Diamyd Medical’s phase 3 diabetes trial passes final safety review

Introduction & Market Context

Mani Inc. (TYO:7730), a Japanese medical device manufacturer specializing in surgical, eyeless needle, and dental products, presented its financial results for fiscal year 2025 and forecasts for fiscal year 2026 on October 8, 2025. The company demonstrated resilience in the face of challenges, particularly a voluntary product recall in China, while continuing to execute on its global expansion strategy.

The presentation highlighted how Mani maintained growth momentum across most regions and segments despite temporary setbacks, with the company projecting a strong recovery in the coming fiscal year as operations in China normalize.

Quarterly Performance Highlights

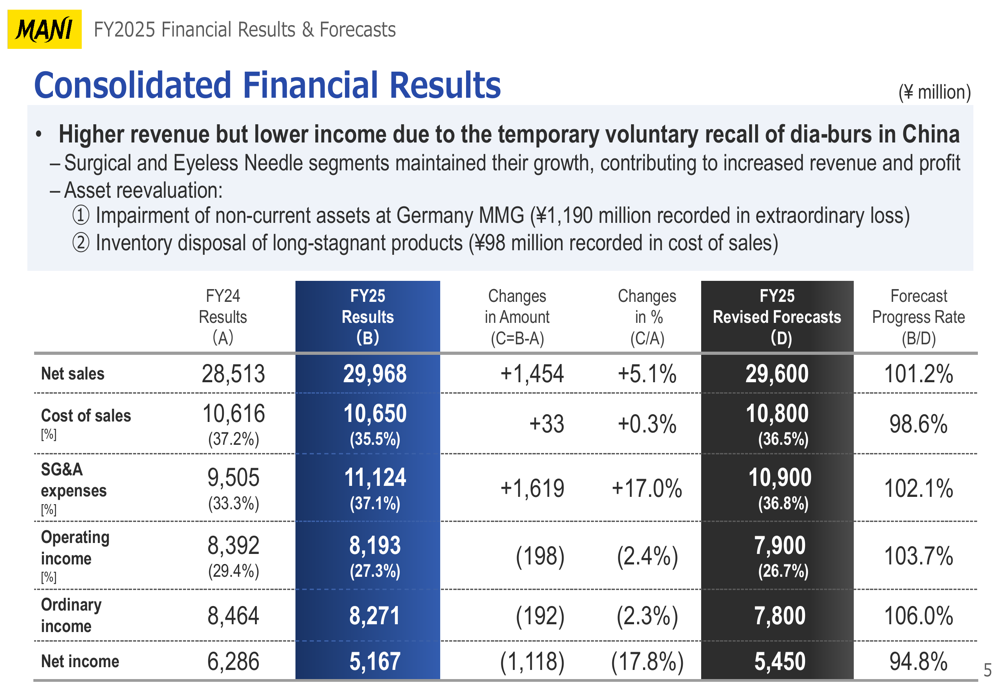

Mani reported consolidated net sales of ¥29,968 million for FY2025, representing a 5.1% increase year-over-year, while operating income declined slightly by 2.4% to ¥8,193 million. The company maintained a healthy operating margin of 27.3%, though this was down from 29.4% in the previous year.

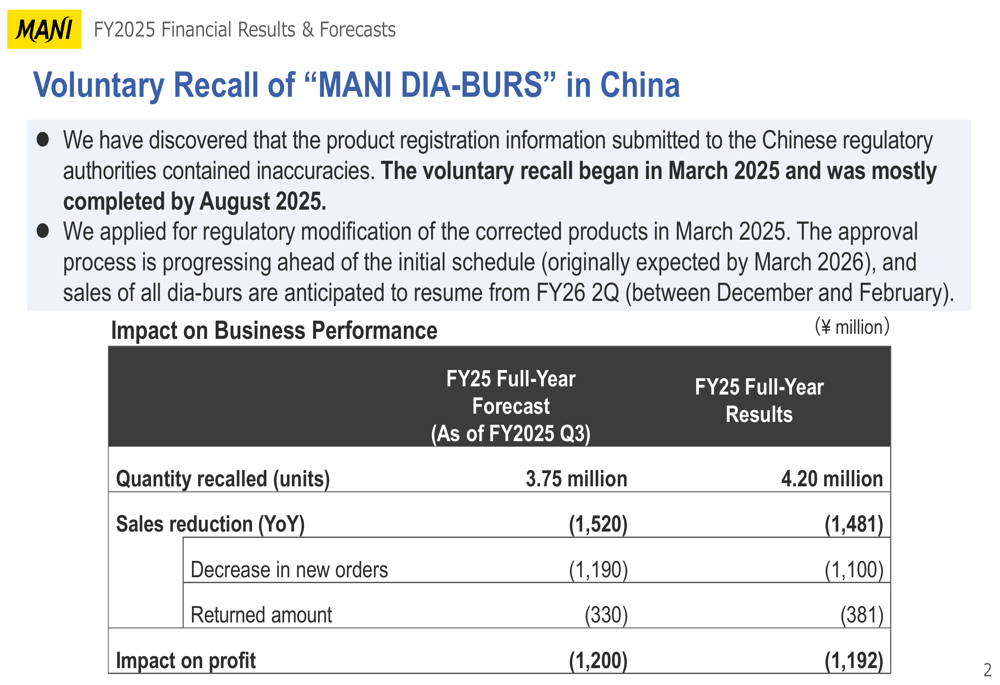

A significant factor impacting the company’s performance was the voluntary recall of "MANI DIA-BURS" products in China, which began in March 2025 due to inaccuracies in product registration information. This recall, which was mostly completed by August 2025, had a substantial impact on the company’s financial results.

As shown in the following detailed breakdown of the recall impact:

The recall resulted in a sales reduction of ¥1,481 million and a profit impact of ¥1,192 million. Despite these challenges, Mani expects to resume sales of these products in China from the second quarter of FY2026 (December-February), following regulatory modifications that were applied for in March 2025.

The company’s consolidated financial results show mixed performance across key metrics:

While revenue increased, net income declined significantly by 17.8% to ¥5,167 million, primarily due to the China recall and an impairment of non-current assets at MMG amounting to ¥1,190 million. The company’s cost of sales ratio improved from 37.2% to 35.5%, demonstrating enhanced operational efficiency despite challenges.

Detailed Financial Analysis

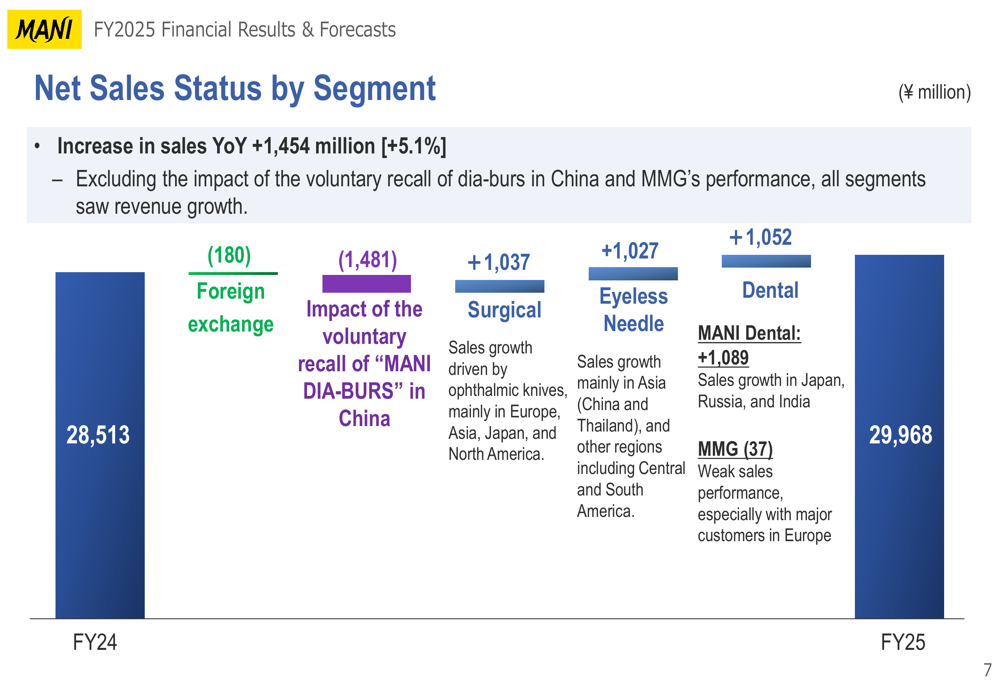

Mani’s performance varied significantly across its three business segments. The following chart illustrates the net sales status by segment:

The Surgical segment showed strong performance with sales growth of 13.8% year-over-year, reaching ¥9,274 million. This growth was primarily driven by ophthalmic knives, particularly in Europe, Asia, Japan, and North America. The segment maintained a robust operating margin of 33.2%.

Similarly, the Eyeless Needle segment performed well with a 9.4% increase in sales to ¥11,183 million, with growth mainly in Asia (China and Thailand) and Central and South America. However, its operating margin declined slightly from 37.9% to 35.8%.

The Dental segment faced significant challenges, with sales declining by 6.2% to ¥9,509 million, primarily due to the dia-burs recall in China. The segment’s operating income dropped substantially, with margin compression from 18.5% to 11.7%.

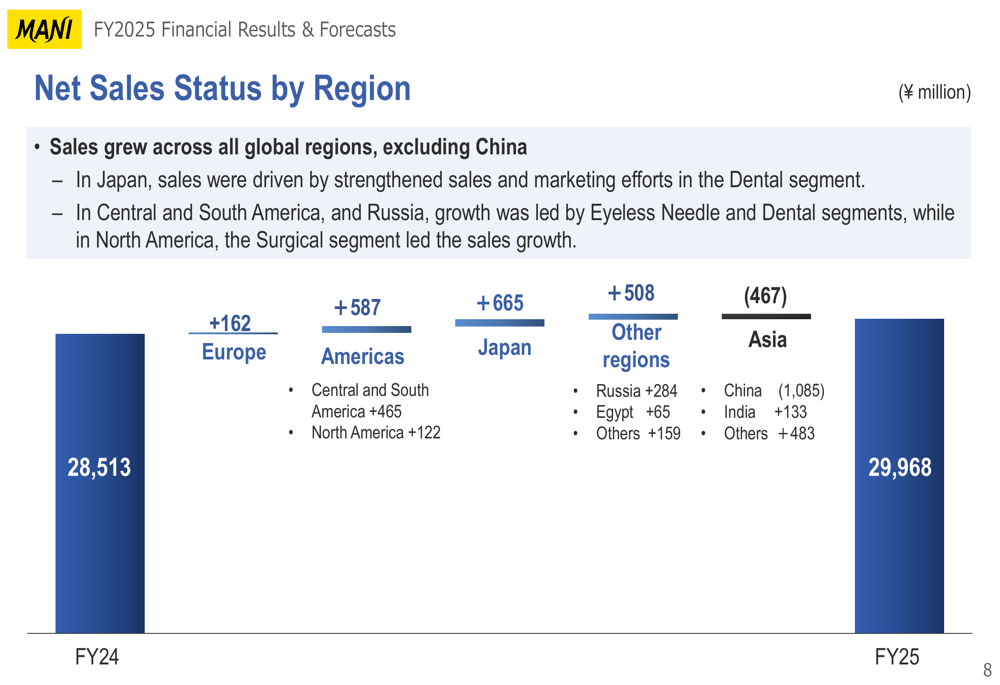

From a regional perspective, Mani achieved sales growth across all global regions except China:

The Americas region showed strong growth with a ¥587 million increase, primarily driven by Central and South America. Japan also performed well with a ¥665 million increase. The decline in Asia (¥467 million) was entirely attributable to China’s ¥1,085 million decrease, as other Asian markets showed positive growth.

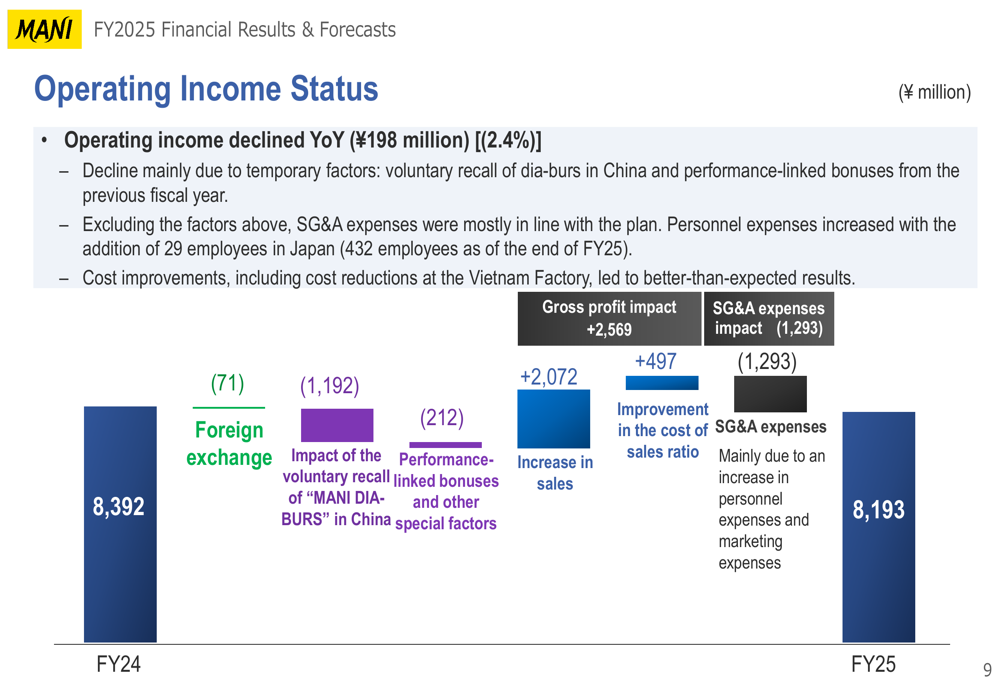

The company’s operating income was impacted by multiple factors as illustrated below:

While increased sales contributed ¥2,072 million to operating income and cost improvements added another ¥497 million, these gains were offset by the China recall impact (¥1,192 million) and increased SG&A expenses (¥1,293 million), primarily from higher personnel and marketing costs.

Strategic Initiatives

Mani highlighted that investments related to its Smart Factory have been largely completed in FY2025, with capital expenditure expected to decrease significantly in FY2026. The company’s cash flow turned slightly negative in FY2025 due to these investments, but this is expected to normalize in the coming year.

The company is implementing structural reforms at MMG, its dental subsidiary that has been underperforming, particularly with major European customers. These reforms aim to improve profitability and operational efficiency.

For the Dental segment, Mani is focusing on recovery from the voluntary recall in China and continuing expansion of its JIZAI product series. In the Surgical segment, key initiatives include strengthening the U.S. market position and expanding in China and Europe. The Eyeless Needle segment will focus on special needles and achieving fundamental reductions in manufacturing costs.

Forward-Looking Statements

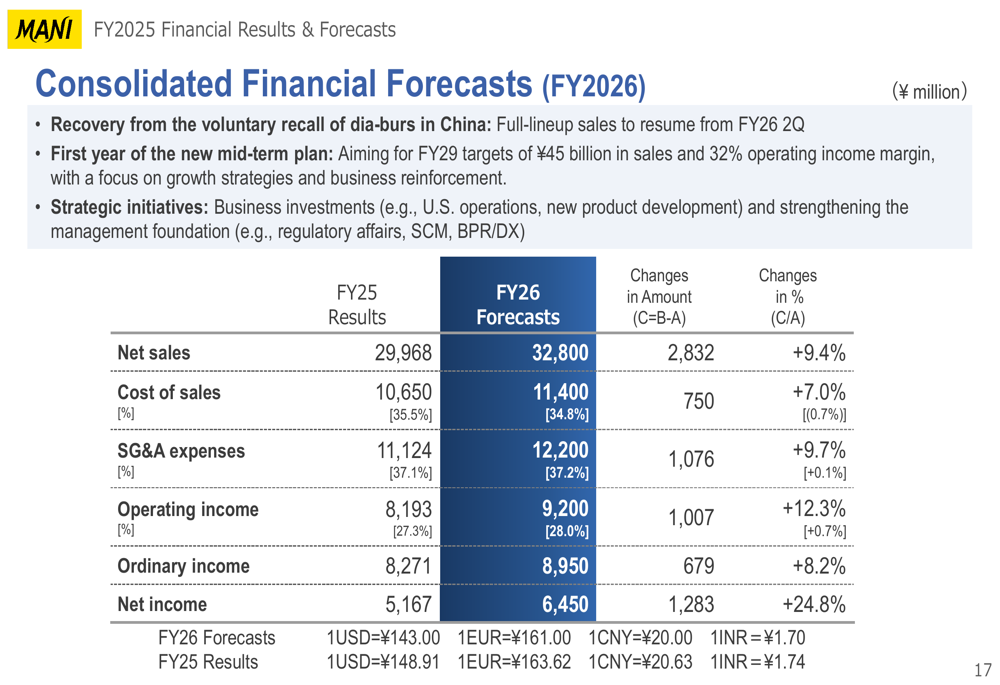

Mani’s outlook for FY2026 is optimistic, with projected recovery from the voluntary recall in China expected to drive growth:

The company forecasts consolidated net sales of ¥32,800 million for FY2026, representing a 9.4% increase from FY2025. Operating income is expected to grow by 12.3% to ¥9,200 million, with the operating margin improving to 28.0%. Net income is projected to increase significantly by 24.8% to ¥6,450 million.

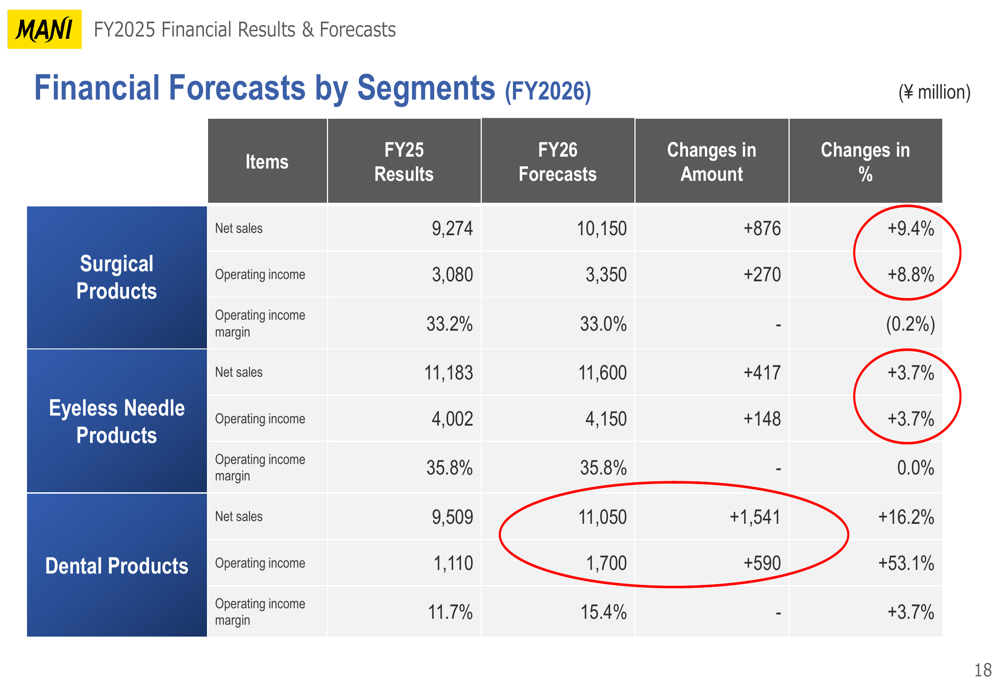

By segment, Mani expects growth across all three business areas, with particularly strong recovery in the Dental segment:

The Dental segment is forecast to grow by 16.2% to ¥11,050 million, with operating income increasing by 53.1% to ¥1,700 million as sales of dia-burs resume in China. The Surgical segment is expected to grow by 9.4% to ¥10,150 million, while the Eyeless Needle segment is projected to increase by 3.7% to ¥11,600 million.

Regarding shareholder returns, Mani announced a year-end dividend of ¥23 per share for FY2025 (annual dividend of ¥39) and forecasts an annual dividend of ¥41 per share for FY2026, continuing its track record of steady dividend increases.

Capital expenditure is expected to decrease significantly to ¥3.06 billion in FY2026, down from ¥6.67 billion in FY2025, as major investments in the Smart Factory have been completed. R&D expenses are projected to increase to ¥2.8 billion, representing 8.5% of consolidated sales.

Mani’s strong balance sheet, with net assets of ¥54,111 million as of August 31, 2025, provides a solid foundation for the company’s growth strategies and continued investments in innovation. Despite the challenges faced in FY2025, particularly with the China recall, the company’s diversified global presence and segment mix have demonstrated resilience, positioning it well for recovery and growth in FY2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.