JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Martin Midstream Partners LP (NASDAQ:MMLP) released its second quarter 2025 earnings presentation on July 16, 2025, revealing a year-over-year decline in adjusted EBITDA and a shift from net income to net loss. The midstream energy company’s stock closed at $2.95, down 2.34% from the previous close of $3.02, trading closer to the lower end of its 52-week range of $2.56 to $4.131.

The presentation comes amid ongoing challenges in certain business segments, particularly in Specialty Products, which has faced weak demand in recent quarters. The company continues to navigate a complex market environment while maintaining its focus on service and fixed-fee revenue streams, which now account for 71% of its EBITDA.

Quarterly Performance Highlights

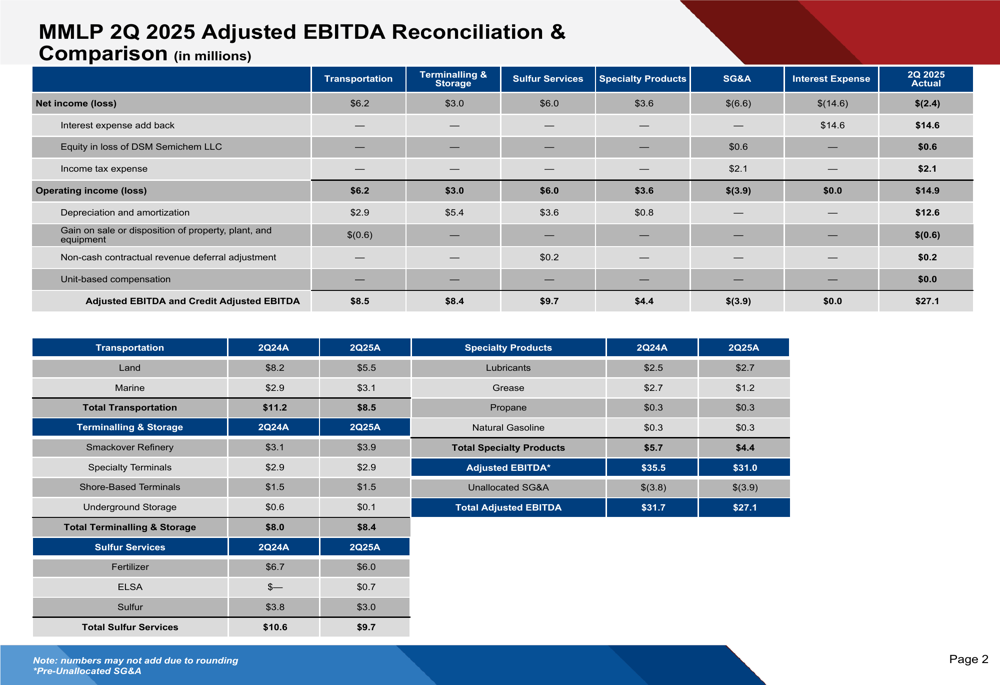

Martin Midstream reported a net loss of $2.4 million for Q2 2025, a significant decline from the $3.8 million net income recorded in the same period last year. Adjusted EBITDA for the quarter came in at $27.1 million, down from $31.7 million in Q2 2024, representing a 14.5% decrease.

As shown in the following detailed reconciliation of Q2 2025 results:

The company’s performance varied significantly across its four business segments. The Transportation segment saw the largest decline, with adjusted EBITDA falling from $11.2 million in Q2 2024 to $8.5 million in Q2 2025. This represents a stark contrast to the previous quarter’s performance, as Transportation had been highlighted as a standout performer in Q3 2024.

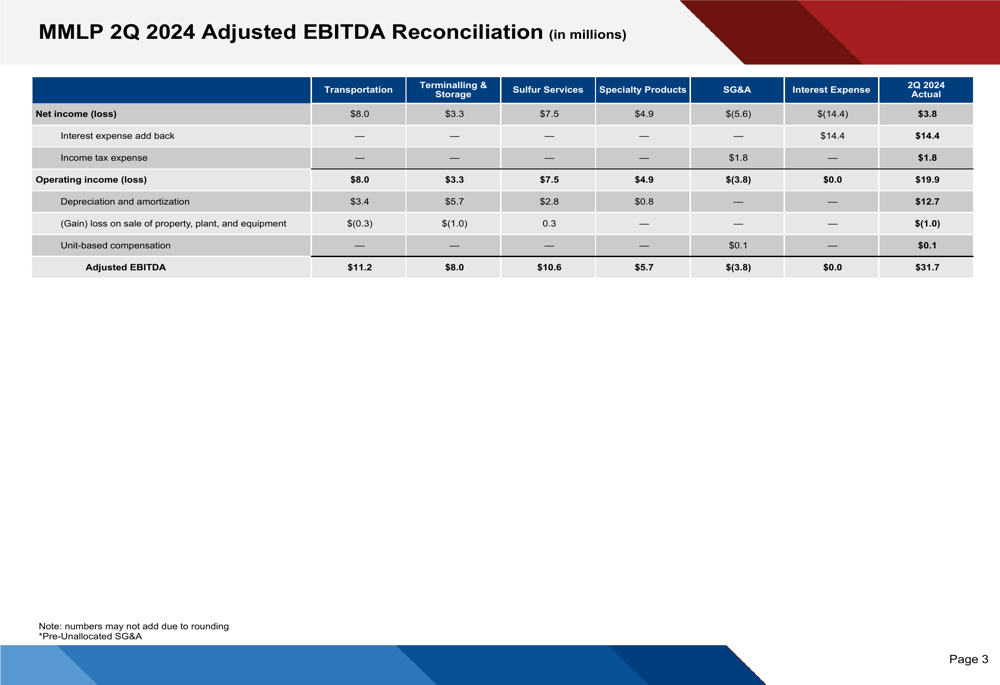

For comparison, here is the reconciliation from Q2 2024:

Segment Analysis

The Terminalling & Storage segment was the only bright spot in Martin Midstream’s quarterly results, posting an increase in adjusted EBITDA from $8.0 million in Q2 2024 to $8.4 million in Q2 2025. This growth was primarily driven by improved performance at the Smackover Refinery, which increased from $3.1 million to $3.9 million.

The Sulfur Services segment experienced a decline, with adjusted EBITDA falling from $10.6 million to $9.7 million. Within this segment, the presentation highlighted a new contribution of $0.7 million from ELSA operations. This is noteworthy as previous earnings reports had mentioned delays in the ELSA plant start-up, which was initially expected to begin receiving feedstock in August 2024 but was postponed to October 2024.

The Specialty Products segment continued to underperform, with adjusted EBITDA dropping from $5.7 million to $4.4 million. This decline aligns with the company’s previous earnings report, which attributed weakness in this segment to softening demand in packaged lubricant and grease markets amid a slowing U.S. economy. The current presentation shows Grease EBITDA falling from $2.7 million to $1.2 million, confirming this ongoing challenge.

Full-Year 2025 Guidance

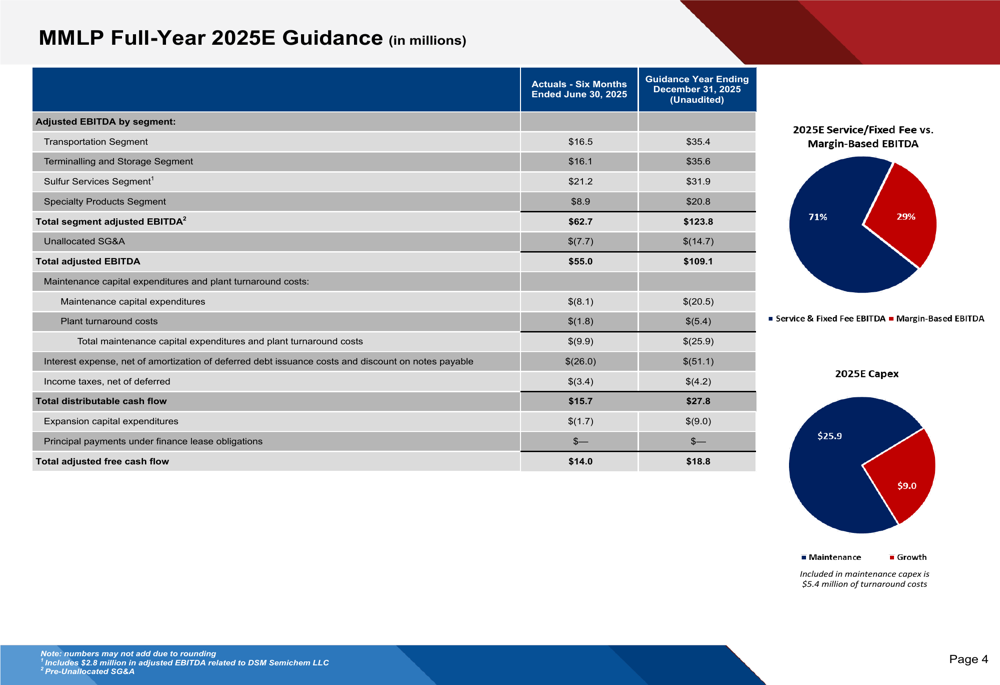

Despite the quarterly challenges, Martin Midstream maintained its full-year guidance for 2025. The company expects total adjusted EBITDA of $109.1 million, with total distributable cash flow of $27.8 million and adjusted free cash flow of $18.8 million.

The following chart details the company’s full-year 2025 guidance across all segments:

The guidance reveals that Martin Midstream expects its revenue mix to remain heavily weighted toward service and fixed-fee revenue (71%) versus margin-based revenue (29%), suggesting a strategic focus on more stable income streams. The company also projects $34.9 million in capital expenditures for the year, with $25.9 million allocated to maintenance and $9.0 million to expansion projects.

Strategic Initiatives & Outlook

While the presentation does not explicitly detail strategic initiatives, the allocation of capital expenditures provides some insight into the company’s priorities. The significant allocation toward maintenance capital expenditures suggests a focus on preserving existing assets and operations rather than aggressive expansion.

The presentation is notably silent on the pending buyout transaction with Martin Resource Management Corporation that was mentioned in previous earnings reports. According to the Q3 2024 earnings call, this transaction was expected to offer nearly a dollar more per unit than the initial proposal, with further details to be disclosed in a proxy statement.

Martin Midstream’s current financial position should be viewed in the context of its previous commitment to reduce leverage below four times by year-end 2024. While the current presentation does not address debt levels directly, the company’s ability to generate $18.8 million in adjusted free cash flow for 2025 could potentially support ongoing deleveraging efforts.

As the company navigates through 2025, investors will likely focus on whether Martin Midstream can reverse the negative trend in its Transportation and Specialty Products segments while capitalizing on the positive momentum in its Terminalling & Storage operations. The contribution from the delayed ELSA plant will also be a key area to watch, as it represents a new revenue stream within the Sulfur Services segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.