EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

Luminar Technologies (NASDAQ:LAZR) presented its Q1 2025 operating plan and business update on May 14, 2025, highlighting a strategic pivot toward a unified product architecture while navigating ongoing revenue challenges. The LiDAR technology provider’s stock closed at $4.76, up 5.08% on the day, with an additional 1.79% gain in after-hours trading, suggesting cautious investor optimism about the company’s restructuring efforts.

The presentation comes as Luminar continues its transition from a development-stage company to a production-focused enterprise, balancing the need to scale operations while managing costs in the competitive automotive LiDAR market. This strategic update follows a challenging Q4 2024, where the company reported mixed results with revenue growth but significant earnings per share misses.

Strategic Initiatives: Unified Product Architecture

The centerpiece of Luminar’s presentation was the introduction of its new unified product architecture centered around "Luminar Halo," which represents a significant departure from both industry norms and Luminar’s previous approach of developing multiple LiDAR variants.

As shown in the following comparison of product architectures:

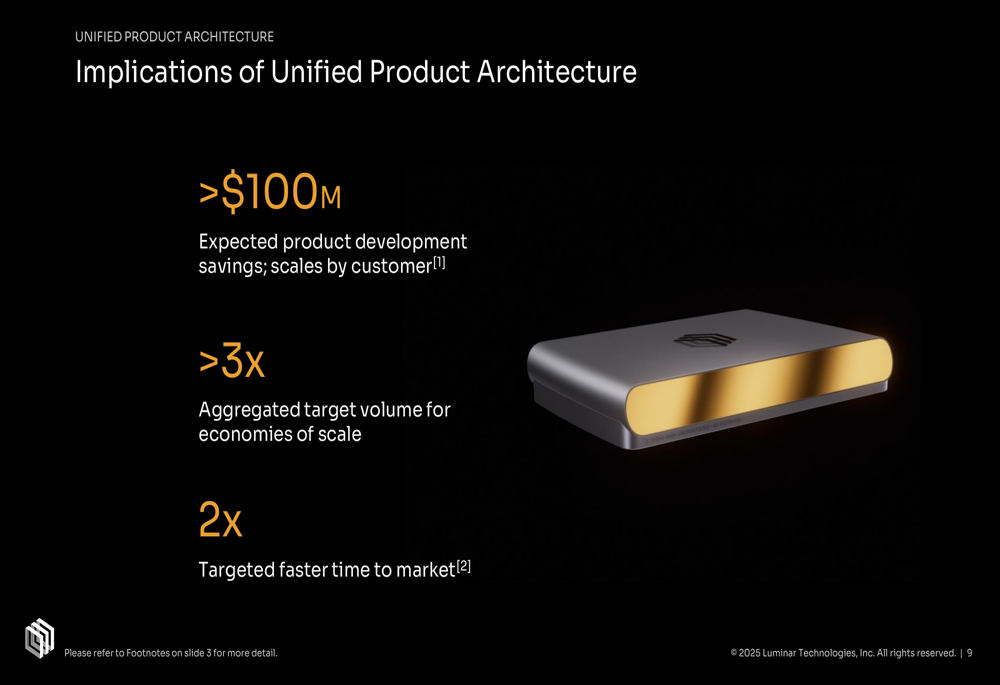

The company emphasized that this unified approach will deliver substantial benefits, including over $100 million in expected product development savings, more than triple the aggregated target volume for economies of scale, and twice the targeted time to market compared to its previous model.

Luminar highlighted three key enablers of this unified architecture:

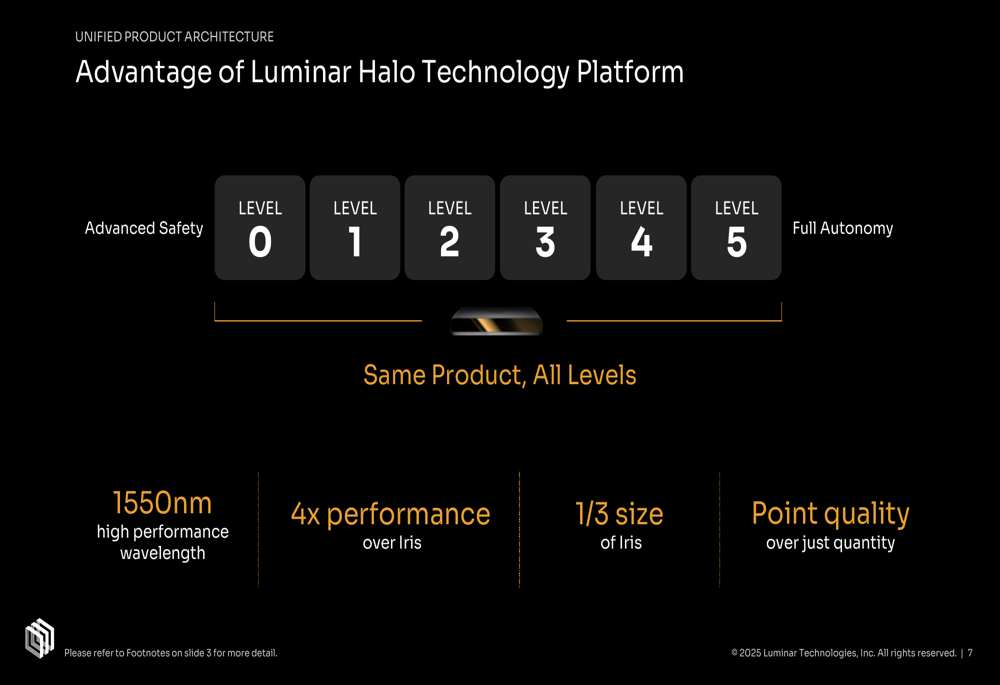

The Luminar Halo platform is designed to support all levels of autonomous driving capabilities, from basic safety features to full autonomy, using the same underlying hardware:

A critical component of Luminar’s strategy is securing global OEM partnerships. The presentation highlighted alignment with major automotive manufacturers including Nissan (OTC:NSANY), Mercedes-Benz (OTC:MBGAF), Volvo (OTC:VLVLY) Cars, and Polestar (NASDAQ:PSNY):

The company quantified the expected benefits of this unified approach:

Operational Streamlining and Cost Reduction

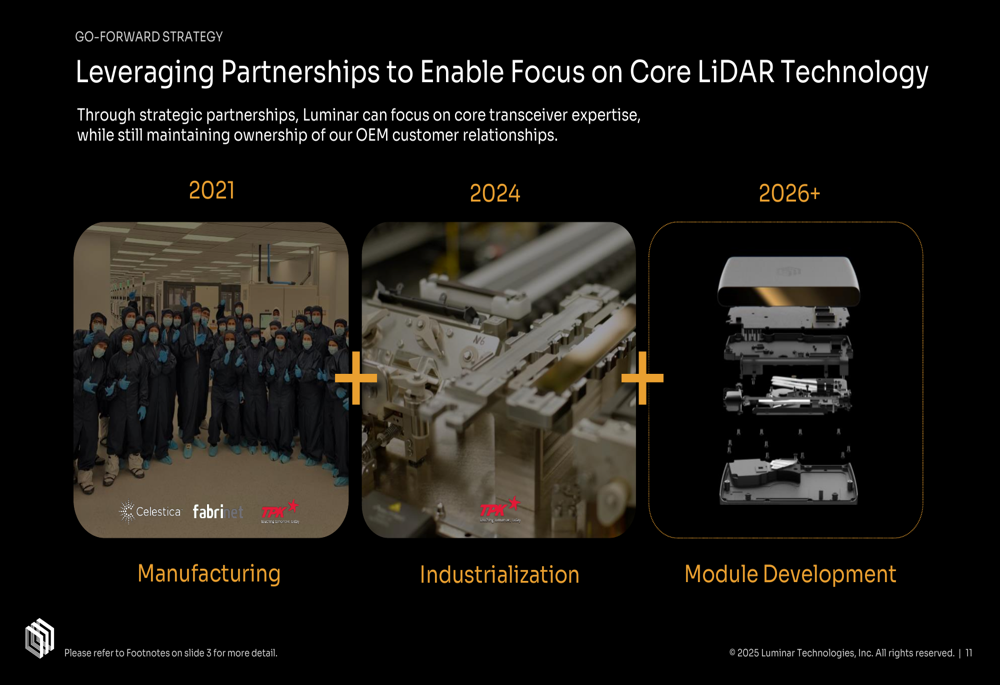

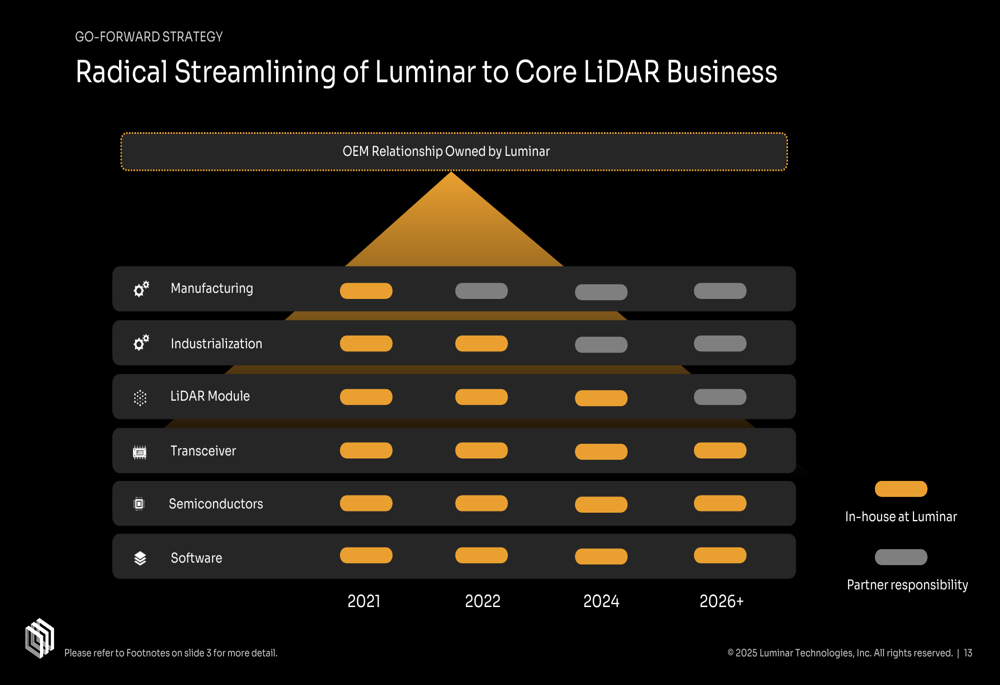

Luminar outlined a comprehensive operational streamlining initiative, shifting from a vertically integrated model to focusing on its core LiDAR technology while leveraging partnerships for manufacturing, industrialization, and module development.

The following timeline illustrates this evolution:

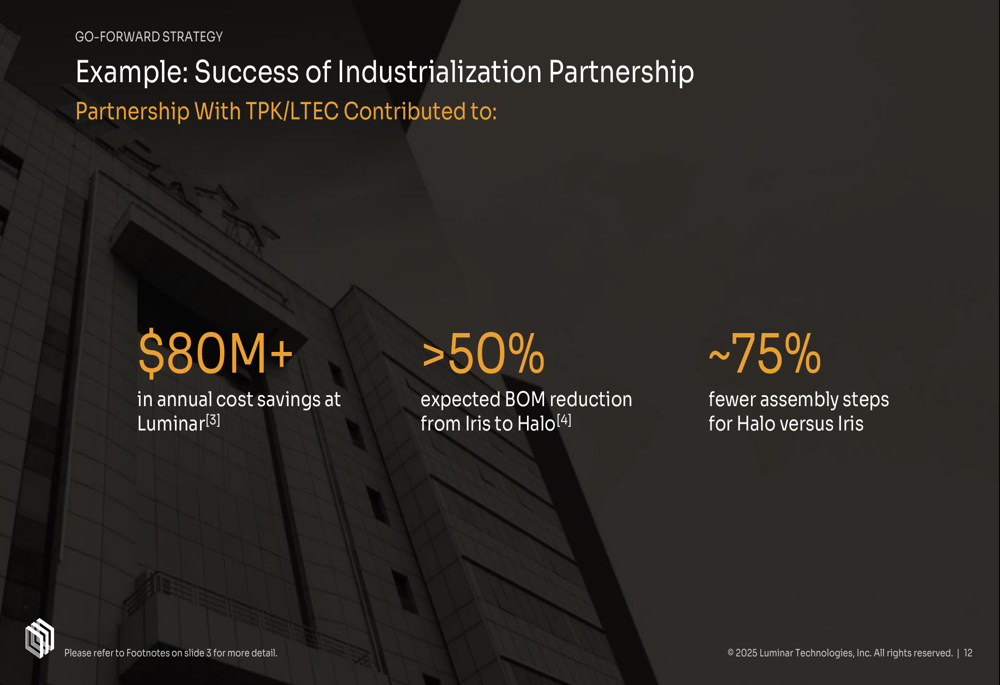

The company highlighted significant cost savings achieved through its industrialization partnership with TPK/LTEC:

Luminar presented a detailed visualization of its shift toward focusing exclusively on core IP and technology:

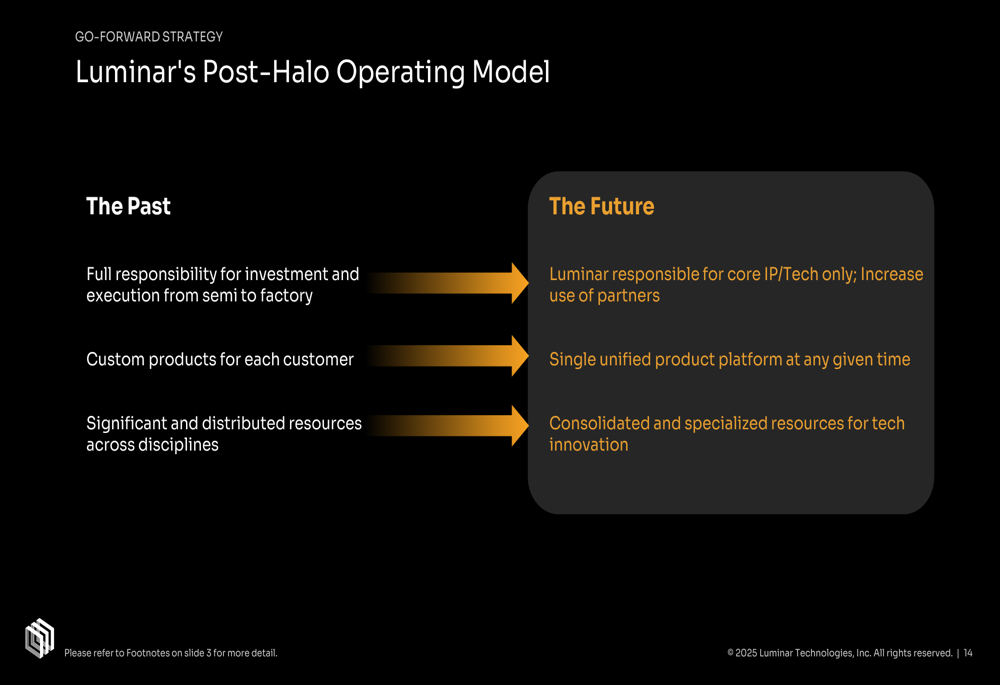

The company contrasted its past operating model with its future vision:

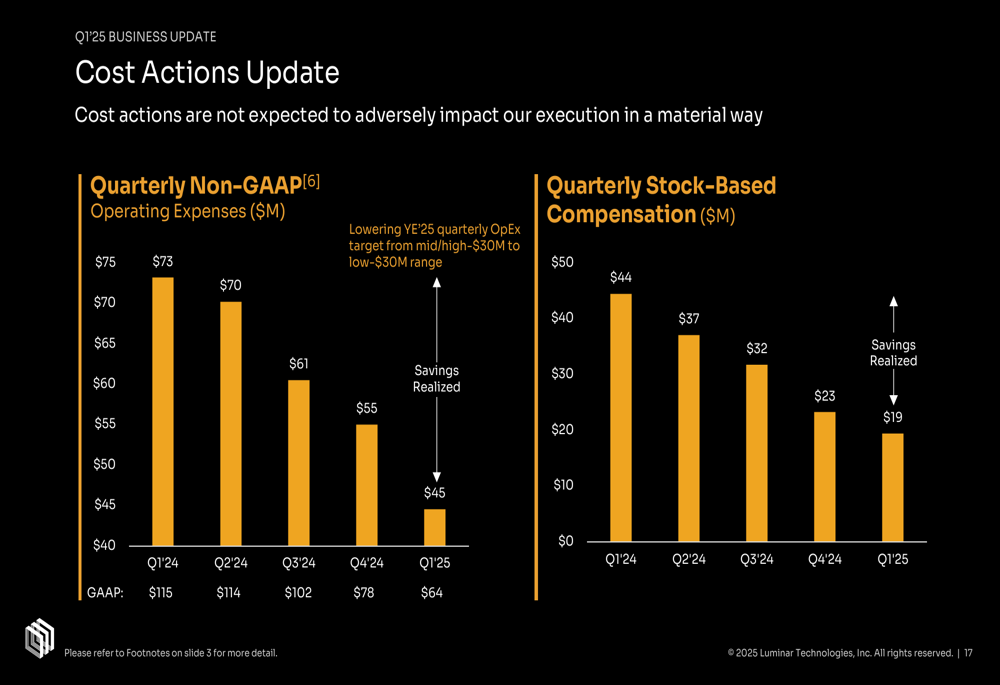

These cost-cutting efforts are already showing results, as demonstrated in the quarterly operating expenses and stock-based compensation charts:

Quarterly Performance Highlights

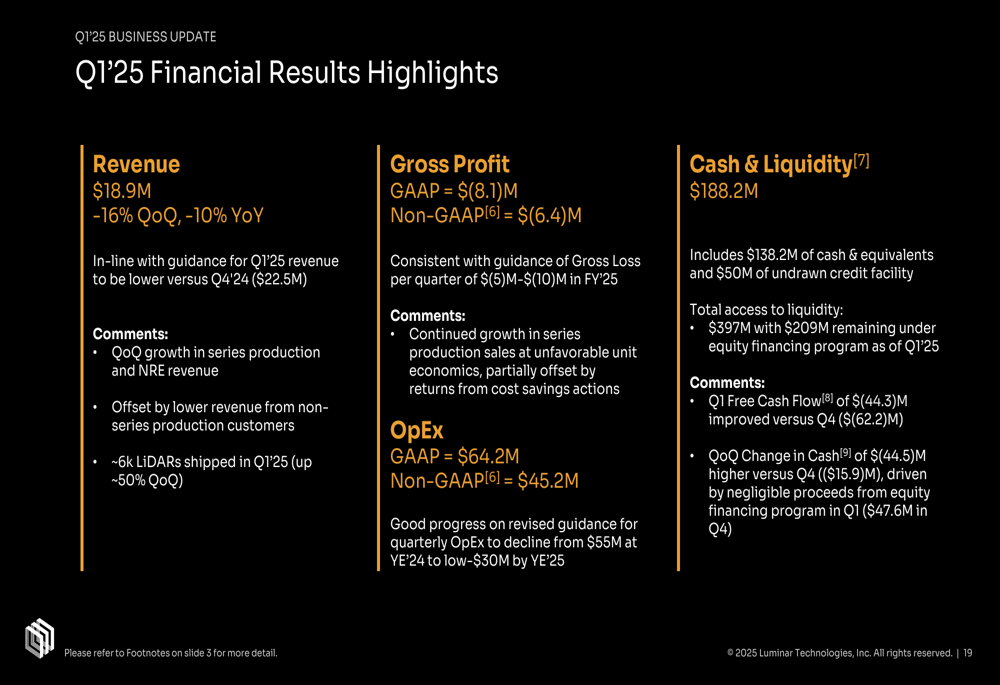

Luminar’s Q1 2025 financial results revealed mixed performance. Revenue declined to $18.9 million, representing a 16% decrease quarter-over-quarter and a 10% drop year-over-year. Despite this revenue decline, the company reported shipping approximately 6,000 LiDARs in Q1, a 50% increase from the previous quarter.

The detailed financial results show continued losses but improving cost structure:

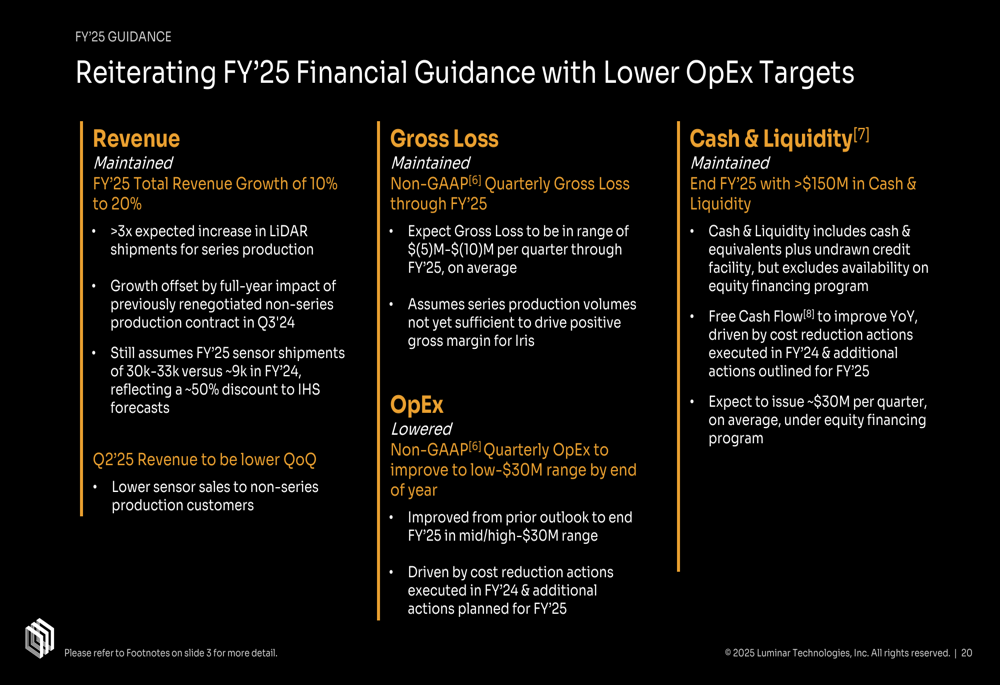

For the full year 2025, Luminar maintained its revenue growth guidance of 10-20%, with expected sensor shipments of 30,000-33,000 units compared to approximately 9,000 in FY 2024. The company also lowered its non-GAAP quarterly operating expense target:

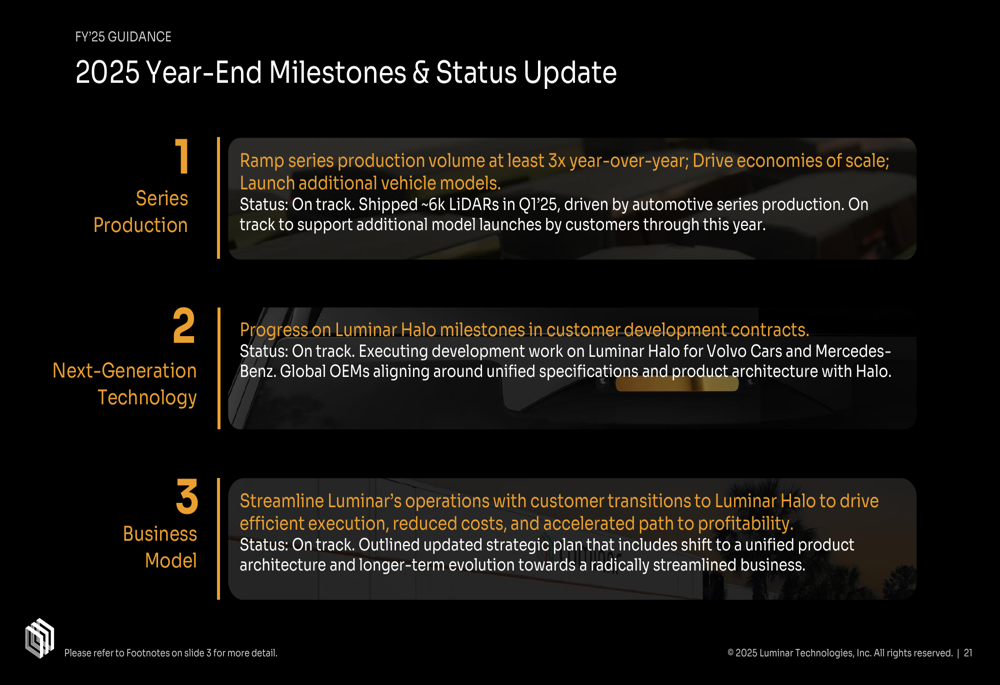

The company also provided an update on its 2025 year-end milestones:

Balance Sheet Management

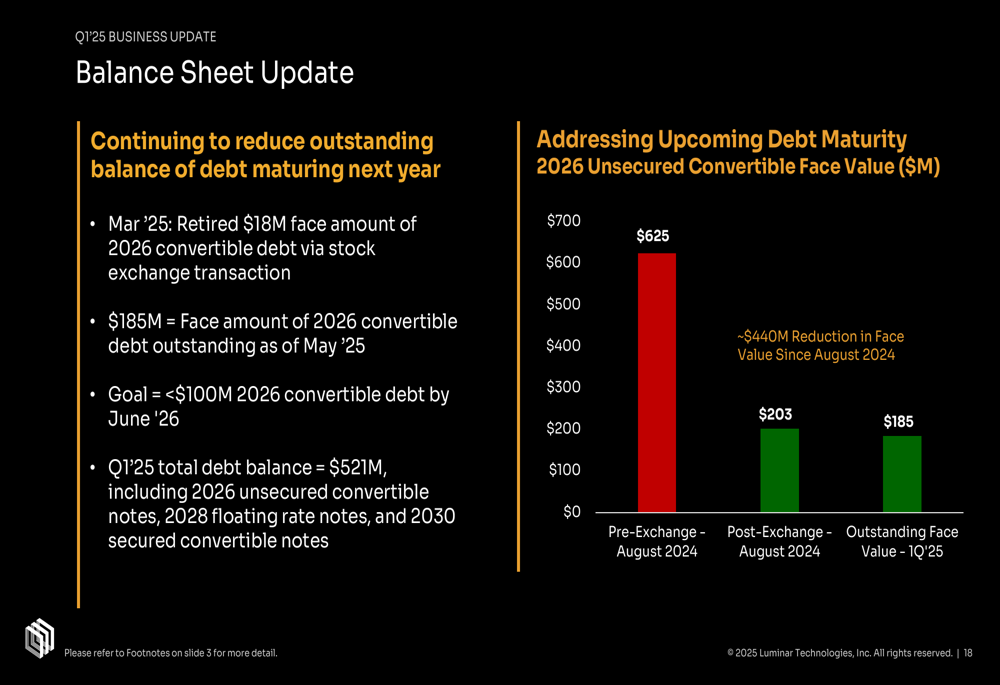

A significant portion of the presentation focused on Luminar’s efforts to strengthen its balance sheet, particularly by reducing its outstanding convertible debt maturing in 2026.

The following chart illustrates the company’s progress in debt reduction:

As of Q1 2025, Luminar reported total cash and liquidity of $188.2 million, including $138.2 million in cash and equivalents plus a $50 million undrawn credit facility. The company also has access to an additional $209 million through its equity financing program.

Forward-Looking Statements

Looking ahead, Luminar is betting heavily on its unified Halo platform to drive economies of scale and reduce development costs. The company expects to maintain a quarterly gross loss of $5-10 million throughout 2025, with series production volumes not yet sufficient to drive positive gross margins for its current Iris product.

The transition to the Halo platform represents a significant strategic bet, with the company streamlining operations and focusing exclusively on core technology while leveraging partnerships for manufacturing and industrialization. This approach aims to accelerate Luminar’s path to profitability, though the company did not provide a specific timeline for reaching break-even.

Luminar’s guidance for ending 2025 with more than $150 million in cash and liquidity suggests continued reliance on its equity financing program, with expected issuances of approximately $30 million per quarter on average.

While the company faces near-term revenue and profitability challenges, its strategic realignment around the unified Halo platform and partnerships with major global automakers provides a potential pathway to long-term growth and eventual profitability in the evolving automotive LiDAR market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.