S&P 500 eases slightly from fresh record high after stronger economic growth

Introduction & Market Context

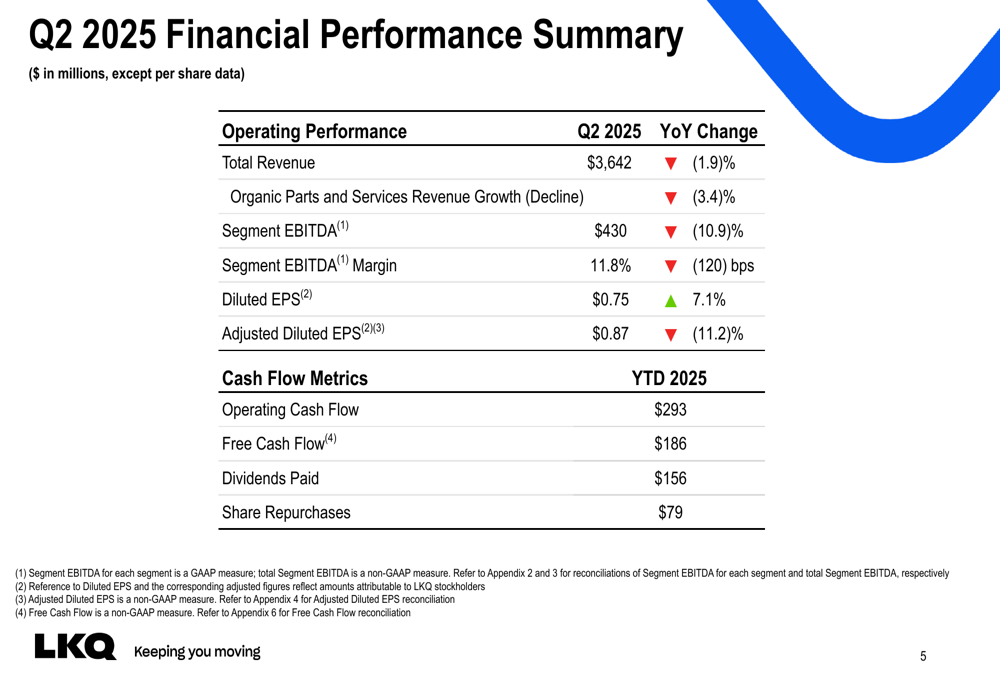

LKQ Corporation (NASDAQ:LKQ) released its second quarter 2025 earnings presentation on July 24, showing declining revenue across all business segments and a reduced full-year outlook. The auto parts distributor reported a 1.9% year-over-year revenue decline to $3.64 billion, while segment EBITDA fell 10.9% to $430 million. The stock dropped 6.81% in premarket trading to $35.98, reflecting investor concerns about the company’s performance and lowered guidance.

The presentation revealed that despite cost-cutting initiatives and continued shareholder returns, LKQ faces significant headwinds in both North American and European markets. This follows a challenging first quarter where the company had already reported declining organic revenues.

Quarterly Performance Highlights

LKQ’s second quarter results showed pressure across most financial metrics. While reported diluted EPS increased 7.1% to $0.75, adjusted diluted EPS declined 11.2% to $0.87, indicating underlying operational challenges.

As shown in the following comprehensive financial summary:

Organic parts and services revenue declined 3.4% year-over-year, with segment EBITDA margin contracting 120 basis points to 11.8%. Year-to-date operating cash flow fell to $293 million from $466 million in the prior year period, while free cash flow decreased to $186 million from $320 million.

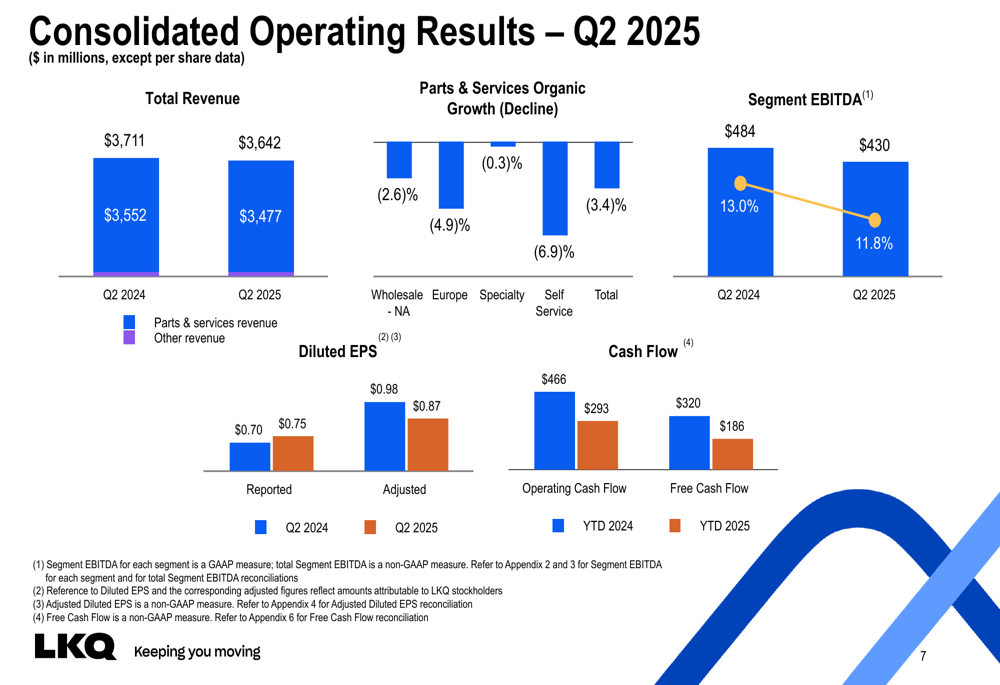

The consolidated operating results provide a clear picture of the company’s performance across key metrics:

All four business segments experienced revenue declines, with particularly challenging conditions in the Wholesale North America and Europe segments. The company’s North American operations were impacted by a significant 9% decline in repairable claims, while Europe faced both temporary operational challenges and persistent market softness.

Segment Performance Analysis

Wholesale North America, LKQ’s largest segment, saw revenue decrease 2.2% to $1.44 billion, with segment EBITDA falling 11.3% to $227 million. Despite the challenging environment, management noted that the segment outperformed the broader market in terms of organic revenue.

The European segment, which represents a significant portion of LKQ’s business, reported a 2.0% revenue decline to $1.61 billion and a 13.2% drop in segment EBITDA to $151 million. The company cited temporary operational challenges and ongoing market conditions as key factors, while also noting that divestitures of operations in Poland, Slovenia, and Bosnia contributed to the revenue decline.

The Specialty segment, focused on recreational vehicle and marine products, showed the smallest revenue decline at 0.2%, though segment EBITDA still fell 4.9% to $39 million. Management noted that demand softness in recreational vehicle product lines was partially offset by growth in marine products.

Self Service was the only segment to maintain EBITDA at $13 million despite a 3.0% revenue decline to $129 million. The company attributed this resilience to disciplined vehicle procurement, effective cost controls, and favorable movements in commodity prices.

Strategic Initiatives

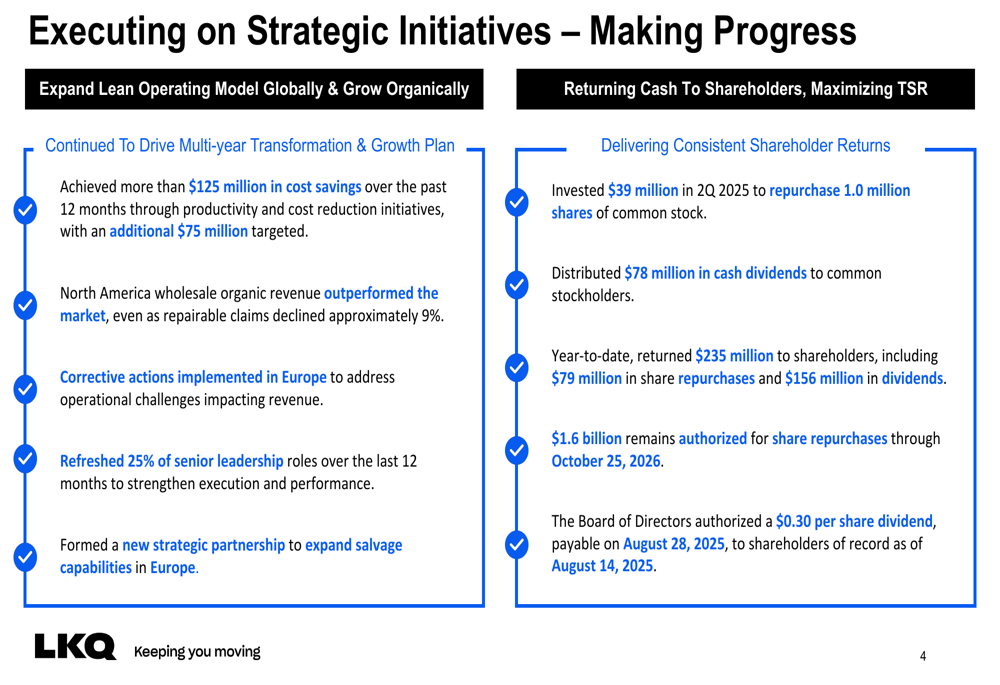

Despite the challenging quarter, LKQ highlighted several strategic initiatives aimed at improving performance. The company has achieved more than $125 million in cost savings over the past 12 months through productivity and cost reduction initiatives, with an additional $75 million targeted.

The following slide details the company’s progress on key strategic initiatives:

LKQ has refreshed 25% of senior leadership roles over the last 12 months to strengthen execution and performance. The company also formed a new strategic partnership to expand salvage capabilities in Europe, addressing one of the operational challenges in that region.

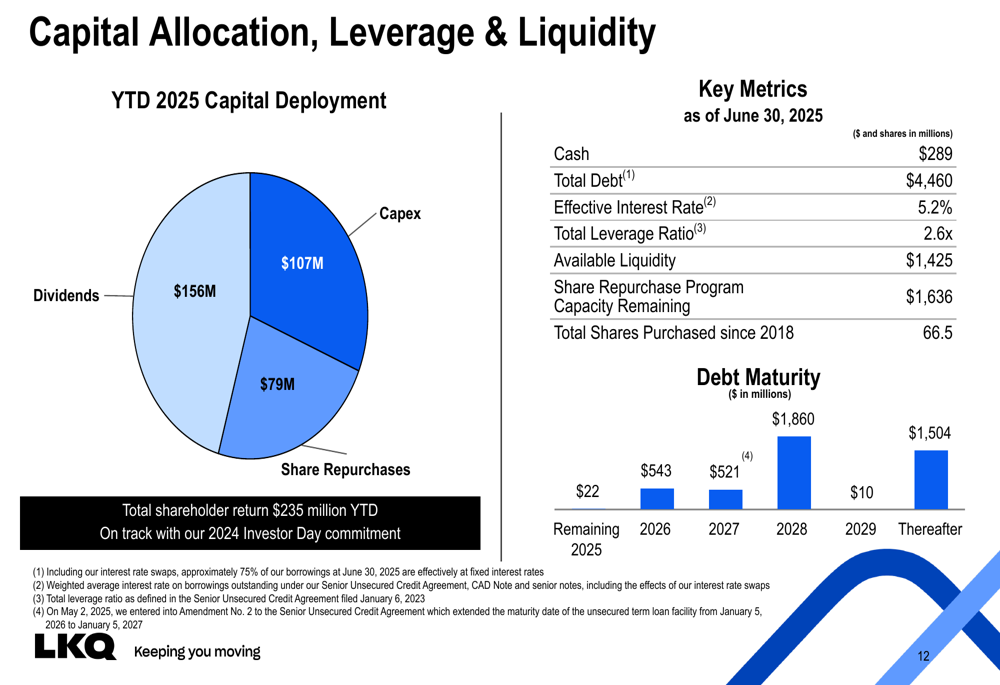

Capital allocation remains focused on shareholder returns, with $235 million returned to shareholders year-to-date, including $79 million in share repurchases and $156 million in dividends. The Board of Directors authorized a $0.30 per share dividend, payable on August 28, 2025.

The company’s capital allocation strategy and financial position are illustrated in the following chart:

LKQ maintains a solid balance sheet with $289 million in cash, total debt of $4.46 billion, and a total leverage ratio of 2.6x. Available liquidity stands at $1.43 billion, providing flexibility to navigate the current challenging environment.

Industry Context

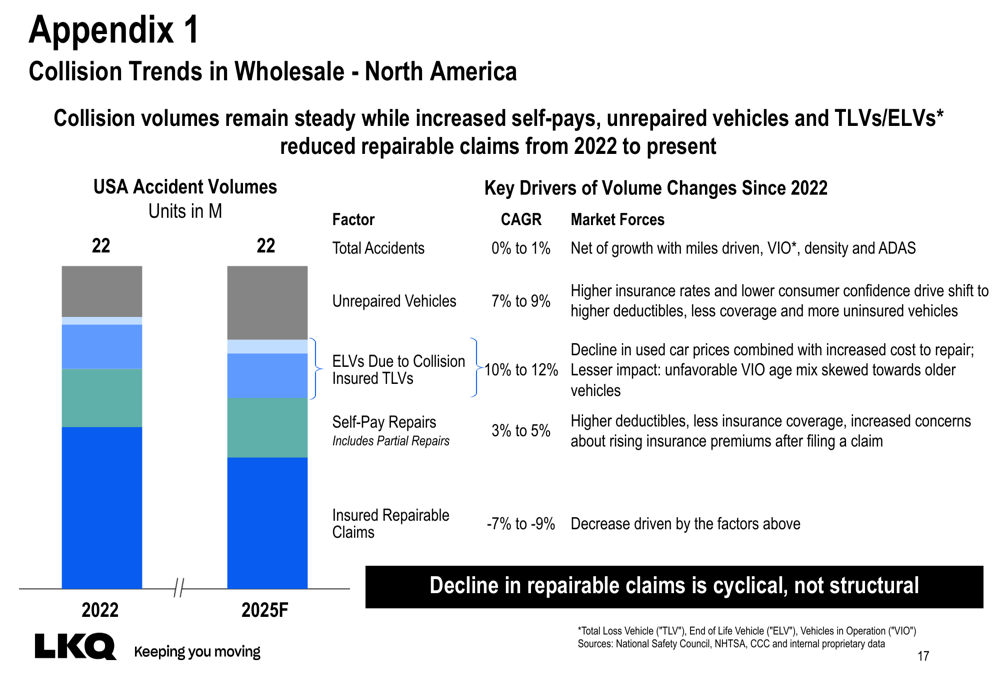

The presentation provided valuable insights into collision trends affecting LKQ’s North American wholesale business. The company noted that while overall accident volumes remain steady, there has been a significant shift in how these accidents translate to repairable claims.

The following chart illustrates these trends:

According to LKQ, insured repairable claims have declined at a 7-9% CAGR since 2022, driven by increases in unrepaired vehicles, total loss vehicles (TLVs), and self-pay repairs. The company attributes these changes to higher insurance rates, lower consumer confidence, declining used car prices, and increased repair costs. Importantly, LKQ believes this decline in repairable claims is cyclical rather than structural.

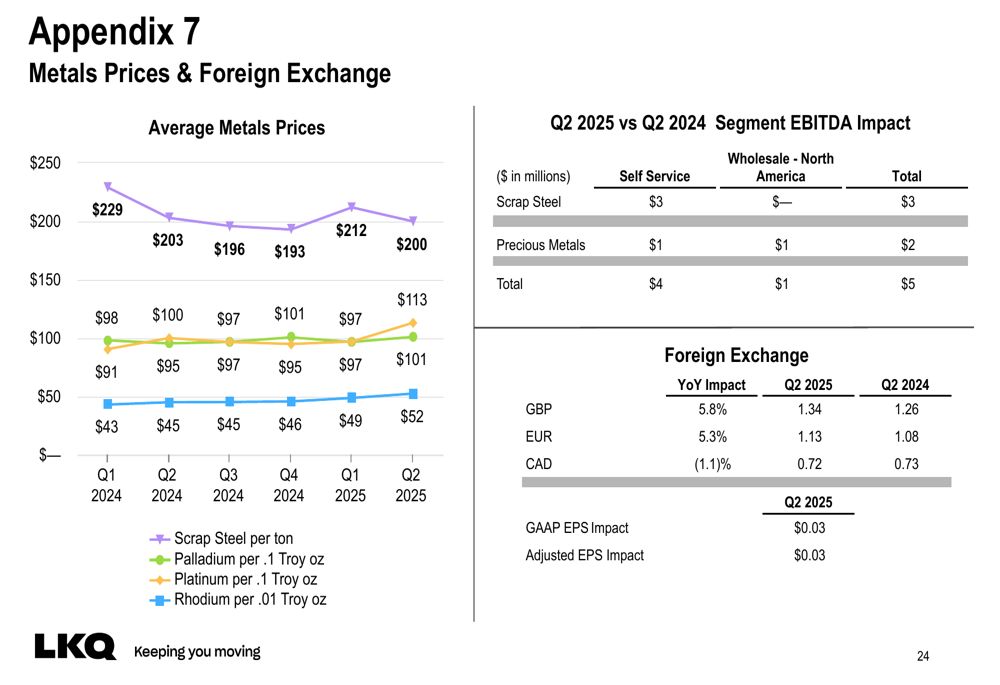

External factors such as metals prices and foreign exchange rates also impacted the quarter’s results:

Favorable movements in scrap steel and precious metals prices provided a $5 million boost to segment EBITDA, while foreign exchange movements, particularly the strengthening of the British pound and euro against the U.S. dollar, had a positive impact on reported EPS of $0.03.

Forward-Looking Statements

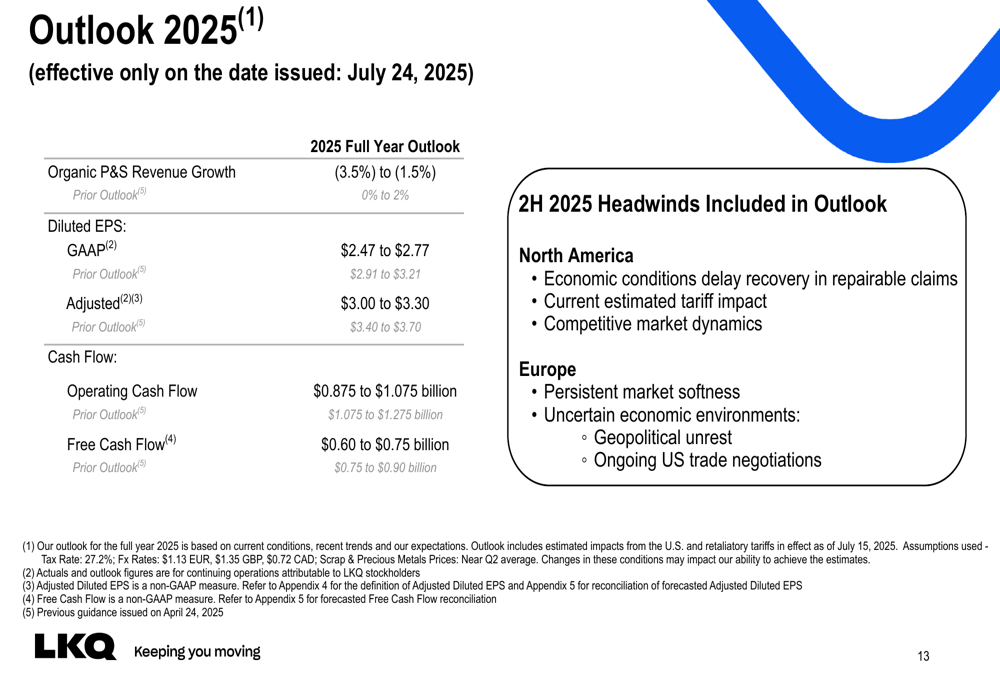

Perhaps most significantly, LKQ reduced its full-year 2025 outlook across several key metrics. The company now expects organic parts and services revenue to decline between 3.5% and 1.5%, compared to the previous guidance of growth at the lower end of a 0-2% range mentioned in the Q1 earnings call.

The revised outlook is detailed in the following slide:

Adjusted diluted EPS is now forecast at $3.00 to $3.30, down from the previous range of $3.40 to $3.70. Free cash flow expectations were also lowered to $0.60 to $0.75 billion from the prior range of $0.75 to $0.90 billion.

The company cited several headwinds for the second half of 2025, including delayed recovery in repairable claims, tariff impacts, competitive market dynamics in North America, persistent market softness in Europe, and geopolitical unrest.

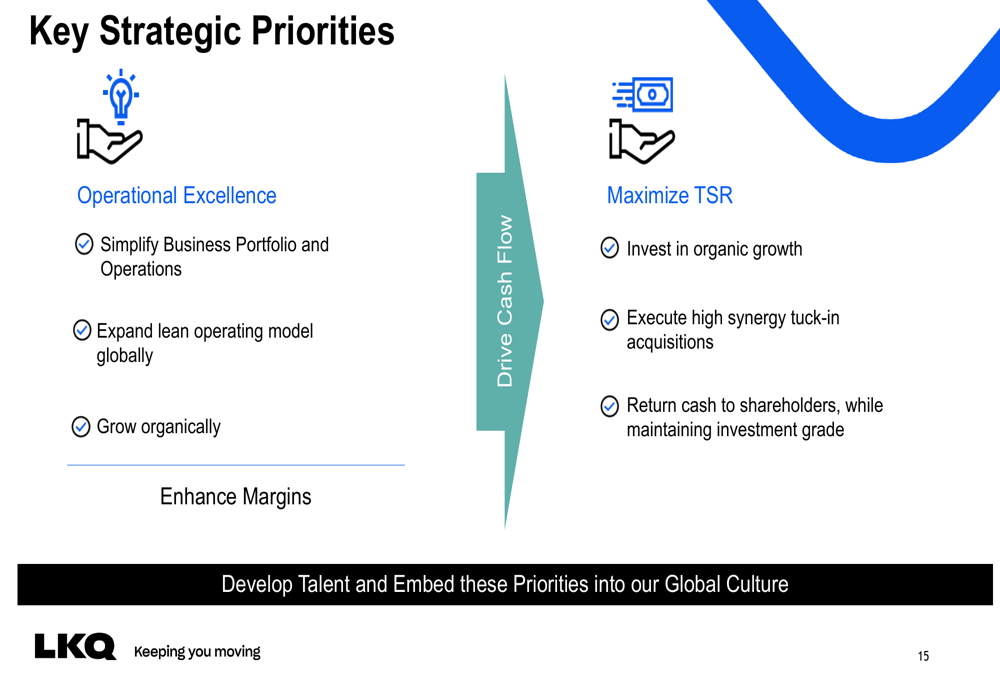

Despite these challenges, LKQ remains focused on its key strategic priorities:

The company’s strategic framework emphasizes operational excellence through simplifying the business portfolio, expanding the lean operating model, growing organically, and enhancing margins. LKQ also aims to maximize total shareholder return through organic growth investments, tuck-in acquisitions, and returning cash to shareholders while maintaining its investment grade status.

As LKQ navigates this challenging period, investors will be watching closely to see if the company’s cost-cutting initiatives and strategic repositioning can offset the significant market headwinds it faces across its global operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.