Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Magnolia Oil & Gas Corporation (NYSE:MGY) released its first quarter 2025 earnings presentation on April 30, showing strong operational performance that allowed the company to raise production guidance while simultaneously reducing planned capital expenditures for the year. The stock closed down 3.66% at $20.53 following the release, despite the generally positive results.

Quarterly Performance Highlights

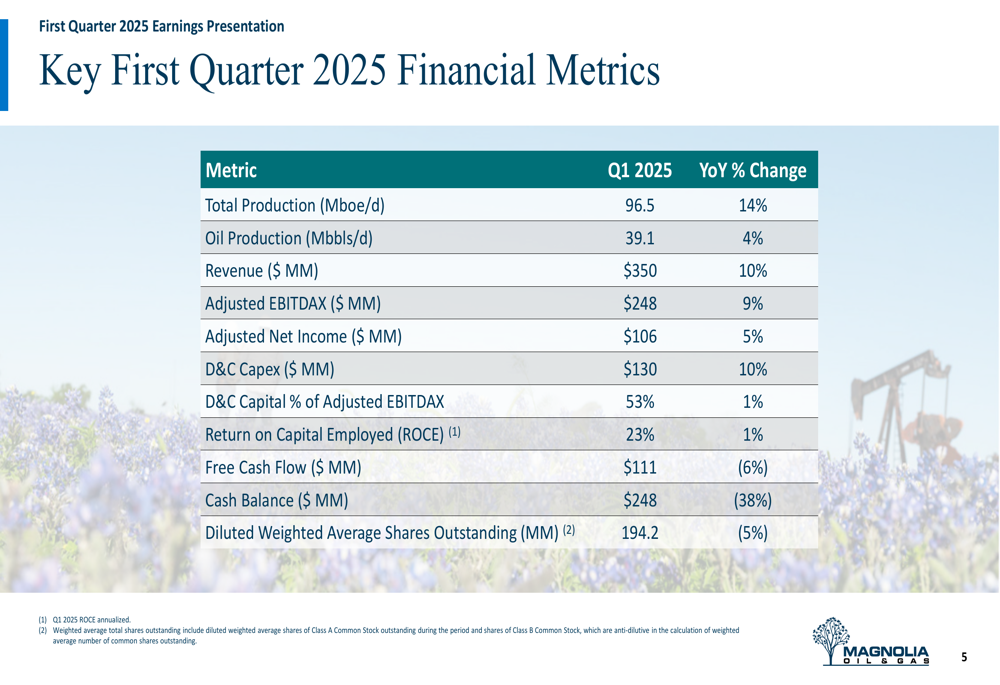

Magnolia reported total production of 96.5 thousand barrels of oil equivalent per day (Mboe/d) in Q1 2025, representing a 14% year-over-year increase and exceeding guidance. Oil production reached 39.1 thousand barrels per day (Mbbls/d), up 4% from the same period last year. The company’s Giddings field was the standout performer, with total production increasing 25% year-over-year and oil production growing 17%.

As shown in the following comprehensive financial metrics table, Magnolia maintained strong profitability despite relatively flat commodity prices:

The company generated $350 million in revenue, up 10% year-over-year, while adjusted EBITDAX reached $248 million, a 9% increase. Adjusted net income rose 5% to $106 million. Magnolia maintained its disciplined capital approach with drilling and completion (D&C) capital expenditures of $130 million, representing 53% of adjusted EBITDAX, in line with the company’s target of keeping capital spending below 55% of EBITDAX.

Detailed Financial Analysis

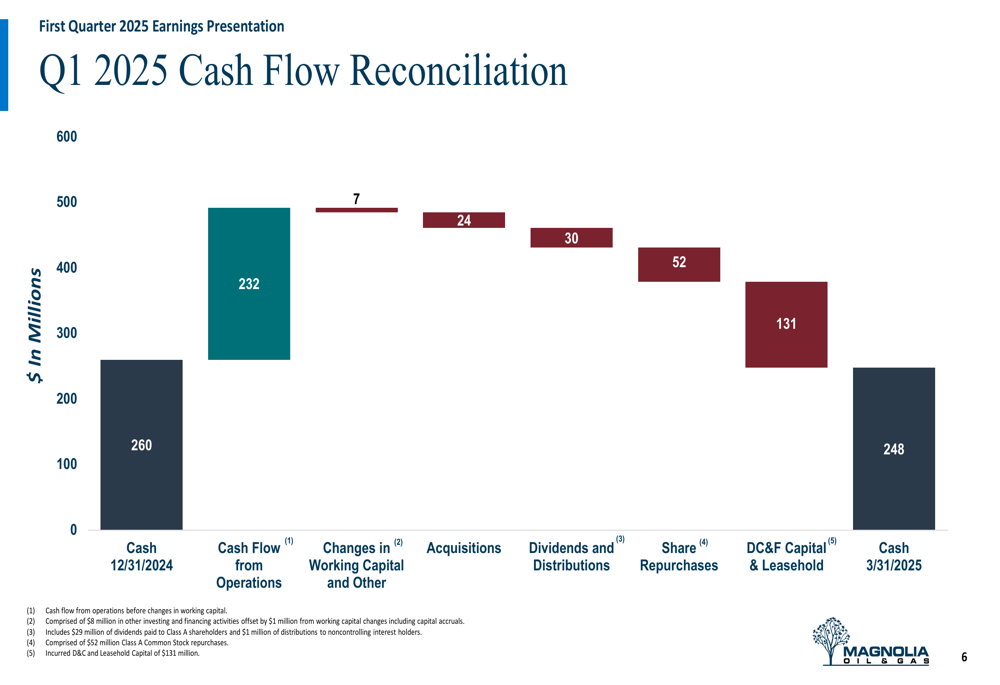

Magnolia’s financial strength was evident in its Q1 cash flow and balance sheet metrics. The company generated $111 million in free cash flow, slightly down 6% from the prior year, but still representing a significant portion of revenue.

The following cash flow reconciliation illustrates how Magnolia allocated its capital during the quarter:

The company ended the quarter with $248 million in cash, down from $260 million at year-end 2024. This reduction was primarily due to $52 million in share repurchases and $30 million in dividends, representing a total shareholder return of approximately $82 million or 74% of free cash flow.

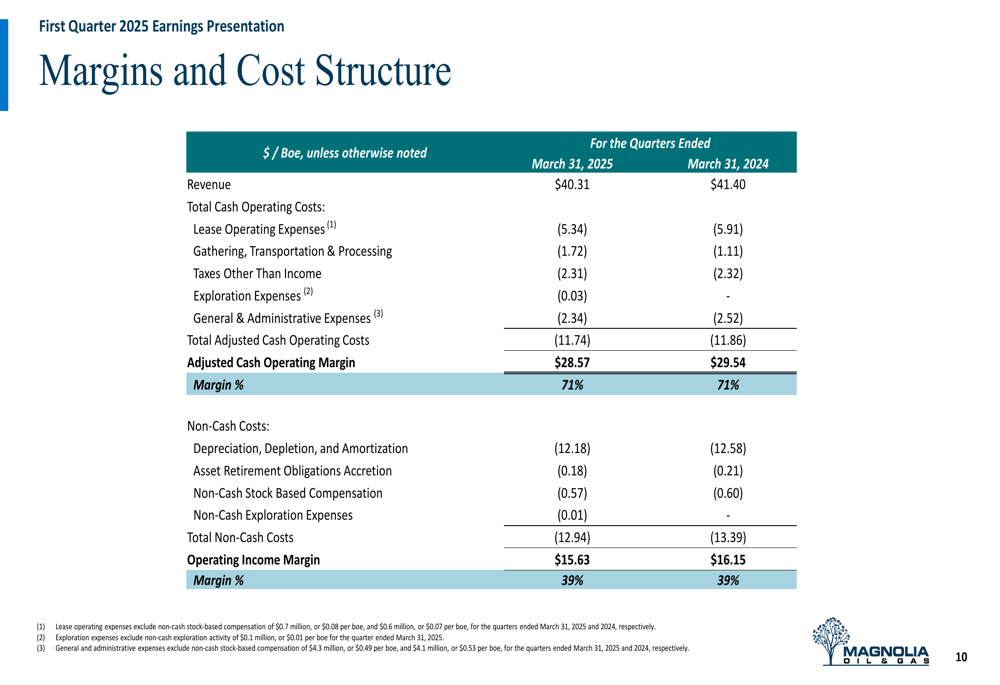

Magnolia’s margins remained robust, with an operating income margin of 39%, unchanged from the prior year period. The company’s adjusted cash operating margin was 71%, also flat year-over-year, demonstrating consistent operational efficiency despite industry cost pressures.

As shown in the following margin breakdown, the company maintained strong cost discipline:

Strategic Initiatives & Guidance

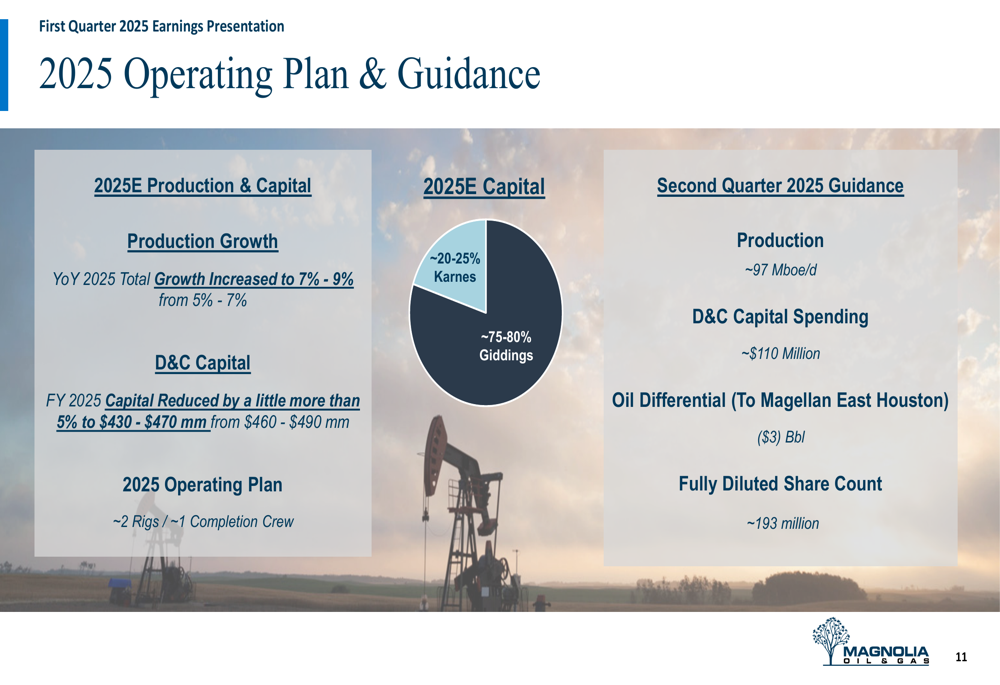

Based on stronger than expected well performance and productivity in the first quarter, Magnolia raised its full-year 2025 production growth guidance to 7-9% from the previous 5-7%. Simultaneously, the company reduced its capital expenditure guidance by more than 5% to $430-$470 million from the previous $460-$490 million.

The following slide details the company’s updated operating plan and guidance:

For the second quarter of 2025, Magnolia expects production of approximately 97 Mboe/d with D&C capital spending of around $110 million. The company plans to maintain its operating plan of approximately 2 rigs and 1 completion crew, with 75-80% of capital directed toward the high-growth Giddings area and 20-25% allocated to Karnes.

Capital Allocation & Shareholder Returns

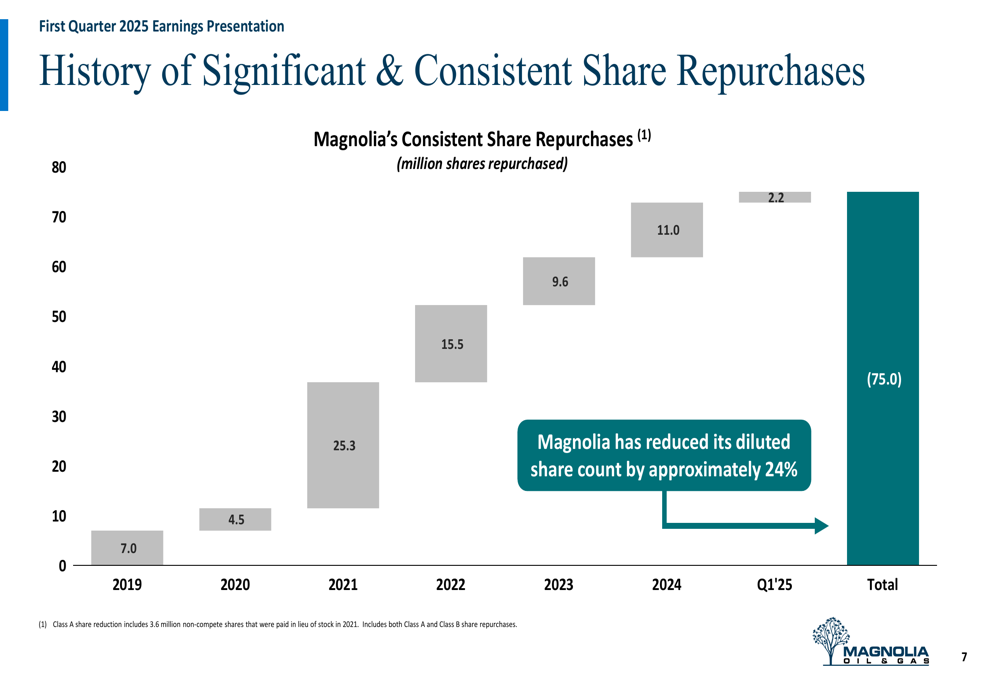

Magnolia continued its track record of significant shareholder returns through both dividends and share repurchases. The company has reduced its diluted share count by approximately 24% since inception through consistent repurchases.

The following chart illustrates Magnolia’s share repurchase history:

In Q1 2025, the company repurchased 2.2 million shares, continuing its commitment to reducing share count by at least 1% per quarter. This strategy has helped drive per-share value growth over time.

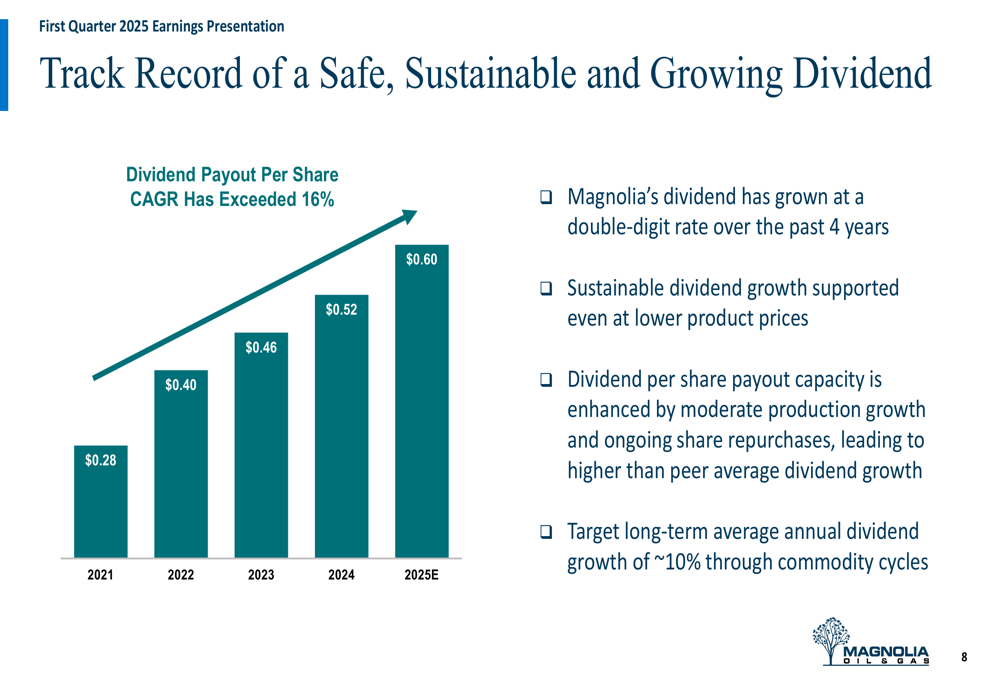

Magnolia has also maintained a growing dividend, with the 2025 expected dividend of $0.60 per share representing a compound annual growth rate exceeding 16% since 2021:

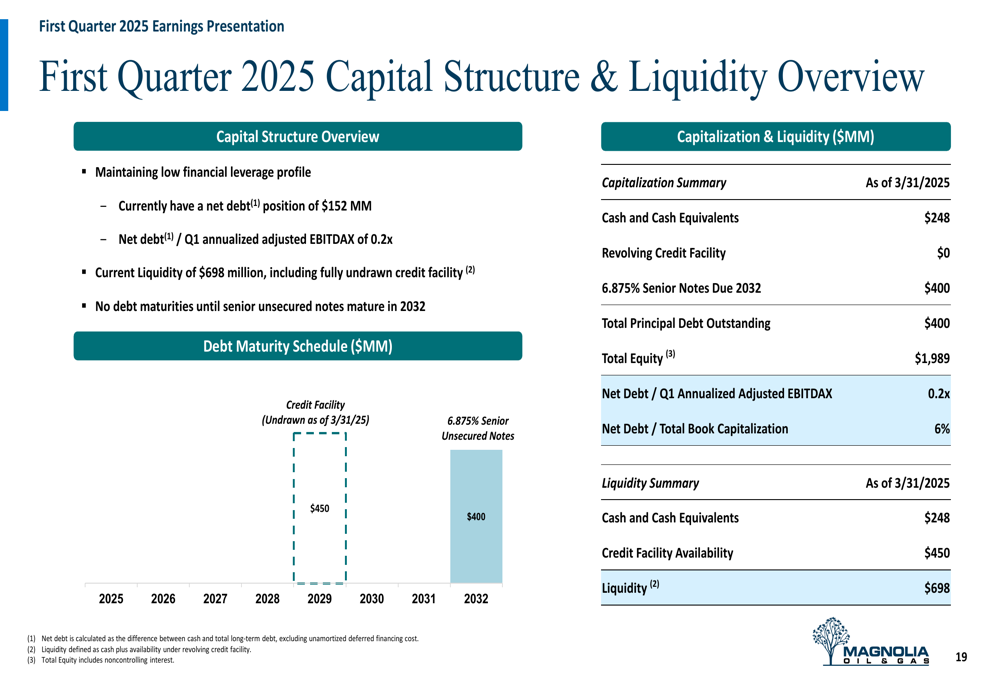

The company’s strong balance sheet provides flexibility for its capital return program. As of March 31, 2025, Magnolia reported total liquidity of $698 million, including $248 million in cash and a fully undrawn credit facility. The company’s net debt position was just $152 million, representing a minimal 0.2x ratio to annualized Q1 adjusted EBITDAX.

The following capital structure overview highlights Magnolia’s conservative financial approach:

Business Model & Investment Thesis

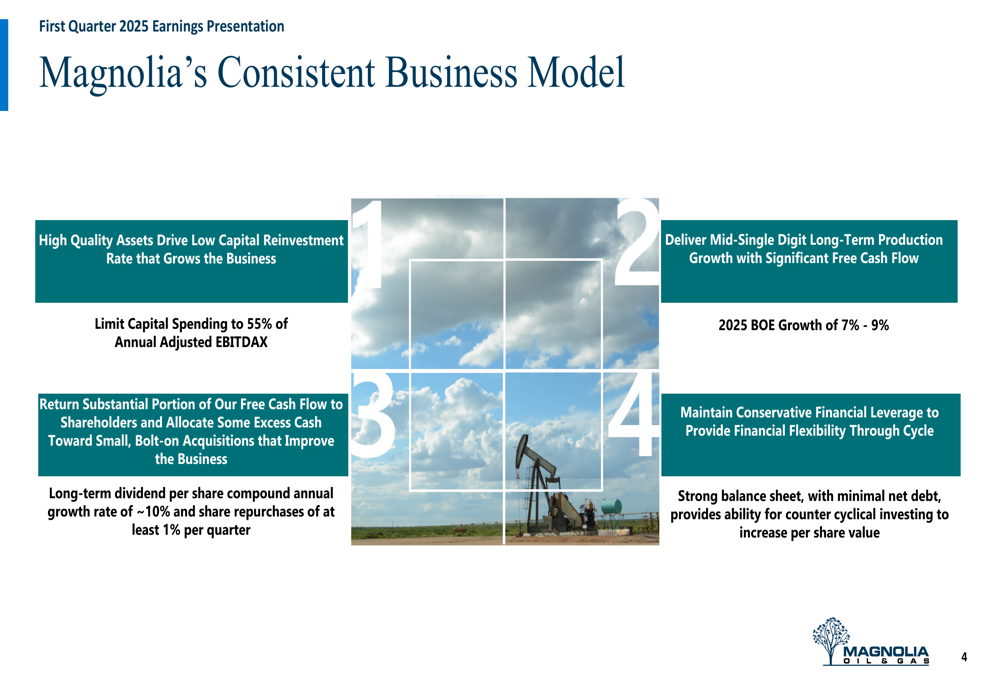

Magnolia continues to emphasize its differentiated business model focused on disciplined capital allocation, moderate production growth, and significant shareholder returns. The company limits capital spending to 55% of annual adjusted EBITDAX while targeting mid-single-digit production growth and substantial free cash flow.

As illustrated in the following business model framework:

This approach has allowed Magnolia to maintain a strong return on capital employed (ROCE) of 23% in Q1 2025, slightly higher than the 22% achieved in the same period last year. The company’s focus on high-quality assets in the Giddings and Karnes areas of the Eagle Ford shale provides a foundation for sustainable growth with relatively low capital requirements.

Magnolia’s commitment to sustainability was also highlighted, with the company reporting an 86% reduction in flaring intensity and a 12% reduction in greenhouse gas intensity from 2019 to 2023. These environmental improvements, combined with the company’s strong financial performance, position Magnolia as a differentiated player in the U.S. exploration and production sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.