These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

LivePerson , Inc. (NASDAQ:LPSN) released its first quarter 2025 earnings presentation on May 7, showing the company exceeded its revenue and adjusted EBITDA guidance despite ongoing revenue contraction. The conversational AI company’s stock, which has struggled near 52-week lows, responded positively with a 5.72% gain in after-hours trading following the announcement.

The company, which reported $64.7 million in revenue for Q1 2025, continues to navigate a challenging business environment while emphasizing growth in its generative AI capabilities and focusing on regulated industries. This follows a difficult Q4 2024 where LivePerson significantly missed EPS expectations despite exceeding revenue forecasts.

Quarterly Performance Highlights

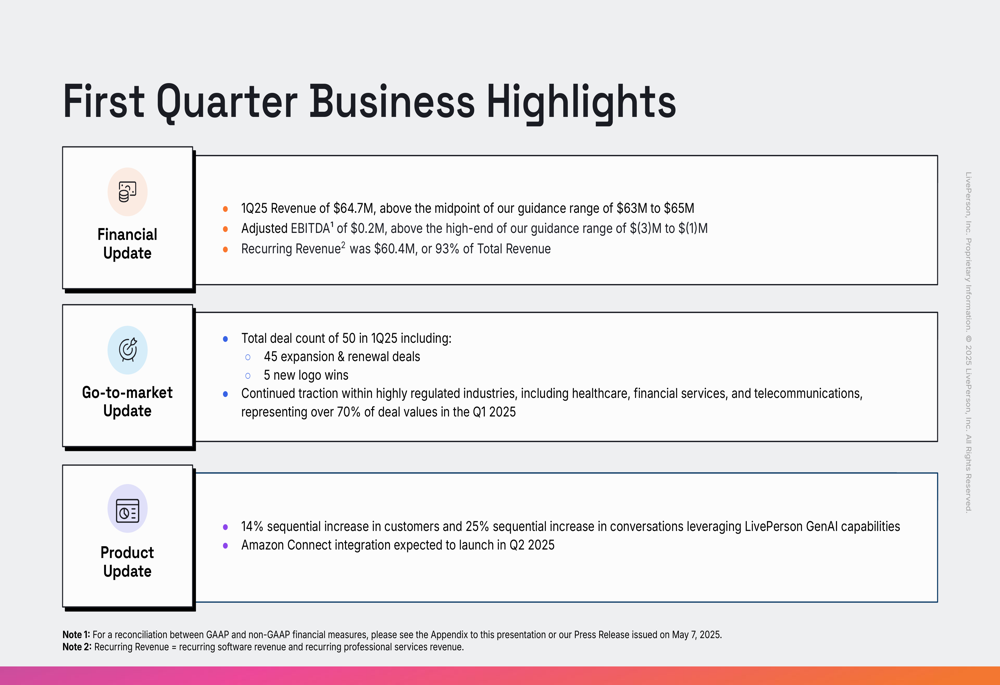

LivePerson’s Q1 2025 revenue of $64.7 million came in above the midpoint of its guidance range of $63-65 million, though this represents a 24% year-over-year decline from $85.1 million in Q1 2024. The company achieved positive adjusted EBITDA of $0.2 million, exceeding the high end of its guidance range of $(3)M-$(1)M.

As shown in the following business highlights slide, the company secured 50 deals during the quarter, including 45 expansion/renewal deals and 5 new logo wins:

Recurring revenue accounted for 93% of total revenue at $60.4 million, maintaining the high percentage seen in recent quarters. The company highlighted strong performance within highly regulated industries, with healthcare, financial services, and telecommunications representing over 70% of deal values.

Strategic Initiatives

LivePerson’s strategic focus on AI capabilities showed progress, with a 14% sequential increase in customers and a 25% sequential increase in conversations leveraging its GenAI capabilities. The company also announced an upcoming Amazon (NASDAQ:AMZN) Connect integration expected in Q2 2025, expanding its platform compatibility.

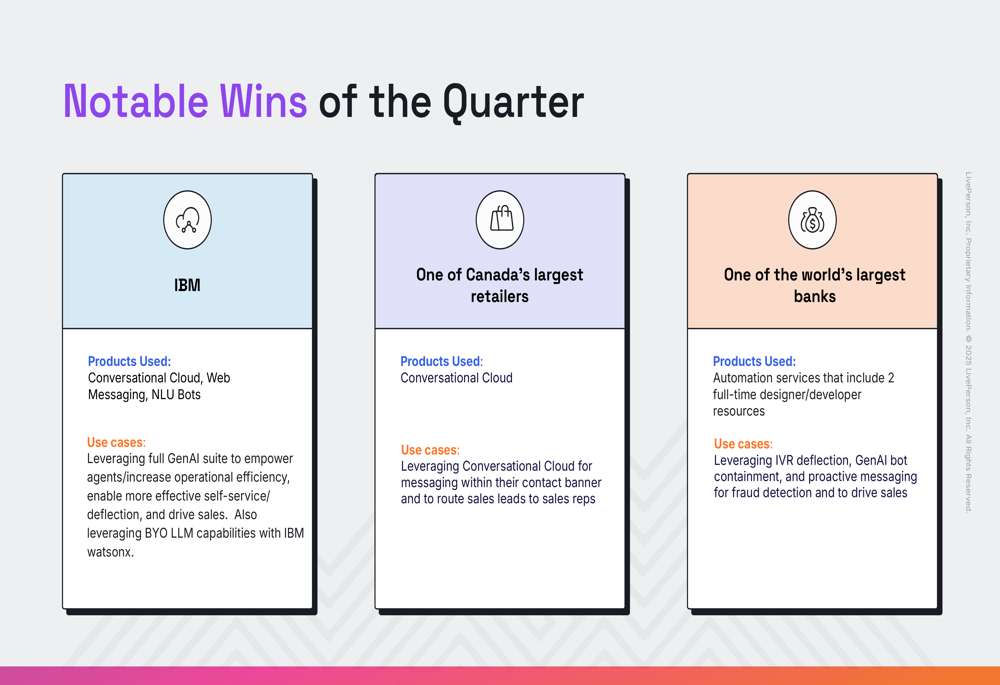

The company highlighted several notable customer wins that demonstrate its value proposition across different industries:

IBM (NYSE:IBM)’s implementation showcases LivePerson’s full GenAI suite along with "bring your own LLM" capabilities integrated with IBM’s watsonx. Meanwhile, one of the world’s largest banks is leveraging LivePerson’s automation services for fraud detection and sales generation, illustrating the company’s penetration in the financial services sector.

Detailed Financial Analysis

LivePerson’s revenue composition shows a continuing shift toward international markets, with the U.S. share of revenue decreasing from 71% in Q1 2024 to 62% in Q1 2025. This geographic diversification is illustrated in the following chart:

The recurring revenue percentage has remained relatively stable between 91-94% over the past five quarters, demonstrating the company’s subscription-based business model resilience despite overall revenue contraction.

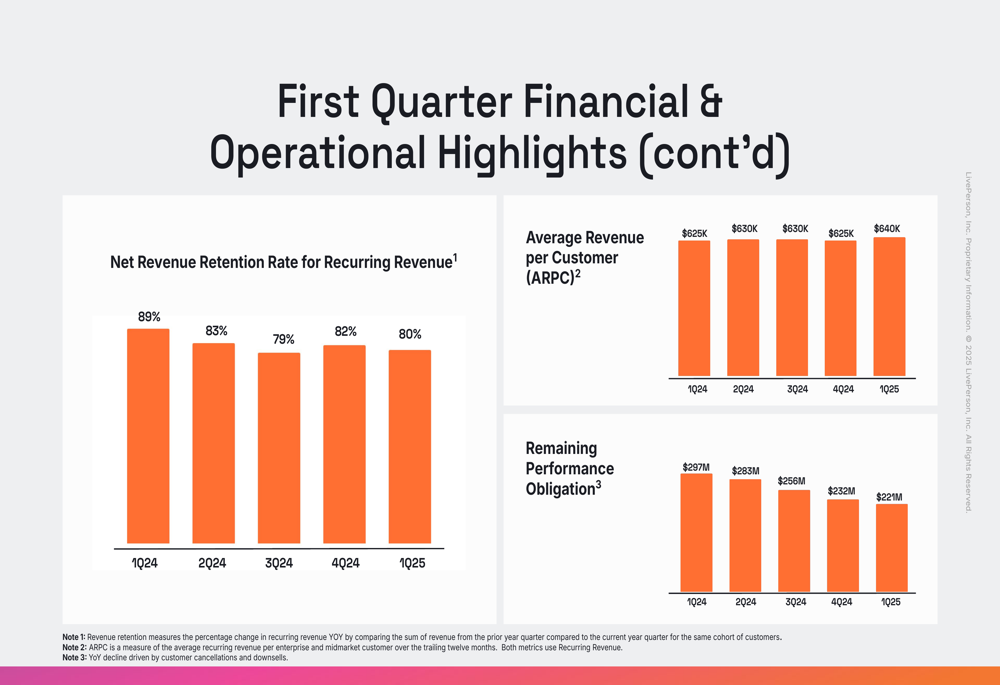

Customer metrics reveal both challenges and stability. The net revenue retention rate for recurring revenue stood at 80% in Q1 2025, down from 89% in Q1 2024, indicating continued customer spending contraction:

Average revenue per customer (ARPC) remained stable at $625,000, matching the Q1 2024 figure after a slight increase to $640,000 in Q4 2024. However, the remaining performance obligation declined to $221 million, down 26% from $297 million a year earlier, suggesting continued pressure on future contracted revenue.

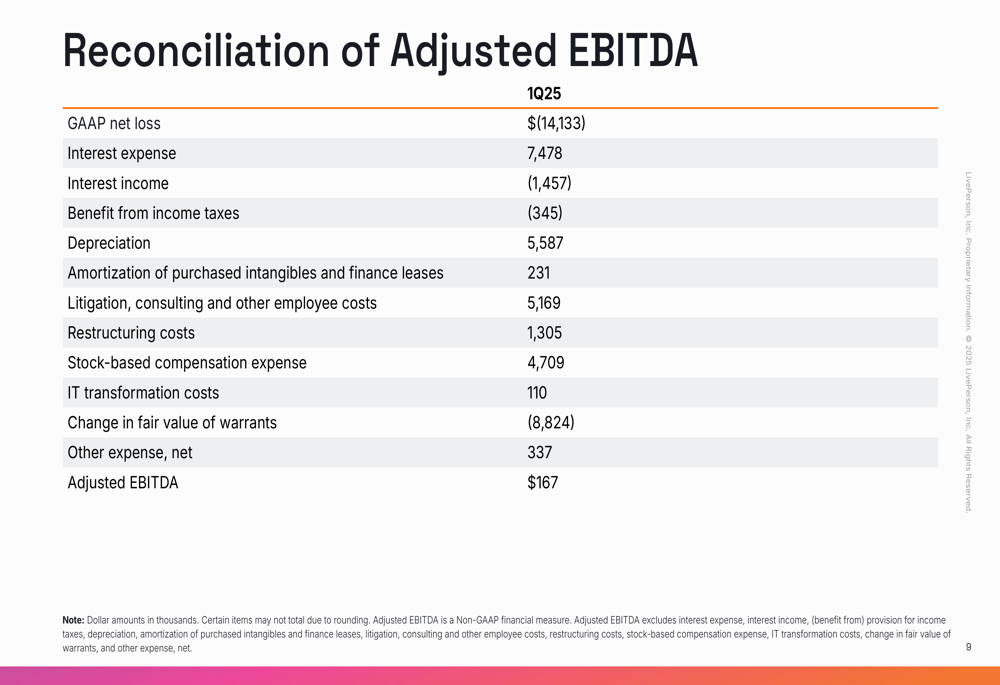

The company’s adjusted EBITDA reconciliation reveals the significant adjustments made to reach positive territory from a GAAP net loss:

Notable adjustments include $7.5 million in interest expense, $5.6 million in depreciation, $5.2 million in litigation and consulting costs, and $4.7 million in stock-based compensation. The company also benefited from an $8.8 million positive adjustment related to the change in fair value of warrants.

Forward-Looking Statements

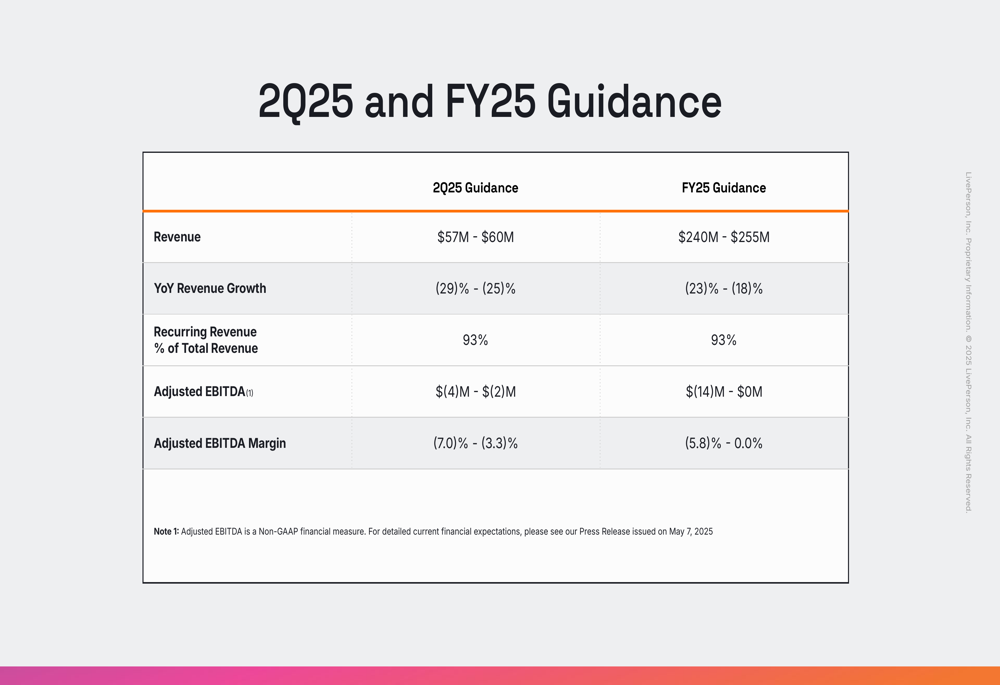

LivePerson’s guidance for Q2 2025 and the full year 2025 confirms continued revenue contraction, though at an improving rate as the year progresses:

For Q2 2025, the company expects revenue between $57-60 million, representing a year-over-year decline of 25-29%. Full-year 2025 guidance projects revenue of $240-255 million, a decline of 18-23% compared to 2024.

On the profitability front, LivePerson expects adjusted EBITDA of $(4)M-$(2)M for Q2 and $(14)M-$0M for the full year 2025, suggesting potential breakeven by year-end.

CEO John Sabino emphasized the company’s vision, stating, "Our vision for 2025 and beyond is to create a future where brands can engage and inspire their customers with every interaction." Meanwhile, CFO/COO John Collins expressed optimism about continued business improvement throughout 2025.

While the company faces ongoing revenue challenges, its focus on AI capabilities, regulated industries, and operational efficiency appears to be yielding some stability in a difficult transition period. Investors will be watching closely to see if LivePerson can stabilize its revenue decline and return to growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.