BofA warns Fed risks policy mistake with early rate cuts

Linamar Corporation (TSX:LNR) reported improved profitability and market share gains despite revenue declines in its Q1 2025 earnings presentation on May 7. The Canadian manufacturing company achieved normalized earnings growth in both its Industrial and Mobility segments while navigating challenging market conditions.

Quarterly Performance Highlights

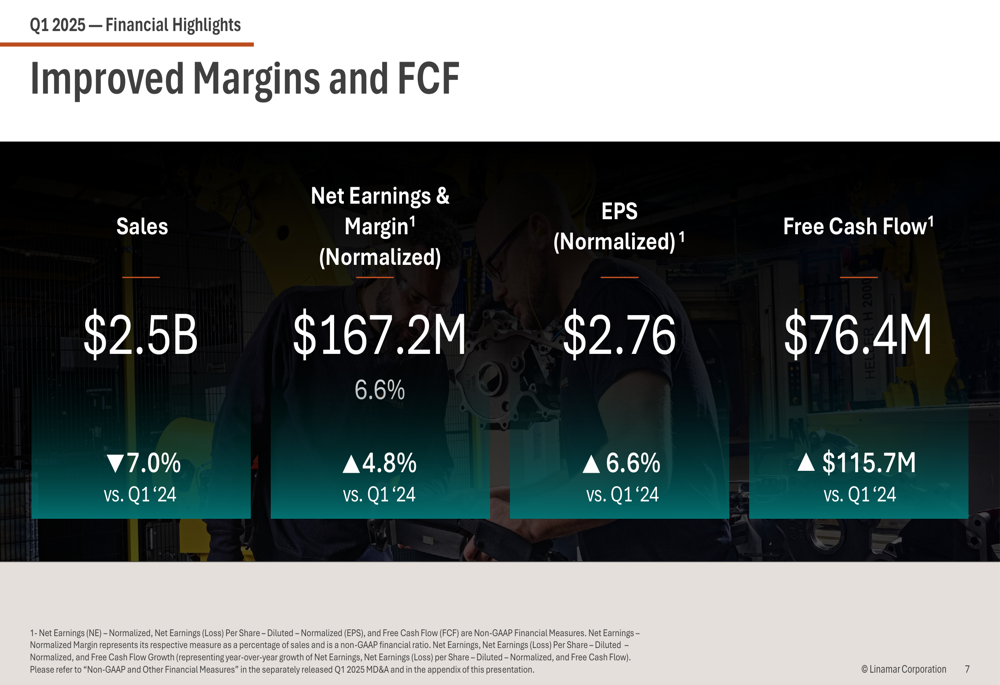

Linamar reported Q1 2025 sales of $2.5 billion, down 7.0% compared to the same period last year, but delivered normalized net earnings of $167.2 million, representing a 4.8% year-over-year increase. Normalized earnings per share grew 6.6% to $2.76, reflecting the company’s operational efficiency improvements and cost reduction initiatives.

As shown in the following financial highlights slide, free cash flow reached $76.4 million, though this marked a decrease from Q1 2024:

"Normalized earnings are up overall and in both segments despite down markets," noted the company in its executive summary. "Solid cost reductions and enhanced operational efficiency drives Normalized OE margin to 10%."

Segment Performance Analysis

The Industrial segment, which includes Skyjack access equipment and agricultural products, reported Q1 revenue of $633.4 million, down 13.1% year-over-year. However, normalized operating earnings increased 5.3% to $126.6 million, with margins expanding significantly from 16.5% to 20.0%.

The following chart illustrates the Industrial segment’s financial performance:

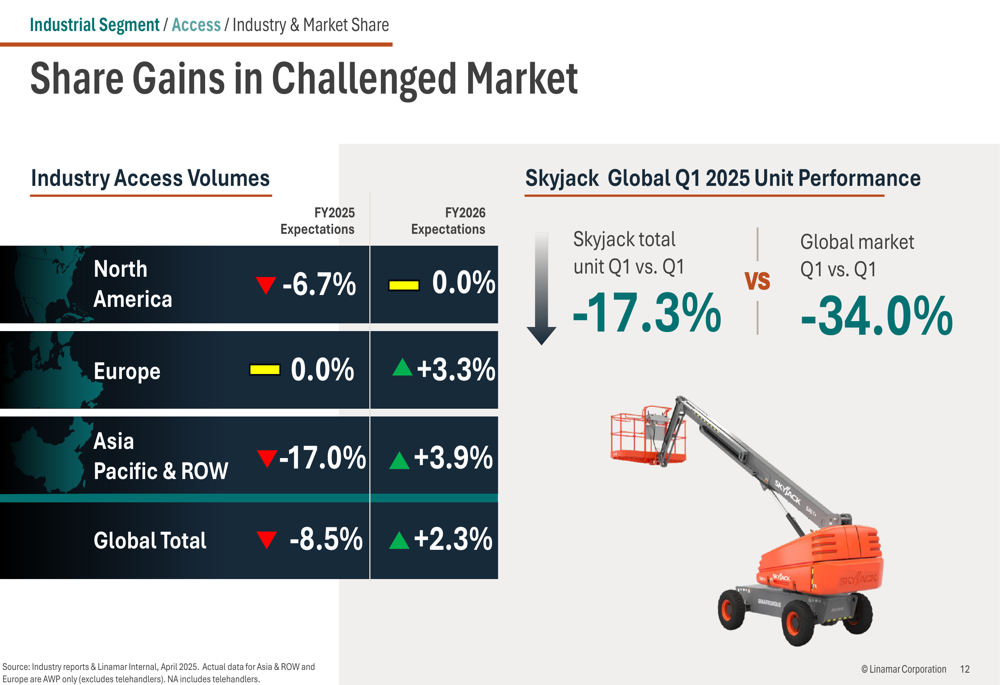

Skyjack outperformed its market significantly, with unit sales declining 17.3% compared to the global market’s 34.0% contraction. This market share gain helped cushion the impact of challenging industry conditions.

As shown in the following slide, Skyjack’s performance relative to the broader market demonstrates its competitive strength:

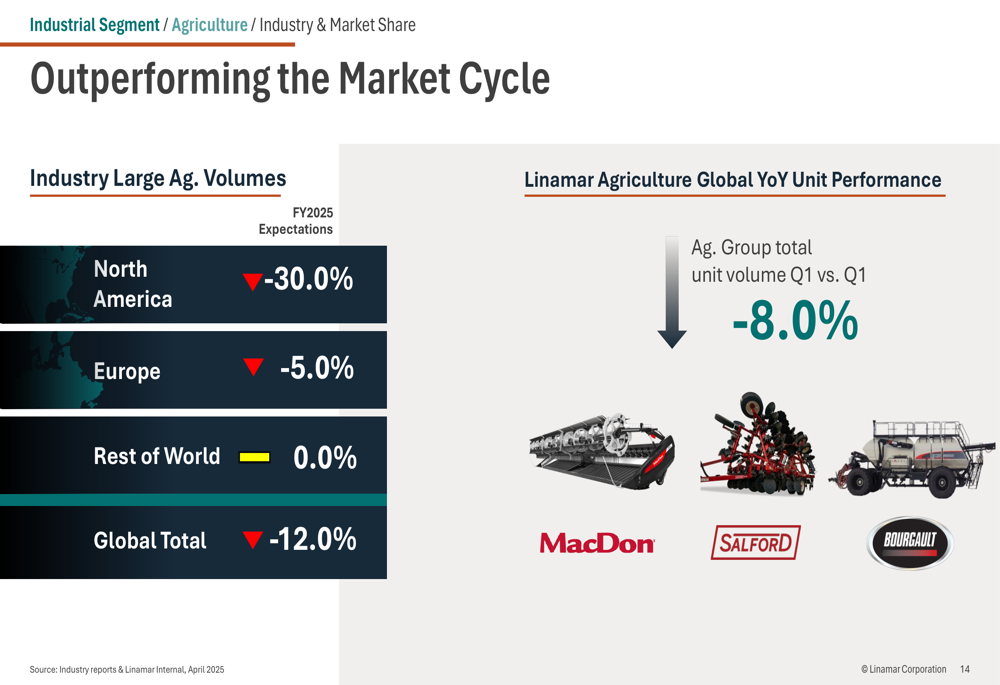

Similarly, Linamar’s Agricultural Group outperformed industry trends with an 8.0% decline in unit volume compared to the global market’s 12.0% drop:

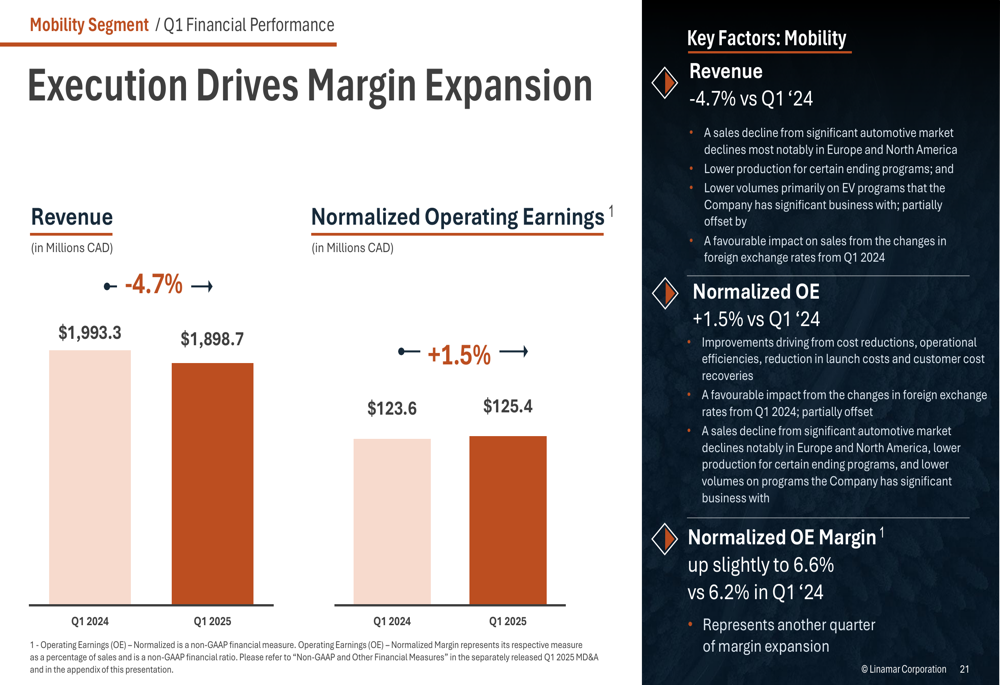

The Mobility segment, which manufactures automotive components, reported revenue of $1.9 billion, down 4.7% year-over-year. Despite this, normalized operating earnings increased 1.5% to $125.4 million, with margins improving slightly from 6.2% to 6.6%.

The company highlighted its continued content per vehicle growth in North America (+1.4% to $300.79) and Asia Pacific (+8.0% to $11.76), though Europe saw a 5.0% decline to $99.06.

Strategic Initiatives & Market Positioning

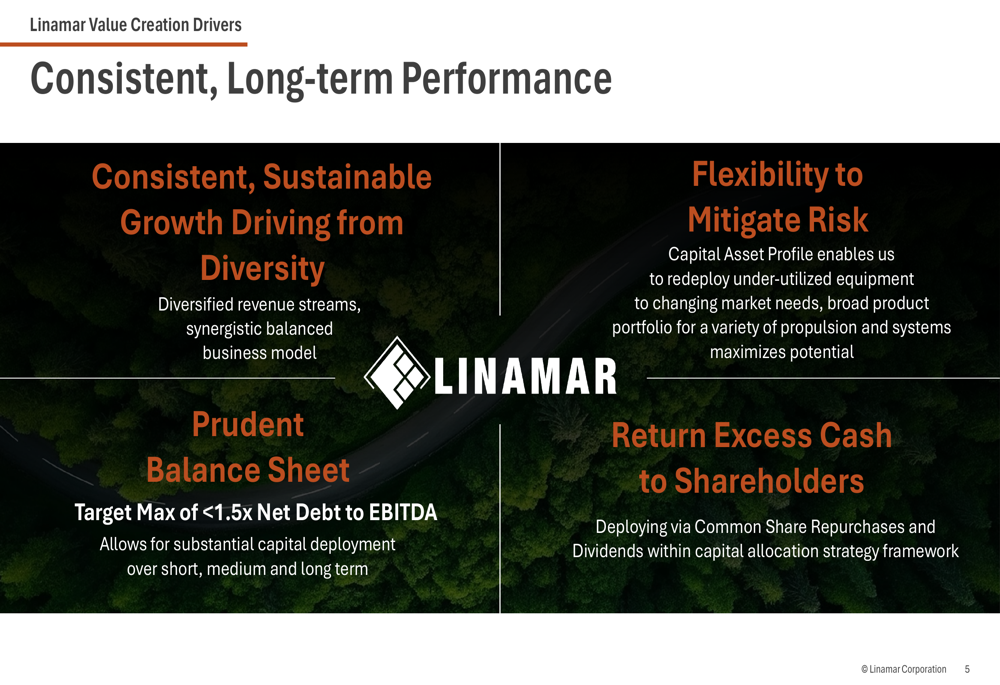

Linamar’s value creation strategy centers on four key drivers: consistent growth through diversification, prudent balance sheet management, flexibility to mitigate risk, and returning excess cash to shareholders.

The following slide outlines these strategic priorities:

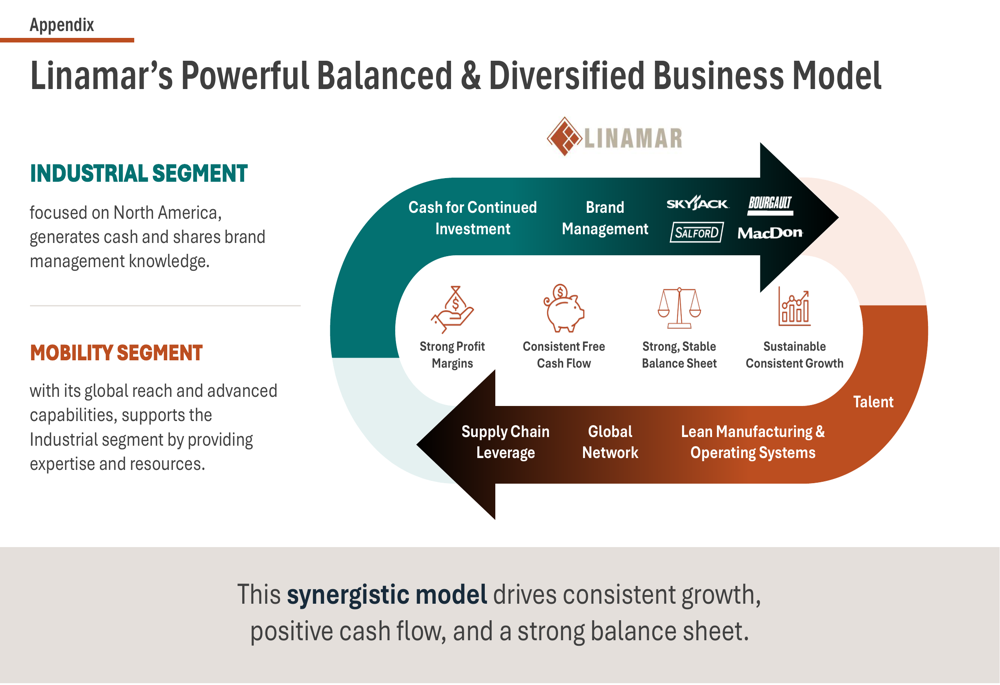

The company’s balanced and diversified business model continues to provide resilience against market volatility:

Linamar highlighted its success in winning takeover work worth approximately $200 million, including a rear floor assembly for an electric commercial van in Europe, steering knuckles for a major North American OEM, and cylinder head assemblies for a European manufacturer.

The company’s operational excellence was recognized by General Motors (NYSE:GM), which named Linamar a 2024 Supplier of the Year:

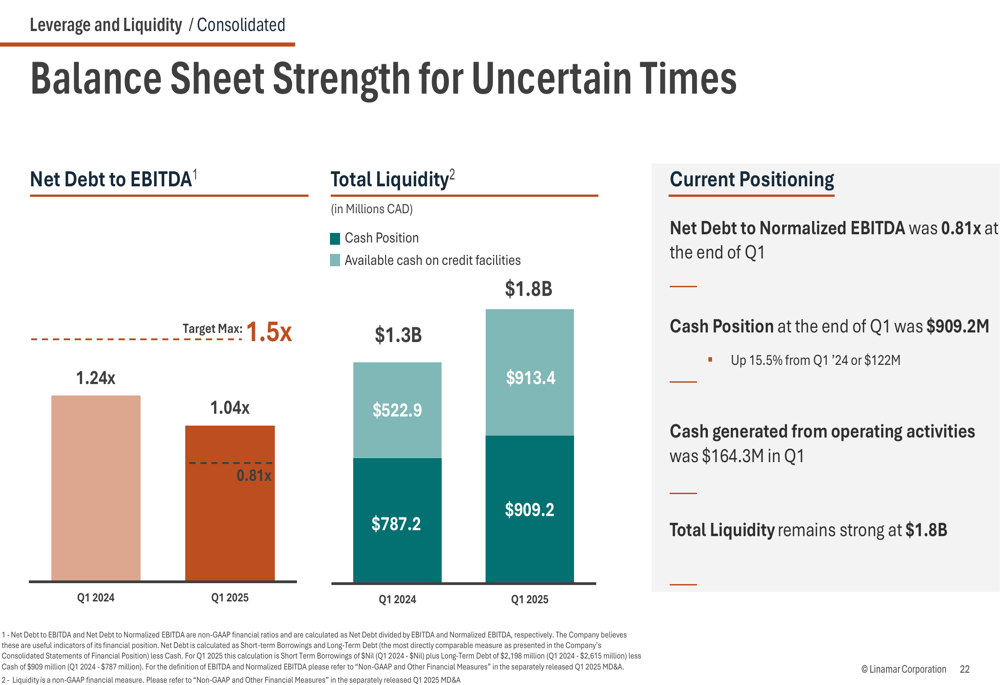

Balance Sheet & Capital Allocation

Linamar maintained a strong financial position with Net Debt to Normalized EBITDA of 0.81x at the end of Q1, well below its target maximum of 1.5x. Cash position increased 15.5% to $909.2 million, with total liquidity of $1.8 billion.

The following slide illustrates the company’s balance sheet strength:

The company continues to execute its share repurchase program initiated in November 2024, having retired nearly 1.8 million shares and returned almost $100 million to shareholders to date. The current program allows for the repurchase of up to 4,021,282 shares, representing 10% of the public float.

Forward-Looking Statements

Looking ahead, Linamar expects Q2 2025 mobility segment sales to be flat year-over-year, while the industrial segment is projected to experience a double-digit decline compared to Q2 2024.

For the full year 2025, the auto industry outlook has been revised downward, with global light vehicle volumes expected to decline 1.7% before returning to 1.1% growth in 2026. The company noted that industry experts have factored in the negative impact of tariffs on these projections.

Linamar indicated that U.S. tariffs would have minimal direct impact on its operations, and suggested potential opportunities as automakers onshore parts supply over the next three years.

The company’s stock closed at $52.14 on May 7, up 1.8% for the day, and has traded between $43.84 and $73.84 over the past 52 weeks.

Linamar will host an Investor Tech Day on May 15, 2025, in Guelph, Ontario, featuring executive management presentations and showcasing the latest technologies from each segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.