Vivek Ramaswamy buys Strive Inc (ASST) stock worth $1.25 million

Introduction & Market Context

Magnolia Oil & Gas Corporation (NYSE:MGY) released its third quarter 2025 earnings presentation on October 29, 2025, revealing record production levels despite missing earnings expectations. The company’s stock dipped 0.65% following the announcement, closing at $23, and has since declined further to trade at $22.72, down 1.2% as of October 30.

The oil and gas producer, focused on the Eagle Ford Shale and Austin Chalk formations in South Texas, delivered mixed results as it navigated commodity price challenges while maintaining its disciplined capital allocation strategy and commitment to shareholder returns.

Quarterly Performance Highlights

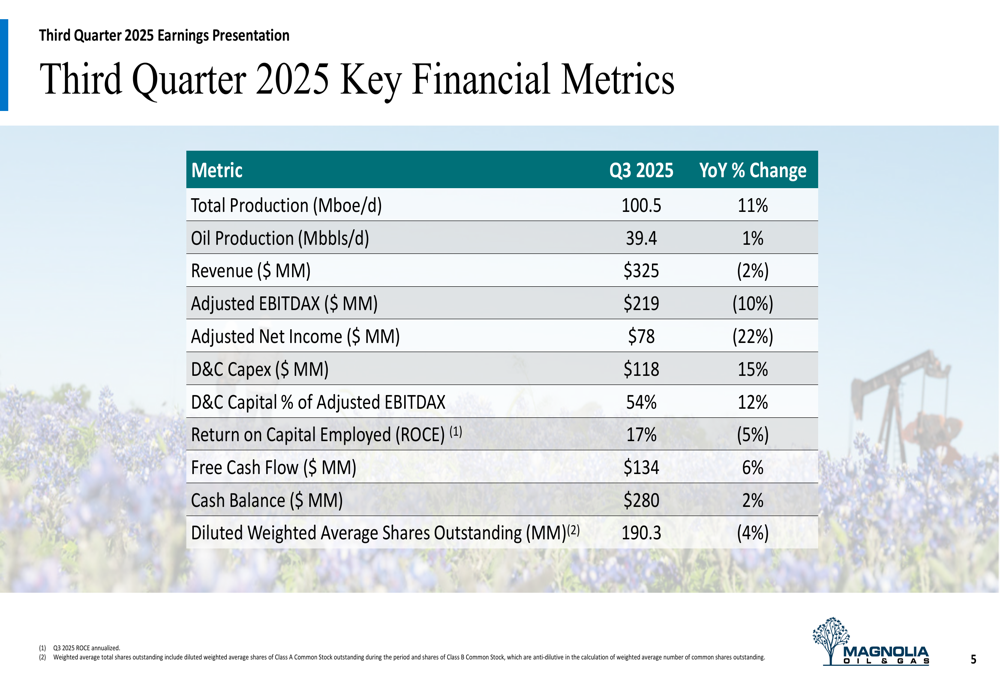

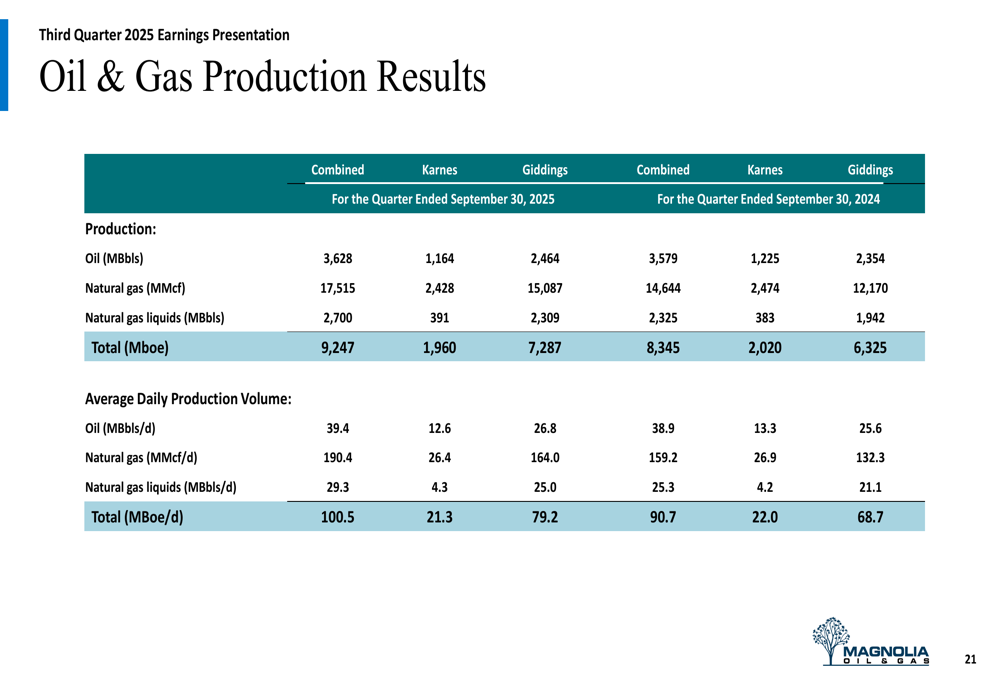

Magnolia achieved record total production of 100.5 thousand barrels of oil equivalent per day (Mboe/d) in the third quarter, representing an 11% increase year-over-year. Oil production reached 39.4 thousand barrels per day (Mbbls/d), a modest 1% improvement from the same period last year.

As shown in the following comprehensive financial metrics table from the presentation:

Despite the production growth, Magnolia reported revenue of $325 million, a 2% decrease from Q3 2024, reflecting lower realized commodity prices. Adjusted EBITDAX fell 10% year-over-year to $219 million, while adjusted net income declined 22% to $78 million. This translated to adjusted earnings per share of approximately $0.40, missing analysts’ expectations of $0.42 by 4.76%.

The company generated $134 million in free cash flow, a 6% improvement year-over-year, while drilling and completion capital expenditures increased 15% to $118 million. Magnolia maintained its capital discipline with a D&C capital reinvestment rate of 54% of adjusted EBITDAX.

Shareholder Returns & Capital Allocation

Consistent with its business model, Magnolia returned approximately $80 million to shareholders during the quarter, representing 60% of free cash flow. This included $51 million in share repurchases (2.15 million shares) and $29 million in dividends.

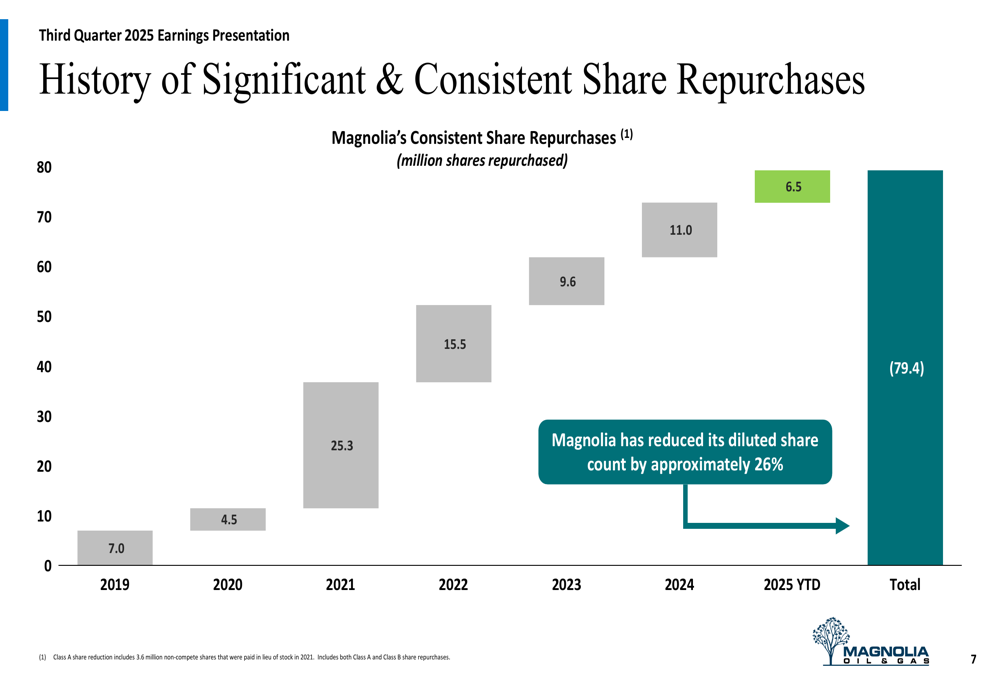

The company has demonstrated a consistent commitment to reducing its share count, as illustrated in this historical share repurchase chart:

Since 2019, Magnolia has repurchased 79.4 million shares, reducing its diluted share count by approximately 26%. This strategy has enhanced per-share metrics and supported dividend growth capacity.

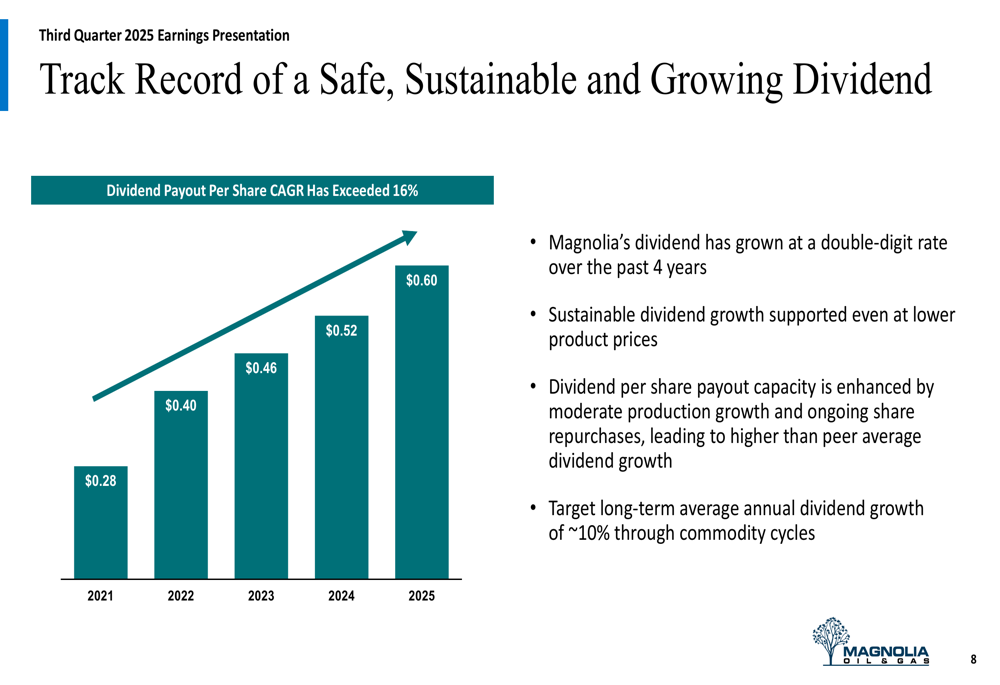

The dividend program has shown steady growth, with the per-share payout increasing from $0.28 in 2021 to $0.60 in 2025, representing a compound annual growth rate exceeding 16%:

Magnolia targets long-term average annual dividend growth of approximately 10% through commodity cycles, supported by its production growth and ongoing share repurchases.

Financial Position & Margins

The company maintained a strong balance sheet with $280 million in cash and only $120 million in net debt as of September 30, 2025. This represents a net debt to Q3 annualized adjusted EBITDAX ratio of just 0.1x, providing significant financial flexibility.

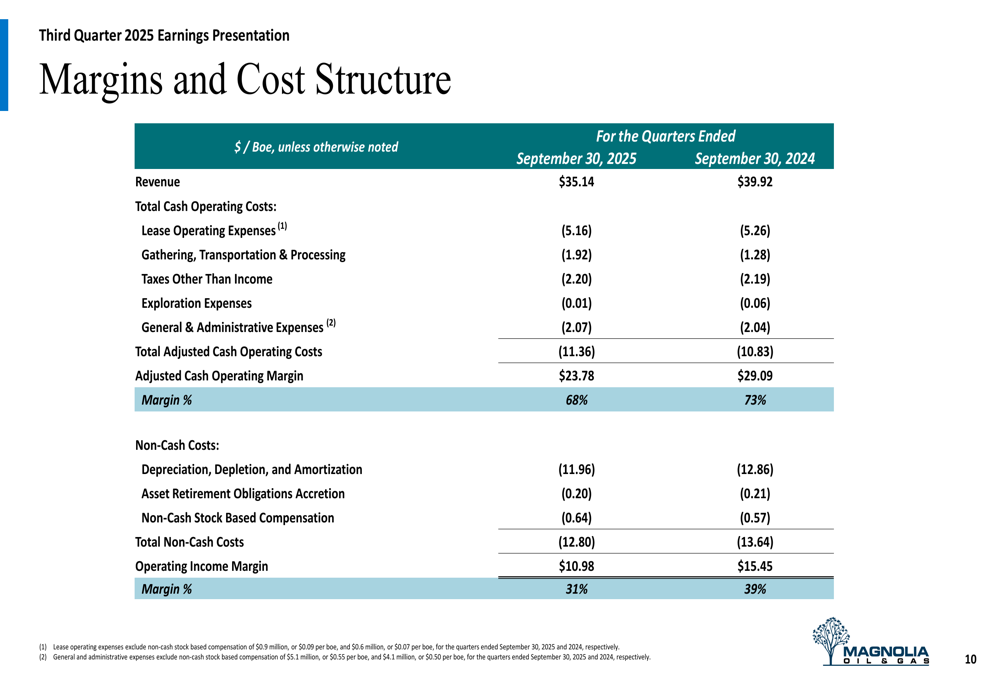

However, Magnolia’s margins have contracted year-over-year due to lower commodity prices and slightly higher operating costs, as detailed in this comprehensive cost structure breakdown:

Revenue per barrel of oil equivalent declined from $39.92 to $35.14, while total adjusted cash operating costs increased from $10.83 to $11.36 per barrel. This resulted in an operating income margin of 31%, down from 39% in the same quarter last year. The margin compression highlights the challenges faced by producers in the current commodity price environment.

Forward Guidance & Strategic Focus

Despite margin pressures, Magnolia raised its full-year 2025 production growth guidance to approximately 10%, up from its original projection of 5-7%, while expecting to spend about 5% less on drilling and completion capital than initially planned.

For the fourth quarter of 2025, the company anticipates:

- Production of approximately 101 Mboe/d

- D&C capital spending of approximately $110 million

- Oil price differential to Magellan East Houston of ($3) per barrel

- Fully diluted share count of approximately 189 million

The company’s operating plan and guidance are summarized in the following slide:

Magnolia plans to maintain its current operational cadence of approximately 2 drilling rigs and 1 completion crew, with capital allocation heavily weighted toward its Giddings asset (75-80%) versus Karnes (20-25%).

Executive Commentary & Conclusion

During the earnings call, CEO Christopher Stavros emphasized the company’s commitment to its differentiated business model, stating, "Since our founding more than seven years ago, Magnolia has consistently executed around the principles of its differentiated business model."

The company’s business approach remains focused on four key pillars, as illustrated in this strategic framework:

Magnolia’s consistent strategy involves maintaining a low capital reinvestment rate that still drives production growth, delivering free cash flow, returning capital to shareholders, and maintaining conservative financial leverage.

While the company faces challenges from commodity price volatility and margin compression, its strong balance sheet, disciplined capital allocation, and focus on shareholder returns position it to navigate market fluctuations. Investors will be watching closely to see if Magnolia can maintain its production momentum while managing costs in the current price environment.

The detailed production results by region demonstrate Magnolia’s operational success, particularly in the Giddings area which showed 15% year-over-year growth in total production:

With its record production levels, raised guidance, and continued focus on shareholder returns, Magnolia aims to enhance per-share value despite the challenging commodity price environment that contributed to its earnings miss in the third quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.