US stock futures edge lower after S&P 500 hits record high; PCE data in focus

Magnolia Oil & Gas Corp (NYSE:MGY) reported record production levels in its second quarter 2025 earnings presentation released on July 30, 2025. Despite achieving all-time high output, the company faced headwinds from lower commodity prices, with shares declining 2.85% in after-hours trading to $23.90 following the announcement.

Quarterly Performance Highlights

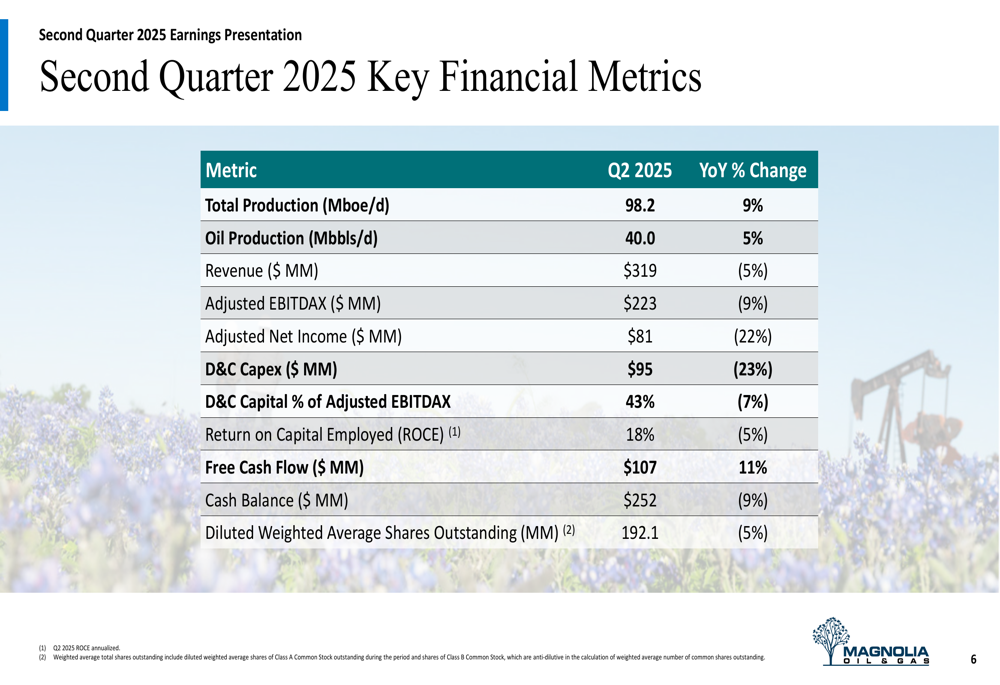

Magnolia achieved record total production of 98.2 thousand barrels of oil equivalent per day (Mboe/d) in Q2 2025, representing a 9% year-over-year increase. Oil production grew 5% year-over-year to 40.0 thousand barrels per day (Mbbls/d). However, revenue declined 5% to $319 million compared to the same period last year, reflecting the challenging commodity price environment.

The company reported adjusted EBITDAX of $223 million, down 9% year-over-year, while adjusted net income fell 22% to $81 million. Despite these challenges, Magnolia maintained its disciplined capital approach with drilling and completion capital of $95 million, representing 43% of adjusted EBITDAX.

As shown in the following summary of key financial metrics:

Free cash flow showed strength, increasing 11% year-over-year to $107 million, demonstrating the company’s ability to generate cash even in a more difficult pricing environment. The company ended the quarter with a cash balance of $252 million, down 9% from the previous year.

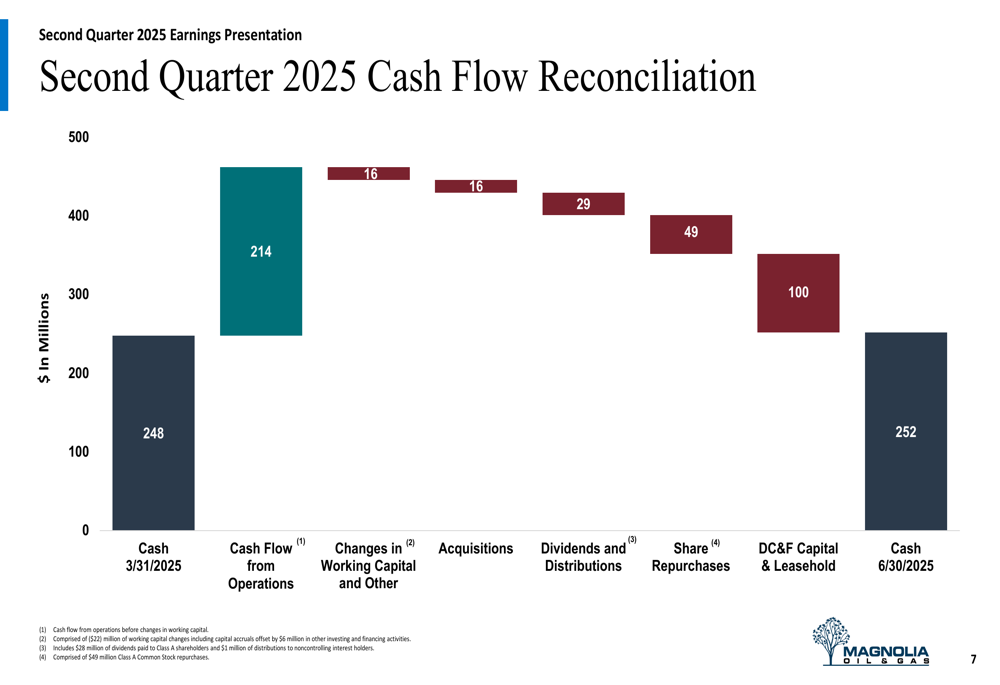

The following cash flow reconciliation illustrates how Magnolia allocated its capital during the quarter:

Strategic Initiatives

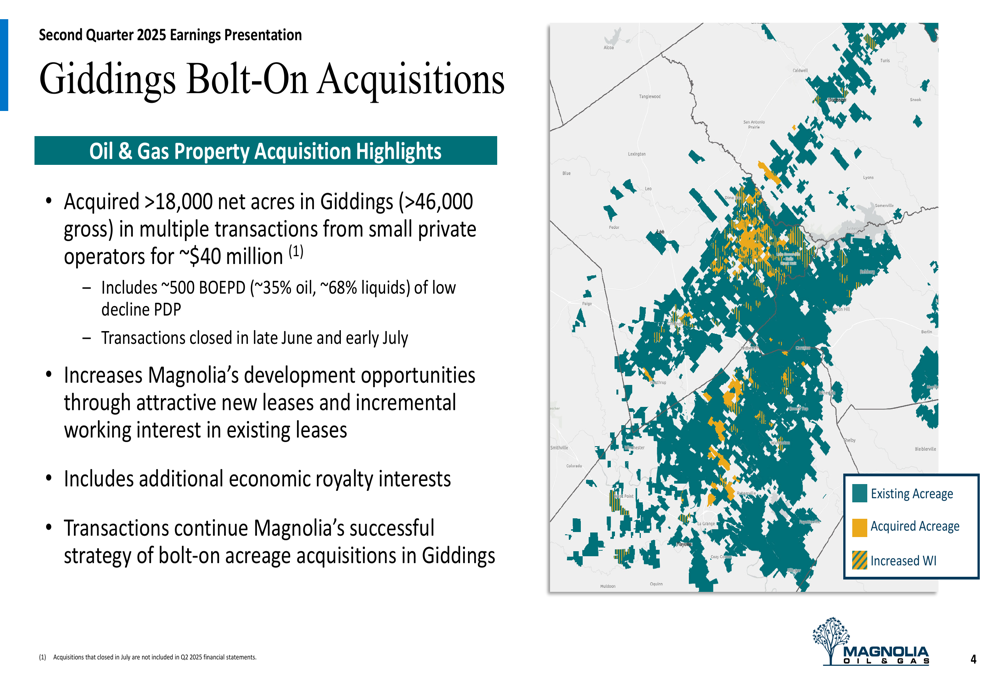

A significant development during the quarter was Magnolia’s completion of multiple bolt-on acquisitions, adding over 18,000 net acres and approximately 500 Boe/d of production (35% oil) for approximately $40 million. These acquisitions, which closed in late June and early July, strengthen the company’s position in the Giddings field.

The strategic importance of these acquisitions is illustrated in the following map:

"These transactions continue Magnolia’s successful strategy of bolt-on acreage acquisitions in Giddings," the company noted in its presentation. The acquisitions increase Magnolia’s development opportunities through attractive new leases and incremental working interest in existing leases.

Overall, the company has expanded its Giddings development area by 40,000 net acres or 20% to approximately 240,000 net acres, with about 75% coming from organic appraisal and 25% from bolt-on acquisitions.

Capital Allocation & Shareholder Returns

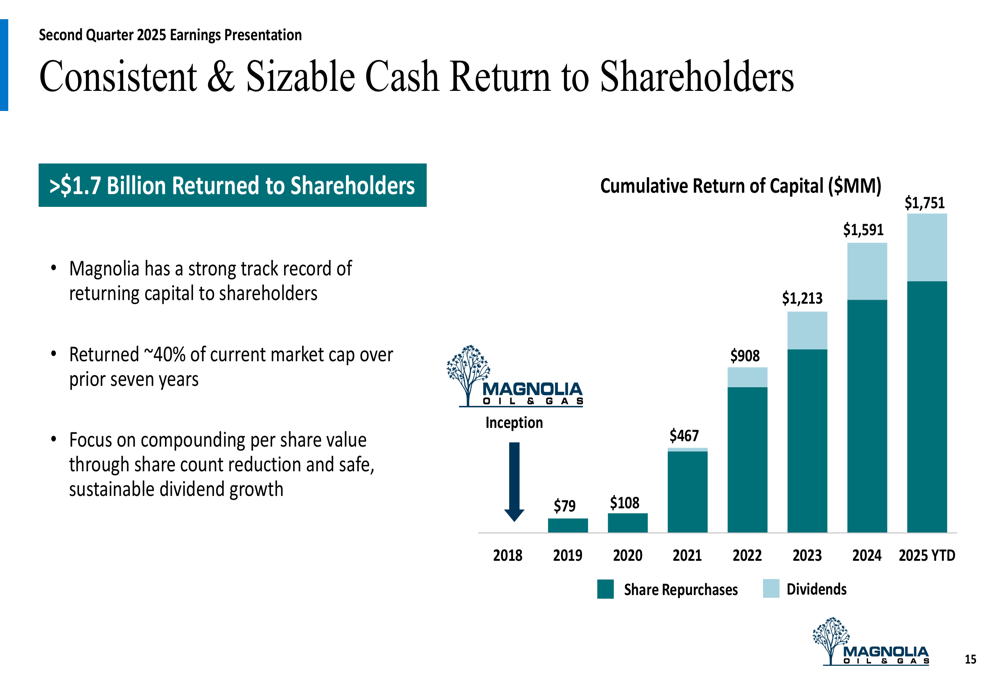

Magnolia continued its commitment to shareholder returns through dividends and share repurchases. The company has repurchased 77.2 million shares since 2019, reducing its diluted share count by approximately 25%. In 2025 year-to-date, the company has repurchased 4.4 million shares.

The company’s dividend growth has been impressive, with a compound annual growth rate exceeding 16% since 2021. Magnolia projects a 2025 dividend of $0.60 per share, up from $0.52 in 2024 and $0.28 in 2021.

The following chart shows Magnolia’s cumulative return of capital to shareholders:

"Magnolia has returned approximately 40% of current market cap over prior seven years," the company highlighted in its presentation. This focus on compounding per share value through share count reduction and dividend growth remains a cornerstone of Magnolia’s strategy.

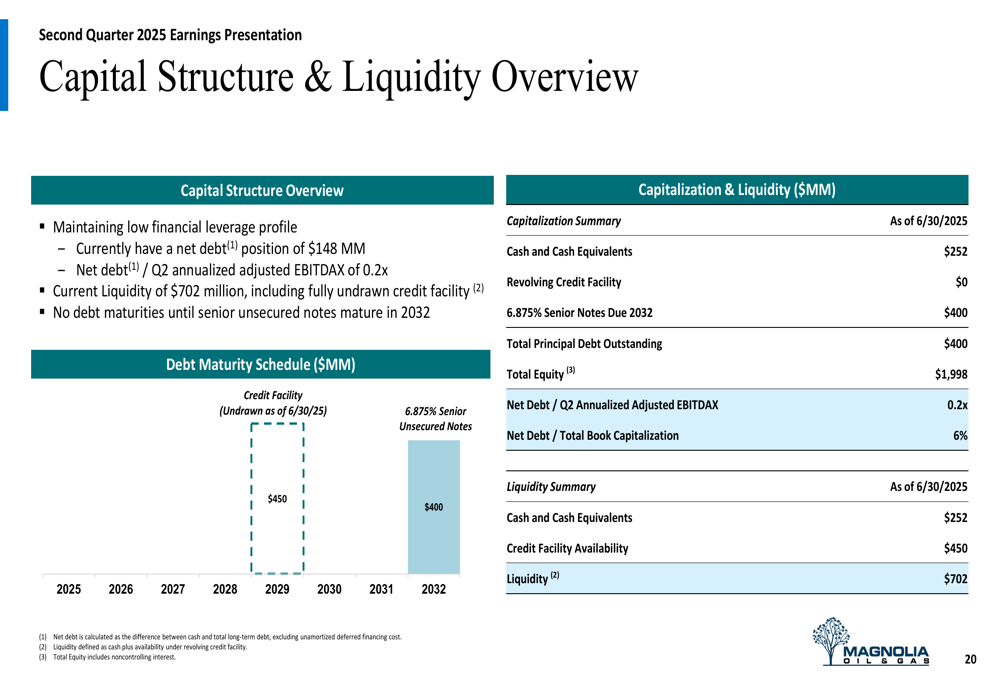

The company maintains a strong balance sheet with a net debt position of $148 million, representing just 0.2x Q2 annualized adjusted EBITDAX. This conservative financial approach provides flexibility for future opportunities.

As illustrated in the capital structure overview:

Forward-Looking Statements

Looking ahead, Magnolia raised its full-year 2025 production growth guidance to approximately 10%, up from its previous range of 7-9%, citing ongoing strong well performance. The company reiterated its drilling and completion capital guidance of $430-470 million for the full year.

For the third quarter of 2025, Magnolia expects production of approximately 99 Mboe/d and drilling and completion capital spending of approximately $115 million.

The company’s operating plan and guidance are summarized below:

Magnolia continues to focus on its core business model of maintaining a low capital reinvestment rate while delivering production growth and significant free cash flow. The company limits capital spending to 55% of annual adjusted EBITDAX, which allows for substantial shareholder returns while still growing the business.

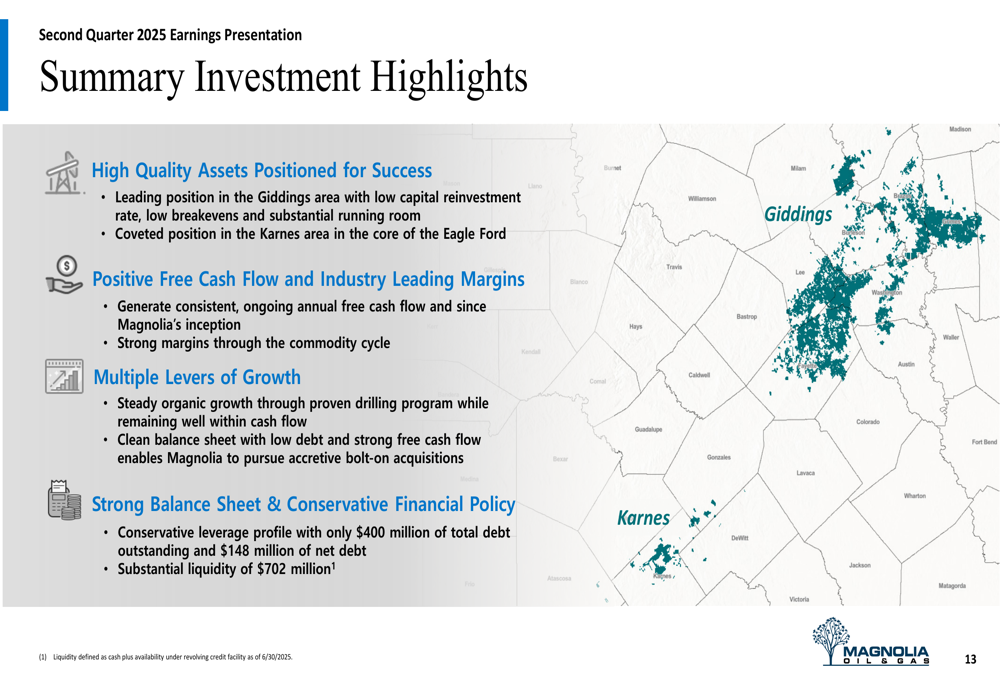

The company’s investment highlights emphasize its high-quality assets in the Giddings and Karnes areas, consistent free cash flow generation, and strong balance sheet:

While Magnolia’s Q2 results showed the impact of lower commodity prices on revenue and income, the company’s operational performance remained strong with record production levels. The raised production guidance for 2025 suggests confidence in continued operational execution despite market challenges. Investors will be watching closely to see if the company can maintain its balance of production growth, capital discipline, and shareholder returns in the current commodity price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.