Caesars Entertainment misses Q2 earnings expectations, shares edge lower

Introduction & Market Context

Magnera Corp (NYSE:MAGN) presented its Q1 2025 earnings results on February 6, 2025, showcasing the company’s performance in its first quarter as a newly formed entity following the spinoff and merger of Berry’s HHNF Business with Glatfelter . The presentation highlighted Magnera’s position as a global leader in nonwovens with a broad platform of solutions for the specialty materials industry.

The company’s stock closed at $15.17 on May 6, 2025, with premarket trading showing a slight decline of 0.73%. This represents a significant drop from the $20.31 price reported following the initial earnings announcement, suggesting investors may have reassessed the company’s prospects in the intervening months.

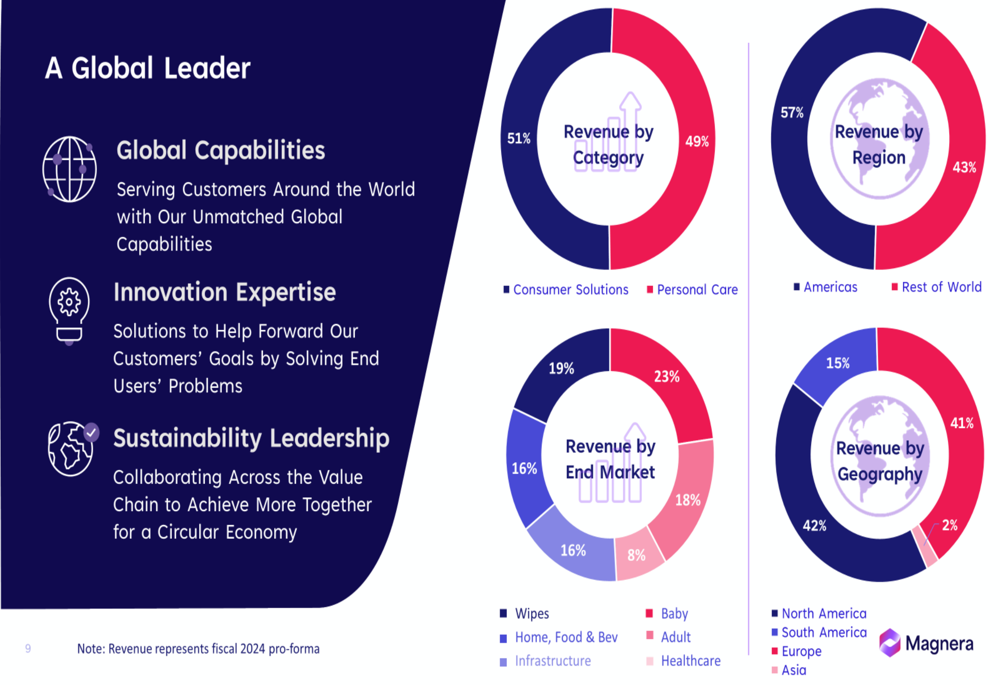

Magnera serves over 1,000 customers worldwide through its 46 global facilities and approximately 9,000 employees, with operations spanning more than 100 countries across North America, South America, Europe, and Asia.

Quarterly Performance Highlights

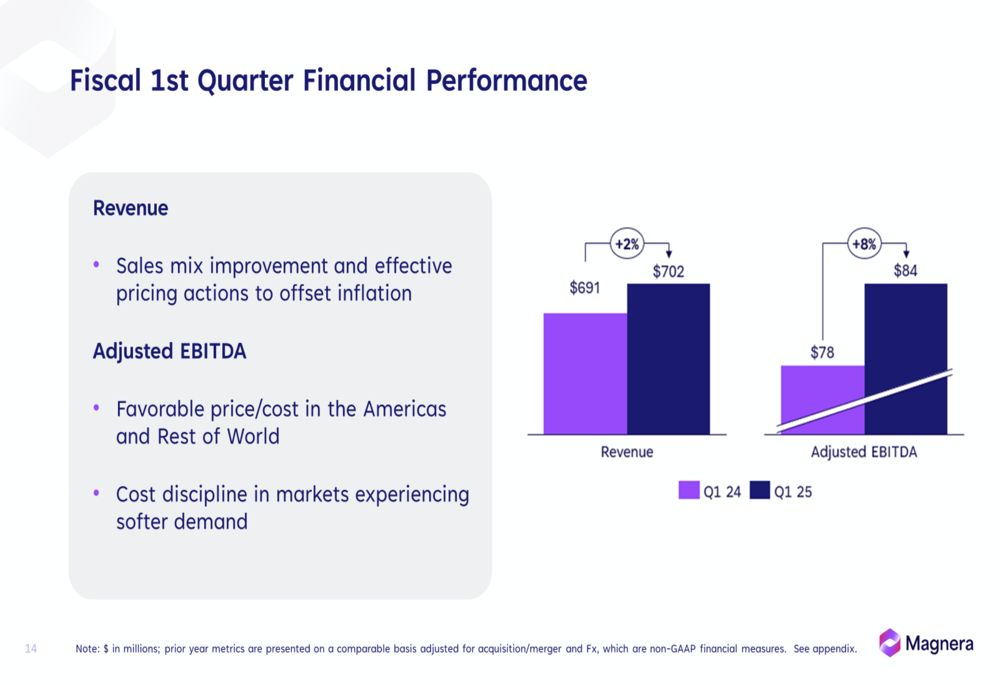

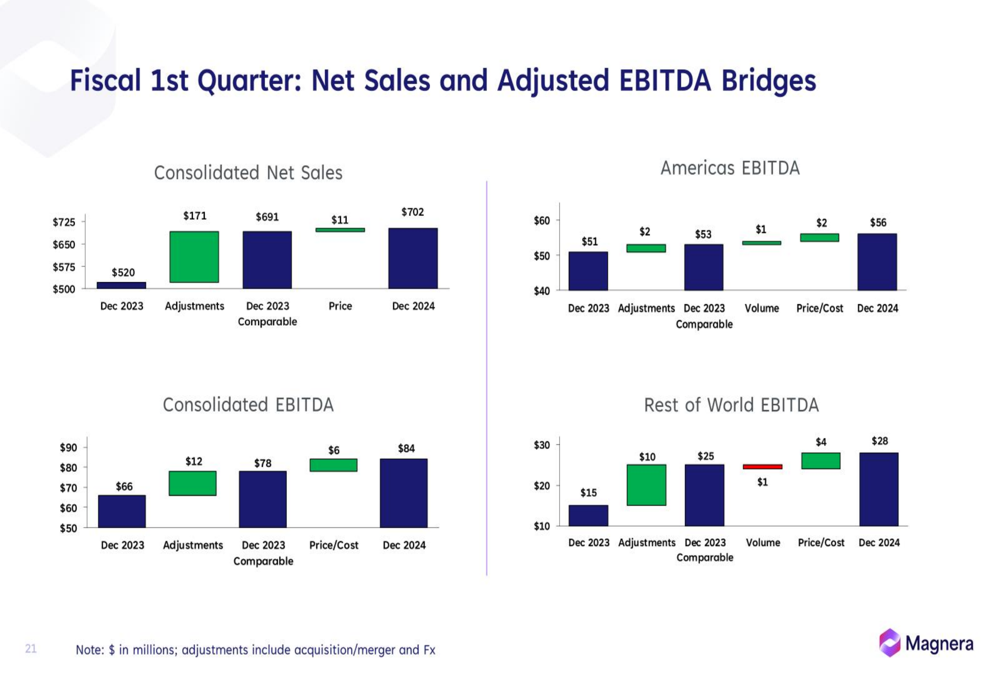

Magnera reported solid financial results for Q1 2025, with revenue increasing 2% year-over-year to $702 million, up from $691 million in Q1 2024. More impressively, adjusted EBITDA grew 8% to $84 million compared to $78 million in the prior year period, demonstrating improved operational efficiency.

The company attributed this performance to favorable price/cost dynamics in both the Americas and Rest of World segments, as well as effective cost discipline in markets experiencing softer demand. Sales mix improvements and pricing actions to offset inflation also contributed to the positive results.

As shown in the following chart detailing the fiscal first quarter financial performance:

The company’s revenue is well-balanced across categories, with Consumer Solutions accounting for 51% and Personal Care representing 49%. Geographically, North America (42%) and Europe (41%) make up the bulk of revenue, with South America (15%) and Asia (2%) comprising the remainder.

The diversification across end markets provides stability to Magnera’s business model, with Baby products representing the largest segment at 23%, followed by Wipes (19%), Adult products (18%), Infrastructure (16%), Home, Food & Beverage (16%), and Healthcare (8%).

This balanced portfolio is illustrated in the following breakdown:

Regional Performance Analysis

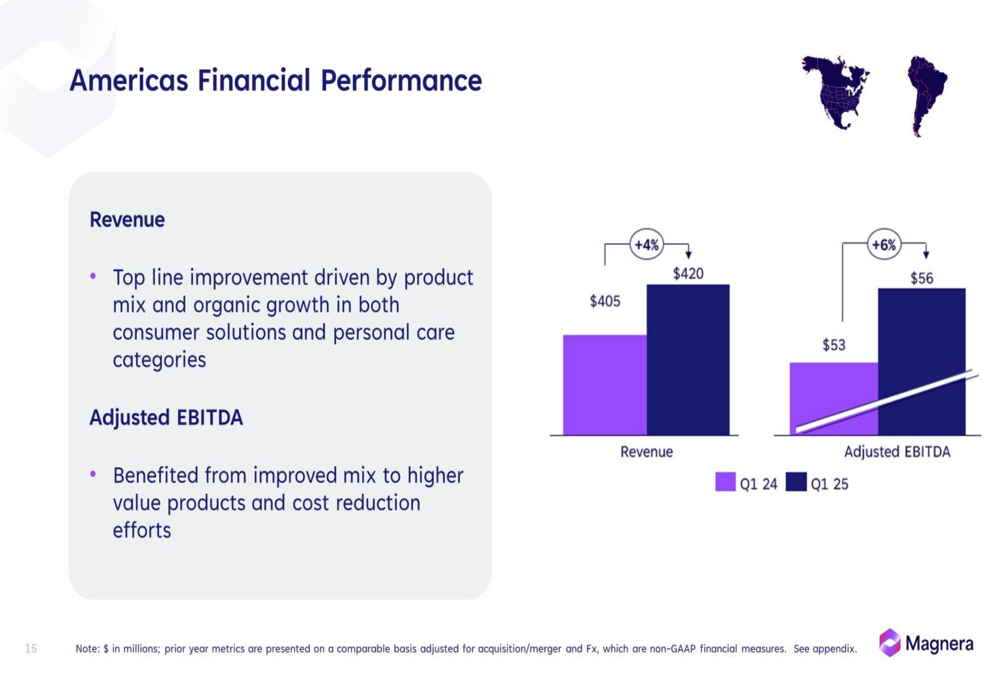

Magnera’s Americas segment delivered strong results, with revenue increasing 4% to $420 million compared to $405 million in Q1 2024. Adjusted EBITDA for the region grew 6% to $56 million from $53 million in the prior year period. The company attributed this growth to improved product mix and organic growth in both consumer solutions and personal care categories.

The Americas performance is detailed in the following chart:

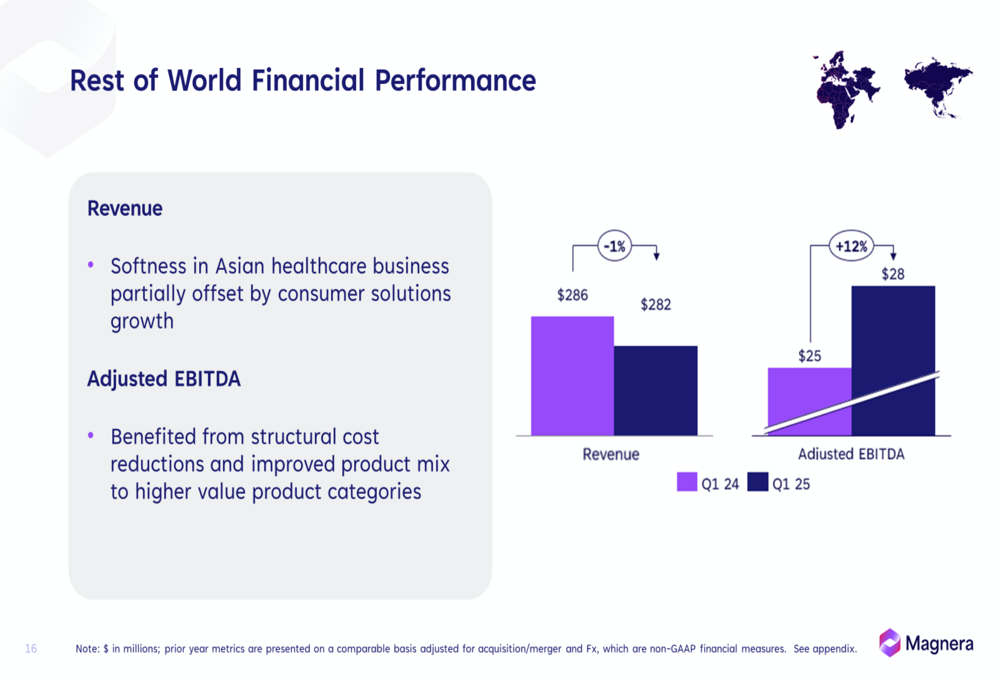

In contrast, the Rest of World segment experienced a slight revenue decline of 1%, with sales falling to $282 million from $286 million in Q1 2024. Despite this top-line pressure, adjusted EBITDA for the region increased by an impressive 12% to $28 million from $25 million, reflecting successful structural cost reductions and improved product mix toward higher-value categories.

The company noted softness in its Asian healthcare business, which was partially offset by growth in consumer solutions.

The Rest of World performance is illustrated in the following chart:

A detailed bridge analysis shows the key drivers behind the company’s financial performance, with price/cost improvements contributing $6 million to the overall EBITDA growth:

Strategic Initiatives & Outlook

Magnera outlined its strategic roadmap centered around three key pillars: Stabilize, Optimize, and Grow. The stabilization phase focuses on successful integration, exceptional customer service, and brand launch. The optimization phase emphasizes strategic transformation, operational excellence, and organizational effectiveness. The growth phase targets value creation, innovation excellence, and long-term shareholder returns.

The company highlighted its synergy program, noting that the design is complete with execution in progress. Management also emphasized strong organic growth in infrastructure and hard surface disinfecting categories, while acknowledging mixed results across different regions.

Magnera is well-positioned to capitalize on anticipated growth in key end markets between 2024-2027, with Infrastructure expected to grow at 8%, Wipes at 7%, Home, Food & Beverage at 5%, and Personal Care at 2-3%.

The company also emphasized its commitment to sustainability, highlighting initiatives such as 15 facilities with zero waste to landfill and 17 facilities with ISO 14001 environmental management certification.

Financial Guidance & Capital Allocation

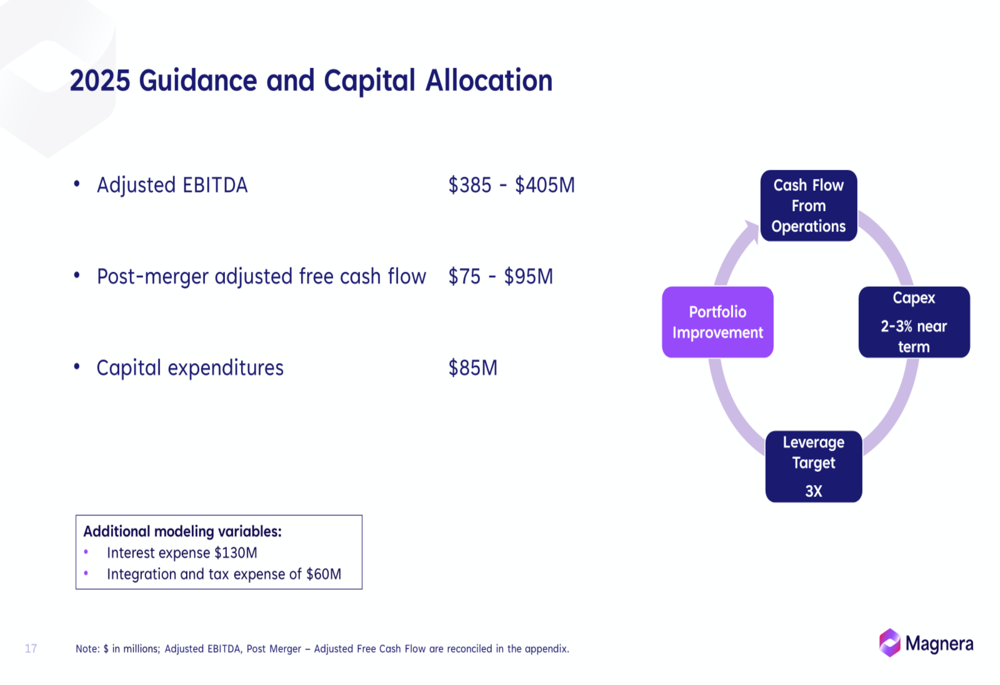

Looking ahead, Magnera provided financial guidance for fiscal year 2025, projecting adjusted EBITDA of $385-405 million and post-merger adjusted free cash flow of $75-95 million. The company plans capital expenditures of approximately $85 million, with interest expense expected to be around $130 million and integration and tax expenses of $60 million.

The company’s capital allocation strategy prioritizes portfolio improvement, capital expenditures (2-3% of revenue in the near term), and debt reduction, with a leverage target of 3x (down from the current level).

This guidance and capital allocation approach is outlined in the following chart:

Management emphasized that the company’s strong cash flow generation will support both strategic investments and debt reduction efforts. The focus on higher-value products and cost discipline is expected to continue driving margin improvement, even in challenging market environments.

As Magnera continues to integrate operations following the merger, investors will be closely watching the company’s progress toward achieving synergies and improving its financial position while navigating varying market conditions across its global footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.