Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Lexicon Pharmaceuticals (NASDAQ:LXRX) presented its second quarter 2025 earnings on August 6, highlighting its successful transition to an R&D-focused business model. The company reported a profit for the quarter, a significant turnaround from losses in previous periods, primarily driven by licensing revenue from strategic partnerships.

The stock, which closed at $1.05 on August 5, rose 7.62% to $1.13 in premarket trading following the earnings release, signaling positive investor sentiment about the company’s progress. This represents a substantial recovery from the $0.609 trading price seen after Q1 results, though still well below its 52-week high of $2.175.

Quarterly Performance Highlights

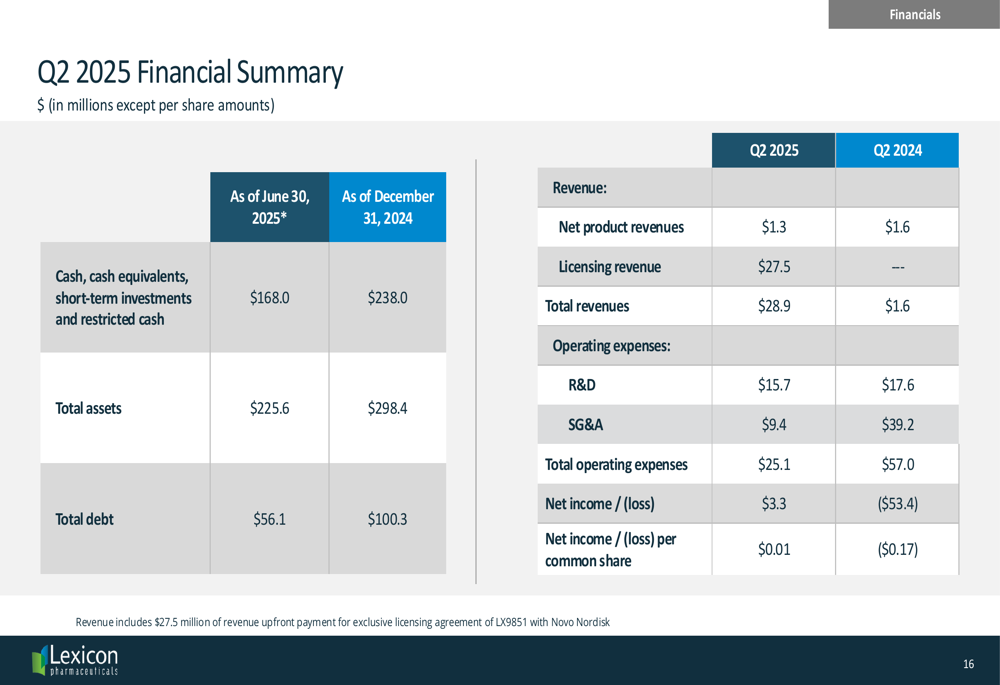

Lexicon reported total revenues of $28.9 million for Q2 2025, compared to just $1.6 million in the same period last year. This dramatic increase was primarily due to $27.5 million in licensing revenue from its agreement with Novo Nordisk (NYSE:NVO) for LX9851. Net product revenues were $1.3 million, slightly down from $1.6 million in Q2 2024.

The company achieved a net income of $3.3 million ($0.01 per share) in Q2 2025, a remarkable improvement from the net loss of $53.4 million (-$0.17 per share) in Q2 2024. This represents Lexicon’s first profitable quarter in recent history and a substantial improvement from the $25.3 million net loss reported in Q1 2025.

As shown in the following financial summary:

Operating expenses decreased significantly to $25.1 million in Q2 2025 from $57.0 million in Q2 2024, reflecting the company’s strategic repositioning. R&D expenses were $15.7 million (down from $17.6 million), while SG&A expenses dropped dramatically to $9.4 million (down from $39.2 million).

Strategic Initiatives

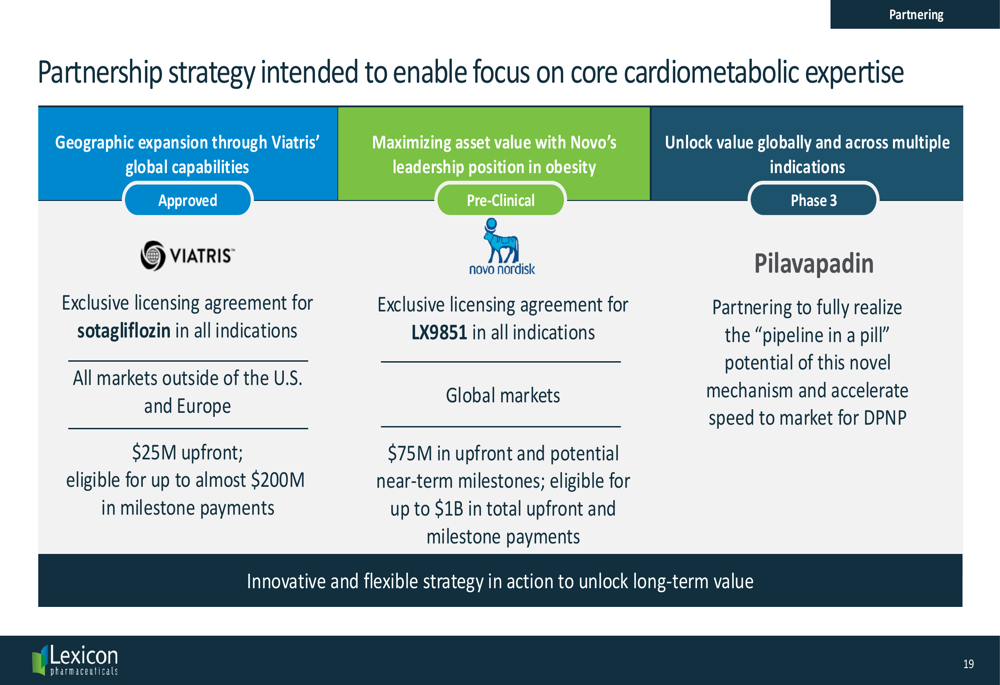

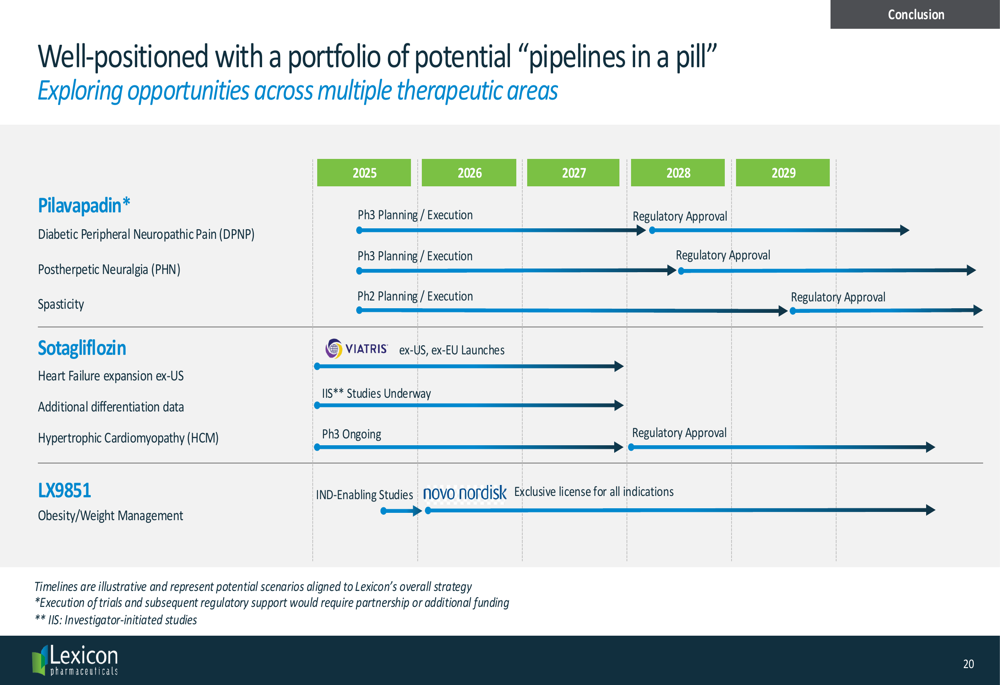

Lexicon’s strategic pivot to an R&D-focused company is yielding results across its pipeline. The company has made significant progress with its three key assets: Pilavapadin, Sotagliflozin, and LX9851.

The company has established strategic partnerships to maximize the value of its assets while focusing on its core cardiometabolic expertise. As illustrated in this partnership strategy overview:

The $45 million upfront payment received from Novo Nordisk in April was used to strengthen Lexicon’s balance sheet by reducing long-term debt from $100.3 million at the end of 2024 to $56.1 million as of June 30, 2025.

Pipeline Progress

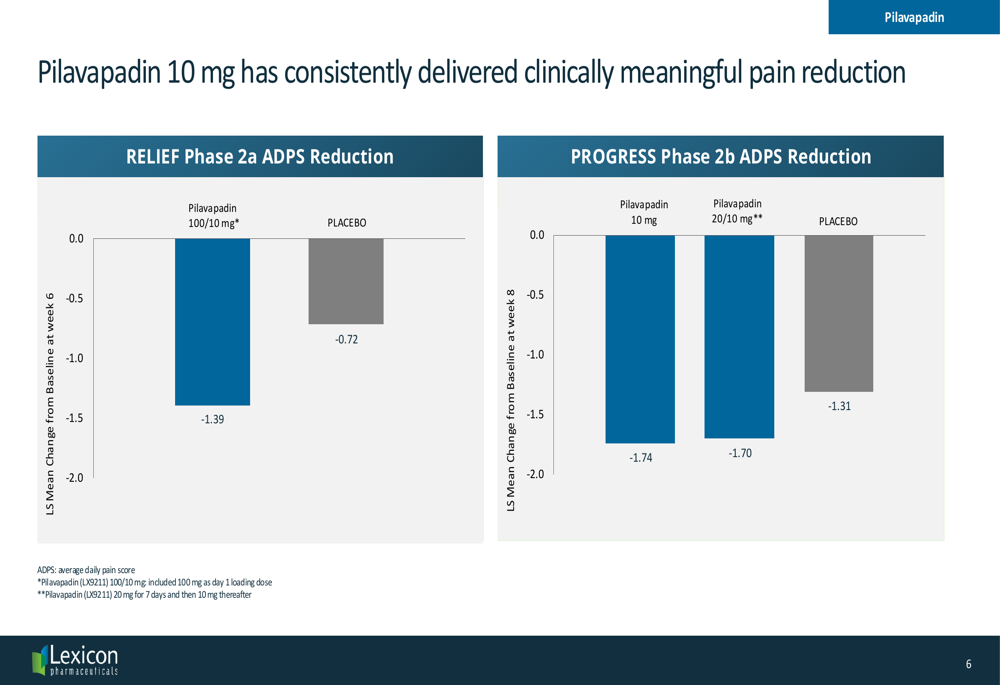

Pilavapadin, Lexicon’s lead pain candidate, demonstrated consistent and clinically meaningful pain reduction in Phase 2 trials for diabetic peripheral neuropathic pain (DPNP). The company plans to present full Phase 2 results in September 2025 and is currently in partnership discussions.

As shown in the following clinical trial results:

Lexicon describes Pilavapadin as "a portfolio in a pill" with multiple potential indications beyond DPNP, including postherpetic neuralgia and spasticity. The drug has patent protection through 2040.

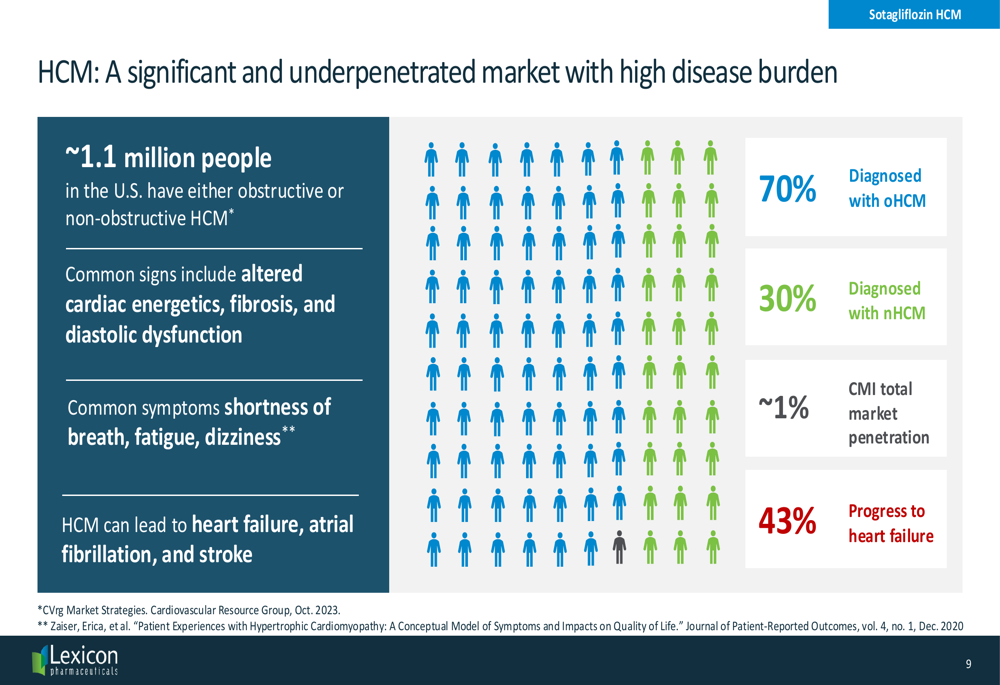

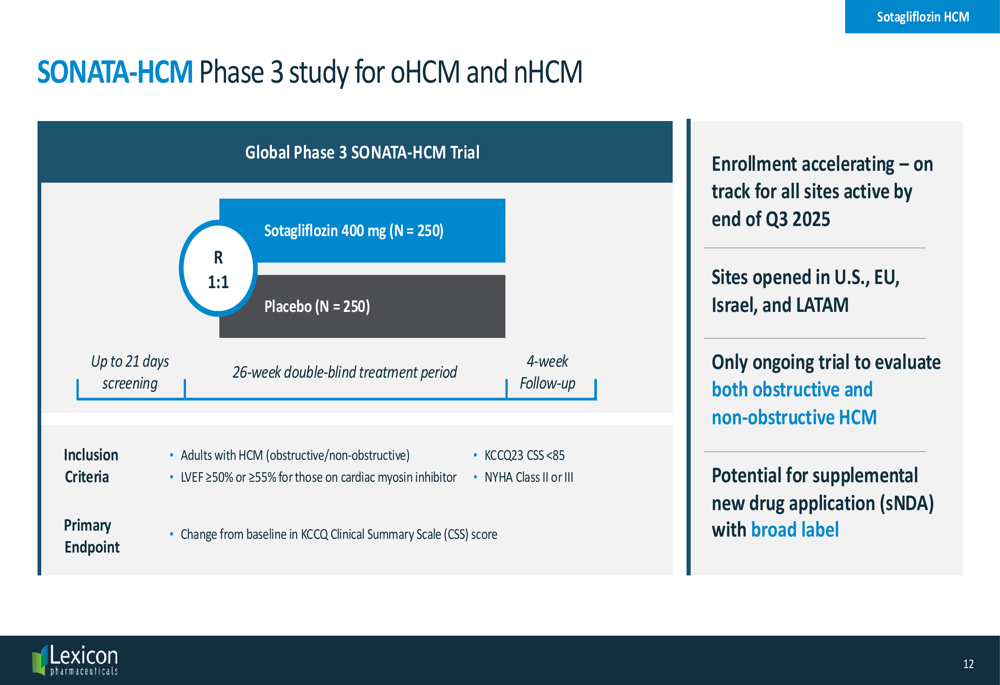

For Sotagliflozin, Lexicon is accelerating site initiations in its Phase 3 SONATA-HCM study for hypertrophic cardiomyopathy (HCM). The company highlights the significant market opportunity in HCM, which affects approximately 1.1 million people in the U.S.

The HCM market represents a substantial opportunity as illustrated here:

Lexicon positions Sotagliflozin as the only HCM agent that works both inside and outside the heart to reduce symptoms and cardiovascular events. The SONATA-HCM Phase 3 study is designed to evaluate the drug in both obstructive and non-obstructive HCM patients:

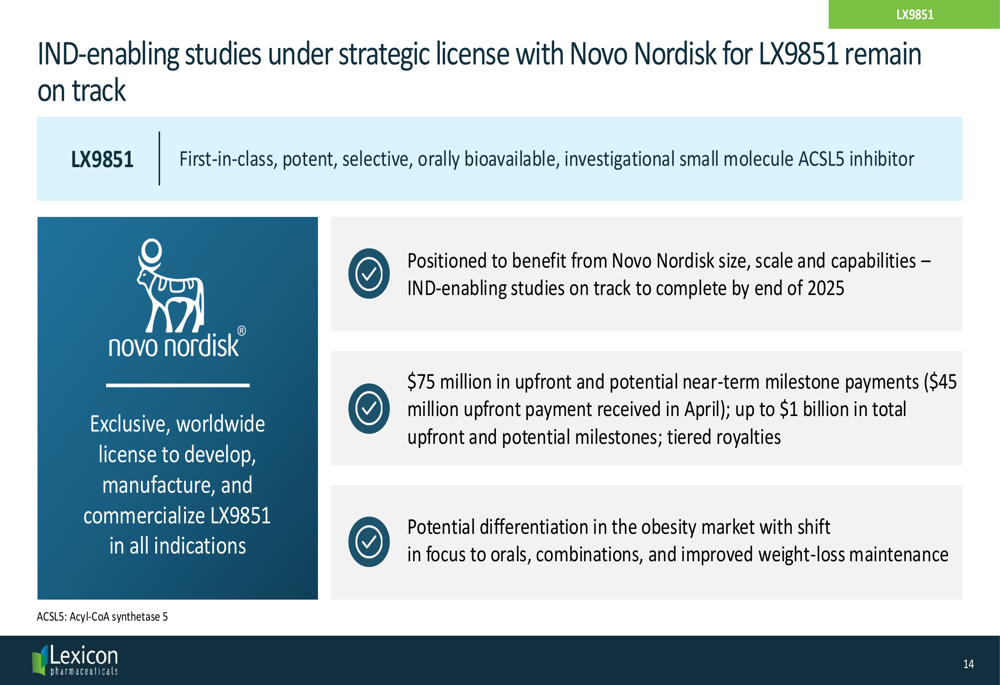

For LX9851, Lexicon’s obesity candidate licensed to Novo Nordisk, IND-enabling studies remain on track to complete by the end of 2025. The partnership includes $75 million in upfront and potential near-term milestone payments, with up to $1 billion in total potential milestones plus tiered royalties.

Detailed Financial Analysis

Lexicon ended Q2 2025 with $168.0 million in cash and cash equivalents, down from $238.0 million at the end of 2024. However, the company significantly improved its debt position, reducing total debt to $56.1 million from $100.3 million at year-end 2024.

The company has revised its full-year 2025 operating expense guidance downward to $105-$115 million from the previous $135-$145 million. R&D expenses are now expected to be between $70-$75 million (previously $100-$105 million), while SG&A guidance remains unchanged at $35-$40 million.

As detailed in the financial highlights:

The revised guidance excludes clinical trial costs related to Phase 3 pivotal studies of pilavapadin, suggesting these would be covered by a potential partnership.

Forward-Looking Statements

Lexicon outlined its pipeline opportunities and upcoming catalysts for the remainder of 2025 and beyond. Key milestones include:

1. Pilavapadin: Full PROGRESS data anticipated in Q3 2025, End of Phase 2 meeting before year-end, and ongoing partnership discussions

2. Sotagliflozin: All Phase 3 SONATA-HCM study sites expected to be running by Q3 2025, with data from investigator-initiated studies beginning late 2025

3. LX9851: Completion of IND-enabling studies by the end of 2025

The company presented a timeline of potential regulatory approvals extending through 2029, including possible approvals for pilavapadin in DPNP and postherpetic neuralgia by 2028, and sotagliflozin in HCM by 2028.

Lexicon’s strategic repositioning appears to be yielding positive results, with reduced expenses, strategic partnerships generating revenue, and pipeline advancement across multiple assets. The return to profitability in Q2 2025, albeit driven by one-time licensing revenue, represents a significant milestone in the company’s transformation into an R&D-focused organization.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.