Paul Tudor Jones sees potential market rally after late October

Introduction & Market Context

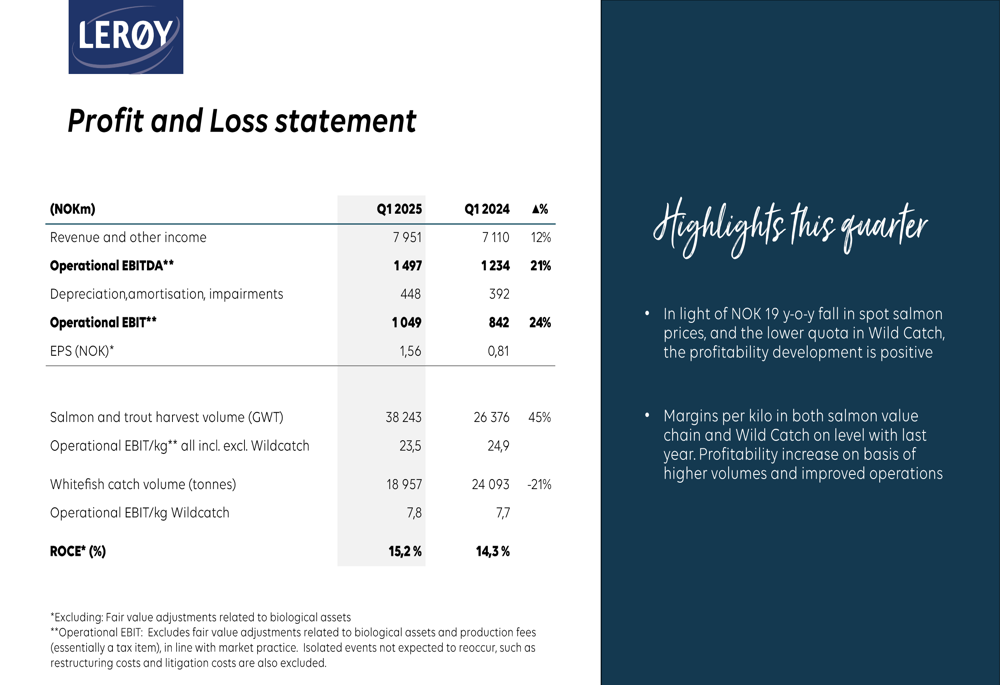

Lerøy Seafood Group ASA (OB:LSG) reported strong first-quarter results for 2025 on May 15, demonstrating resilience in its integrated value chain model despite facing headwinds from lower salmon prices. The Norwegian seafood producer, which operates across farming, wild catch, and value-added processing segments, leveraged increased harvest volumes and operational efficiencies to deliver significant earnings growth.

The company’s performance comes amid a challenging market environment for salmon producers, with spot prices for salmon and trout well below last year’s levels. However, Lerøy’s fully integrated value chain has proven to be a competitive advantage, allowing the company to mitigate price pressures through operational improvements and diversified revenue streams.

Quarterly Performance Highlights

Lerøy reported an Operational EBIT of NOK 1,049 million for Q1 2025, representing a 24% increase from NOK 842 million in the same period last year. Revenue rose 12% to NOK 7,951 million, up from NOK 7,110 million in Q1 2024. Earnings per share nearly doubled to NOK 1.56 from NOK 0.81 in the comparable quarter.

As shown in the following profit and loss statement, the company demonstrated strong growth across key financial metrics despite market challenges:

The company’s return on capital employed (ROCE) improved to 15.2% from 14.3% in Q1 2024, reflecting enhanced operational efficiency. Based on these results, Lerøy has proposed a dividend of NOK 2.50 per share to be approved at the Annual General Meeting.

Segment Analysis

Farming

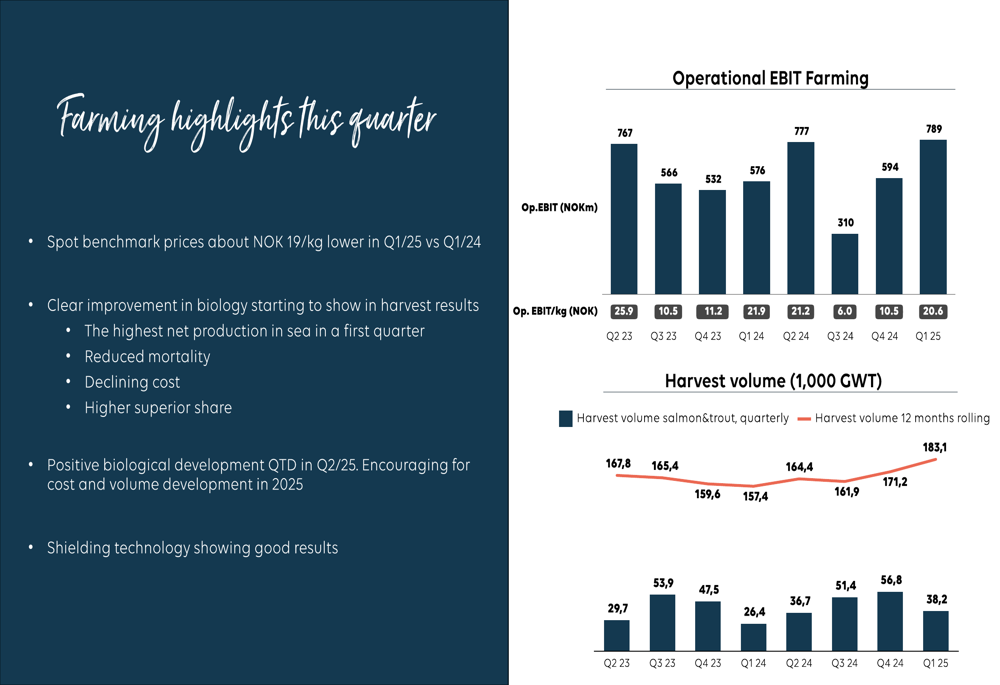

The farming segment showed particularly strong performance, with harvest volumes increasing by 45% to 38,243 GWT compared to 26,376 GWT in Q1 2024. This significant volume growth helped offset the impact of lower spot prices, which were approximately NOK 19/kg lower than in the same quarter last year.

The company highlighted improved biological performance across all farming regions, with record net growth in Q1, reduced mortality, declining costs, and higher superior share of harvest. The following chart illustrates the positive trends in both operational EBIT and harvest volumes:

Lerøy’s regional farming operations all showed improvements, with Lerøy Aurora achieving an operational EBIT/kg of NOK 29.7, Lerøy Midt reaching NOK 31.9, and Lerøy Sjøtroll improving significantly to NOK 18.2 (up from NOK 9.6 in Q1 2024). The company also noted that its investments in shielding technology are showing good results.

Wild Catch

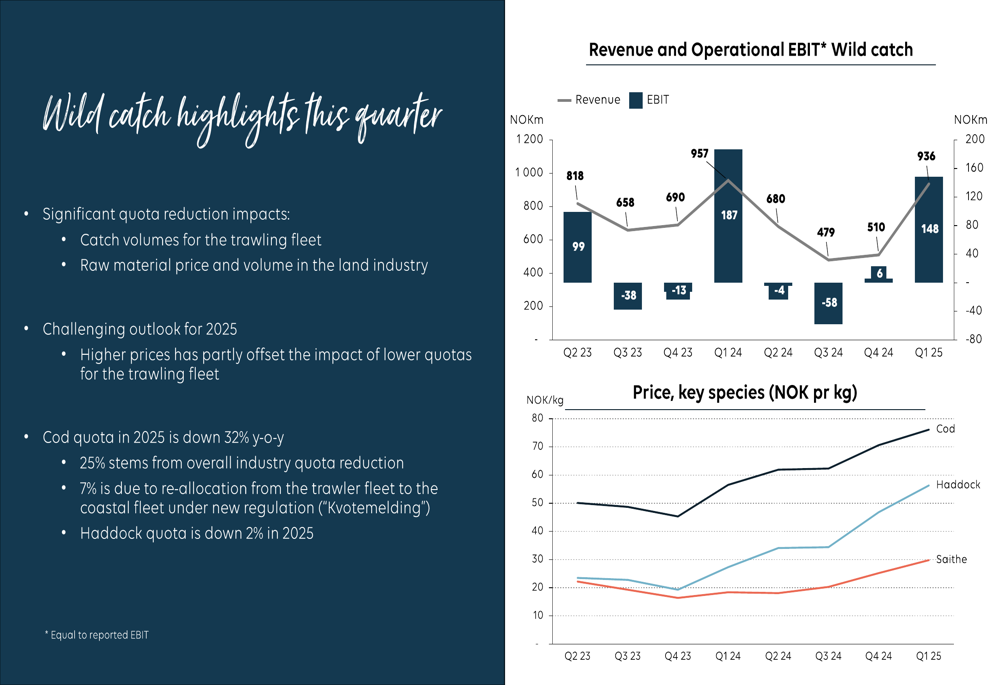

The wild catch segment faced more challenging conditions, with catch volumes declining 21% to 18,957 tonnes due to significant quota reductions. Most notably, the cod quota was reduced by 32% year-over-year, with 25% from overall reduction and 7% due to re-allocation to the coastal fleet.

Despite these volume challenges, the segment achieved an operational EBIT of NOK 148 million in Q1 2025, down slightly from NOK 187 million in Q1 2024. This relatively resilient performance was supported by substantial price increases for key species, particularly cod, which reached NOK 76/kg in Q1 2025 compared to NOK 54/kg in Q1 2024.

The following chart illustrates the revenue, operational EBIT, and price trends for key species in the wild catch segment:

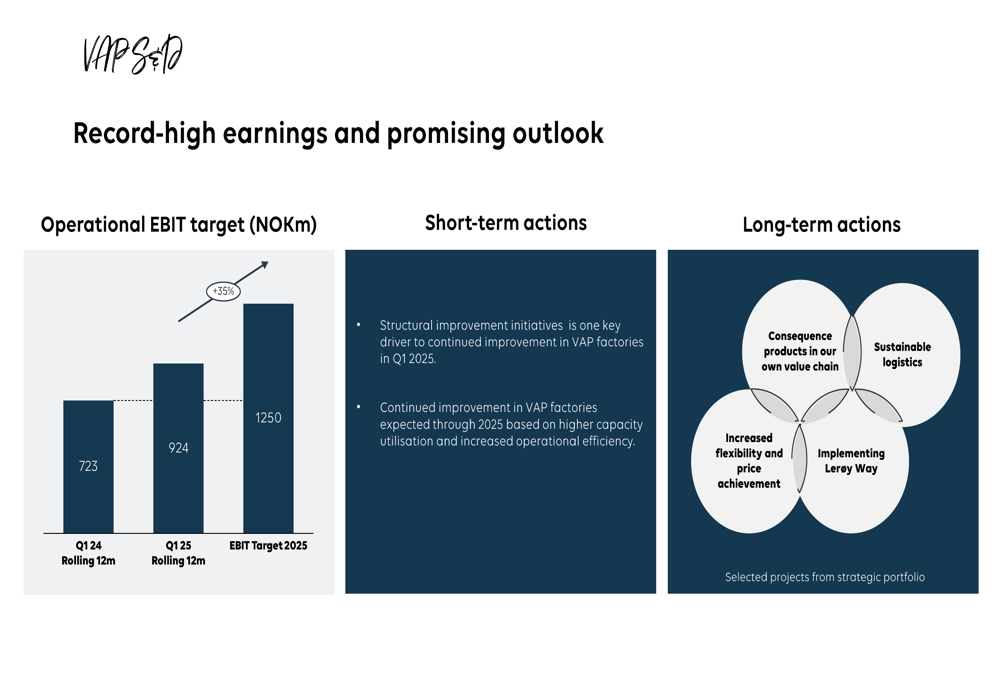

Value-Added Products, Sales & Distribution (VAPS&D)

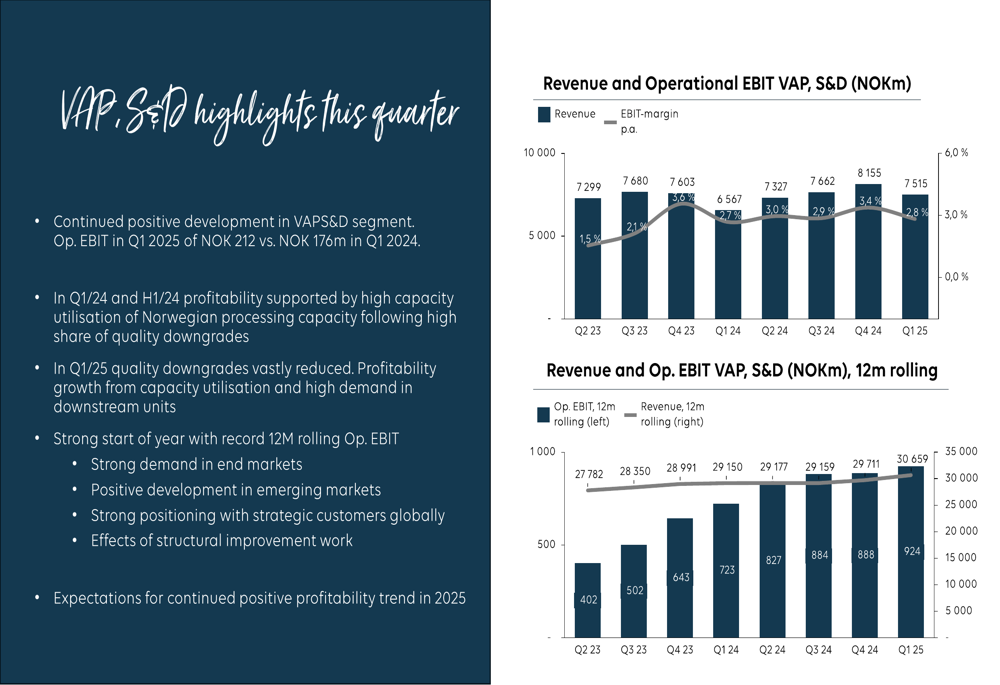

The VAPS&D segment continued its strong performance trajectory, achieving an operational EBIT of NOK 212 million in Q1 2025, up from NOK 176 million in Q1 2024. On a rolling 12-month basis, the segment’s operational EBIT reached NOK 924 million, approaching the company’s 2025 target of NOK 1.25 billion.

The segment’s performance is illustrated in the following chart showing revenue and operational EBIT trends:

Lerøy attributed the segment’s success to continued positive development and reduced quality downgrades. The VAPS&D segment has become an increasingly important contributor to the company’s overall profitability, demonstrating the value of Lerøy’s integrated business model.

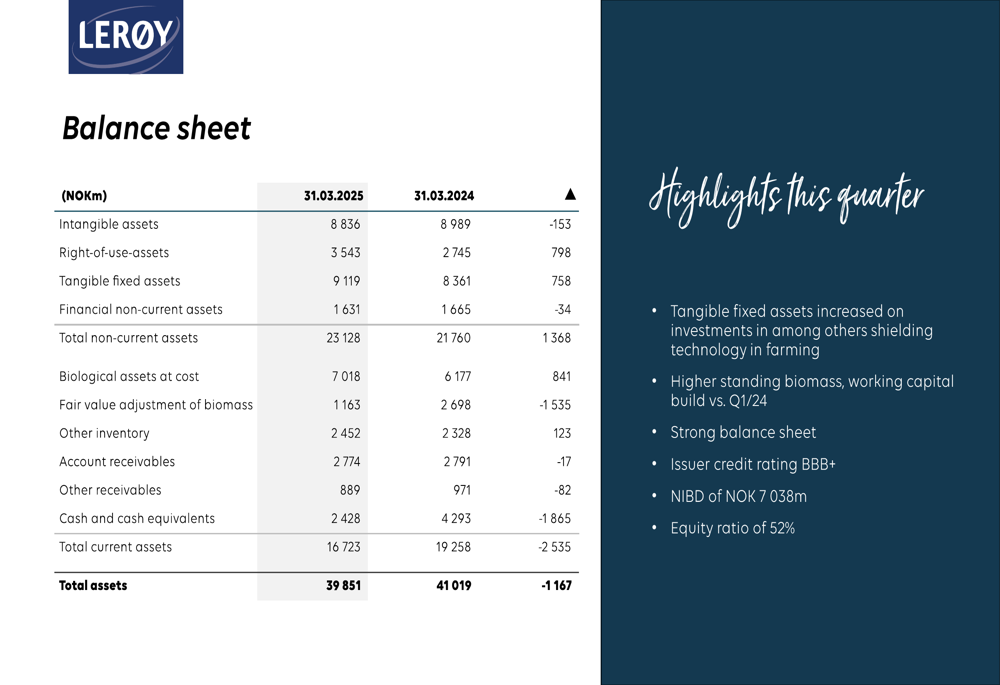

Balance Sheet and Financial Position

Lerøy maintained a strong balance sheet with an equity ratio of 52%. The company’s net interest-bearing debt stood at NOK 7,038 million at the end of Q1 2025, down from NOK 7,705 million at the beginning of the quarter. This reduction was primarily driven by strong EBITDA generation of NOK 1,444 million, partially offset by capital expenditures of NOK 440 million.

The following chart illustrates the changes in net interest-bearing debt during the quarter:

The company’s capital expenditure for 2025 is estimated at approximately NOK 2.0 billion, focusing on investments in farming technology (including shielding technology), postsmolt projects, and developing the VAPS&D and Wild Catch segments.

Strategic Initiatives and Outlook

Lerøy reaffirmed its strategic targets, including achieving revenue of over NOK 50 billion by 2030 (up from approximately NOK 31 billion in 2024), becoming the industry leader in EBIT/kg for farming and VAPS&D by 2025, and reaching a harvest volume of 200,000 tonnes of salmon and trout in Norway by 2025.

For the VAPS&D segment, the company is making significant progress toward its 2025 EBIT target of NOK 1.25 billion, as shown in the following chart:

The company also outlined its position on the recently launched Norwegian Aquaculture White Paper, stating support for the goals of increased food production, job creation, and value generation, while expressing concerns that parts of the paper lack sufficient scientific basis. Lerøy emphasized that its own development and results demonstrate the possibility of making significant improvements within the current licensing regime.

Looking ahead, Lerøy expects continued positive cost development in farming throughout 2025, while acknowledging that the wild catch segment faces a challenging outlook due to lower quotas, which will be only partially offset by higher prices. The VAPS&D segment is expected to continue its strong performance trajectory toward the 2025 target.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.