German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Lument Finance Trust Inc (NYSE:LFT) released its Q1 2025 earnings presentation on May 13, 2025, revealing a challenging quarter marked by a GAAP net loss and increased loan loss provisions. The real estate investment trust, which focuses primarily on multifamily debt investments, reported results that indicate some deterioration in portfolio performance while maintaining its strategic focus on multifamily assets.

The company’s stock closed at $2.63 on May 12, down 0.75% for the day, with a modest 0.33% gain in after-hours trading. LFT shares have been trading between $2.22 and $2.84 over the past 52 weeks, suggesting relatively stable investor sentiment despite the quarterly challenges.

Quarterly Performance Highlights

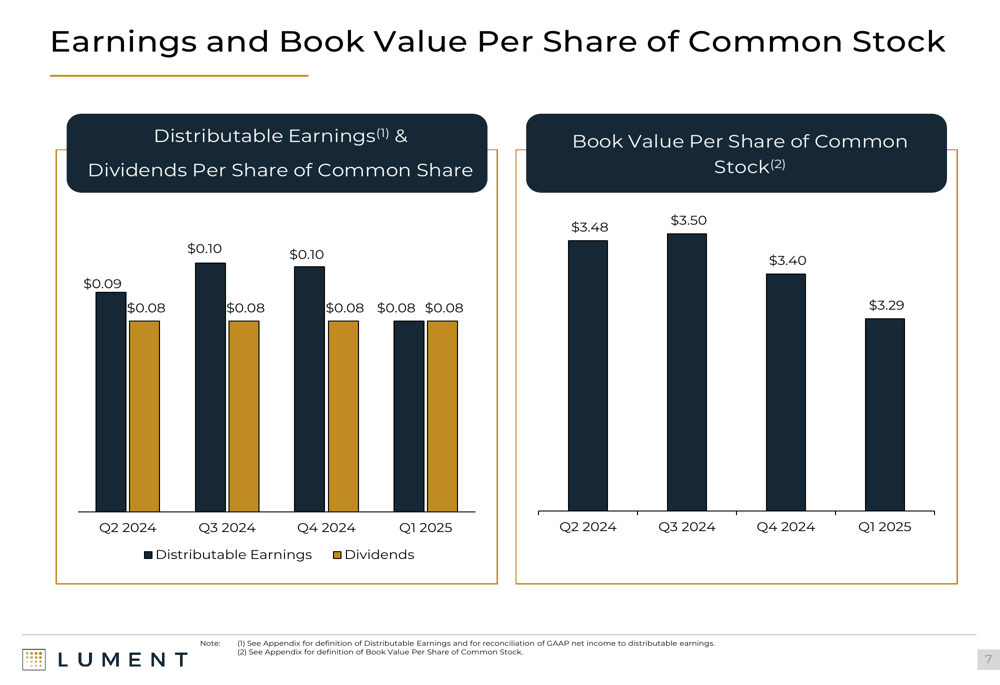

Lument Finance Trust reported a GAAP net loss attributable to common stockholders of $0.03 per share for Q1 2025, a significant decline from the $0.07 per share net income reported in Q4 2024. Distributable earnings, a key metric for REITs, came in at $0.08 per share, down from $0.10 in the previous quarter but still covering the declared dividend of $0.08 per share.

As shown in the following chart of quarterly distributable earnings and dividends:

The company’s book value per share of common stock declined to $3.29 as of March 31, 2025, continuing a downward trend from $3.40 at the end of Q4 2024 and $3.50 at the end of Q3 2024. This represents a 3.2% quarter-over-quarter decrease in book value.

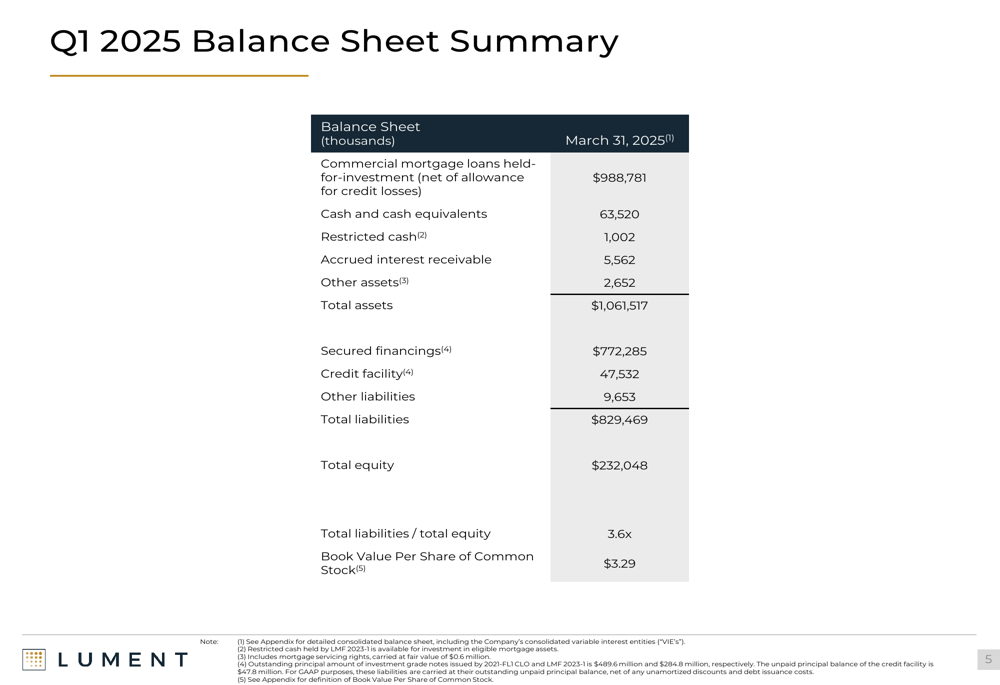

The balance sheet showed total assets of $1.06 billion as of March 31, 2025, with commercial mortgage loans held-for-investment (net of allowance for credit losses) accounting for $988.8 million. The company maintained a healthy cash position of $63.5 million.

The detailed balance sheet summary reveals the company’s financial position:

Portfolio Composition and Credit Quality

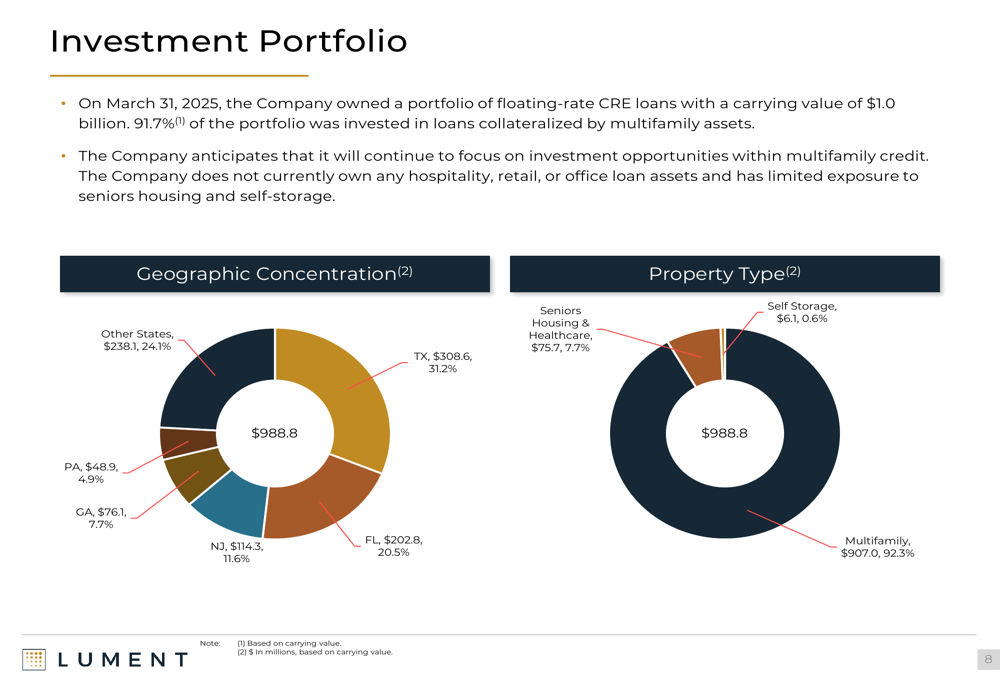

Lument Finance Trust’s investment strategy remains heavily focused on multifamily assets, which comprised 91.7% of its floating-rate commercial real estate loan portfolio as of March 31, 2025. The remainder consisted of seniors housing & healthcare (7.7%) and self-storage (0.6%), with no exposure to hospitality, retail, or office loan assets.

The geographic distribution of the portfolio shows significant concentration in Texas (31.2%), Florida (20.5%), and New Jersey (11.6%), as illustrated in the following breakdown:

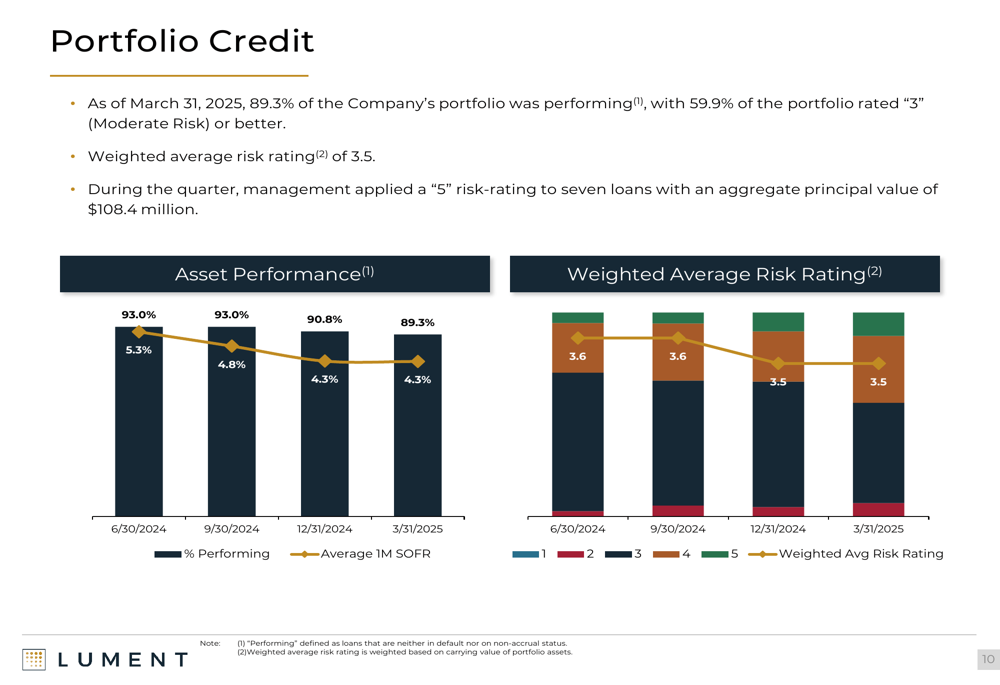

Portfolio credit quality showed signs of stress during the quarter. While the weighted average risk rating remained stable at 3.5, the percentage of performing loans decreased from 90.8% at the end of Q4 2024 to 89.3% as of March 31, 2025. Management applied a "5" risk-rating (the highest risk category) to seven loans with an aggregate principal value of $108.4 million during the quarter.

The following chart illustrates the trend in asset performance and weighted average risk rating:

The company recorded a significant provision for credit losses of $5.7 million in Q1 2025, contributing to the quarterly net loss. This increased the allowance for credit losses to $17.1 million as of March 31, 2025, up from $11.3 million at the beginning of the period.

Capital Structure and Financing

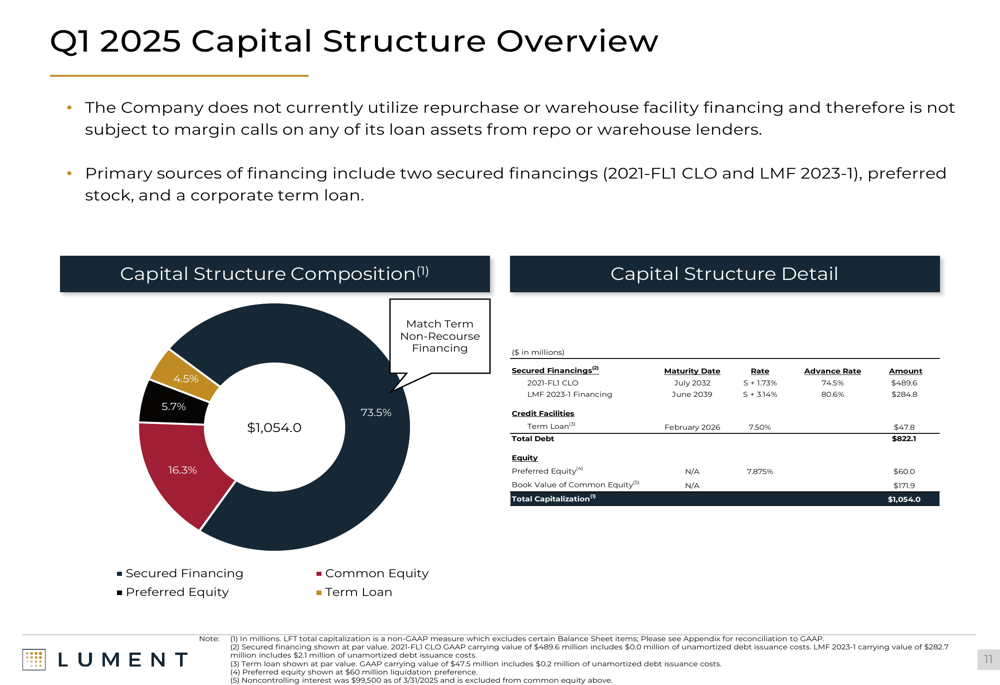

Lument Finance Trust maintains a diversified capital structure with a focus on secured financing. The company does not utilize repurchase or warehouse facility financing, instead relying primarily on two secured financings: the 2021-FL1 CLO ($489.6 million) and LMF 2023-1 ($284.8 million).

The capital structure composition as of March 31, 2025 is illustrated below:

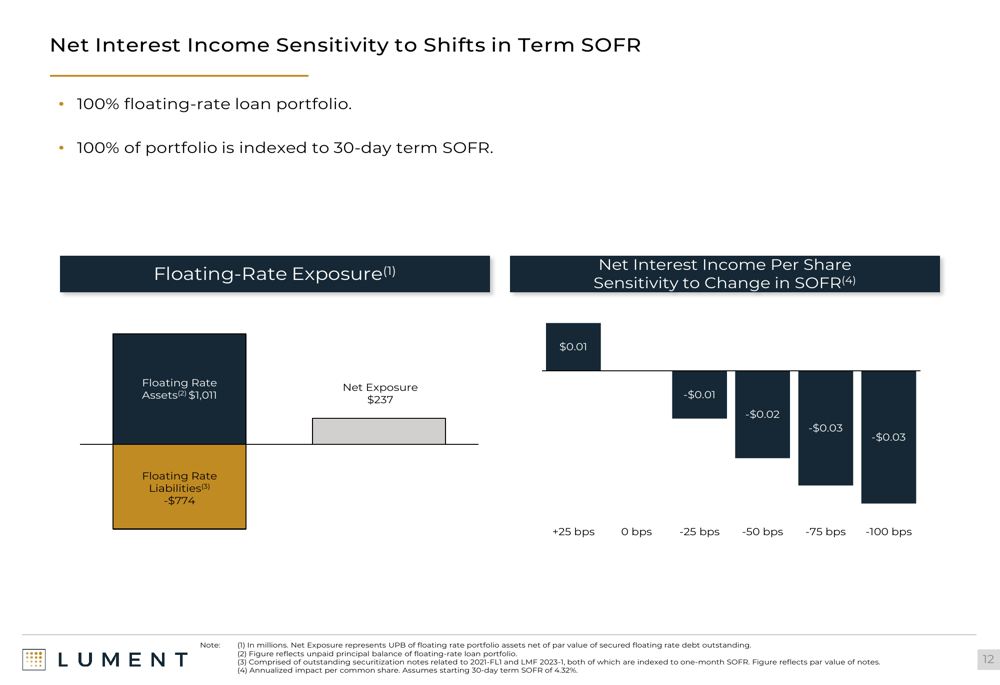

The company’s leverage ratio improved slightly from 3.7x to 3.6x quarter-over-quarter. The loan portfolio was 100% floating-rate and indexed to 30-day term SOFR, creating a net floating rate exposure of $237 million after accounting for floating-rate liabilities.

The sensitivity of net interest income to shifts in SOFR is shown in the following chart:

Forward-Looking Statements

Despite the challenging quarter, Lument Finance Trust continues to emphasize its strategic focus on middle market multifamily debt investments. The company highlights its strong sponsorship through its external manager, Lument Investment Management, LLC, an affiliate of ORIX Corporation USA, which provides access to an extensive loan origination platform and experienced management team.

The company experienced $54.7 million of loan payoffs during Q1 2025, all from multifamily properties. With a weighted average remaining initial term of 5 months across the portfolio, Lument may see additional loan resolutions in the coming quarters.

Looking ahead, investors should monitor the company’s ability to address the increased number of higher-risk loans in its portfolio and the impact of potential interest rate changes on its net interest income. The significant provision for credit losses in Q1 2025 suggests management is taking a more conservative approach to potential credit issues, which could impact distributable earnings in future quarters if the trend continues.

In its Q4 2024 earnings call, CEO Jim Flynn had expressed optimism about "increasing stability in commercial real estate," but the Q1 2025 results indicate ongoing challenges in portfolio performance. The company’s ability to maintain its dividend coverage while addressing credit quality concerns will be a key focus for investors in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.