IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

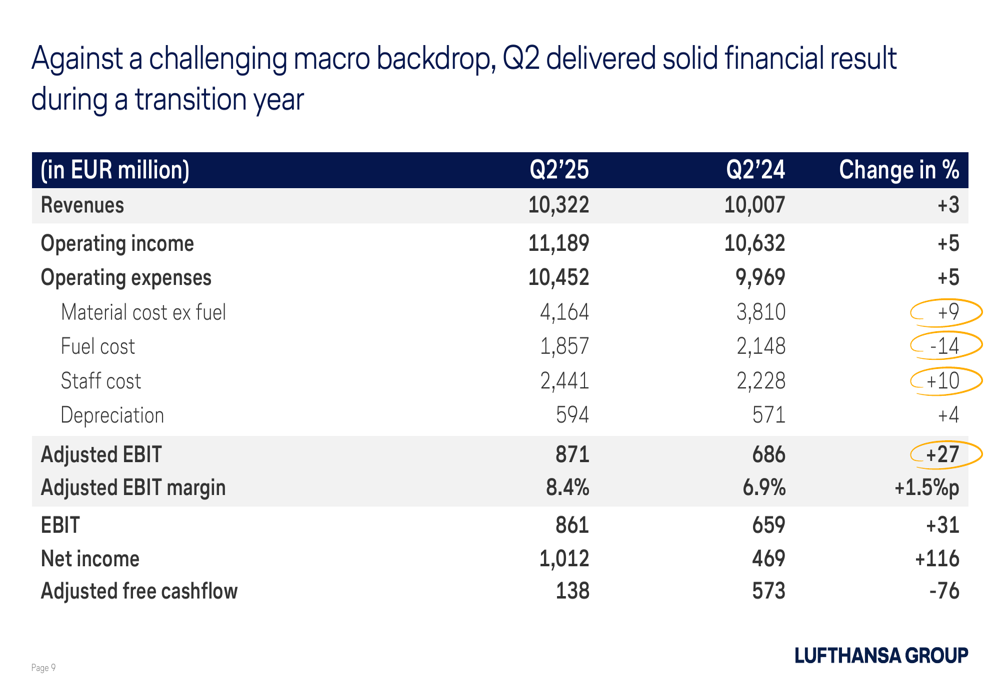

Deutsche Lufthansa AG (OTC:DLAKY) (ETR:LHA) presented its Q2 2025 financial results on July 31, 2025, revealing significant improvements in profitability despite ongoing challenges in the aviation sector. The German airline group reported a 27% increase in adjusted EBIT to €871 million and more than doubled its net income compared to the same period last year.

The results come after a strong first quarter, when the company reported a 10% year-over-year revenue increase. Lufthansa’s stock has shown positive momentum, with shares rising 9.41% following the Q1 announcement earlier this year, reflecting investor confidence in the company’s recovery trajectory.

Quarterly Performance Highlights

Lufthansa reported Q2 2025 revenues of €10.3 billion, representing a €315 million increase compared to Q2 2024. The company achieved this growth despite facing yield pressure, with passenger yield declining by 1.5% year-over-year.

As shown in the following comprehensive financial breakdown, the airline significantly improved its profitability metrics across the board:

The most notable improvement came in net income, which more than doubled to €1,012 million (+116% year-over-year). This substantial increase was achieved despite a 5% rise in operating expenses, driven primarily by a 10% increase in staff costs and 9% higher material costs excluding fuel.

Operational stability also improved markedly, with 99% regularity and an 8 percentage point improvement in punctuality compared to Q2 2024. The company highlighted that these operational improvements resulted in a 28% reduction in financial irregularity impact.

Segment Performance

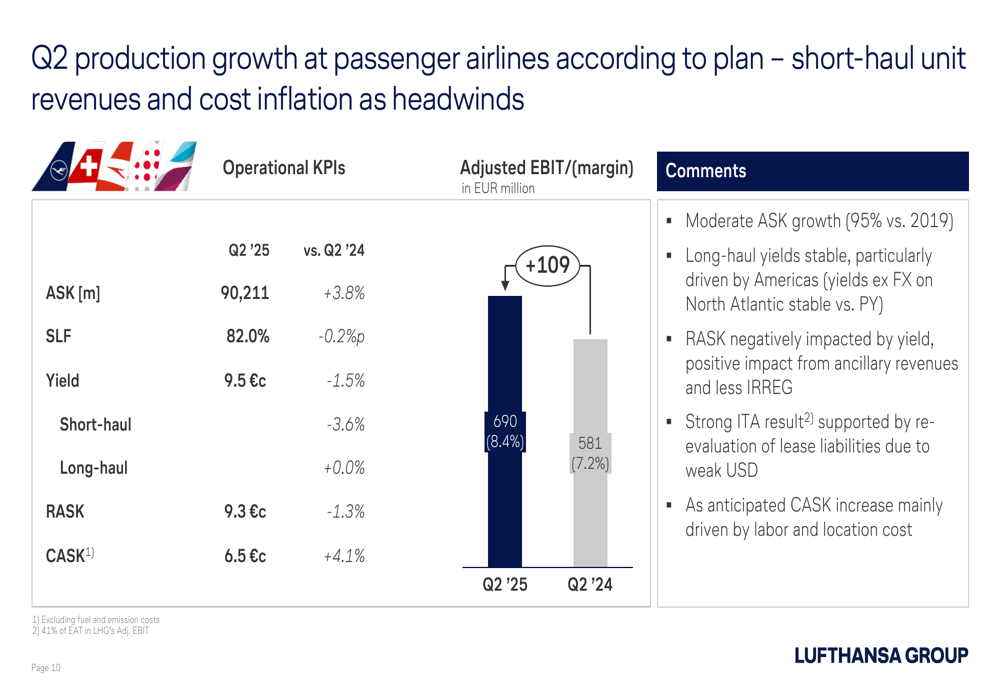

Lufthansa’s passenger airlines segment faced mixed results, with capacity growth offset by yield pressure. Available seat kilometers (ASK) increased by 3.8% year-over-year, while passenger load factor remained relatively stable at 82.0% (-0.2 percentage points).

The following slide illustrates the passenger airlines’ performance metrics:

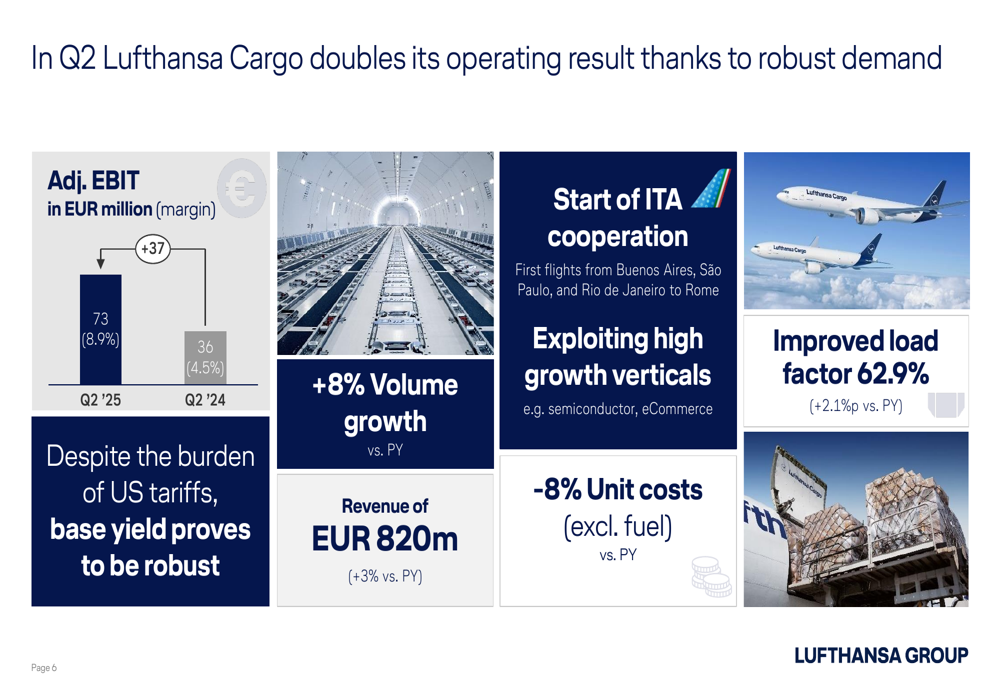

In contrast to the passenger business, Lufthansa Cargo delivered exceptional results, doubling its operating result thanks to robust demand. The cargo division achieved an 8% volume growth compared to the previous year, with revenues increasing by 3% to €820 million.

As shown in this detailed breakdown of the cargo segment’s performance:

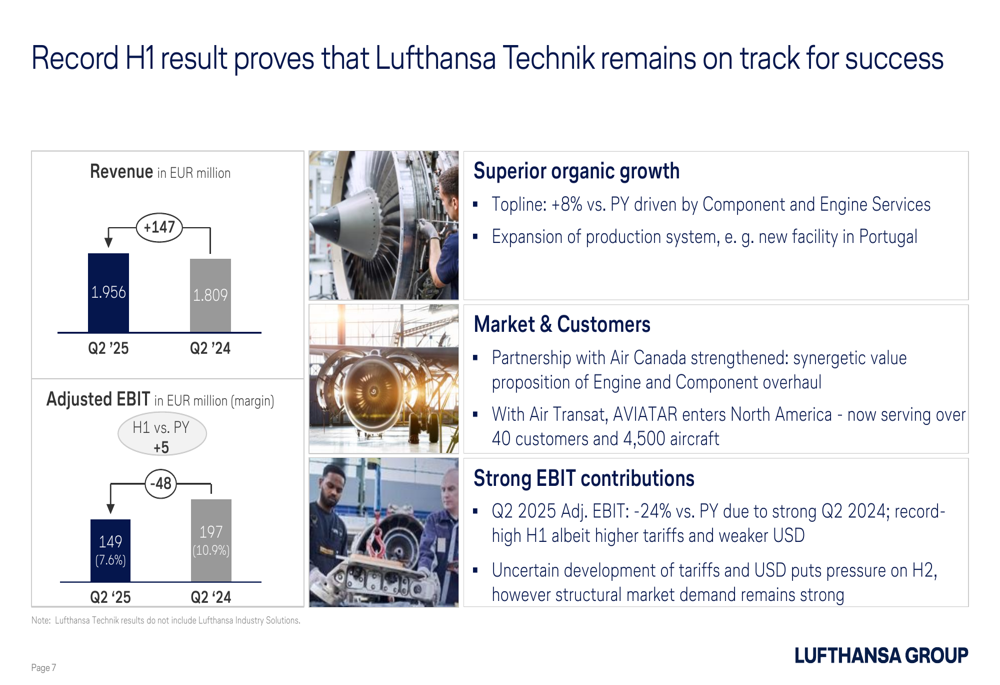

Lufthansa Technik also performed strongly, achieving record H1 results despite headwinds from higher tariffs and a weaker USD. The maintenance, repair, and overhaul division reported an 8% revenue growth driven by Component and Engine Services.

Strategic Initiatives

The company highlighted several strategic initiatives that contributed to its improved performance. The Lufthansa Airlines turnaround program is showing tangible results, with a 35% reduction in irregularity costs compared to H1 2024 and significant operational improvements.

The integration of ITA Airways is progressing rapidly, with codeshares now possible on long-haul flights and the first positive financial contribution to Lufthansa Group results. The company also reported harmonized benefits for status customers between the two airlines.

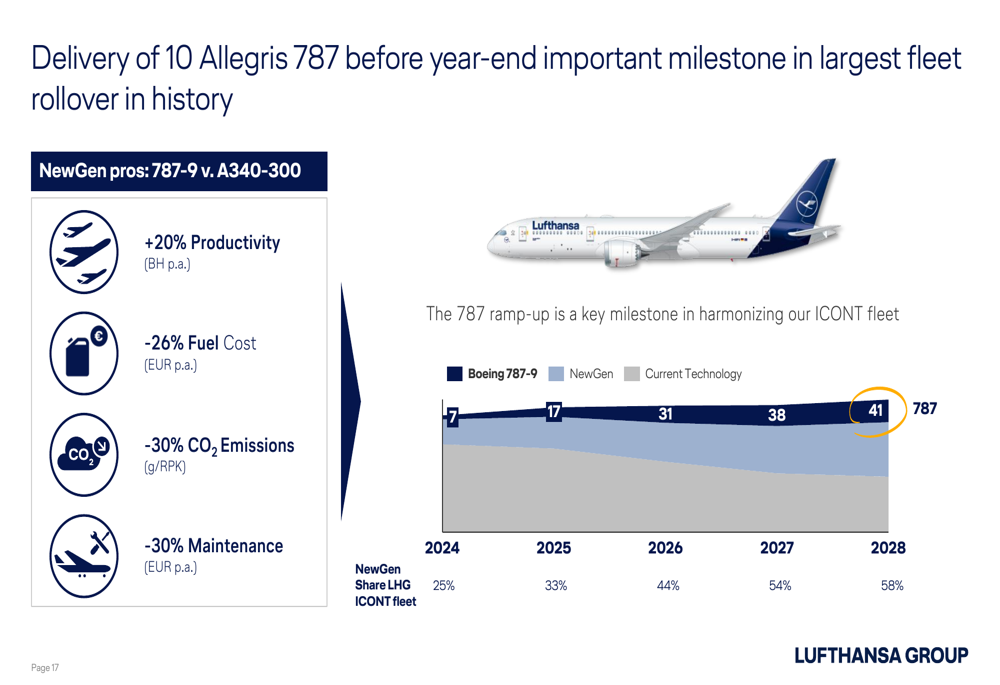

Fleet modernization remains a key focus, with 10 Allegris-equipped Boeing (NYSE:BA) 787 aircraft expected to be in operation by year-end. These next-generation aircraft offer significant advantages over older models:

The company is also enhancing customer experience through premiumization and advanced digitization, resulting in improved customer satisfaction metrics:

Balance Sheet and Cash Flow

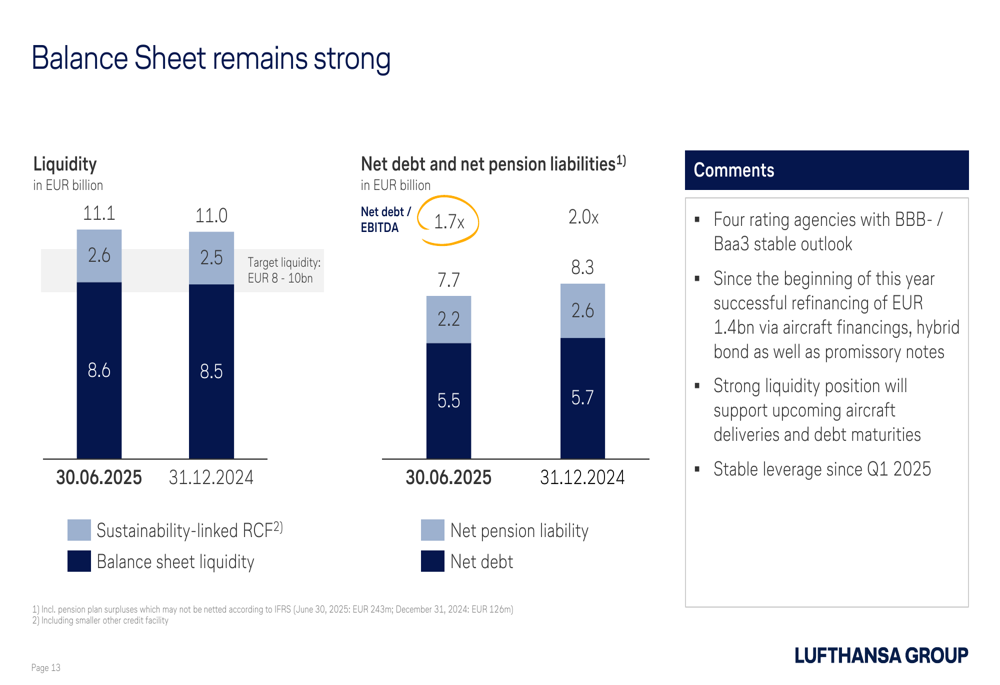

Lufthansa maintained a strong financial position with total liquidity of €11.1 billion as of June 30, 2025. The company’s net debt to EBITDA ratio stood at 1.7x, indicating a healthy balance sheet.

The following slide illustrates the company’s balance sheet strength:

Adjusted free cash flow for Q2 2025 was €138 million, representing a 76% decrease compared to the same period last year. However, for the first half of 2025, adjusted free cash flow increased to €1,024 million from €878 million in H1 2024.

Forward-Looking Statements

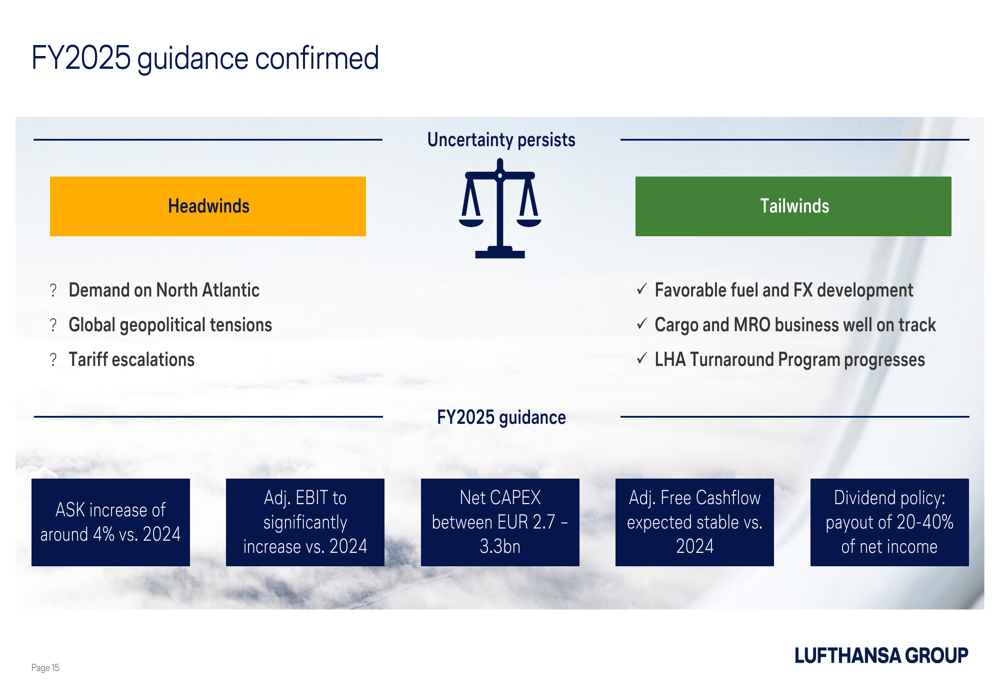

Looking ahead, Lufthansa maintained its positive outlook for FY2025 despite acknowledging several headwinds and tailwinds affecting the business:

The company expects ASK to increase by approximately 4% compared to 2024 and projects adjusted EBIT to significantly increase versus the previous year. Net capital expenditure is forecast between €2.7-3.3 billion, with adjusted free cash flow expected to remain stable compared to 2024.

Fuel costs are projected to be €7.2 billion for the full year, slightly lower than the April guidance of €7.3 billion. The company has hedged 82% of its fuel requirements for Q3 and 81% for the full year 2025.

Lufthansa’s dividend policy remains unchanged, with a planned payout of 20-40% of net income, underscoring management’s confidence in the company’s financial performance and future prospects despite ongoing challenges in the global aviation market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.