60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

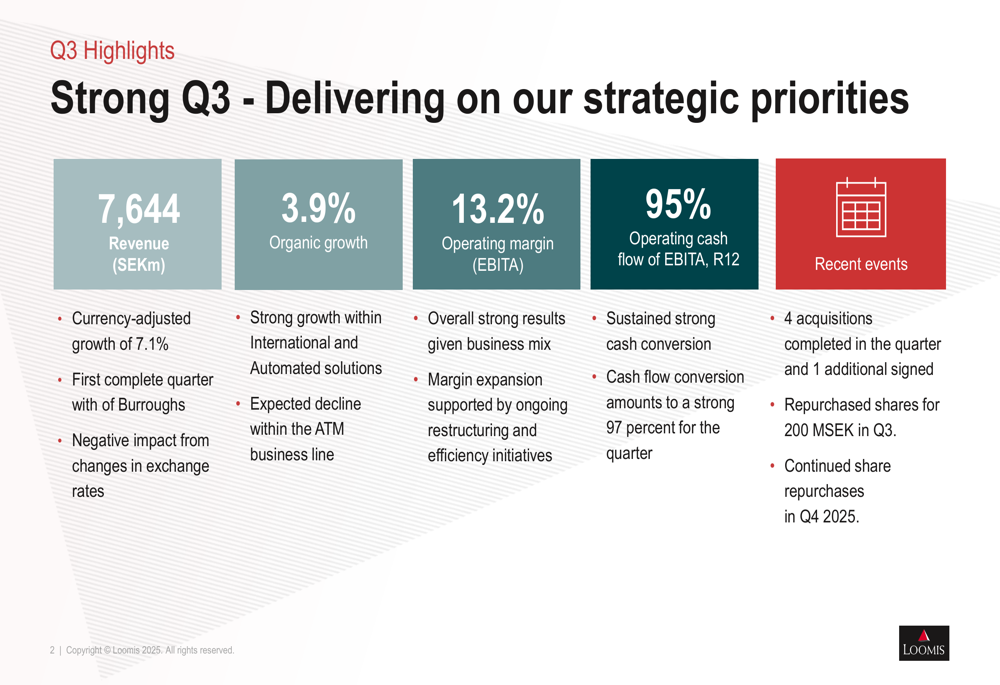

Loomis AB (STO:LOOMIS) presented its third-quarter 2025 results on October 31, showing continued growth despite currency headwinds. The cash handling and logistics company reported a 7.1% currency-adjusted revenue growth, with organic growth reaching 3.9%. Following the announcement, Loomis shares rose 0.68% to 387.2 SEK, building on the previous close of 384.6 SEK.

The company continues to execute its strategic transformation, shifting its business mix toward higher-margin services while maintaining strong cash conversion in its core operations. This quarter marked the first complete period with the Burroughs acquisition fully integrated into operations.

Quarterly Performance Highlights

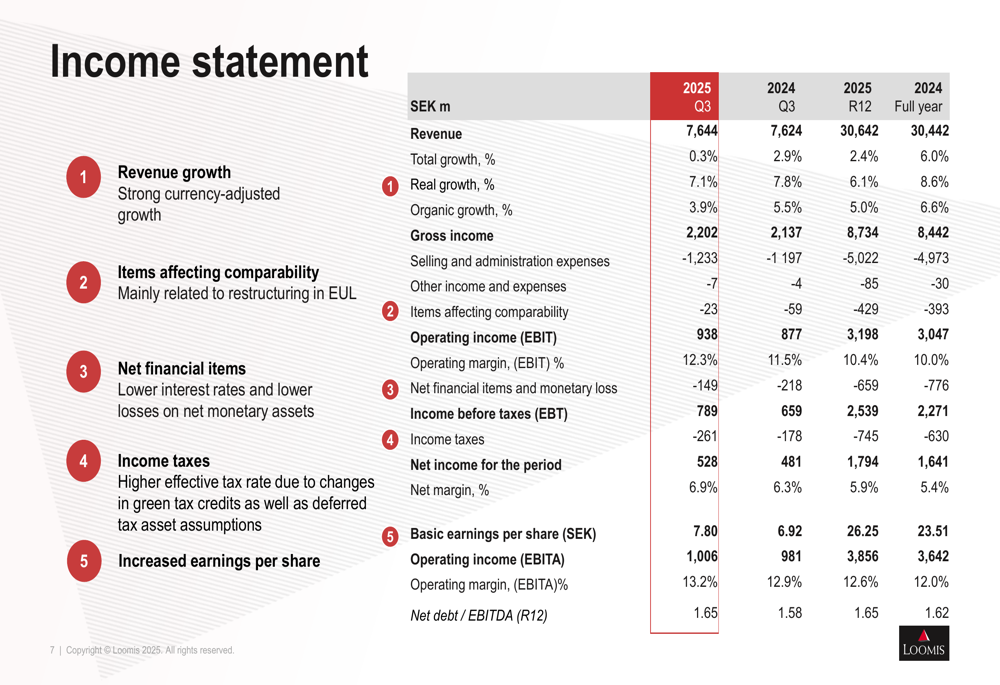

Loomis delivered solid financial results for Q3 2025, with revenue reaching 7,644 million SEK and an operating margin (EBITA) of 13.2%, an improvement from 12.9% in the same period last year. The company's operating cash flow represented 95% of EBITA, demonstrating strong cash conversion of 97% for the quarter.

As shown in the following comprehensive income statement, Loomis achieved total growth of 0.3% year-over-year, with real growth of 7.1% offset by negative currency effects:

The quarterly results reflect Loomis' ongoing business transformation, with strong performance in International and Automated solutions offsetting an expected decline in the ATM business line. The margin expansion was supported by ongoing restructuring and efficiency initiatives across the company's operations.

Segment Performance Analysis

Europe and Latin America

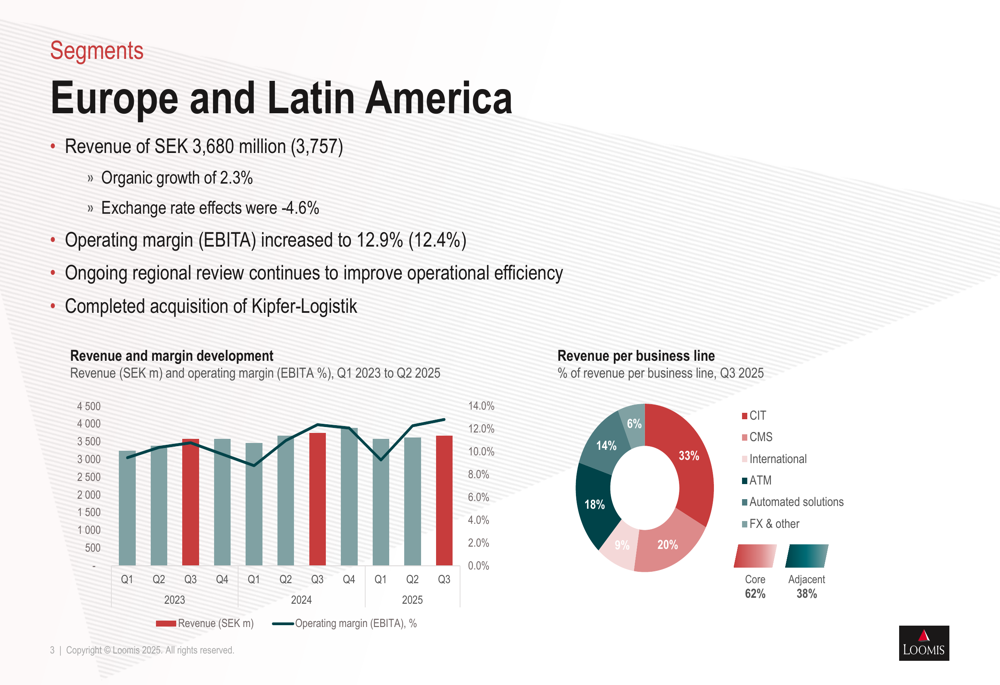

The Europe and Latin America segment generated revenue of 3,680 million SEK, down from 3,757 million SEK in the previous year, primarily due to negative exchange rate effects of -4.6%. However, organic growth remained positive at 2.3%, and the operating margin improved to 12.9% from 12.4%.

The segment's business mix shows diversification, with International services representing 33% of revenue, while traditional Cash in Transit (CIT) operations account for just 6%:

The ongoing regional review continues to improve operational efficiency in this segment, and the company completed the acquisition of Kipfer-Logistik during the quarter, strengthening its position in key European markets.

USA Segment

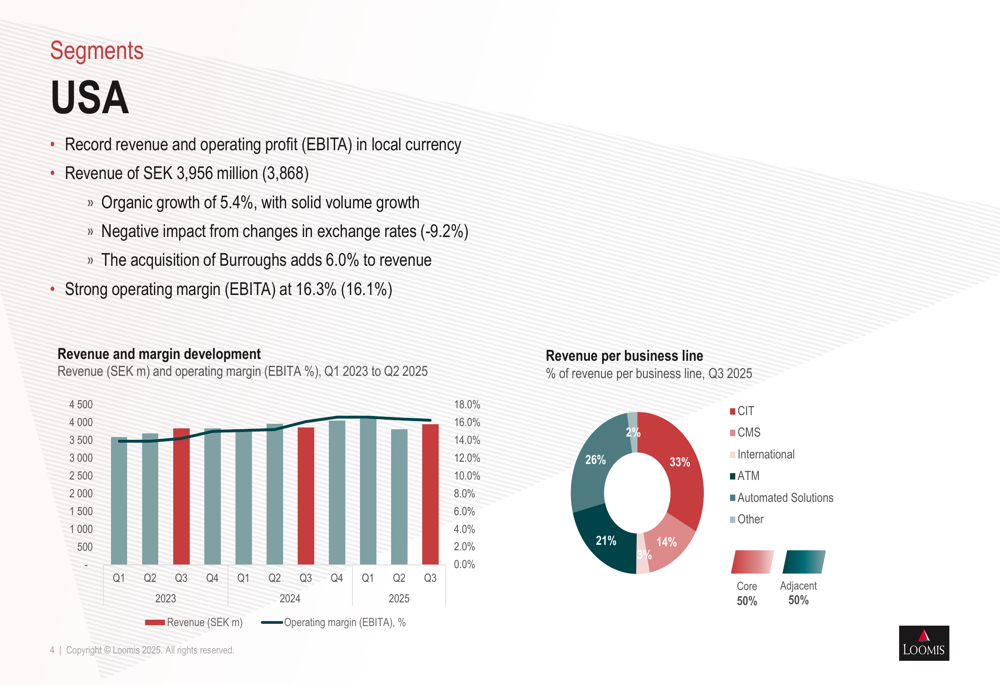

Loomis' USA segment achieved record revenue and operating profit in local currency, with total revenue reaching 3,956 million SEK compared to 3,868 million SEK in the previous year. The segment posted strong organic growth of 5.4%, though this was partially offset by negative currency effects of -9.2%.

The acquisition of Burroughs contributed significantly to growth, adding 6.0% to revenue. The operating margin remained strong at 16.3%, slightly up from 16.1% in the previous year:

The USA segment shows a more balanced revenue distribution between core and adjacent businesses (50% each), with International services (33%), Cash Management Services (26%), and ATM services (21%) representing the largest business lines.

SME/Pay Segment

The newly established SME/Pay segment, which reflects Loomis' strategic priority to expand solutions for small and medium-sized enterprises, generated revenue of 65 million SEK, up from 32 million SEK in the previous year. While still operating at a loss, the segment's operating income improved to -32 million SEK from -44 million SEK year-over-year.

Strategic Initiatives and Acquisitions

Loomis continued its active M&A strategy in Q3, completing four acquisitions during the quarter and signing an additional deal. The company also repurchased shares worth 200 million SEK in Q3 and indicated that share repurchases would continue in Q4 2025.

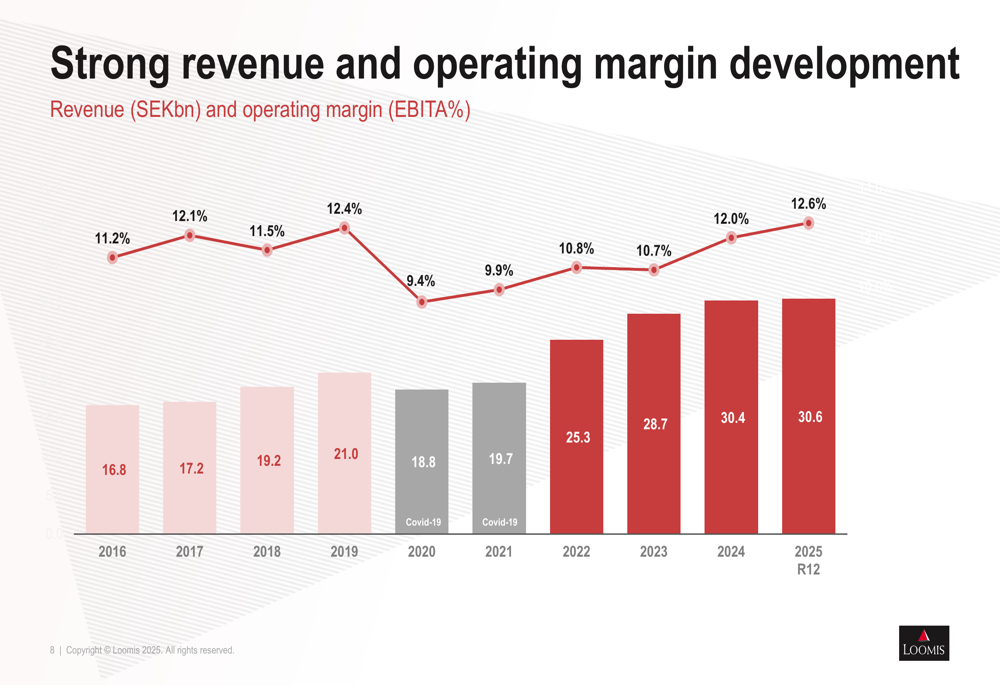

The company's long-term growth trajectory remains impressive, with revenue expanding from 16.8 billion SEK in 2016 to 30.6 billion SEK on a rolling 12-month basis in 2025, while operating margins have improved from 11.2% to 12.6% over the same period:

In July, Loomis acquired two point-of-sale companies in Spain, Central Cash and Sighore-ICS, strengthening its position in the payment solutions market. Transaction volumes for the SME/Pay segment exceeded 2.5 billion SEK during the quarter.

Sustainability Focus

Loomis continues to advance its emissions reduction initiatives, with the company reporting ongoing progress in reducing carbon emissions according to plan. The sequential increase in emissions from Q2 to Q3 was attributed to seasonality and recent acquisitions.

The company continues to roll out HVO (Hydrotreated Vegetable Oil) as an alternative fuel, though it noted that charging infrastructure remains a challenge for electrifying its fleet. During the quarter, Loomis' Board of Directors adopted two new policies to strengthen ESG commitments: a Human Rights Policy and an Environmental Policy.

Forward-Looking Statements

Loomis remains focused on delivering on its strategic priorities, with continued emphasis on expanding its footprint in the SME market and growing its adjacent and digital business lines. The company expects the decline in the ATM business to continue, reflecting broader industry trends, but aims to offset this through growth in other segments.

CEO Aritz Larrea characterized the quarter as "strong," highlighting the company's successful execution of strategic priorities despite currency headwinds. With a robust cash conversion rate and ongoing margin improvement, Loomis appears well-positioned to continue its business transformation while maintaining financial discipline.

The company's Q3 2025 highlights demonstrate the progress being made across key strategic initiatives:

As Loomis continues to shift its business mix toward higher-margin services and expand through strategic acquisitions, investors will be watching closely to see if the company can maintain its momentum in an evolving cash management and payment solutions landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.