Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

LiveRamp Holdings Inc (NYSE:RAMP) released its first quarter fiscal year 2026 earnings presentation on August 6, 2025, revealing accelerated revenue growth and significant margin expansion despite some slowing in annual recurring revenue (ARR) metrics. The data connectivity platform provider’s stock has been trading near $32.05, up 1.65% in the most recent session, continuing its recovery from a 52-week low of $21.45.

The company’s results come amid ongoing industry evolution in data privacy regulations and the continued shift away from third-party cookies, positioning LiveRamp’s authenticated identity and data collaboration solutions as increasingly strategic for marketers.

Quarterly Performance Highlights

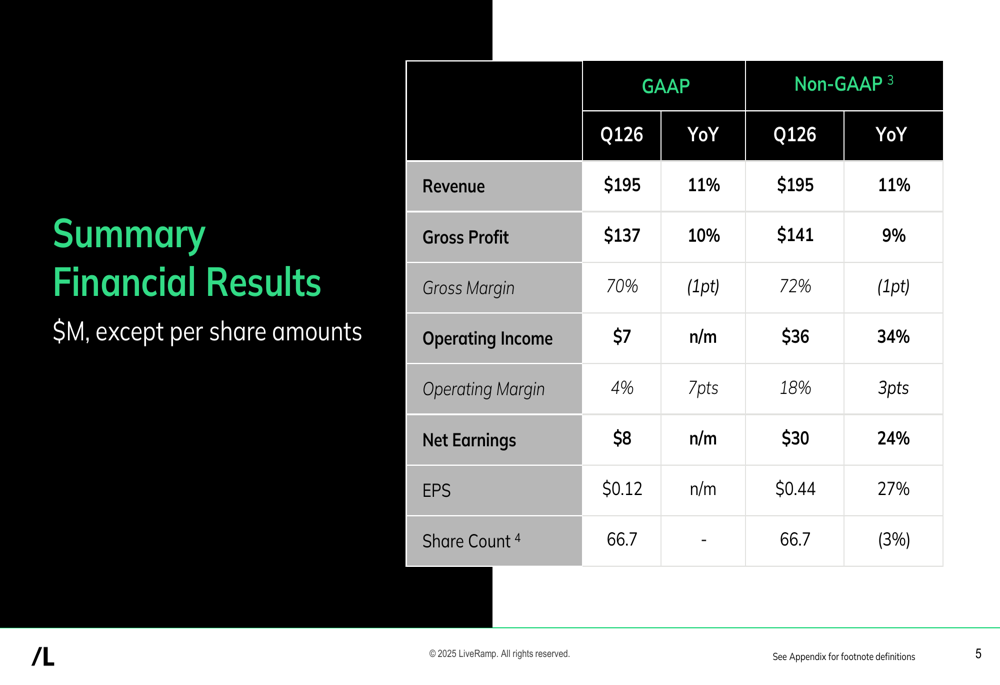

LiveRamp reported total revenue of $195 million for Q1 FY26, representing an 11% year-over-year increase, slightly accelerating from the 10% growth seen in the previous quarter. The company’s subscription business, which accounts for 76% of total revenue, grew by 10% to $148 million.

As shown in the following summary financial results:

Non-GAAP operating income jumped 34% year-over-year to $36 million, with operating margin expanding 3 percentage points to reach 18%. This improvement demonstrates LiveRamp’s focus on operational efficiency while maintaining growth. Non-GAAP earnings per share increased 27% to $0.44, benefiting from both operational improvements and a 3% reduction in share count.

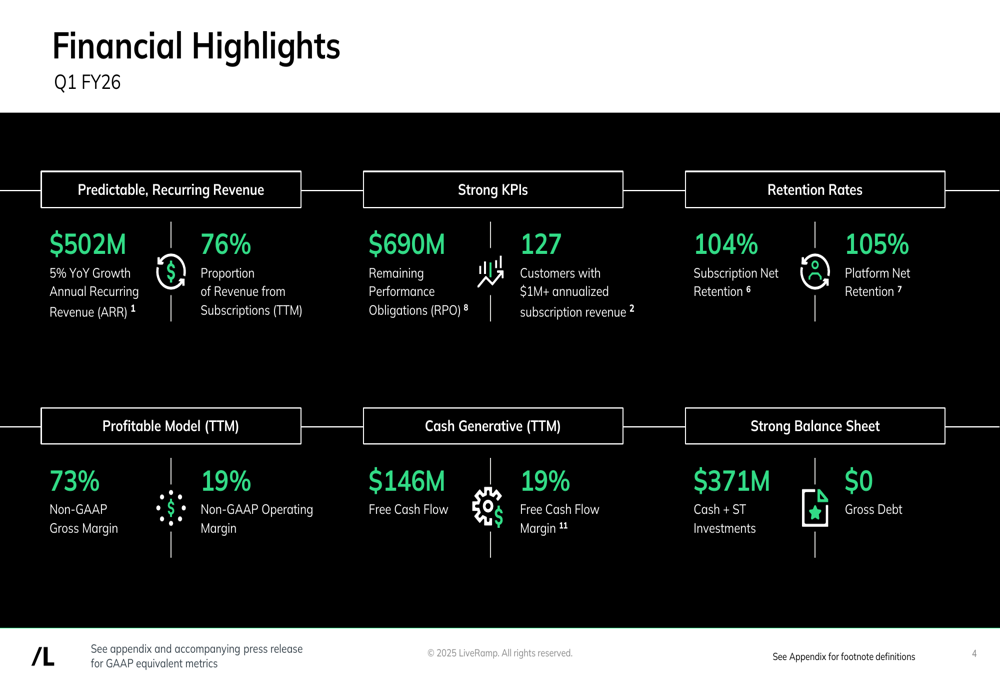

The company’s financial health remains strong, as highlighted in this overview of key metrics:

Detailed Financial Analysis

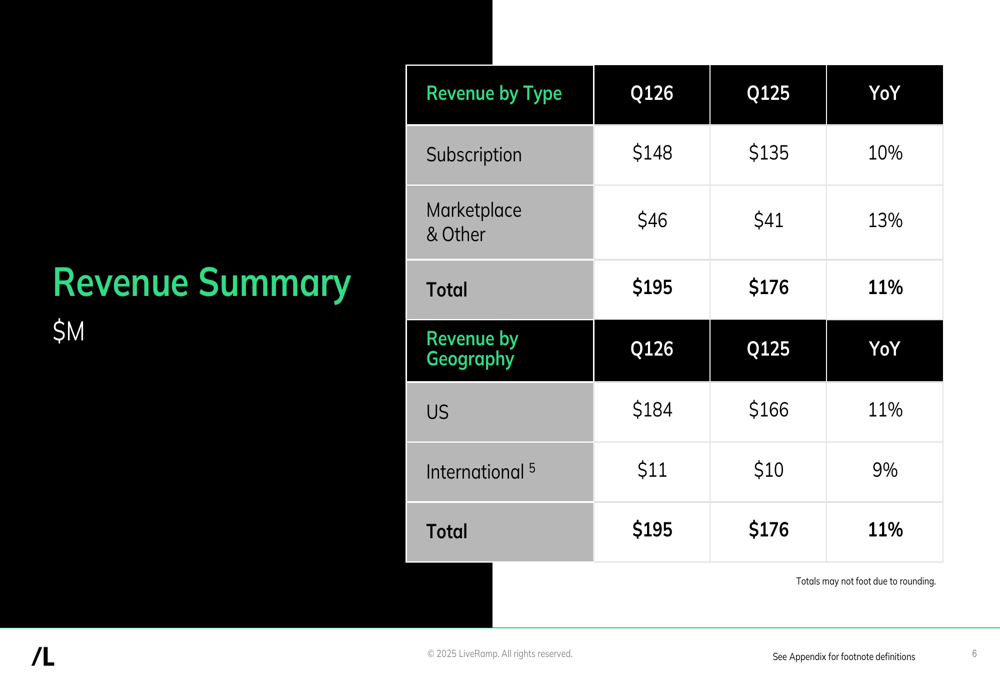

LiveRamp’s revenue composition shows continued strength across both subscription and marketplace segments. Subscription revenue, which provides predictable recurring income, grew 10% year-over-year to $148 million, with fixed subscriptions representing 85% of that total. Marketplace and other revenue increased 13% to $46 million, driven by 9% growth in data marketplace revenue and 25% growth in other revenue streams.

The detailed revenue breakdown by type and geography shows:

While quarterly free cash flow was negative at -$16 million compared to -$9 million in the prior-year period, the trailing twelve-month free cash flow remained robust at $146 million with a 19% margin. This seasonal fluctuation is typical for the company’s first quarter.

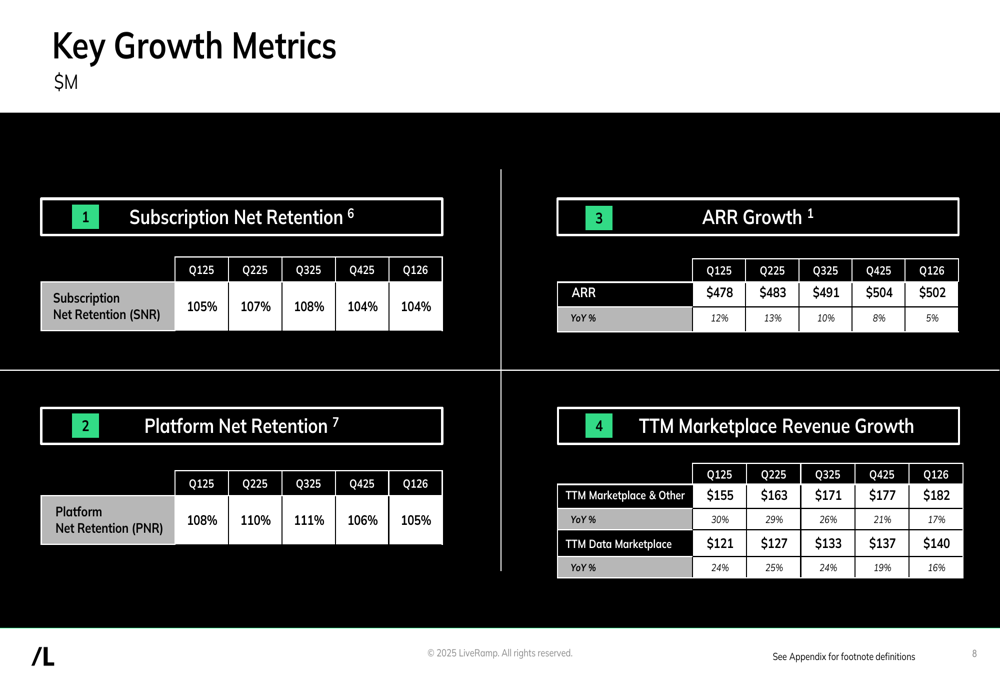

A concerning trend appears in the company’s key growth metrics, particularly in ARR (Annual Recurring Revenue), which grew just 5% year-over-year to $502 million, down from 8% growth in the previous quarter:

Customer retention metrics have also stabilized at lower levels, with subscription net retention at 104% and platform net retention at 105%, down from their peaks of 108% and 111% in Q3 FY25, respectively.

Strategic Initiatives & Competitive Position

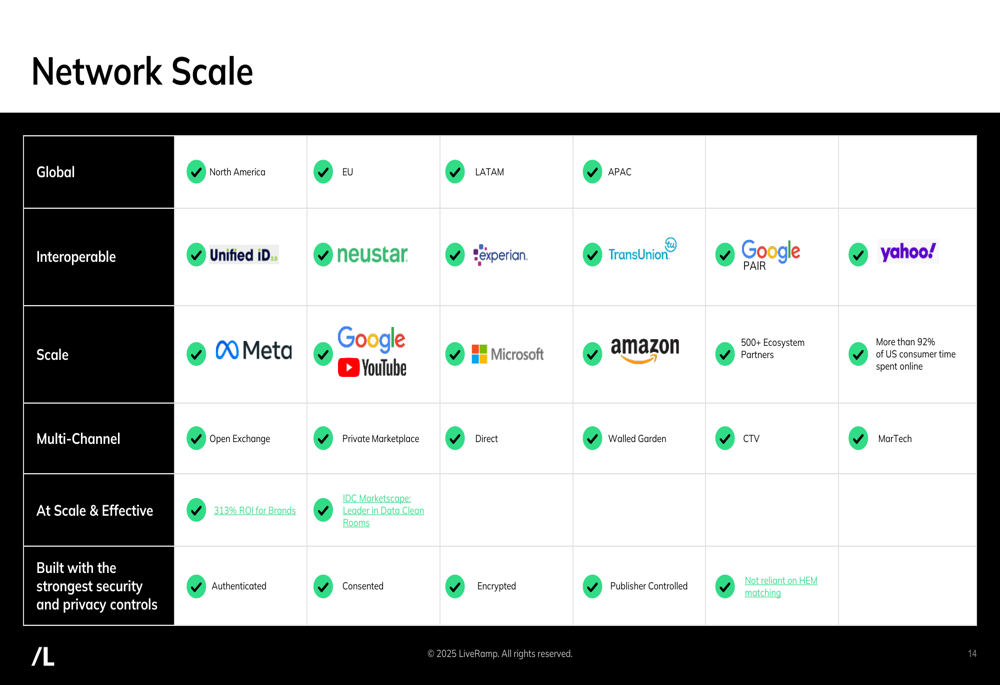

LiveRamp continues to strengthen its competitive position through its extensive network and partner ecosystem. The company’s presentation highlighted its global reach, interoperability with major identity solutions, and multi-channel capabilities:

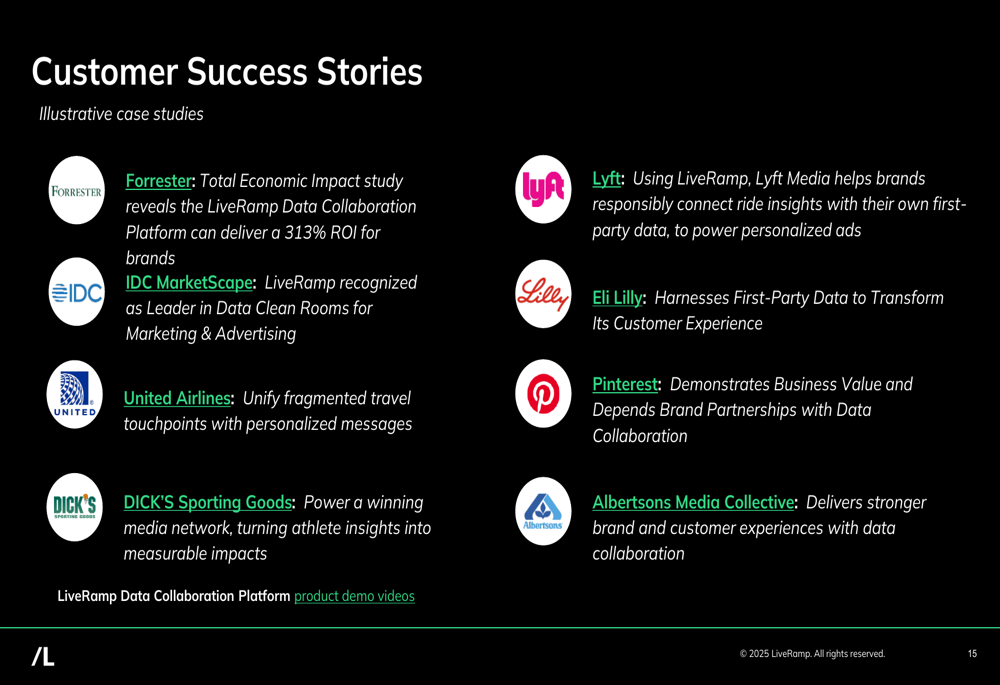

The company emphasized its leadership in the data clean room space, citing recognition from IDC MarketScape. Customer success stories featured prominent brands like United Airlines, DICK’S Sporting Goods, and Albertsons (NYSE:ACI) Media Collective, with a Forrester study claiming LiveRamp’s Data Collaboration Platform can deliver a 313% ROI for brands.

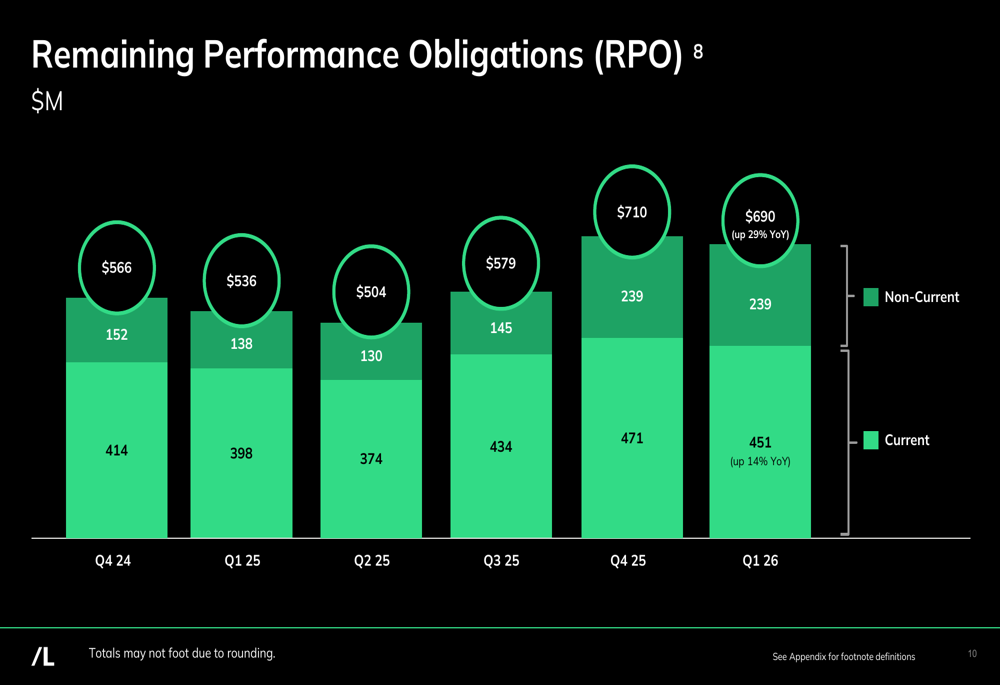

Remaining Performance Obligations (RPO), an important indicator of future revenue, reached $690 million, up 29% year-over-year, suggesting strong forward momentum despite the slowing ARR growth:

Forward-Looking Statements & Guidance

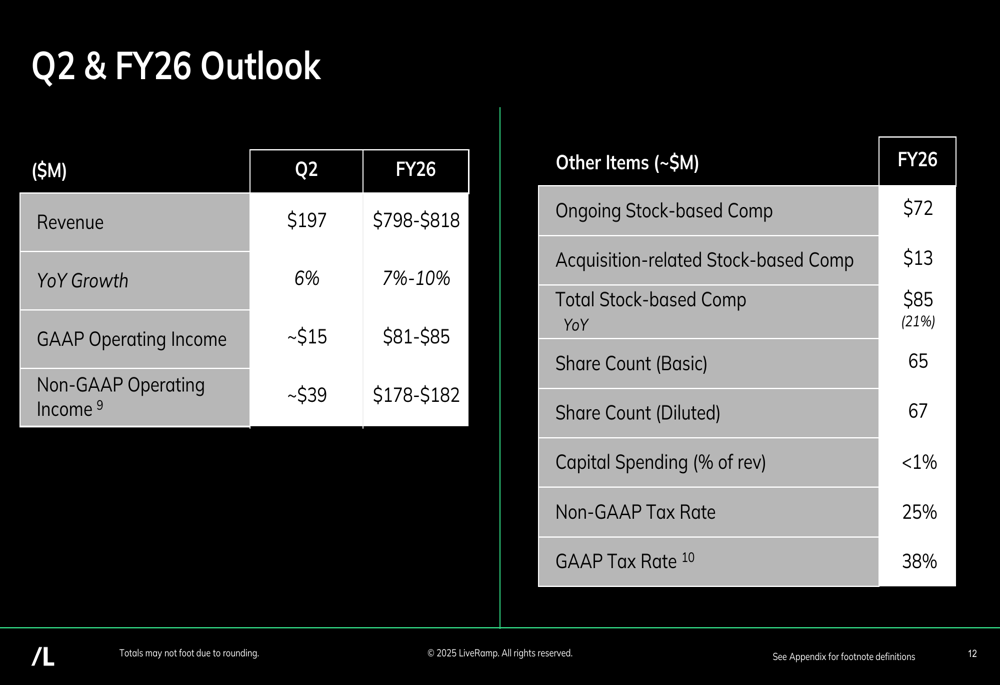

For the second quarter of FY26, LiveRamp expects revenue of approximately $197 million, representing 6% year-over-year growth, with non-GAAP operating income of around $39 million. For the full fiscal year 2026, the company projects revenue between $798 million and $818 million, implying 7-10% growth:

The company expects to maintain its focus on profitability, with full-year non-GAAP operating income projected between $178 million and $182 million. Capital spending is expected to remain below 1% of revenue, reflecting the asset-light nature of LiveRamp’s business model.

These projections suggest that while LiveRamp anticipates continued growth, the pace may moderate slightly compared to the 11% growth achieved in Q1. However, the emphasis on margin expansion indicates management’s confidence in driving increased profitability even as revenue growth potentially decelerates.

In summary, LiveRamp’s Q1 FY26 results demonstrate the company’s ability to accelerate revenue growth and significantly expand margins despite some moderation in key subscription metrics. With a strong balance sheet, growing RPO, and continued focus on operational efficiency, LiveRamp appears well-positioned to navigate the evolving data privacy landscape while delivering improved financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.