Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Leumi (TASE:LUMI) delivered strong financial results in the second quarter of 2025, maintaining its trajectory of high profitability amid Israel’s continued economic recovery. The bank’s presentation, released on August 13, 2025, highlights robust performance across key metrics despite ongoing regional challenges.

Israel’s macroeconomic environment shows signs of resilience, with GDP growth forecast at 4.6% for 2025, significantly outpacing OECD averages. This positive backdrop has supported Leumi’s business expansion, though rising government debt-to-GDP ratios (projected at 70% for 2025) and persistent inflation (expected at 3.1% for 2025) present ongoing challenges.

The bank’s stock responded positively to the results, with shares rising 1.86% to 6,149 in trading following the presentation, approaching its 52-week high of 6,425.

Quarterly Performance Highlights

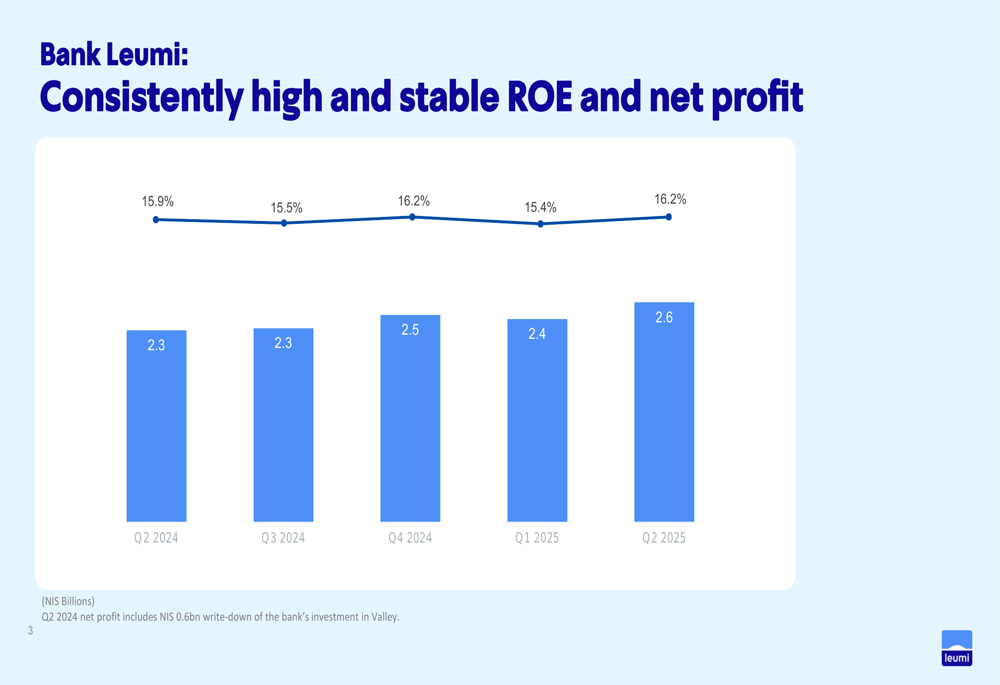

Leumi reported a net profit of NIS 2.61 billion for Q2 2025, representing a 13.5% increase from the NIS 2.3 billion recorded in Q2 2024. Return on equity (ROE) reached 16.2%, up from 15.9% in the same quarter last year, demonstrating the bank’s consistent ability to generate strong returns for shareholders.

As shown in the following chart tracking ROE and net profit over five consecutive quarters, Leumi has maintained ROE above 15% throughout this period, with Q2 2025 marking a return to the peak level seen in Q4 2024:

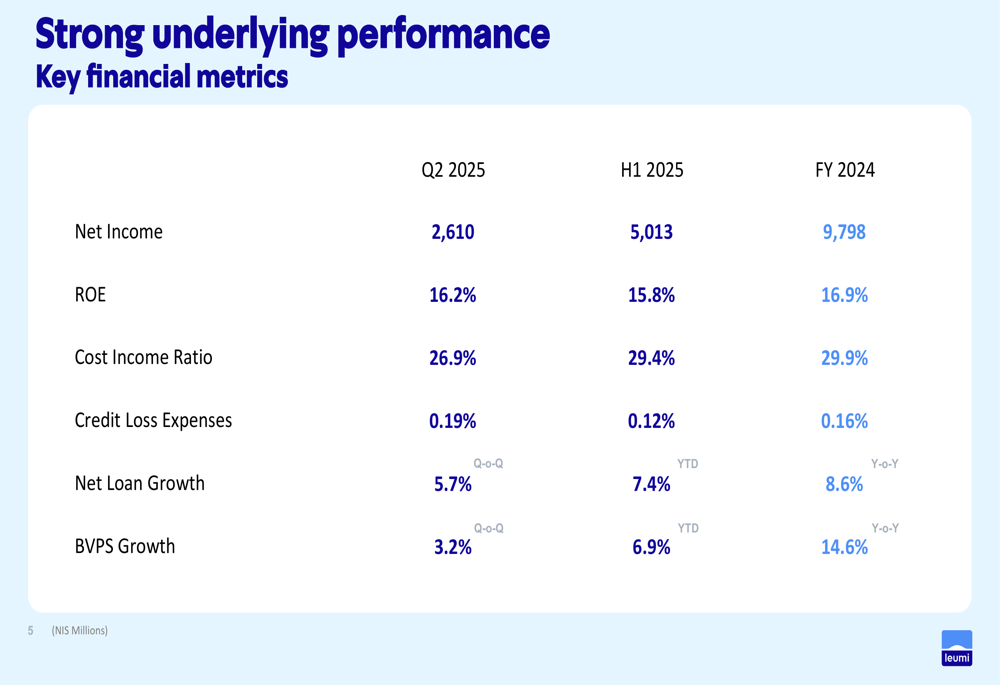

The bank’s comprehensive performance metrics for Q2 2025 show improvements across multiple dimensions, with a notably low cost-income ratio of 26.9% and credit loss expenses at a manageable 0.19% of the loan portfolio:

Detailed Financial Analysis

Leumi’s finance income reached NIS 4.95 billion in Q2 2025, a 2.6% increase from NIS 4.82 billion in Q2 2024. This growth was primarily driven by a 3.7% rise in net interest income to NIS 4.54 billion, partially offset by a slight decline in non-interest finance income.

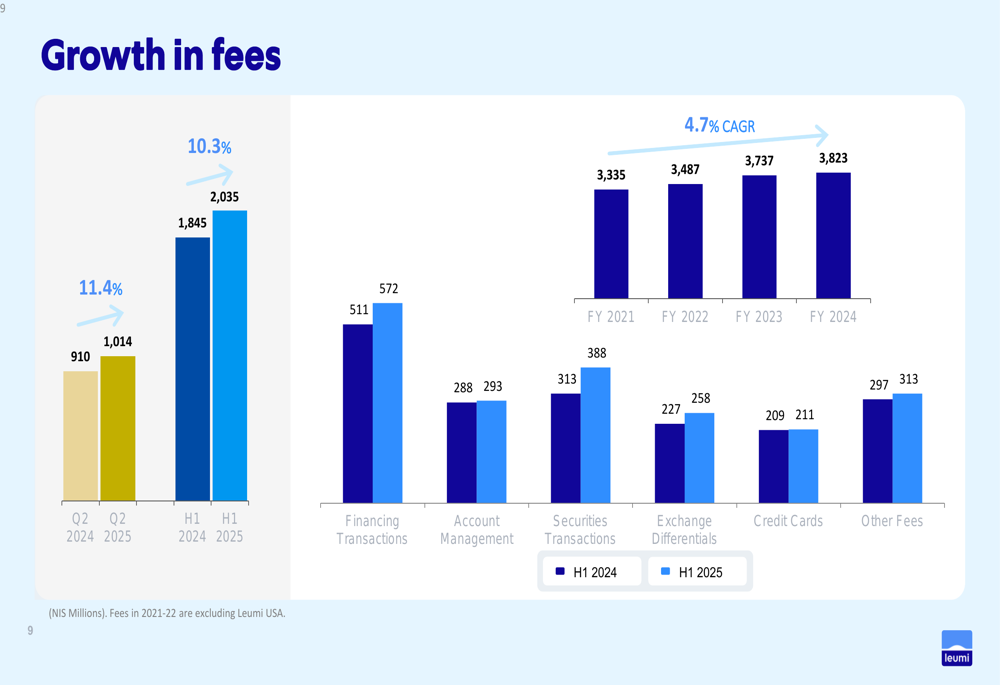

The bank’s operational efficiency continues to improve, with operating and other expenses decreasing by 2.5% year-over-year to NIS 1.61 billion in Q2 2025. This reduction in expenses, coupled with an 11.4% increase in fees and commissions to NIS 1.01 billion, contributed to a 6.9% growth in pre-provision net revenue (PPNR) to NIS 4.38 billion.

Fee income has become an increasingly important revenue stream for Leumi, showing consistent growth across multiple categories. The following chart illustrates this positive trend:

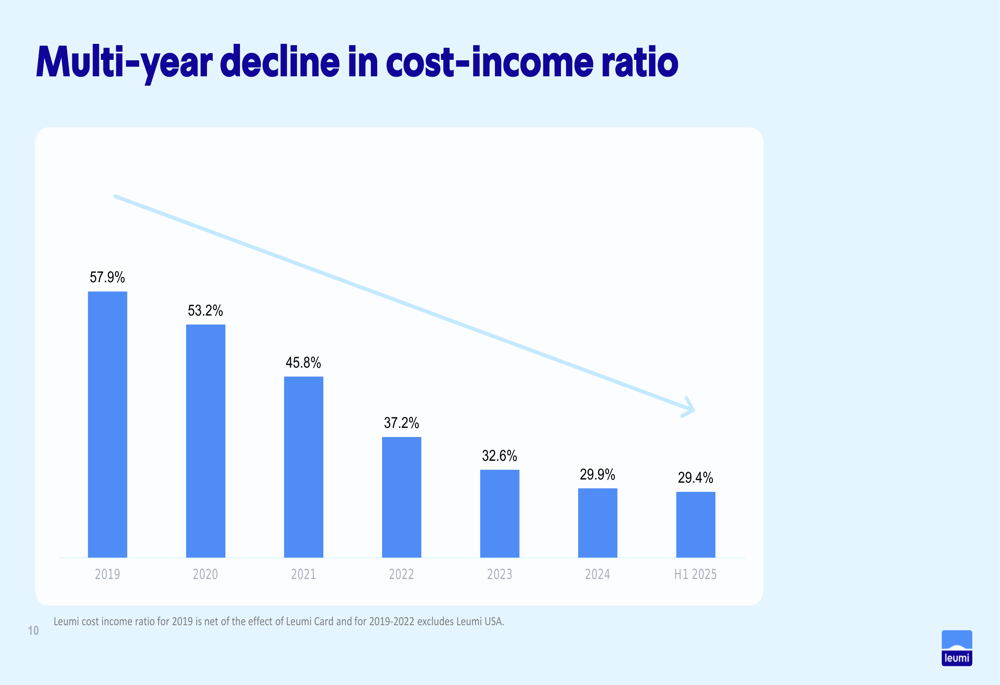

Leumi’s cost-income ratio has seen a remarkable multi-year improvement, declining from 57.9% in 2019 to just 29.4% in H1 2025. This transformation reflects the bank’s successful efficiency initiatives and positions it favorably compared to industry peers:

Asset Quality and Loan Growth

Credit quality remains strong, with non-performing loans (NPLs) decreasing to 0.43% in H1 2025 from 0.50% in 2024. Total troubled debts also declined slightly to 1.43% of gross loans, while the bank maintains robust provision coverage with provisions to NPLs at 3.2x in 2024.

Leumi’s loan portfolio expanded by 7.4% from Q4 2024 to Q2 2025, reaching NIS 489.2 billion. Growth was particularly strong in the corporate segment, which increased by 12.5% to NIS 154.5 billion. Mortgage lending also showed healthy growth of 3.3% to NIS 151.5 billion during this period.

The bank’s deposit base continues to expand and diversify, growing to NIS 642.3 billion in Q2 2025. Individual deposits, which represent 35.4% of the total deposit base, increased by 1.0% from Q4 2024. The loan-to-deposit ratio stands at a comfortable 76.2%, supporting the bank’s liquidity position, which is further reinforced by a liquidity coverage ratio of 130%.

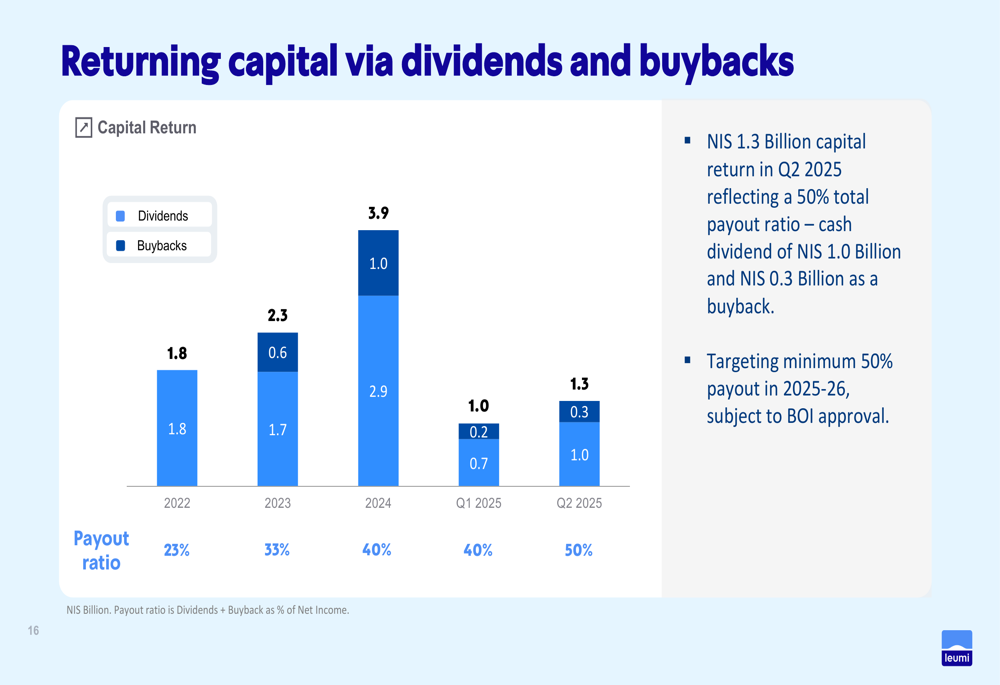

Capital Position and Shareholder Returns

Leumi maintains a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 12.28% as of Q2 2025, well above the regulatory minimum of 10.2%. This solid capital base has enabled the bank to significantly increase returns to shareholders through both dividends and share buybacks.

The following chart illustrates Leumi’s capital return strategy, which has evolved toward higher payout ratios:

In Q2 2025, Leumi returned NIS 1.3 billion to shareholders, representing a 50% payout ratio – NIS 1.0 billion as cash dividend and NIS 0.3 billion through share buybacks. This marks an increase from the 40% payout ratio in Q1 2025 and aligns with management’s stated target of maintaining a minimum 50% payout ratio through 2025-26, subject to regulatory approval.

Forward-Looking Statements

Leumi’s presentation highlights several investment strengths that position the bank for continued success:

Looking ahead, management expects to maintain its focus on targeted loan growth while preserving credit quality. The bank’s efficiency initiatives are expected to continue yielding benefits, supporting profitability despite potential macroeconomic headwinds.

The increased capital return policy signals management’s confidence in Leumi’s financial strength and future earnings capacity. With a solid capital position, diversified revenue streams, and industry-leading efficiency, Leumi appears well-positioned to navigate the evolving economic landscape while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.