Gold prices steady ahead of Fed decision, Trump’s tariff deadline

Lithia Motors Inc . (NYSE:LAD) unveiled its latest investor presentation on July 29, 2025, outlining ambitious growth targets and strategic initiatives designed to cement its position as a leading automotive retailer. The presentation comes after the company reported better-than-expected Q1 2025 results, with the stock trading at $307.07 as of July 28, showing a 1.67% increase in premarket trading on presentation day.

Executive Summary

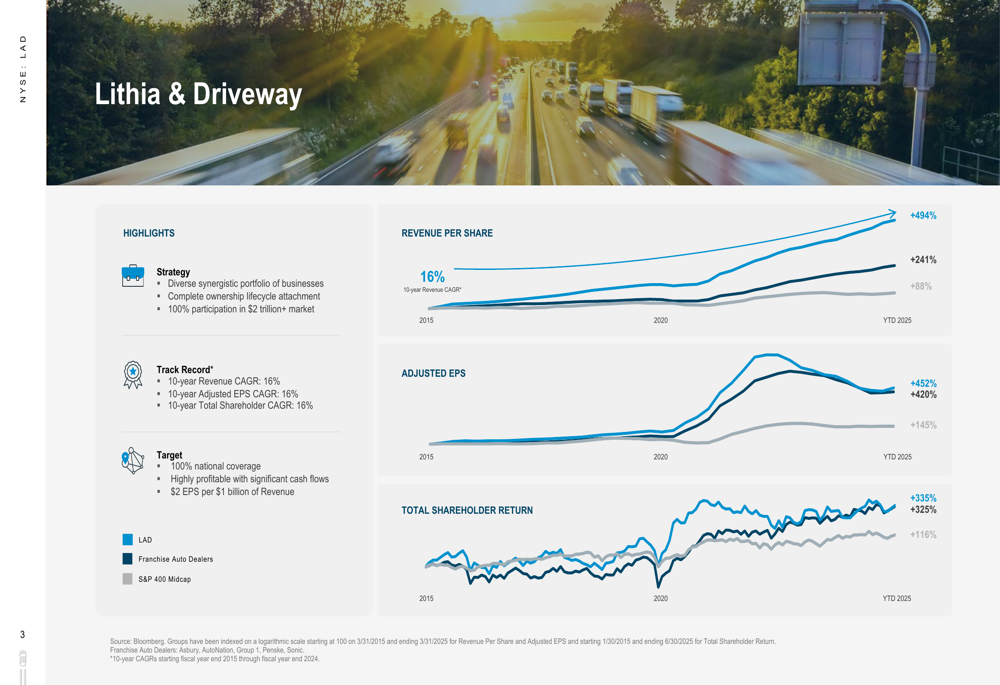

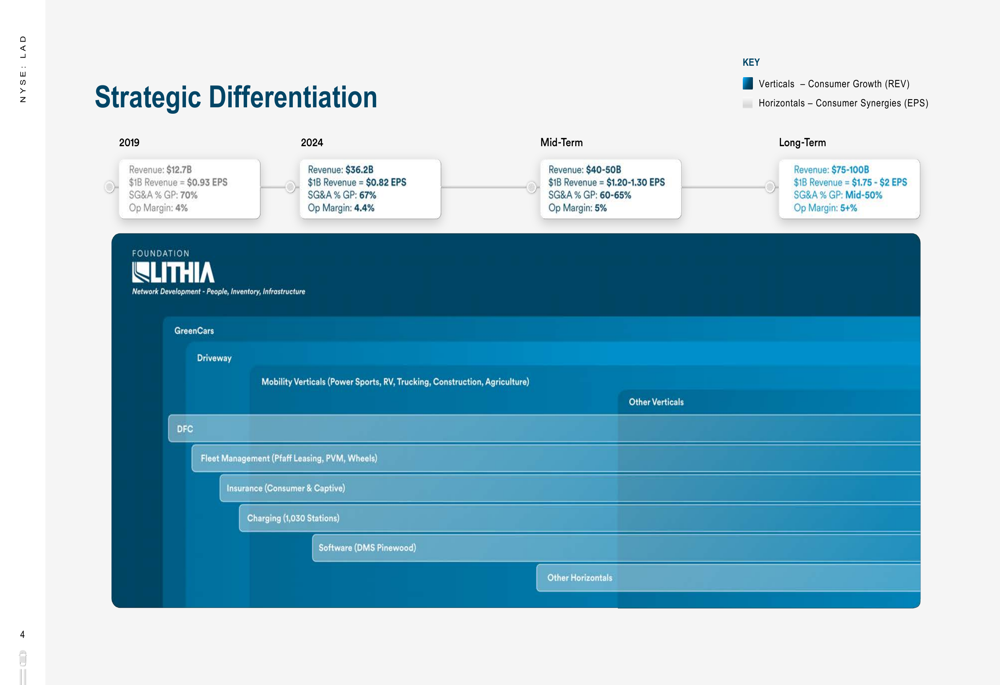

Lithia Motors has demonstrated consistent growth over the past decade, with 10-year CAGRs of 16% across revenue, adjusted EPS, and total shareholder return. The company has expanded its revenue from $12.7 billion in 2019 to $36.2 billion in 2024, with mid-term targets of $40-50 billion and long-term goals of $75-100 billion.

As shown in the following chart highlighting the company’s performance metrics and targets:

A key focus of the presentation is Lithia’s path to achieving $2 in earnings per share for every $1 billion in revenue in the long term, up from $0.82 in 2024. This improvement is expected to come through operational efficiencies, with SG&A as a percentage of gross profit decreasing from 67% in 2024 to the mid-50% range long-term, and operating margins improving from 4.4% to over 5%.

The company’s financial forecast across various time horizons is illustrated in this strategic differentiation slide:

Strategic Initiatives

Lithia is pursuing a multi-faceted growth strategy centered around its expanding dealership network, digital platforms, and financial services. The company currently operates 448 stores globally representing 52 OEM brands, with 135,000+ retail vehicles in inventory. Its goal is to achieve 95% coverage of the U.S. population, requiring customers to travel no more than 205 miles to reach a Lithia location.

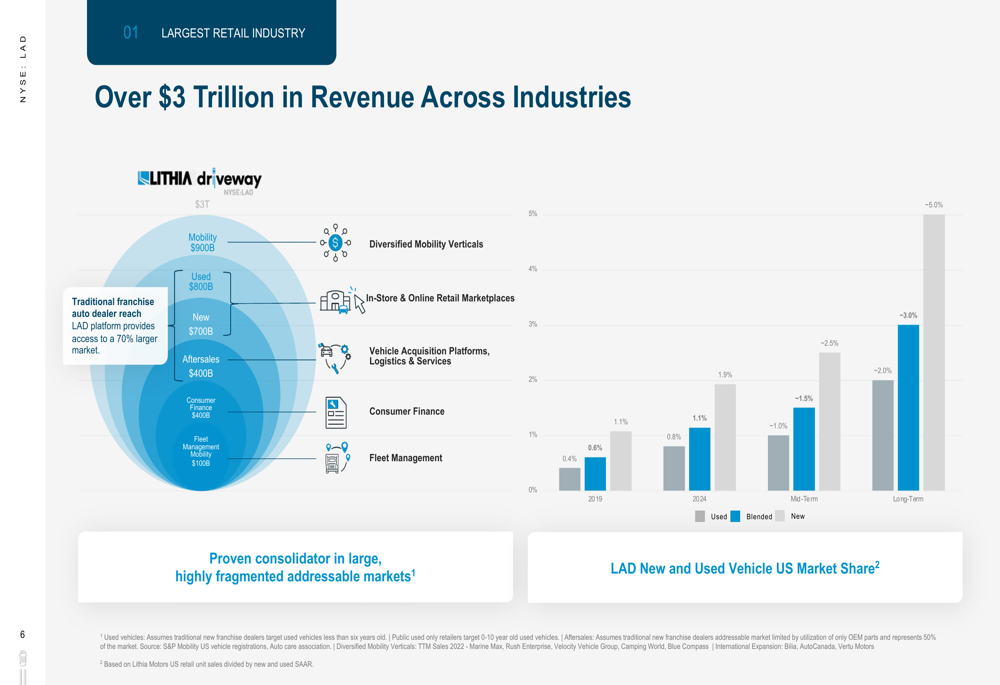

The company’s total addressable market spans multiple segments totaling over $3 trillion, including mobility ($900B), used vehicles ($800B), new vehicles ($700B), aftersales ($400B), consumer finance ($400B), and fleet management ($100B). Lithia’s current blended market share stands at approximately 3%, with plans to reach 5% in the long term.

As illustrated in this visualization of the company’s addressable market and market share:

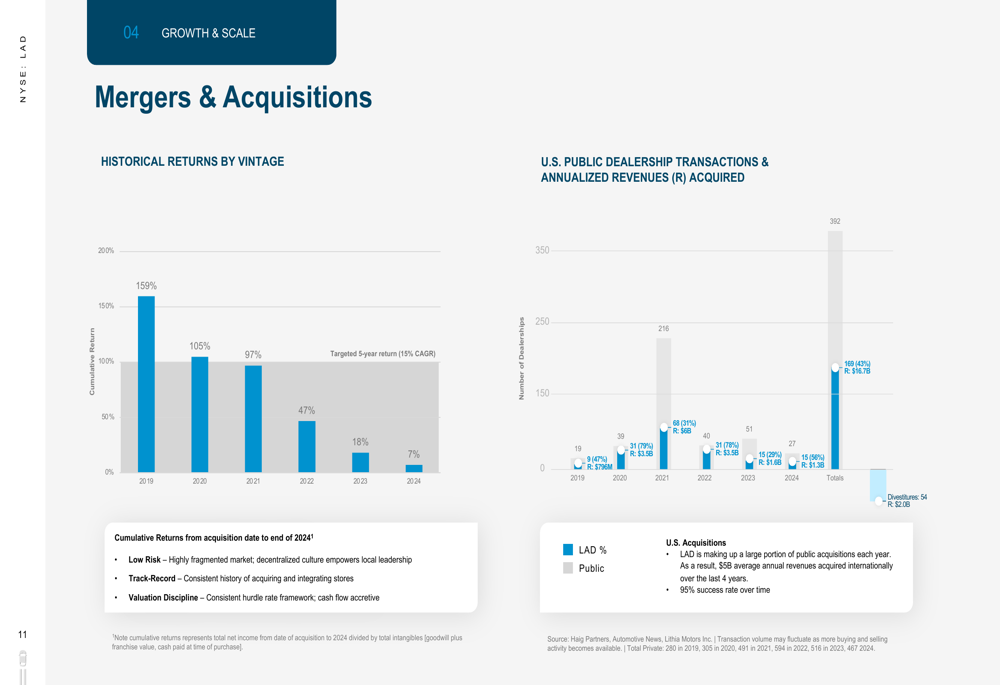

Mergers and acquisitions remain a cornerstone of Lithia’s growth strategy, with the company accounting for 43% of all U.S. public dealership acquisitions. Historical returns on these acquisitions have been strong, with cumulative returns of 159% for 2019 acquisitions, 105% for 2020, and 97% for 2021, all exceeding the company’s targeted 5-year CAGR of 15%.

The following chart details the company’s acquisition performance by vintage:

Detailed Financial Analysis

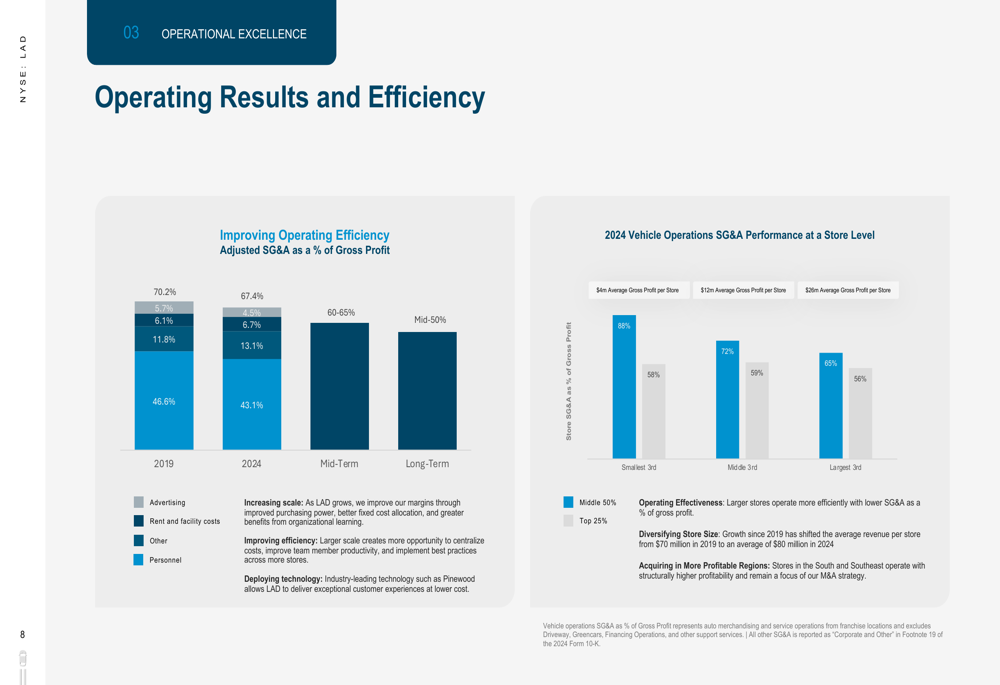

Operational efficiency is a key driver of Lithia’s profitability goals. The company has reduced its adjusted SG&A as a percentage of gross profit from 70.2% in 2019 to 67.4% in 2024, with targets of 60-65% in the mid-term and mid-50% in the long term. Larger stores tend to operate more efficiently, with the top 25% of the largest third of stores achieving an SG&A percentage of 56%.

This operational efficiency trend is clearly demonstrated in the following chart:

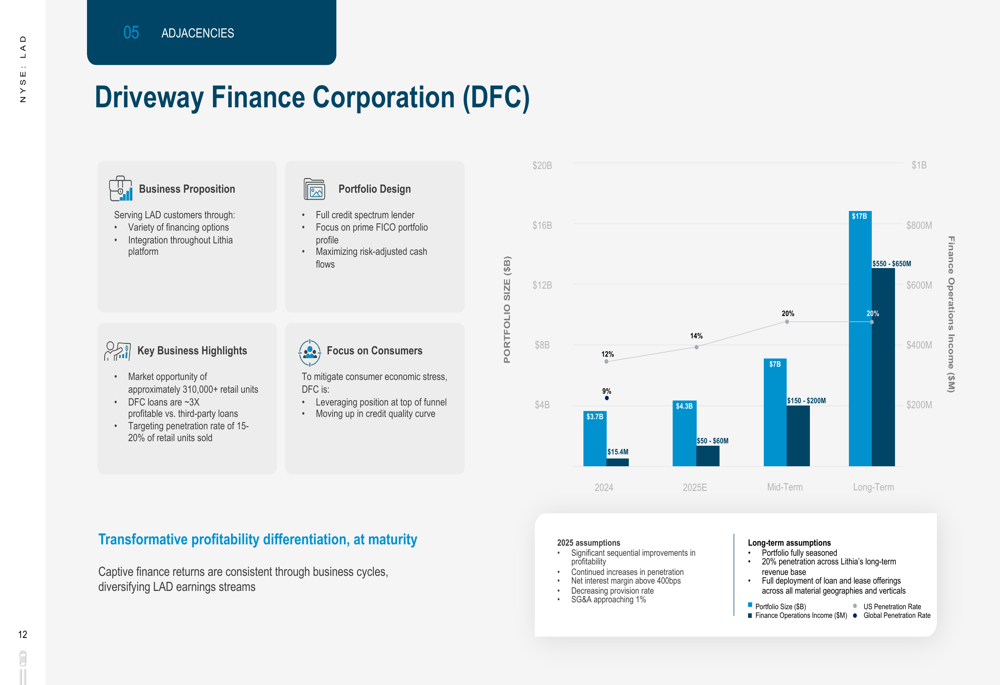

Driveway Finance Corporation (DFC), the company’s captive finance arm, represents a significant growth opportunity. The DFC portfolio has grown to $3.7 billion in 2024, generating $15.4 million in finance operations income. Lithia projects this to expand to a $4.3 billion portfolio with $50-60 million in income for 2025, and ultimately to a $17 billion portfolio generating $800 million in income long-term.

The DFC growth trajectory is illustrated in this chart:

Lithia’s business model demonstrates resilience through its diversified revenue streams. In Q2 2025, the company’s revenue mix included new vehicles, used vehicles, and aftersales, with a balanced new vehicle brand mix of 42% import, 32% luxury, and 26% domestic brands. This diversification helps insulate the company from market fluctuations in any single segment.

The used vehicle market represents a particularly attractive opportunity, with Lithia targeting the full spectrum from certified pre-owned (CPO) to value autos. In Q2 2025, CORE vehicles (average selling price $29,093) represented 60% of the mix, while value autos (average selling price $14,864) delivered the highest ROI at 138%.

The company’s digital ecosystem continues to gain traction, with Driveway.com generating 1.3 million unique visitors per month in Q2 2025. Customers purchased 90,000 vehicles through Lithia’s digital platforms in the first six months of 2025, with approximately half of these sales financed through DFC.

Forward-Looking Statements

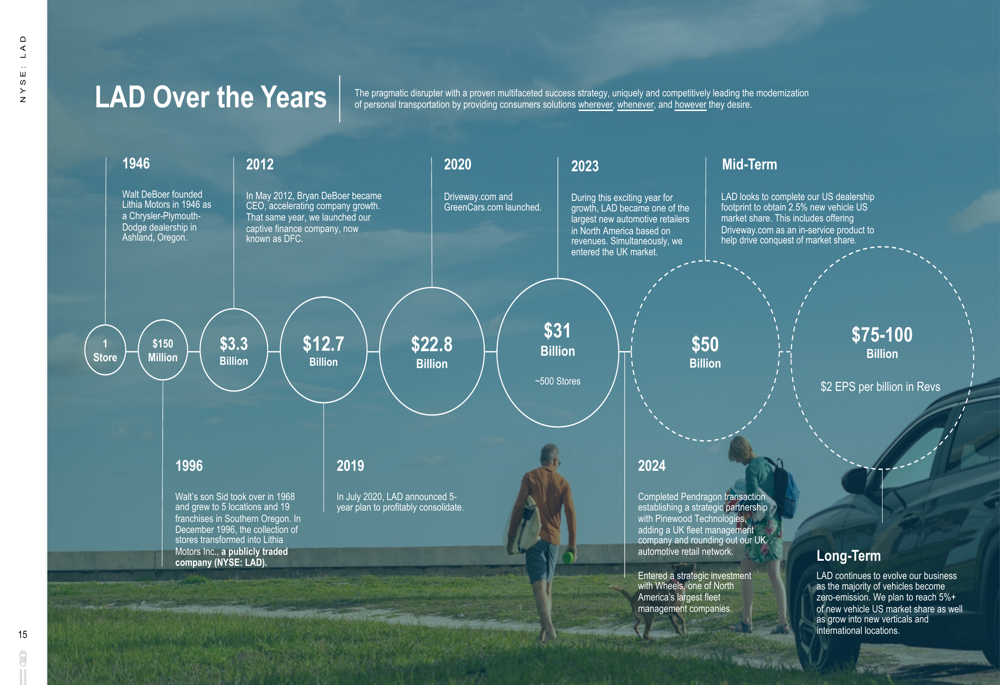

Looking ahead, Lithia has outlined a clear progression from its current position to its long-term goals. The company’s timeline highlights key milestones from its founding in 1946 to its projected future state, including becoming one of North America’s largest automotive retailers in 2023 and entering the UK market that same year.

This comprehensive timeline illustrates the company’s evolution and future aspirations:

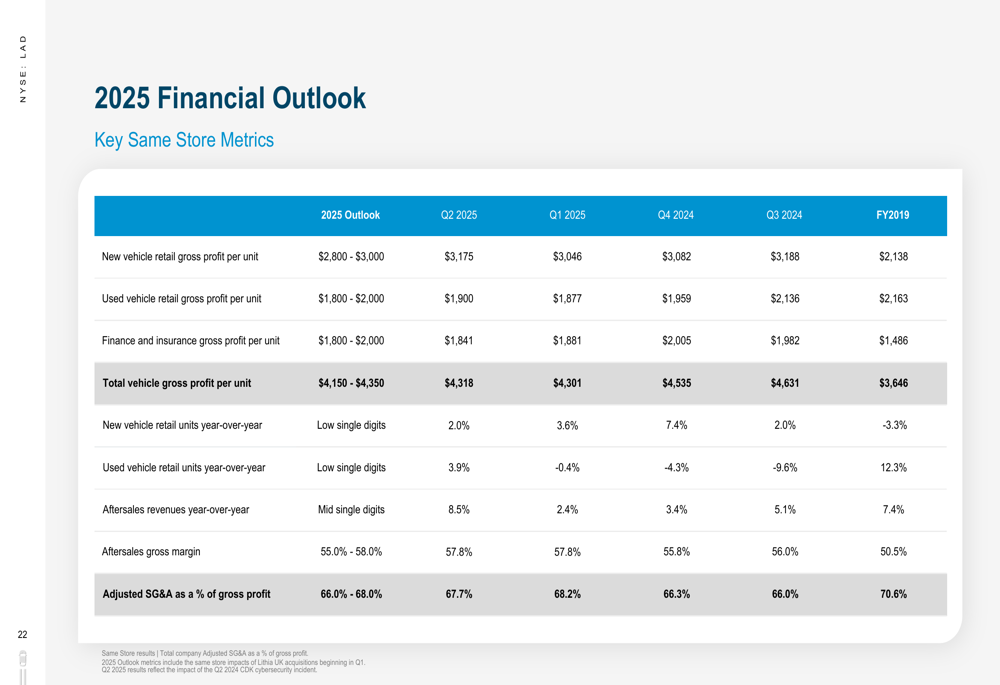

For 2025, Lithia has provided detailed financial guidance across key metrics. The company’s Q2 2025 same-store performance shows mixed results compared to previous periods, with some metrics improving while others face pressure. This aligns with the company’s Q1 2025 earnings report, which noted a slight decline in gross profit per unit despite overall revenue and earnings growth.

The detailed 2025 financial outlook is presented in this comprehensive table:

While Lithia’s presentation paints an optimistic picture of continued growth and margin expansion, investors should note that the stock experienced a 2.28% decline following the Q1 2025 earnings release despite beating expectations. This suggests some market skepticism about the company’s ability to navigate challenges such as tariff impacts, margin pressures, and competition in the digital retail space.

Nevertheless, Lithia’s consistent track record of growth, strategic acquisitions, and operational improvements positions the company well to pursue its ambitious long-term targets of $75-100 billion in revenue, operating margins above 5%, and $2 in EPS for every $1 billion in revenue.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.