Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

LSB Industries (NYSE:LXU) presented its fourth quarter 2024 earnings results on February 27, 2025, revealing a mixed financial performance characterized by improved operational metrics but disappointing bottom-line results. The nitrogen fertilizer and industrial chemicals producer reported a significant year-over-year improvement in adjusted EBITDA despite conducting a major facility turnaround during the quarter.

Following the earnings release, LSB’s stock declined by 2.21%, closing at $7.52, with after-hours trading showing further pressure to around $6.00 per share. The market reaction primarily reflected disappointment over the company’s earnings per share miss, as LSB reported an EPS of -$0.13, falling significantly short of analyst expectations of $0.13.

Quarterly Performance Highlights

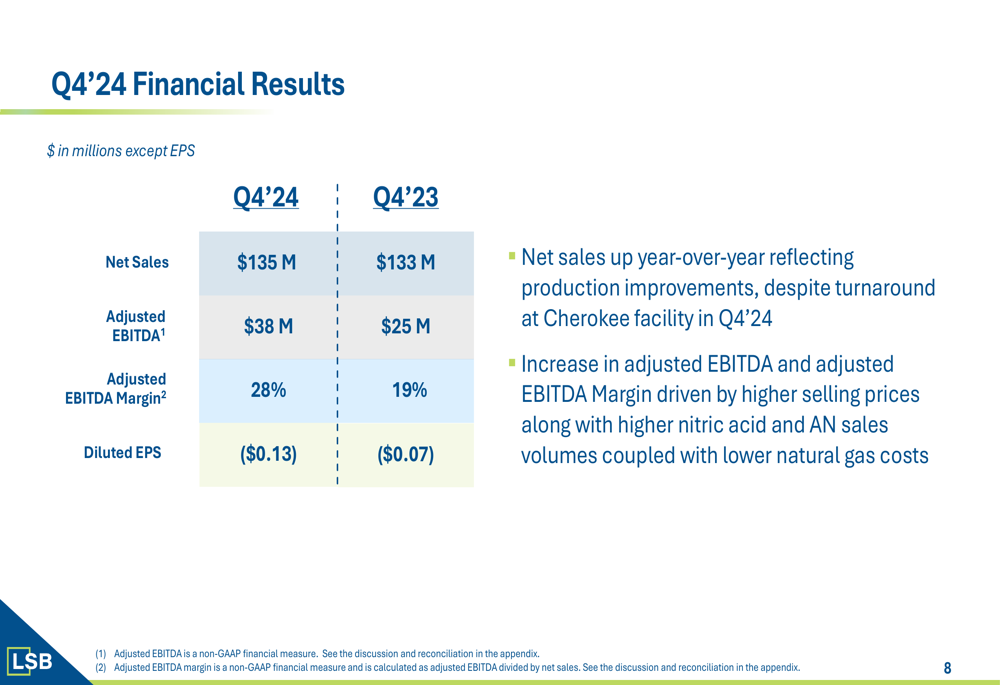

LSB Industries delivered solid year-over-year improvements in key operational metrics during the fourth quarter. The company reported net sales of $135 million, a slight increase from $133 million in Q4 2023, while adjusted EBITDA jumped 52% to $38 million from $25 million in the prior-year period. This improvement drove the adjusted EBITDA margin to 28%, up substantially from 19% in Q4 2023.

As shown in the following chart of quarterly financial performance:

The company attributed the improved EBITDA performance to higher selling prices along with increased nitric acid and ammonium nitrate (AN) sales volumes, coupled with lower natural gas costs. These positive factors were achieved despite a scheduled turnaround at the Cherokee ammonia plant during the quarter.

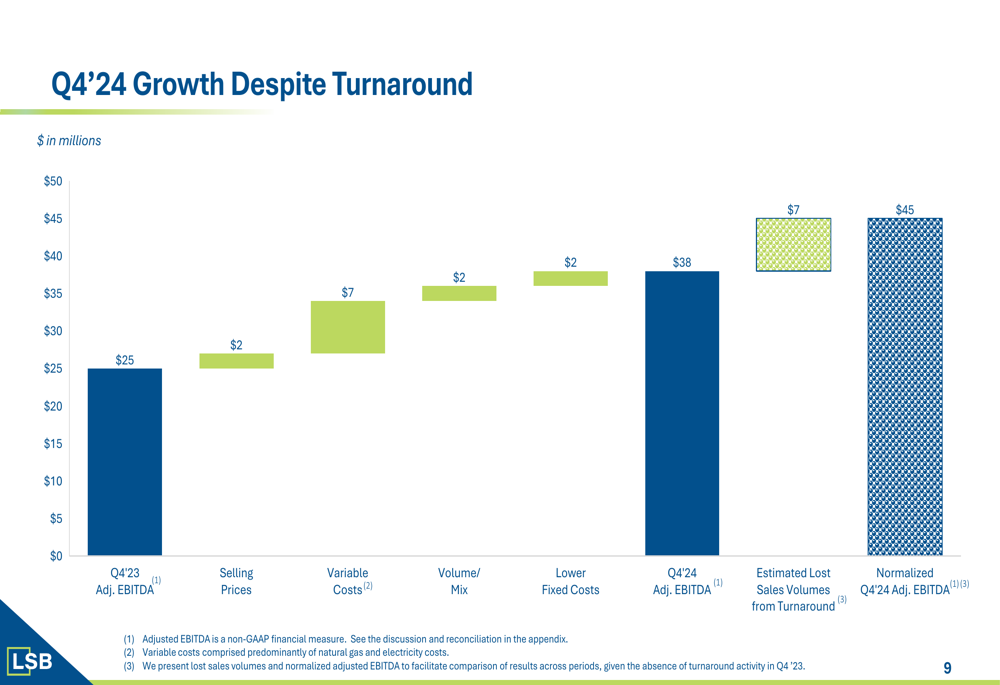

A detailed breakdown of the factors contributing to EBITDA growth is illustrated in this waterfall chart:

The analysis reveals that without the turnaround impact, which the company estimates reduced sales volumes worth approximately $7 million, normalized Q4 2024 adjusted EBITDA would have reached $45 million. This indicates the underlying operational strength of LSB’s business when running at full capacity.

Market Dynamics & Pricing Environment

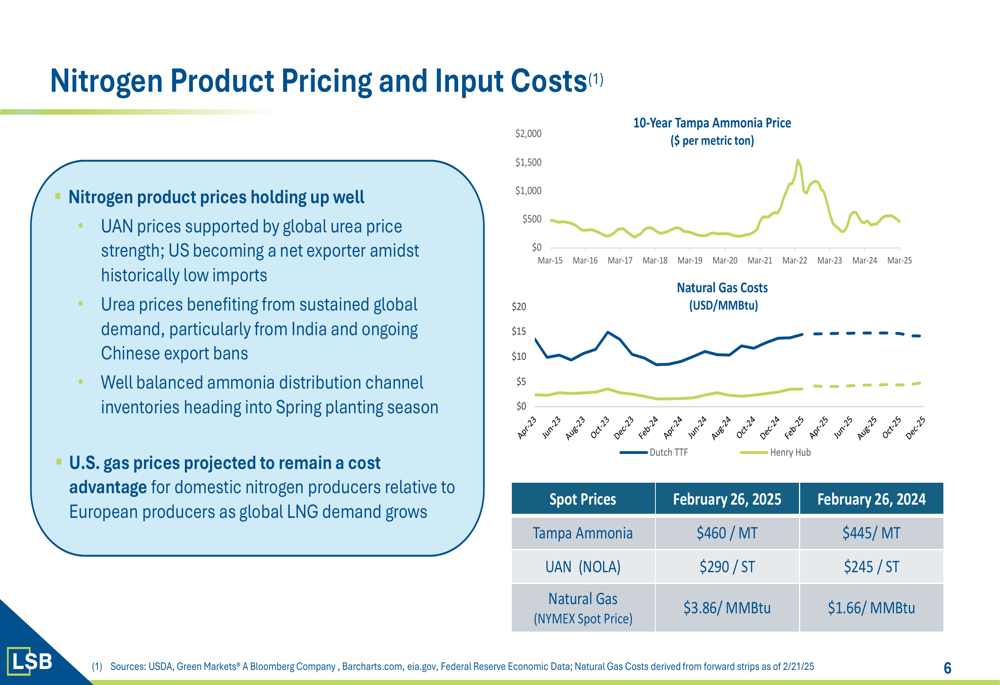

LSB’s presentation highlighted favorable market conditions for nitrogen products, with prices holding up well supported by global urea price strength and sustained demand. The company noted that U.S. natural gas prices, while higher than the previous year, continue to provide a cost advantage for domestic nitrogen producers compared to international competitors.

The pricing environment for key products showed year-over-year improvements, as illustrated in the following chart:

Tampa ammonia prices were $460/MT on February 26, 2025, up from $445/MT a year earlier, while UAN (NOLA) prices increased to $290/ST from $245/ST. However, natural gas costs also rose significantly to $3.86/MMBtu from $1.66/MMBtu in the prior year, creating some margin pressure.

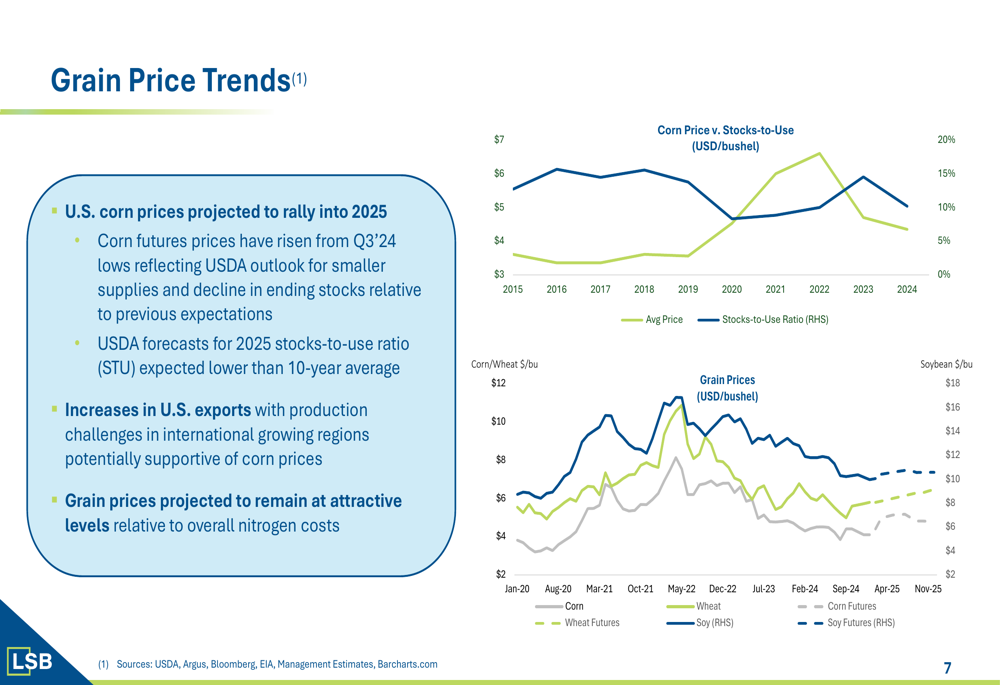

The agricultural market outlook appears positive, with U.S. corn prices projected to rally into 2025, supported by increased exports and production challenges in international growing regions. This favorable grain price environment is expected to sustain strong fertilizer demand.

Strategic Initiatives

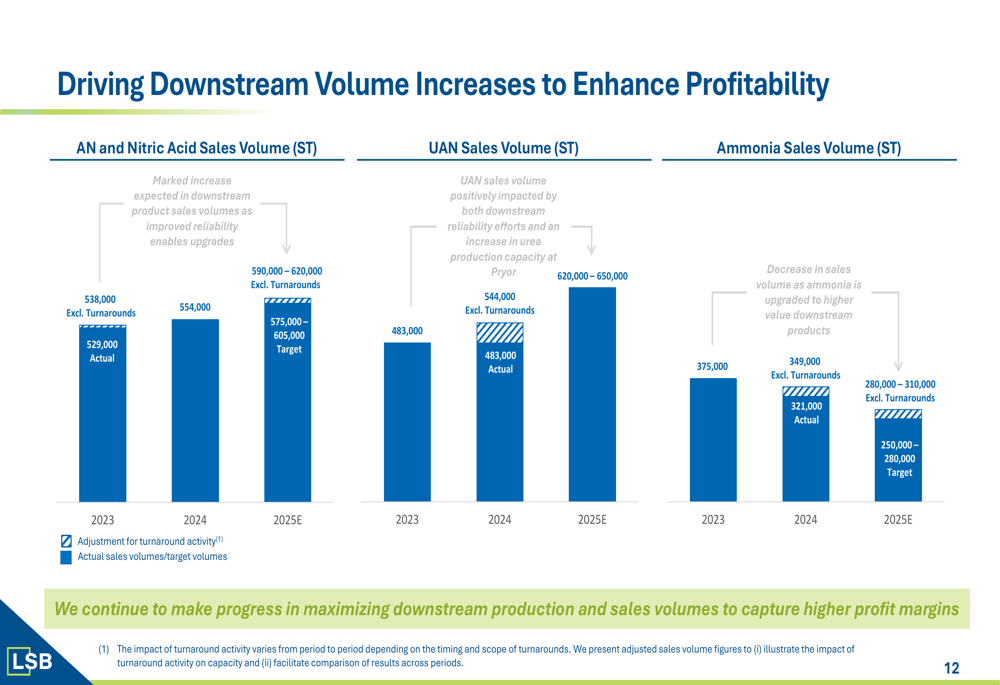

LSB’s presentation emphasized several strategic priorities designed to enhance profitability regardless of market pricing conditions. The company is focusing on maximizing downstream production and sales volumes to capture higher profit margins, reducing reliance on commodity ammonia sales.

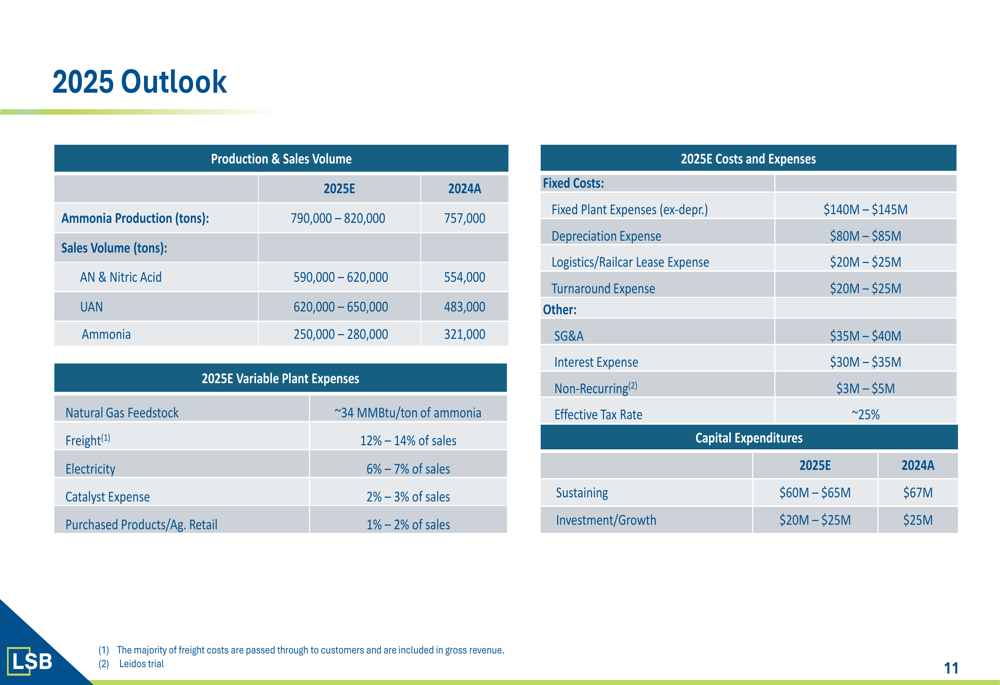

This strategy is reflected in the company’s production and sales volume trends:

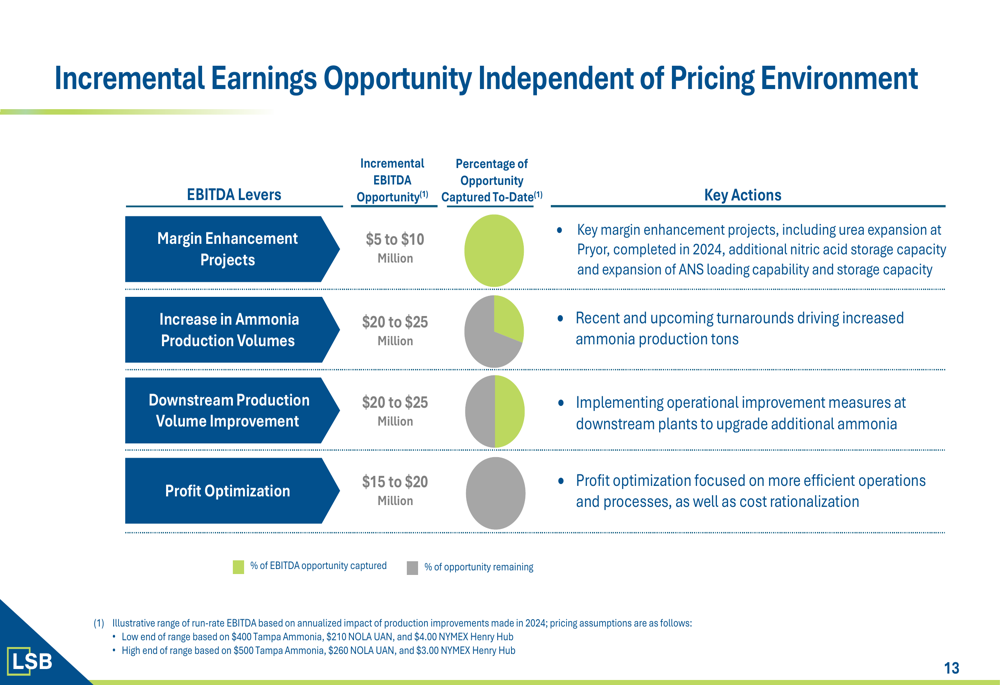

The company has identified incremental earnings opportunities totaling $60-80 million that are independent of the pricing environment, including margin enhancement projects, increased ammonia production volumes, downstream production improvements, and profit optimization initiatives.

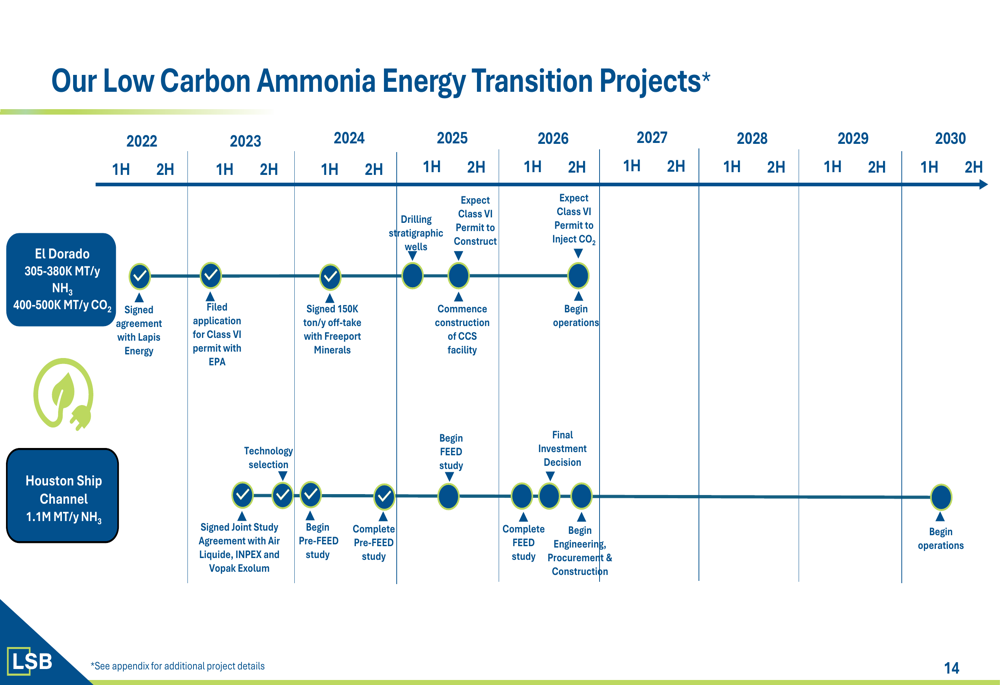

A significant component of LSB’s long-term strategy involves low-carbon ammonia projects, which position the company to benefit from the energy transition. The company provided updates on two major initiatives:

1. El Dorado Low Carbon Ammonia Project - This carbon capture and sequestration project is expected to reduce LSB’s Scope 1 CO2 emissions by approximately 25% and generate an estimated $15-20 million in incremental EBITDA once operational.

2. Houston Ship Channel Ammonia Project - A new 1.1 million TPA low-carbon ammonia plant being developed in partnership with Air Liquide (OTC:AIQUY), INPEX, and Vopak (AS:VOPA) exolun, targeting both domestic and export markets, particularly power generation demand from Japan and Korea.

Balance Sheet & Capital Allocation

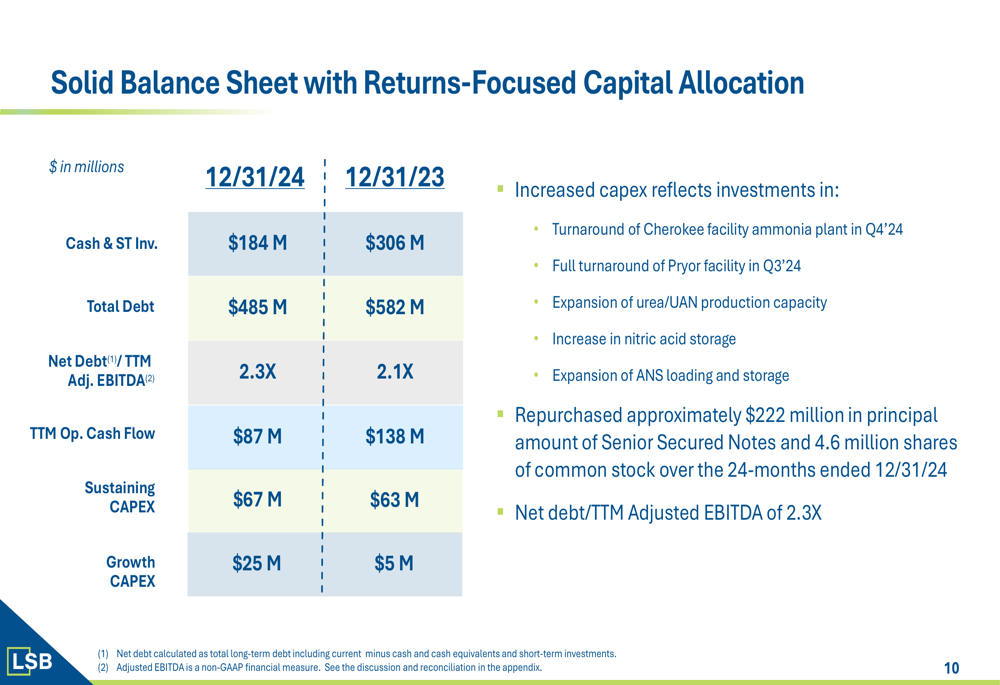

LSB maintained a solid balance sheet while pursuing a returns-focused capital allocation strategy. As of December 31, 2024, the company reported cash and short-term investments of $184 million, down from $306 million at the end of 2023, primarily reflecting investments in growth initiatives and shareholder returns.

The company’s financial position is summarized in the following table:

Total (EPA:TTEF) debt decreased to $485 million from $582 million a year earlier, while the net debt to trailing twelve-month adjusted EBITDA ratio increased slightly to 2.3x from 2.1x. Over the 24 months ended December 31, 2024, LSB repurchased approximately $222 million in principal amount of Senior Secured Notes and 4.6 million shares of common stock, demonstrating its commitment to returning capital to shareholders.

Capital expenditures increased in 2024, reflecting investments in facility turnarounds, expansion of urea/UAN production capacity, and increased nitric acid storage capabilities.

Forward-Looking Statements

Looking ahead to 2025, LSB provided detailed guidance on production volumes, sales, and costs. The company expects ammonia production of 790,000-820,000 tons, with sales volumes of 590,000-620,000 tons for AN and nitric acid, 620,000-650,000 tons for UAN, and 250,000-280,000 tons for ammonia.

The company’s outlook for nitrogen demand and pricing remains favorable, supported by global market dynamics and continued strength in both agricultural and industrial sectors. LSB expects its low-carbon ammonia projects to progress according to the established timelines, with the El Dorado project potentially contributing to earnings in the coming years.

Analyst Perspectives & Market Reaction

Despite the operational improvements and strategic progress highlighted in the presentation, LSB’s stock faced pressure following the earnings release, primarily due to the significant EPS miss. According to available data, the stock closed at $7.52 following the announcement, down 2.21%, with after-hours trading showing further declines.

Analysts have maintained price targets ranging from $8.75 to $15 for LSB stock, suggesting potential upside from current levels if the company can translate its operational improvements and strategic initiatives into consistent profitability. However, the market appears to be taking a cautious approach, focusing on the earnings miss rather than the improved EBITDA performance.

During the earnings call, CEO Mark Berman emphasized the company’s commitment to the energy transition, stating, "We are a big believer in the energy transition. We do think that demand will materialize over time." He also highlighted LSB’s strategic approach to production and profitability, noting, "Ultimately, it’s about taking that product that we produce and trying to make the most money."

As LSB continues to execute its strategic initiatives and navigate market dynamics, investors will be closely watching whether the company can translate its operational improvements into consistent bottom-line results in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.