Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

Liquidia Technologies Inc (NASDAQ:LQDA) presented its second quarter 2025 financial results and corporate update on August 12, 2025, highlighting the company’s first quarter of product sales following the FDA approval of Yutrepia (inhalation treprostinil powder) on May 23, 2025. The stock responded positively to the results, trading up 13.07% in premarket to $23.97, significantly above its 52-week range of $8.26-$21.27.

The presentation focused primarily on the early commercial success of Yutrepia, clinical data supporting its efficacy and tolerability, and the company’s financial position as it transitions from a development-stage to a commercial-stage biopharmaceutical company.

Quarterly Performance Highlights

Liquidia reported total revenue of $8.84 million for Q2 2025, representing a 141% increase from $3.66 million in the same period last year. This growth was primarily driven by the introduction of product sales, which contributed $6.52 million in the first partial quarter of Yutrepia’s commercial availability.

As shown in the following financial summary from the presentation:

Despite the revenue growth, Liquidia’s operating loss widened to $37.51 million compared to $27.20 million in Q2 2024, reflecting the significant investments in commercialization efforts. The company ended the quarter with a strong cash position of $173 million, bolstered by approximately $50 million received in June 2025 from the second tranche of HCRx financing, which was triggered by the first Yutrepia sales.

Yutrepia Launch and Adoption

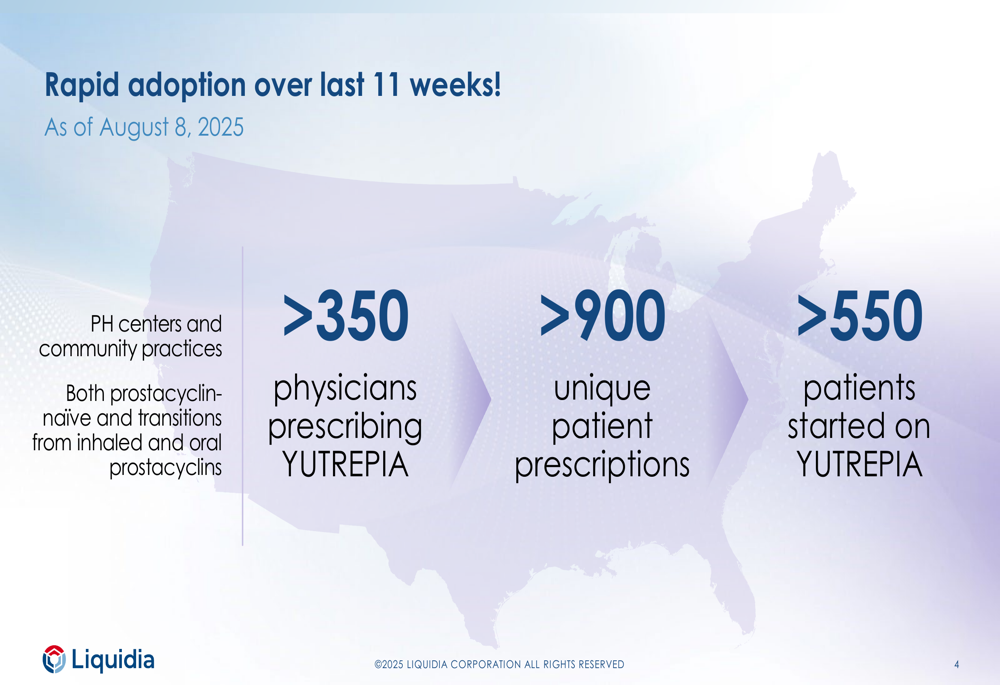

Following FDA approval in May 2025, Liquidia reported impressive early adoption metrics for Yutrepia. As of August 8, 2025, just 11 weeks post-launch, the company has seen rapid uptake across both pulmonary hypertension centers and community practices.

The following slide illustrates the strong initial market penetration:

With over 350 physicians already prescribing the treatment, more than 900 unique patient prescriptions written, and over 550 patients having started therapy, the initial commercial performance suggests strong market acceptance. The company noted that adoption spans both prostacyclin-naïve patients and those transitioning from inhaled and oral prostacyclins.

Clinical Data Insights

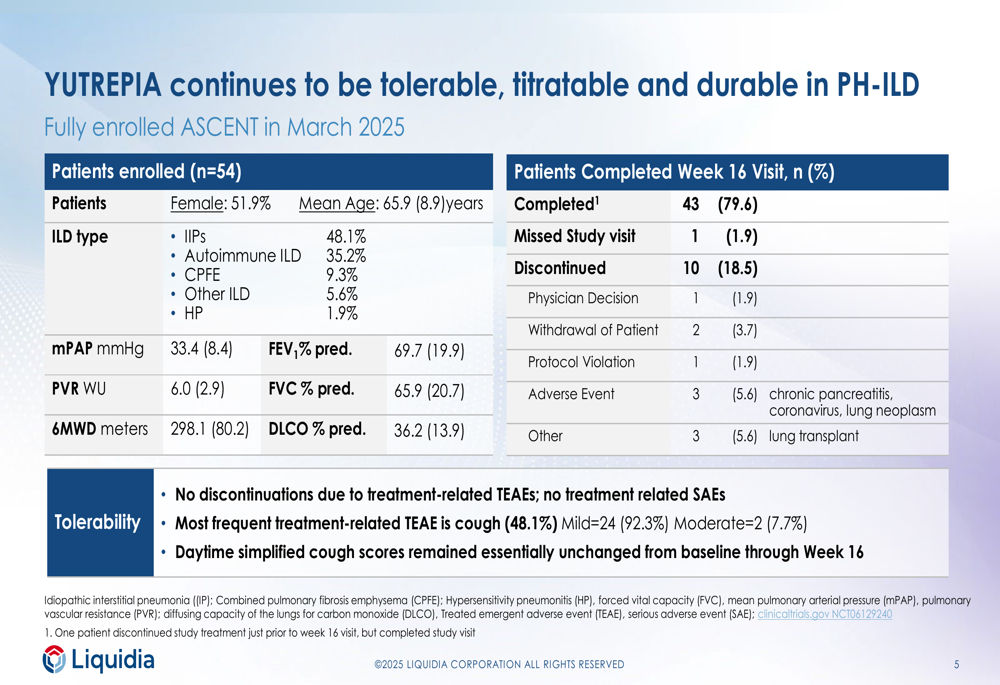

The presentation included detailed clinical data from the ASCENT study of Yutrepia in patients with pulmonary hypertension associated with interstitial lung disease (PH-ILD), which completed enrollment in March 2025.

The following slide provides key insights into the tolerability and durability of Yutrepia treatment:

Notable findings include a high completion rate of 79.6% through Week 16, with no discontinuations due to treatment-related adverse events. While cough was reported in 48.1% of patients, it was predominantly mild (92.3%) and did not lead to treatment discontinuation.

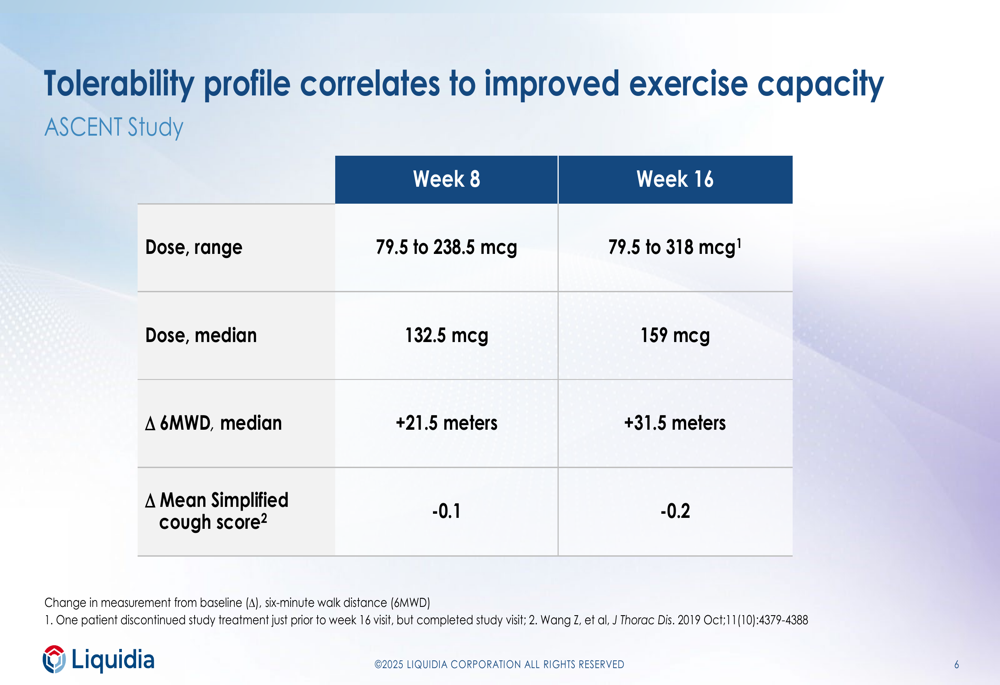

Further data demonstrated meaningful improvements in exercise capacity, with a median increase of 31.5 meters in the six-minute walk distance (6MWD) at Week 16:

This improvement occurred alongside stable cough scores, suggesting that patients were able to tolerate increasing doses (median dose increased from 132.5 mcg at Week 8 to 159 mcg at Week 16) while experiencing functional benefits.

Detailed Financial Analysis

The financial results reveal the significant impact of commercialization efforts on Liquidia’s expense structure. While research and development costs decreased by 36% year-over-year to $6.02 million (down from $9.42 million in Q2 2024), selling, general, and administrative expenses nearly doubled to $38.82 million (up from $19.94 million).

This shift in expense allocation reflects the company’s transition from development to commercialization. The increased operating loss of $37.51 million (compared to $27.20 million in Q2 2024) indicates the substantial investments being made to support the Yutrepia launch.

Notably, these results show improvement from Q1 2025, when the company reported a net loss of $38.4 million according to previous earnings reports. The strong cash position of $173 million provides Liquidia with runway to continue supporting the commercial rollout.

Strategic Positioning

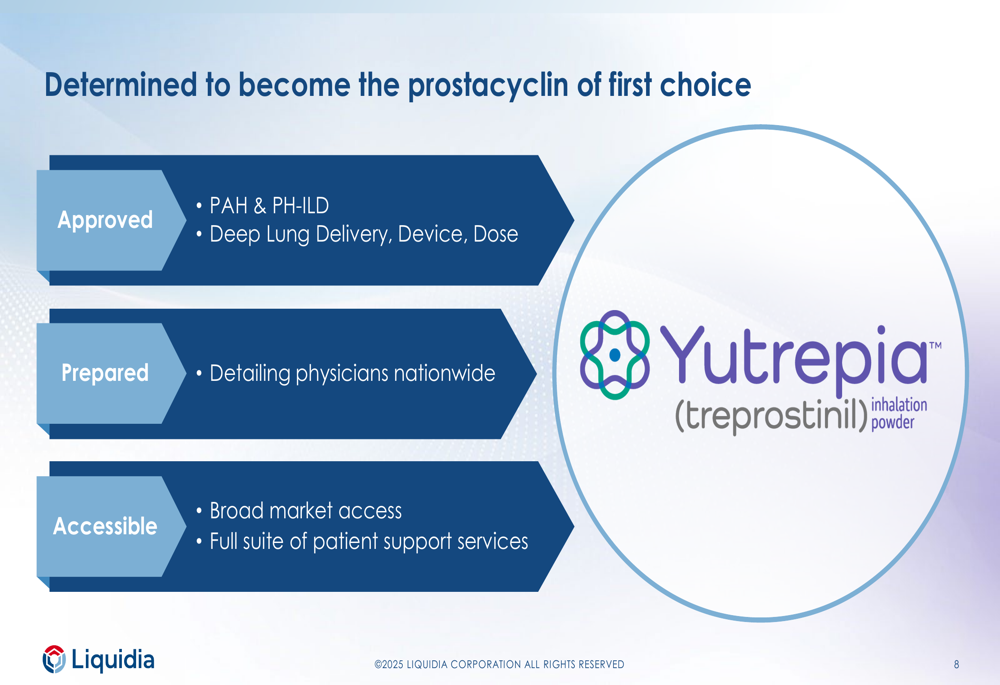

Liquidia’s strategic approach positions Yutrepia as the "prostacyclin of first choice" for pulmonary hypertension, based on three key pillars:

The company’s strategy emphasizes Yutrepia’s approved status for both PAH and PH-ILD indications, its deep lung delivery system, and flexible dosing options. The commercial preparation includes nationwide physician detailing, while accessibility is supported through market access programs and patient support services.

This strategic positioning appears to be gaining traction based on the early adoption metrics, though the competitive landscape in the pulmonary hypertension market remains challenging.

Forward-Looking Statements

Looking ahead, Liquidia indicated that it is well-capitalized to achieve its objectives in 2025, with potential for additional financing. The company noted that an additional $25 million could be available from HCRx when cumulative net sales exceed $100 million, subject to mutual agreement.

Management’s focus remains on expanding Yutrepia’s market penetration while managing the significant commercialization expenses. The substantial increase in SG&A costs suggests that Liquidia anticipates continued investment will be necessary to fully capitalize on Yutrepia’s market opportunity.

While the early adoption metrics are promising, investors should note that the widening operating loss indicates the company remains in investment mode, with profitability likely still some distance away. The strong premarket stock performance suggests investors are focusing on the revenue growth and adoption metrics rather than the near-term profitability outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.