Curb partners with Lyft to integrate ride requests into taxi platform

Magnolia Oil & Gas Corporation (NYSE:MGY) reported record production levels in its second quarter 2025 earnings presentation, helping to offset the impact of lower oil prices. The company highlighted strategic acquisitions and raised its full-year production guidance while maintaining its commitment to shareholder returns.

Introduction & Market Context

Magnolia Oil & Gas shares closed at $23.31 on October 14, down 0.99% for the day, as the market continues to digest the company’s second-quarter performance. The stock is trading well above its 52-week low of $19.09 but remains below its 52-week high of $29.02, reflecting mixed sentiment amid a challenging oil price environment.

The company’s Q2 2025 presentation, delivered on July 31, revealed how Magnolia is navigating the current market conditions through operational excellence and strategic expansion, particularly in its Giddings field assets.

Quarterly Performance Highlights

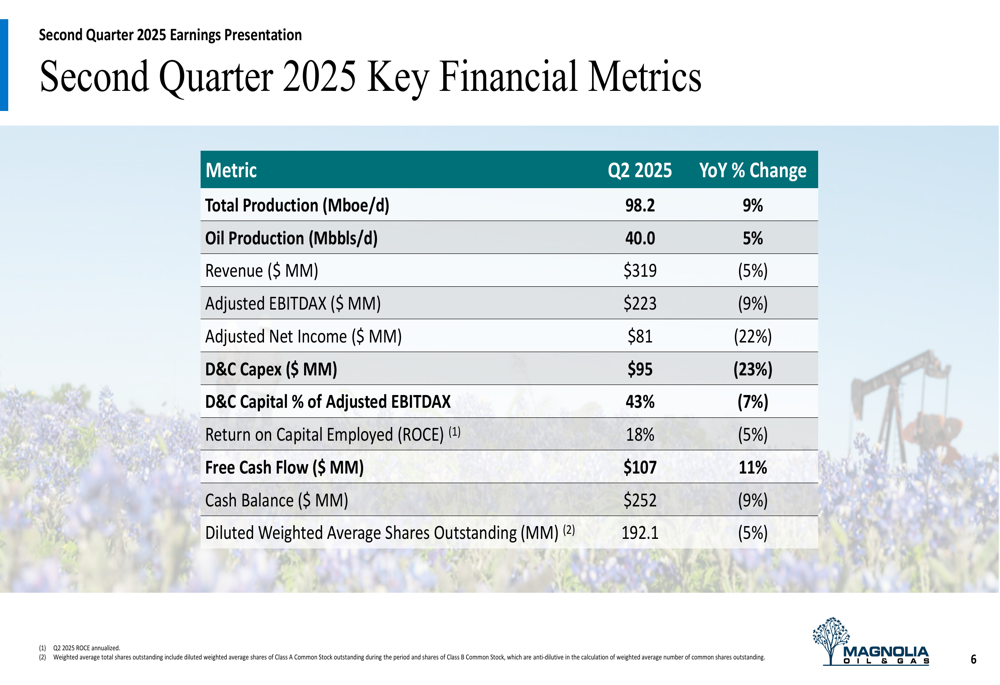

Magnolia achieved record total production of 98.2 thousand barrels of oil equivalent per day (Mboe/d) in the second quarter, representing a 9% increase year-over-year. Oil production grew by 5% to 40.0 thousand barrels per day (Mbbls/d), with the Giddings area showing particularly strong performance with 11% total production growth and 4% oil production growth compared to the same period last year.

As shown in the following comprehensive overview of key quarterly metrics:

Despite the production growth, revenue declined 5% year-over-year to $319 million, reflecting lower commodity prices. This impacted financial metrics, with adjusted EBITDAX decreasing 9% to $223 million and adjusted net income falling 22% to $81 million compared to Q2 2024.

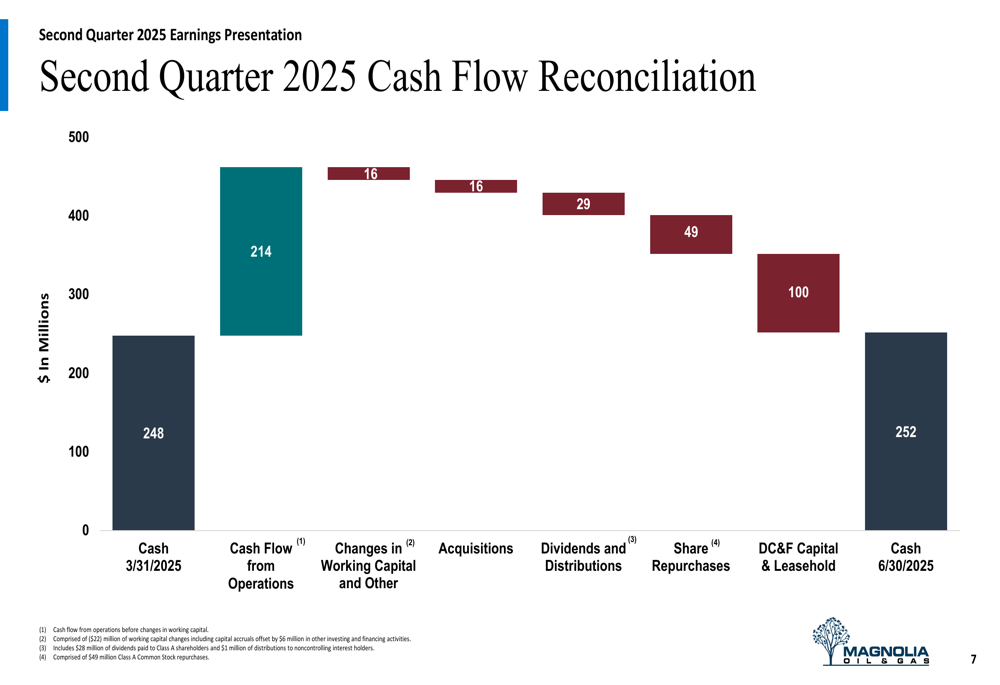

However, the company managed to generate $107 million in free cash flow, an 11% increase from the prior year, while maintaining a disciplined capital program with drilling and completion (D&C) capital expenditures of $95 million, 23% lower than the same period in 2024.

The following cash flow reconciliation illustrates how Magnolia managed its financial resources during the quarter:

Operating income margin stood at 34%, down from 40% in the same quarter last year, while return on capital employed (ROCE) was 18%, representing a 5% year-over-year decrease. These margin compressions reflect the challenging price environment, though Magnolia’s focus on operational efficiency helped mitigate some of the impact.

Strategic Initiatives

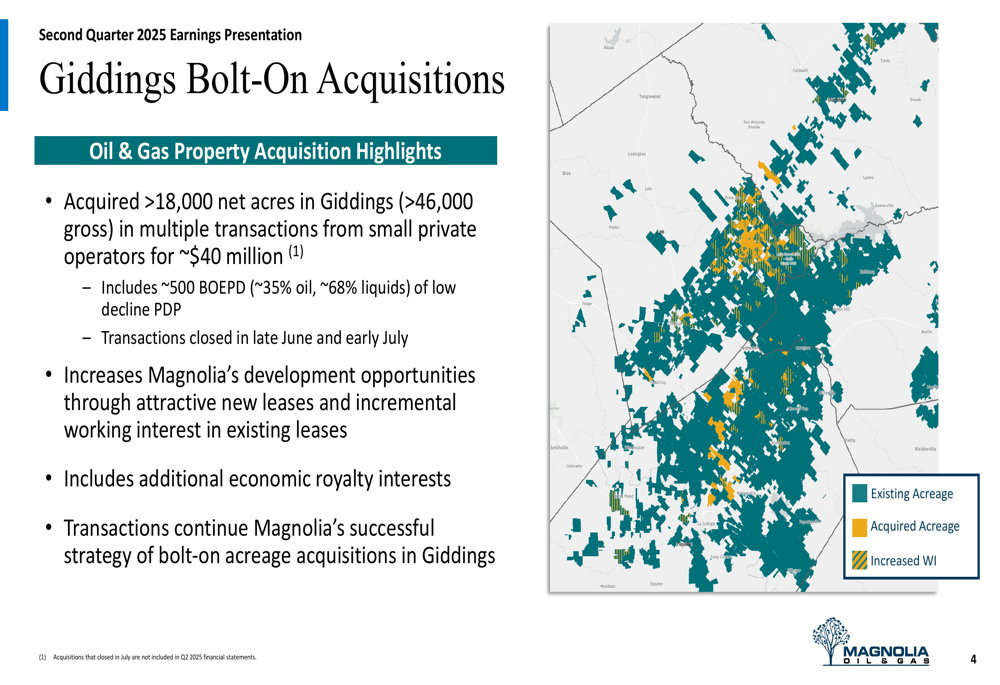

A key highlight of the quarter was Magnolia’s strategic expansion in the Giddings area, where the company completed multiple bolt-on acquisitions adding over 18,000 net acres and approximately 500 barrels of oil equivalent per day of production for about $40 million. These transactions closed in late June and early July 2025.

The acquisitions have increased Magnolia’s development area in Giddings by 20% to approximately 240,000 net acres, with about 75% coming from organic appraisal and 25% from the bolt-on acquisitions. This expansion provides additional development opportunities through new leases and incremental working interest in existing leases.

The following map illustrates Magnolia’s expanded footprint in the Giddings area:

During the earnings call, CEO Chris Stavros emphasized the company’s strategic focus: "The goal for us, drill the best wells with the least amount of capital as possible in order to generate the highest amount of free cash flow." Stavros also highlighted the success of the Giddings field, stating, "Giddings has far exceeded our expectations as far as what it’s been able to generate in terms of growth."

Capital Allocation & Shareholder Returns

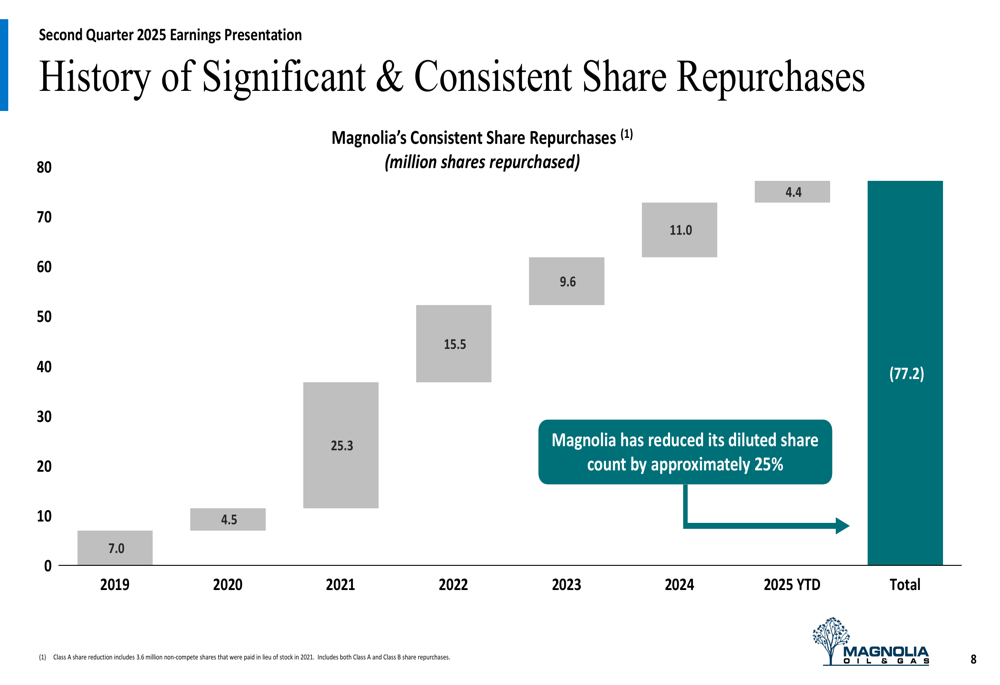

Magnolia continues to demonstrate its commitment to shareholder returns through both dividends and share repurchases. The company has maintained a consistent share repurchase program, having reduced its diluted share count by approximately 25% since inception. In Q2 2025 alone, the company repurchased $49 million worth of shares.

The following chart shows Magnolia’s history of share repurchases since 2019:

In addition to share repurchases, Magnolia has established a track record of growing its dividend, with a compound annual growth rate (CAGR) exceeding 16% since 2021. The company expects to pay $0.60 per share in dividends for 2025, up from $0.52 in 2024.

The company’s cumulative return of capital to shareholders has reached $1.75 billion since inception, representing approximately 40% of its current market capitalization. This consistent capital return strategy is supported by Magnolia’s strong balance sheet, with $252 million in cash and only $148 million in net debt as of June 30, 2025.

Forward-Looking Statements

Based on ongoing strong well performance, Magnolia has increased its full-year 2025 production growth guidance to approximately 10%, up from the previous range of 7-9%. For the third quarter of 2025, the company expects production of approximately 99 Mboe/d with D&C capital spending of around $115 million.

The following slide details Magnolia’s operating plan and guidance for the remainder of 2025:

Magnolia plans to maintain its disciplined approach with approximately two drilling rigs and one completion crew throughout 2025. Capital allocation will continue to favor the Giddings area, which is expected to receive 75-80% of the 2025 capital budget, with the remaining 20-25% directed to Karnes.

The company anticipates a 6-7% reduction in service costs by year-end, which could further enhance its financial performance. However, management acknowledged several potential challenges, including continued oil price volatility, potential fluctuations in service costs, and the impact of deferred well completions on production timing.

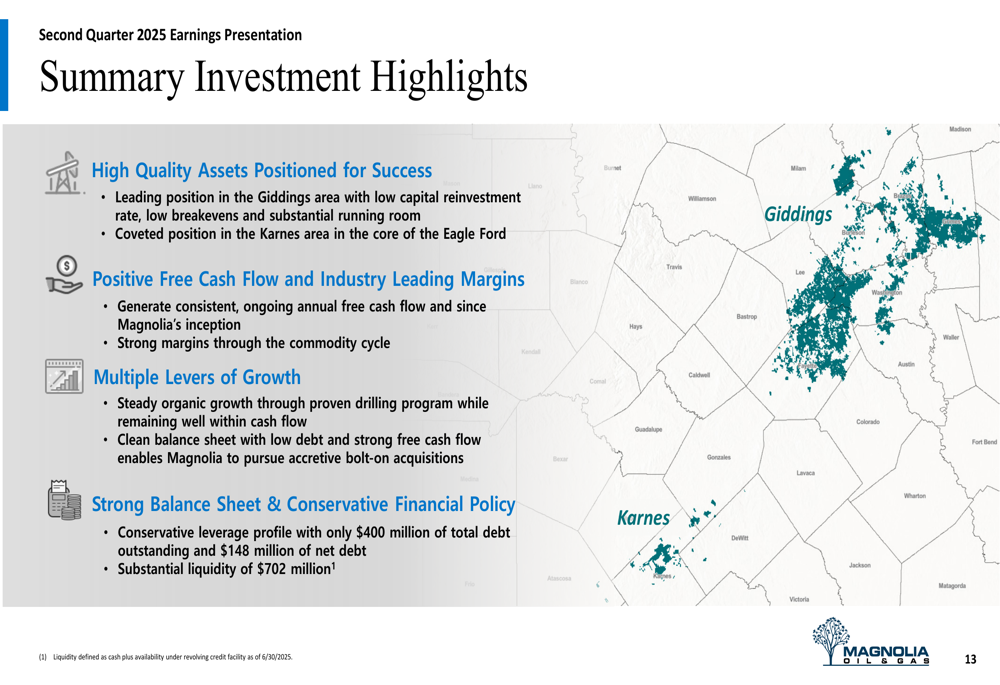

Magnolia summarized its investment highlights, emphasizing its high-quality assets, consistent free cash flow generation, multiple growth levers, and strong balance sheet:

With its record production levels, strategic expansion in Giddings, and commitment to shareholder returns, Magnolia appears well-positioned to navigate the current market environment while continuing to grow its asset base and per-share value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.