U.S. may expand Nvidia and AMD’s 15% China chips deal to other companies

Introduction & Market Context

LifeStance Health Group Inc. (NASDAQ:LFST) presented its Q2 2025 earnings results on August 7, 2025, showcasing continued growth in revenue and improved profitability metrics. The mental healthcare provider’s shares jumped 6.67% in premarket trading to $4.16, reflecting positive investor sentiment following the company’s raised full-year guidance.

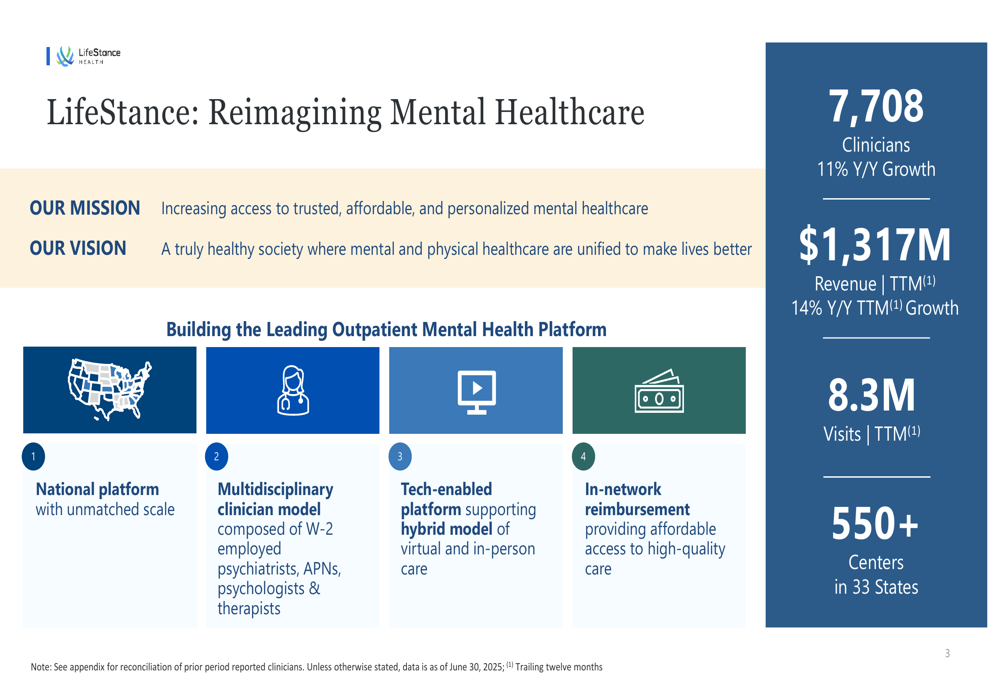

The company continues to expand its national mental healthcare platform, which now includes over 7,700 clinicians across 550+ centers in 33 states. LifeStance’s business model focuses on providing affordable, accessible mental healthcare through a combination of in-person and virtual visits, with all services covered by insurance networks.

As shown in the following platform overview, LifeStance has established itself as a major player in the mental healthcare space with significant scale and reach:

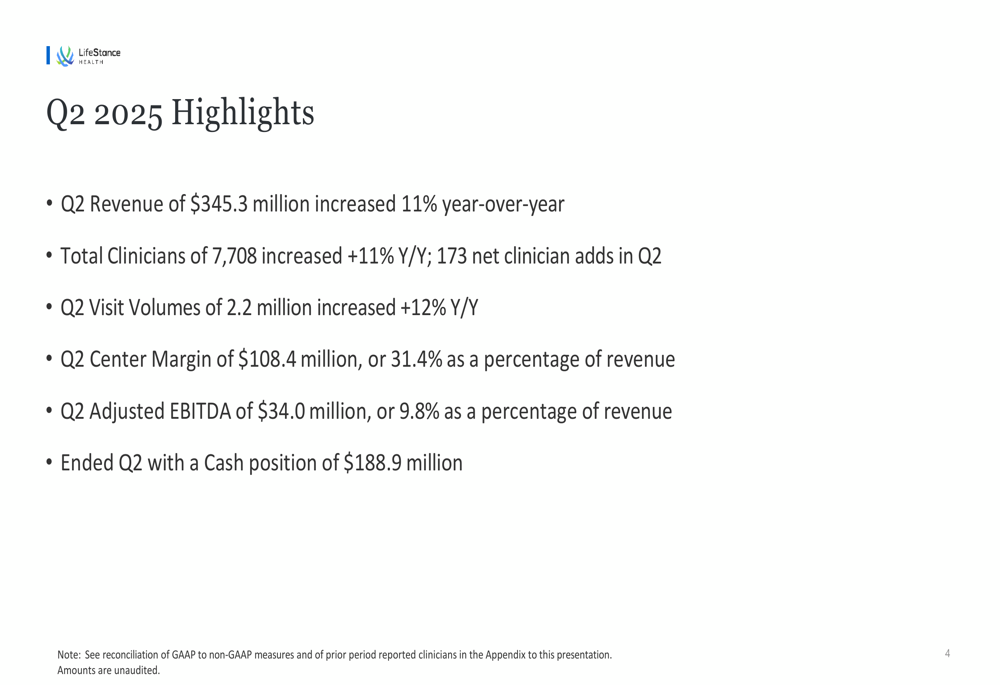

Quarterly Performance Highlights

LifeStance reported Q2 2025 revenue of $345.3 million, representing an 11% increase year-over-year. The company’s clinician base grew at the same rate, reaching 7,708 clinicians (up 11% from Q2 2024), with 173 net clinician additions during the quarter. Visit volumes increased 12% year-over-year to 2.2 million for the quarter.

The company’s Q2 Center Margin reached $108.4 million, or 31.4% of revenue, while Adjusted EBITDA grew to $34.0 million, representing 9.8% of revenue and a 19% increase compared to the same period last year. This performance demonstrates LifeStance’s ability to scale efficiently while improving profitability metrics.

The following slide summarizes these key performance highlights:

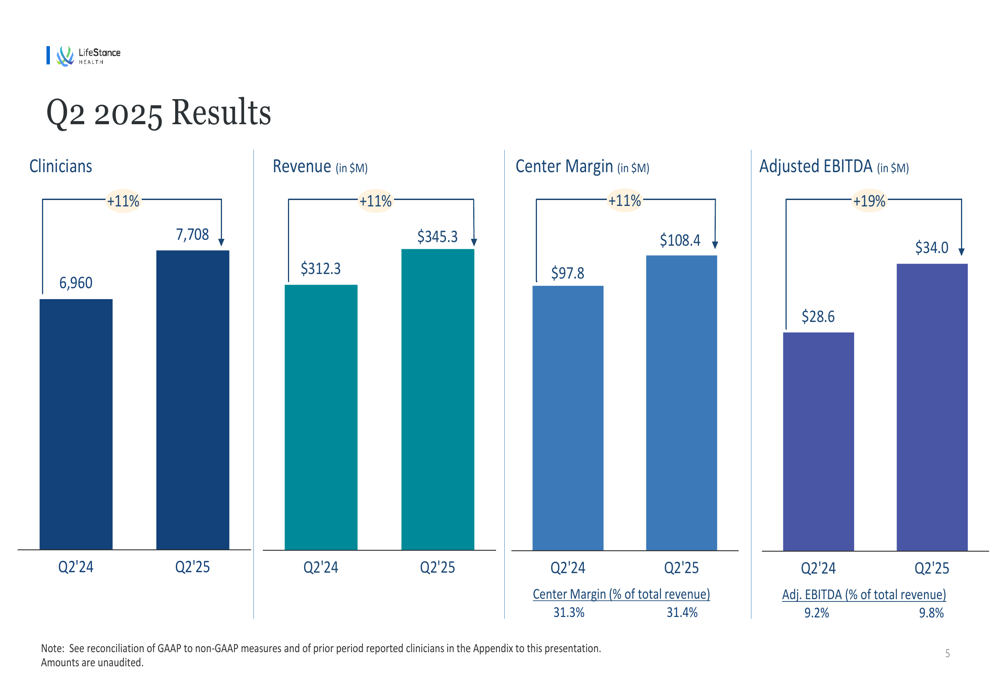

A visual comparison of Q2 2025 results against the prior year clearly illustrates the company’s growth trajectory across all key metrics:

Financial Position and Capital Allocation

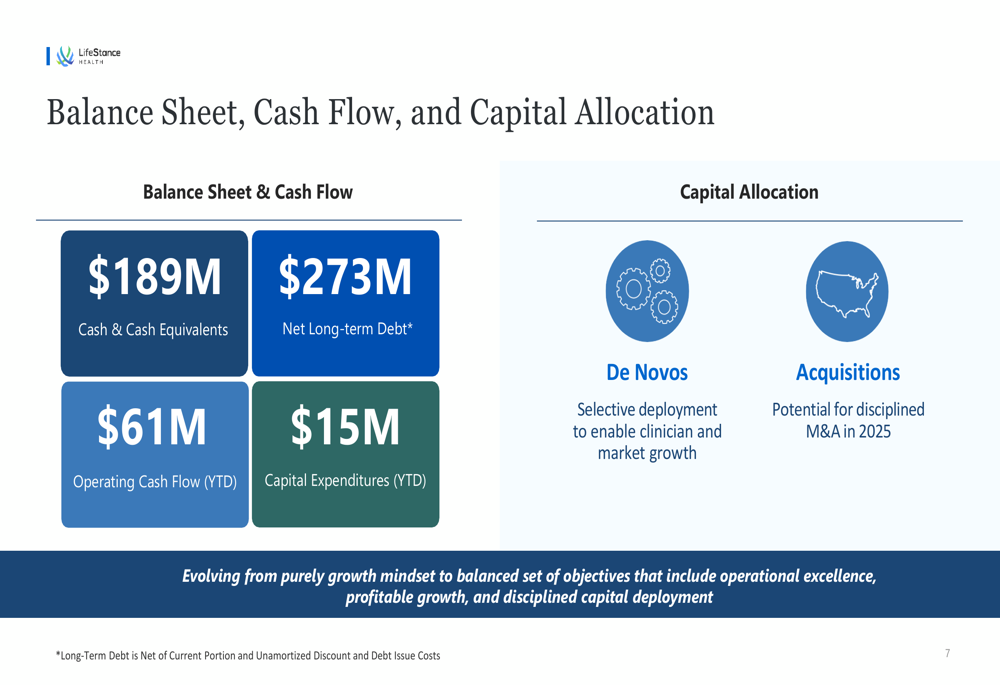

LifeStance ended Q2 2025 with a strong cash position of $188.9 million, while carrying $273 million in net long-term debt. The company reported $61 million in operating cash flow year-to-date and $15 million in capital expenditures. Free cash flow for Q2 2025 reached $56.6 million, a significant improvement from $38.9 million in Q2 2024.

The company’s capital allocation strategy is evolving from what management described as a "purely growth mindset" to a "balanced set of objectives" that include operational excellence, profitable growth, and disciplined capital deployment. LifeStance continues to invest selectively in de novo centers to enable clinician and market growth, while also considering potential acquisitions in the second half of 2025.

The following slide details the company’s financial position and capital allocation approach:

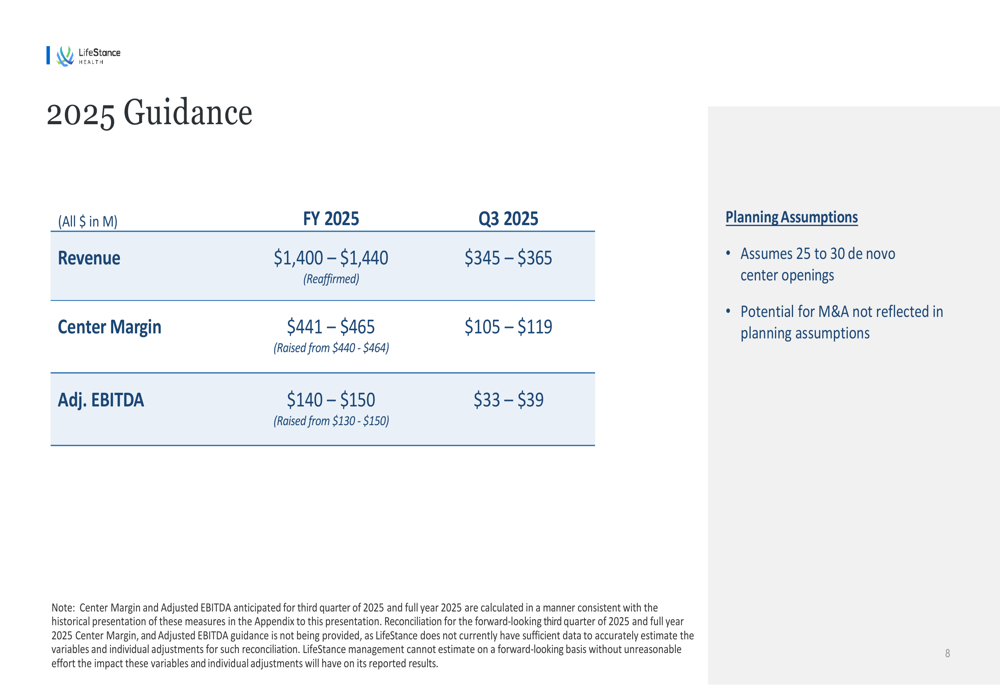

Raised 2025 Guidance

In a significant vote of confidence in its business model and growth trajectory, LifeStance raised its full-year 2025 guidance for Center Margin and Adjusted EBITDA. While reaffirming its revenue guidance of $1,400-$1,440 million, the company increased its Center Margin guidance to $441-$465 million (from $440-$464 million) and Adjusted EBITDA guidance to $140-$150 million (from $130-$150 million).

For Q3 2025, LifeStance expects revenue of $345-$365 million, Center Margin of $105-$119 million, and Adjusted EBITDA of $33-$39 million. The company plans to open 25-30 de novo centers in 2025 and notes that its guidance does not reflect potential M&A activity.

The following slide details the company’s updated guidance:

Strategic Initiatives and Outlook

LifeStance continues to execute on its mission of increasing access to trusted, affordable, and personalized mental healthcare. The company’s tech-enabled platform supports a hybrid model of virtual and in-person care, allowing for flexibility in service delivery while maintaining high-quality care standards.

The company’s evolution toward a more balanced approach to growth and profitability suggests a maturing business model. With consistent growth across key metrics over five consecutive quarters, LifeStance appears well-positioned to capitalize on the ongoing demand for mental health services.

While the company reported a net loss of $3.8 million for Q2 2025, this represents an improvement from previous quarters, continuing the positive trend seen in Q1 2025 when the company achieved its first positive net income of $700,000. The raised guidance for Center Margin and Adjusted EBITDA indicates management’s confidence in further operational improvements throughout the remainder of 2025.

Despite trading well below its 52-week high of $8.61, LifeStance’s stock has shown resilience, with the positive market reaction to Q2 results suggesting investor optimism about the company’s growth trajectory and improved profitability metrics. As the company continues to expand its clinician base and service offerings while focusing on operational excellence, it remains a significant player in the rapidly evolving mental healthcare landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.