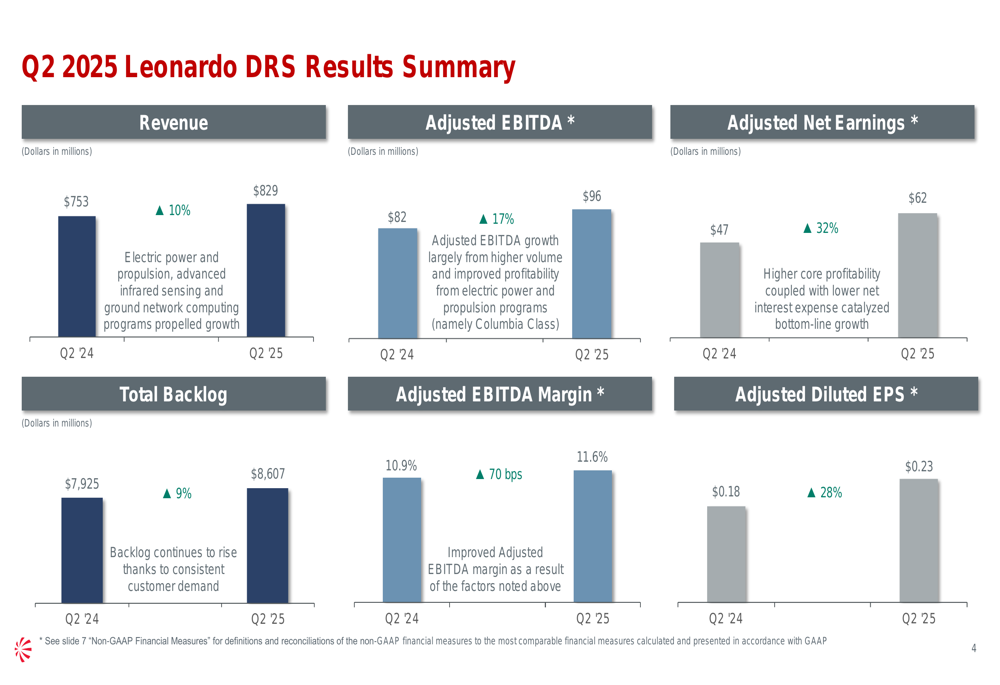

Leonardo DRS reported robust financial results for Q2 2025, with revenue reaching $829 million, representing a 10% increase compared to the same period in 2024. The company’s profitability metrics showed even stronger improvement, with adjusted EBITDA climbing 17% to $96 million and adjusted net earnings surging 32% to $62 million.

As shown in the following comprehensive results summary:

The company’s adjusted EBITDA margin expanded by 70 basis points to 11.6%, reflecting improved operational efficiency despite cost pressures. Adjusted diluted earnings per share increased 28% to $0.23, while total backlog grew 9% to $8.61 billion, indicating strong future revenue potential.

These results build upon the momentum established in Q1 2025, when the company reported 16% year-over-year revenue growth and a 17% increase in adjusted EBITDA, as noted in previous earnings reports.

Segment Analysis

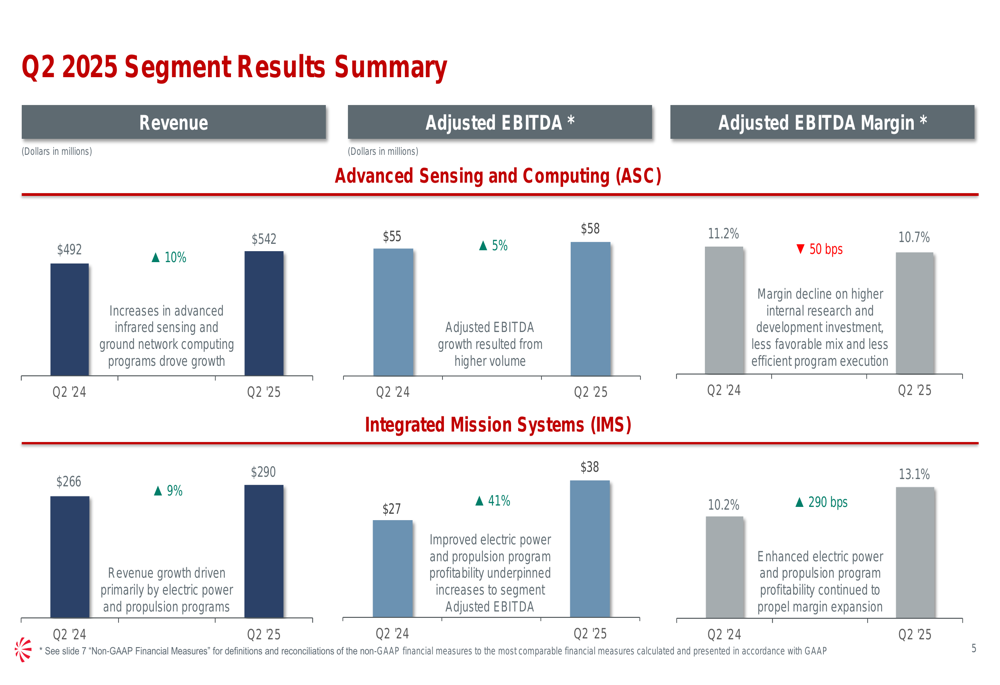

Leonardo DRS operates through two primary business segments: Advanced Sensing and Computing (ASC) and Integrated Mission Systems (IMS). Both segments contributed to the overall growth, though with notably different profitability trends.

The segment breakdown reveals particularly strong performance in the IMS division:

The Advanced Sensing and Computing segment, which represents approximately 65% of total revenue, grew by 10% to $542 million. However, its adjusted EBITDA margin contracted by 50 basis points to 10.7%, suggesting some cost pressures in this division.

In contrast, the Integrated Mission Systems segment delivered exceptional profitability growth, with adjusted EBITDA surging 41% to $38 million on a 9% revenue increase to $290 million. This resulted in a substantial 290 basis point expansion in adjusted EBITDA margin to 13.1%, highlighting the improved operational efficiency in this segment.

Revised Guidance & Outlook

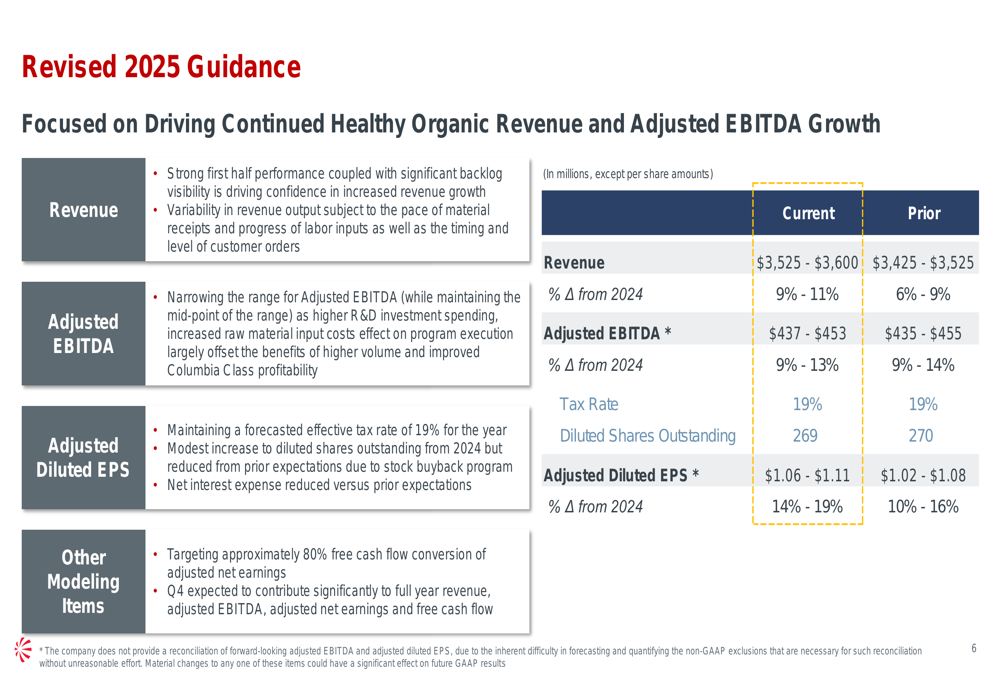

Based on the strong first-half performance, Leonardo DRS has revised its full-year 2025 guidance upward, particularly for revenue and earnings per share:

The company now expects annual revenue between $3.525 billion and $3.600 billion, representing growth of 9% to 11% from 2024. This is an increase from the previous guidance of $3.425 billion to $3.525 billion (6% to 9% growth).

Adjusted diluted EPS guidance has also been raised to $1.06-$1.11, reflecting 14% to 19% growth, compared to the prior guidance of $1.02-$1.08. The adjusted EBITDA range was slightly narrowed to $437-$453 million while maintaining the same growth rate of 9% to 13%.

The company attributed the guidance revision to strong first-half performance, consistent customer demand, and rising backlog, while also accounting for a more dynamic operating environment, higher R&D investments, and elevated raw material costs, particularly germanium.

Strategic Initiatives & Challenges

Leonardo DRS emphasized several key messages that highlight both its strategic direction and the challenges it faces:

The company’s presentation pointed to resilient customer demand across its innovative technology offerings, supporting the increased full-year revenue growth expectations. However, management also acknowledged the challenges of executing in a dynamic and complex operating environment.

The decision to incorporate higher R&D investment suggests a strategic focus on maintaining technological leadership in defense electronics, advanced sensing, and computing systems. This aligns with the company’s long-term strategy of delivering critical innovation efficiently and affordably, as emphasized in previous communications.

The specific mention of elevated raw material input costs for germanium indicates a potential supply chain challenge that the company is navigating. Germanium is a critical material used in infrared sensing technologies, which are core to Leonardo DRS’s product portfolio.

Despite these challenges, the company’s consistent performance across both quarters of 2025 thus far demonstrates its ability to execute effectively while positioning itself for continued growth in the defense technology sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.