US stock futures steady after Wall St soars on dovish Powell; Nvidia earnings due

Introduction & Market Context

Limbach Holdings Inc (NASDAQ:LMB) presented its Q1 2025 investor presentation on May 6, 2025, highlighting the company’s strategic transformation into a building systems solutions firm focused on mission-critical infrastructure. The presentation comes after Limbach reported strong Q4 2024 results that exceeded EPS expectations, driving the stock price to $103.33, near its 52-week high of $107.

The company has positioned itself as a specialist in revitalizing and maintaining mission-critical systems in existing facilities across six key vertical markets: Healthcare, Industrial & Manufacturing, Data Centers, Life Sciences, Higher Education, and Cultural & Entertainment.

Strategic Business Model Shift

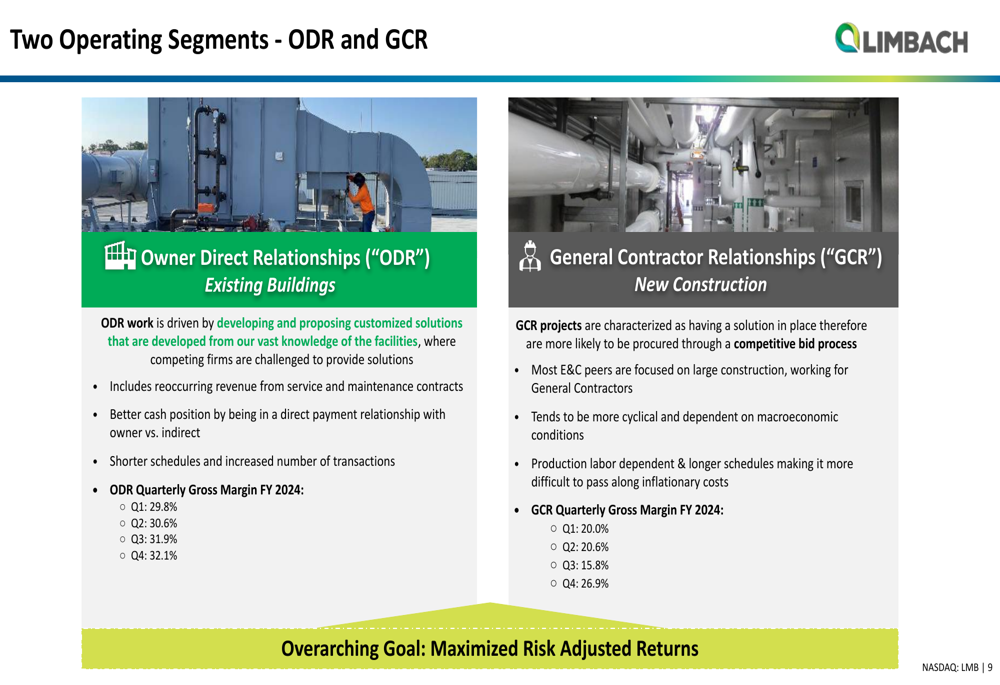

Limbach’s presentation emphasized its strategic shift toward Owner Direct Relationships (ODR), which generate approximately 30% gross margins, versus General Contractor Relationships (GCR) with approximately 20% gross margins. This transformation has been central to the company’s improved profitability despite relatively flat total revenue.

As shown in the following breakdown of Limbach’s two operating segments, the company has clearly defined the advantages of its ODR-focused approach:

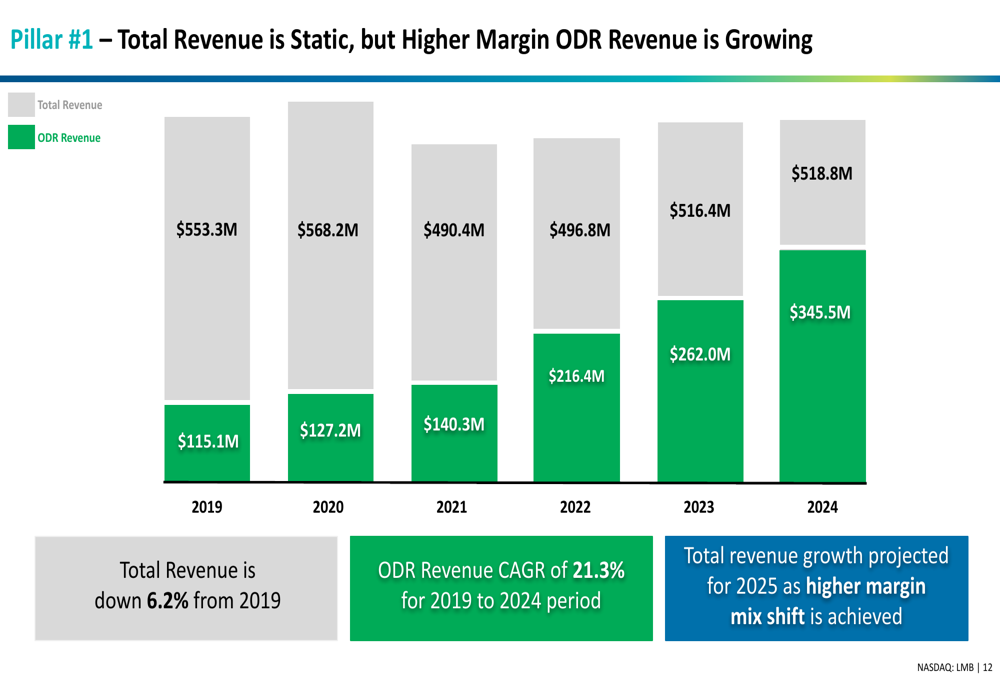

The shift toward ODR has been dramatic, with this segment growing from $115.1M in 2019 to $345.5M in 2024, representing a 21.3% CAGR. Meanwhile, total revenue has remained relatively static, declining 6.2% from $553.3M in 2019 to $518.8M in 2024, as the company strategically reduced its lower-margin GCR business.

Financial Performance Highlights

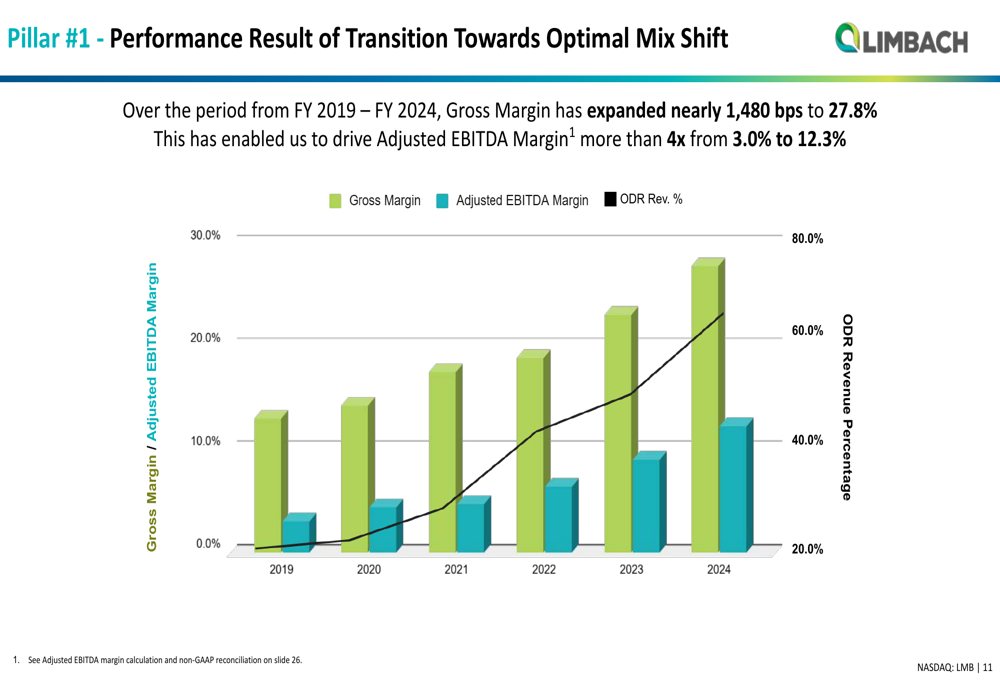

The strategic shift toward higher-margin ODR business has driven significant financial improvements. Gross margin expanded nearly 1,480 basis points to 27.8% from 2019 to 2024, while Adjusted EBITDA margin increased more than four-fold from 3.0% to 12.3% during the same period.

The following chart illustrates this impressive margin expansion correlated with the increasing percentage of ODR revenue:

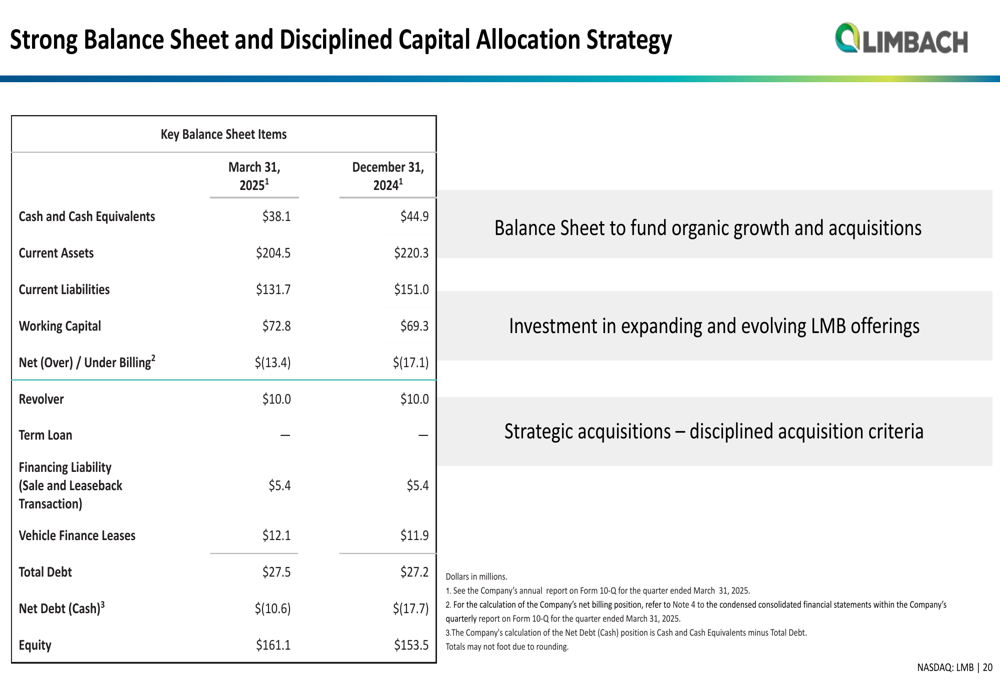

Limbach’s balance sheet remains strong, with $38.1M in cash and cash equivalents as of March 31, 2025, and total debt of $27.5M, resulting in a net cash position of $10.6M. This financial strength supports the company’s disciplined capital allocation strategy focused on organic growth, expanded offerings, and strategic acquisitions.

Growth Strategy and Recent Acquisitions

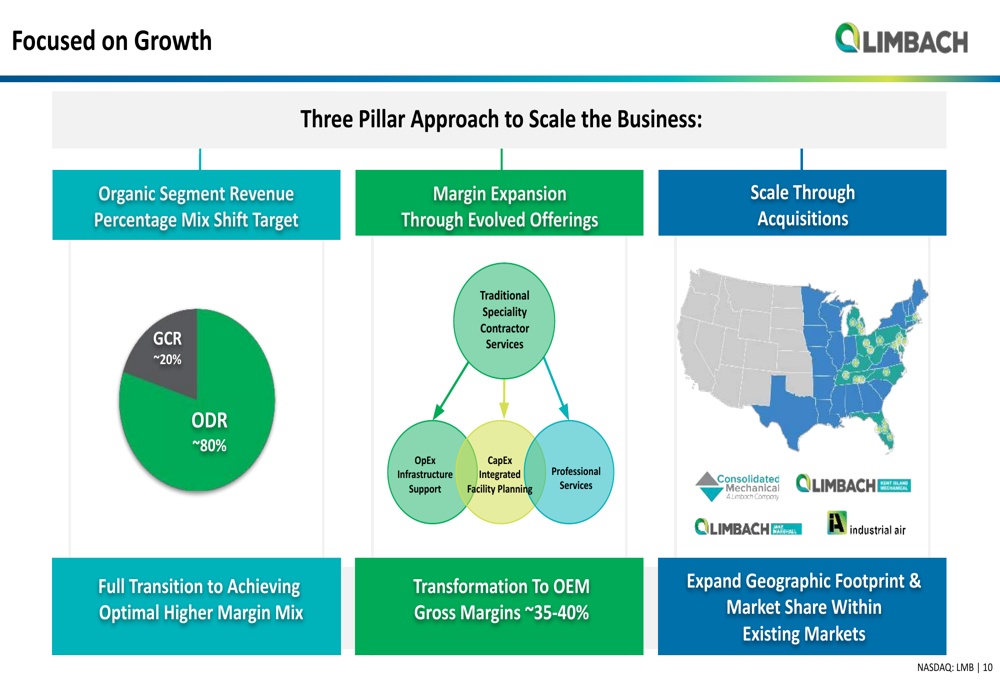

Limbach outlined a three-pillar approach to scaling its business: Organic Segment Revenue, Margin Expansion, and Scale Through Acquisitions. The company is targeting an optimal mix of 80% ODR and 20% GCR, while developing traditional specialty contractor services into higher-margin offerings.

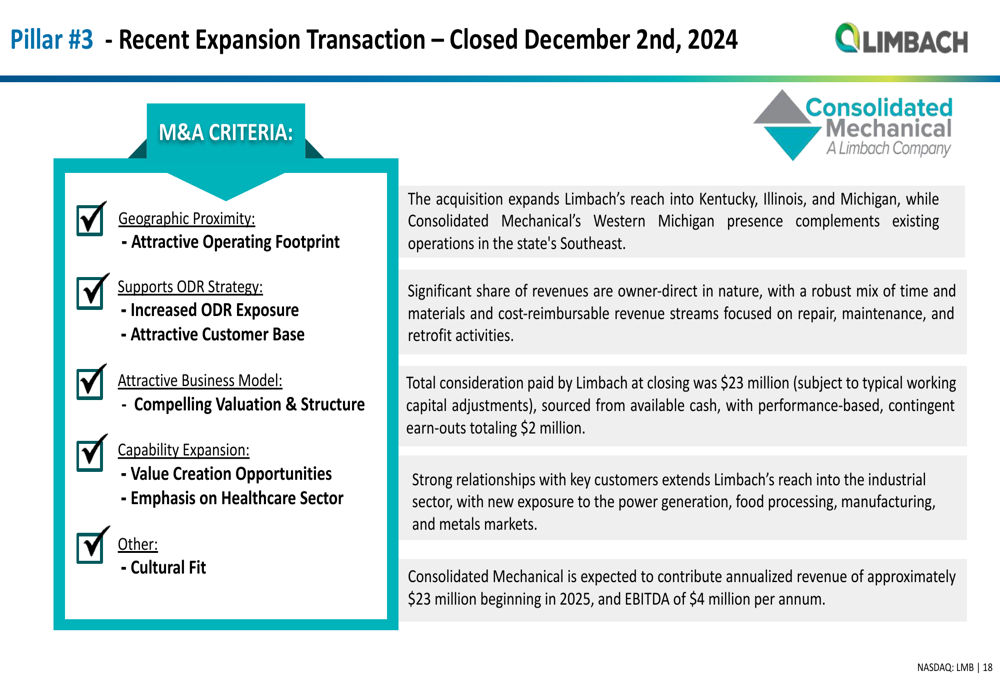

The acquisition strategy has been active, with two significant transactions in recent months. In December 2024, Limbach acquired Consolidated Mechanical, expanding its reach into Kentucky, Illinois, and Michigan. This acquisition is expected to contribute approximately $23 million in annualized revenue and $4 million in EBITDA beginning in 2025.

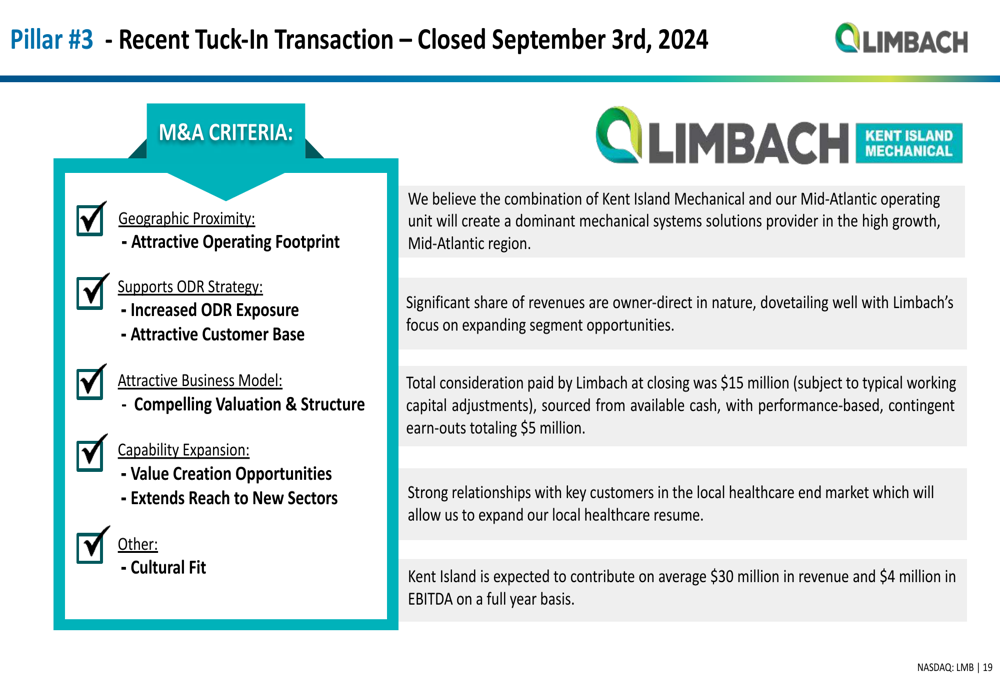

Earlier, in September 2024, the company completed a tuck-in acquisition of Kent Island Mechanical, which is expected to contribute on average $30 million in revenue and $4 million in EBITDA on a full-year basis.

Q1 2025 Results and 2025 Outlook

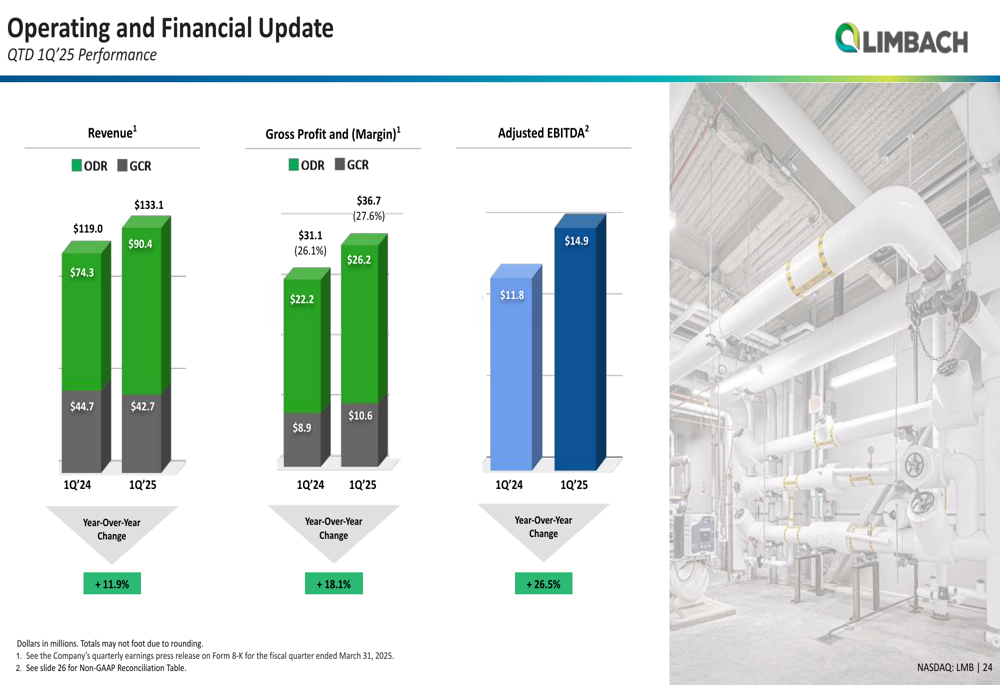

Limbach’s Q1 2025 performance showed continued momentum in its strategic transformation. ODR revenue increased from $74.3M to $90.4M, while GCR revenue decreased slightly from $44.7M to $42.7M. Gross profit improved to $36.7M from $31.1M, and Adjusted EBITDA rose to $14.9M from $11.8M in the same quarter of the previous year.

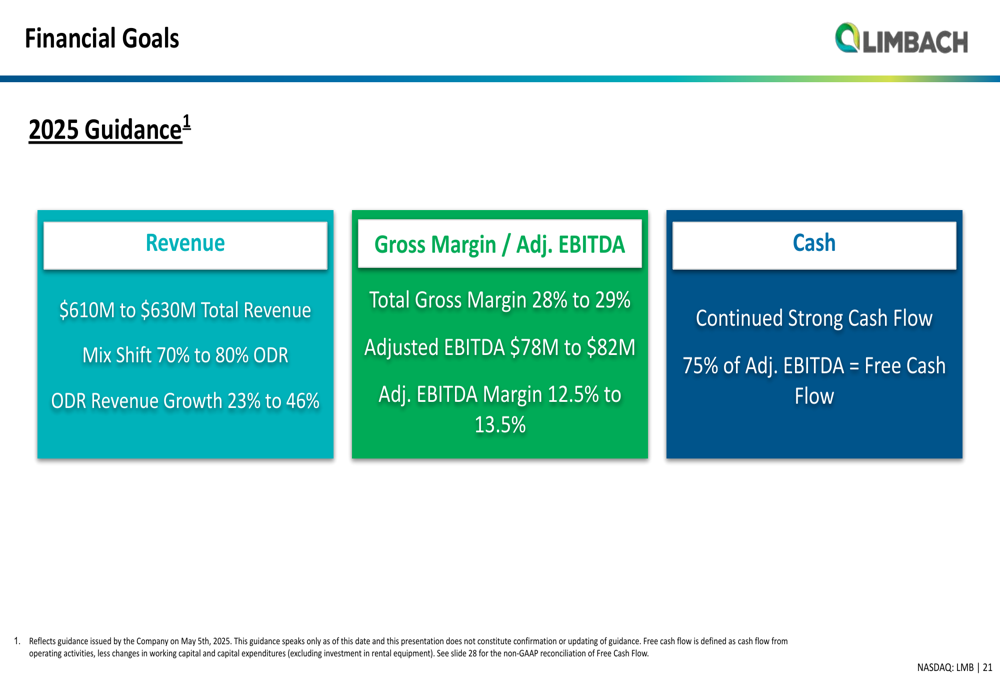

Looking ahead to full-year 2025, Limbach provided optimistic guidance, projecting:

- Revenue of $610M to $630M

- ODR revenue growth of 23% to 46%

- Total (EPA:TTEF) gross margin of 28% to 29%

- Adjusted EBITDA of $78M to $82M

- Adjusted EBITDA margin of 12.5% to 13.5%

- Strong cash flow conversion with 75% of Adjusted EBITDA converting to Free Cash Flow

Competitive Positioning and Market Opportunities

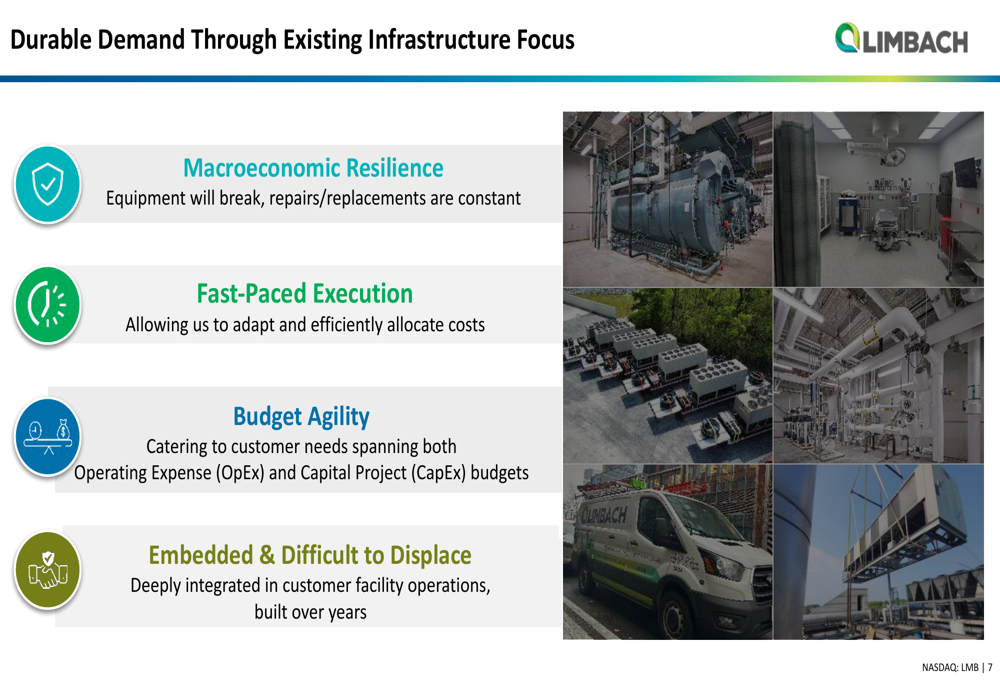

Limbach has positioned itself as a differentiated player in the building systems market by focusing on existing infrastructure rather than new construction. This approach provides several competitive advantages, including macroeconomic resilience, fast-paced execution, budget agility, and deep integration with customer operations.

The company’s focus on existing infrastructure creates durable demand through economic cycles, as equipment will inevitably require repairs and replacements regardless of broader economic conditions. This strategy has allowed Limbach to build strong relationships with building owners and develop recurring revenue streams.

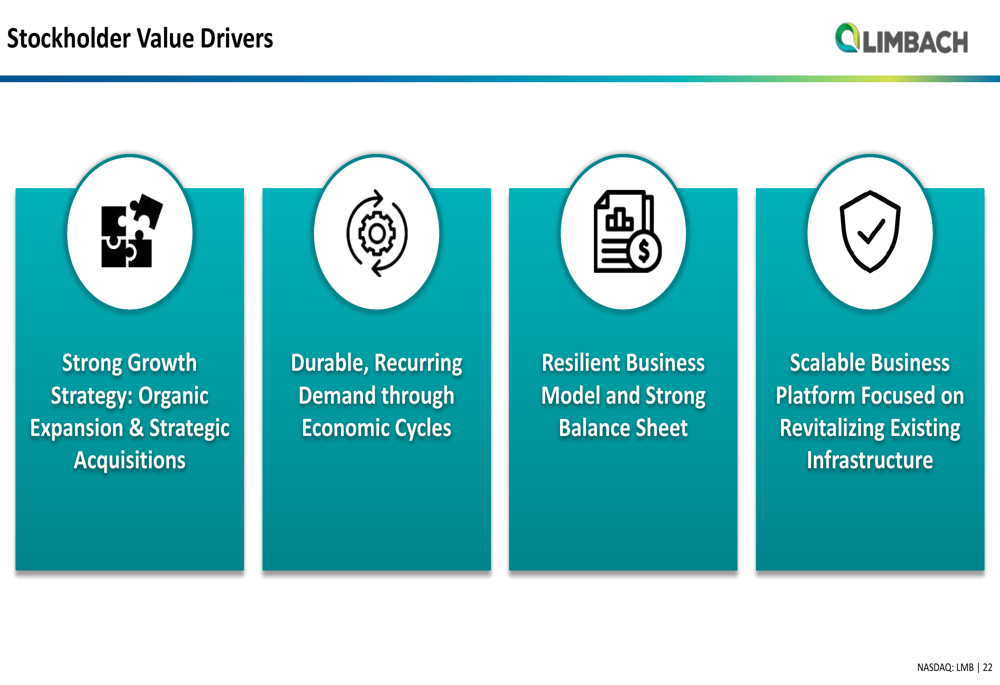

Limbach’s stockholder value proposition centers on four key drivers: a strong growth strategy combining organic expansion and strategic acquisitions; durable, recurring demand through economic cycles; a resilient business model supported by a strong balance sheet; and a scalable business platform focused on revitalizing existing infrastructure.

In conclusion, Limbach’s Q1 2025 presentation demonstrates how the company’s strategic shift toward higher-margin Owner Direct Relationships has driven significant financial improvements despite relatively flat total revenue. With a strong balance sheet, clear growth strategy, and favorable market positioning in mission-critical infrastructure, Limbach appears well-positioned for continued growth and margin expansion in 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.