Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Martinrea International Inc . (TSX:MRE) released its first quarter 2025 results on May 1, revealing a challenging start to the year as the auto parts manufacturer navigates difficult market conditions. The company reported a significant year-over-year revenue decline while maintaining relatively stable operating margins, demonstrating operational resilience amid headwinds.

The company’s stock closed at $7.34 on the day of the announcement, near the middle of its 52-week range of $6.12 to $12.65, reflecting ongoing investor caution about the automotive supply sector.

Quarterly Performance Highlights

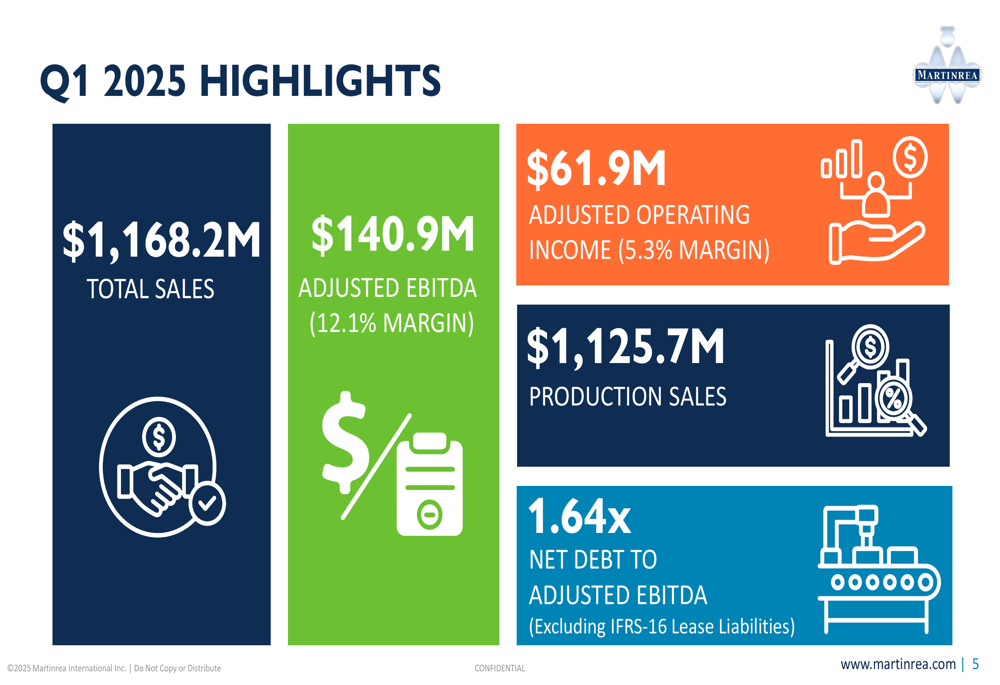

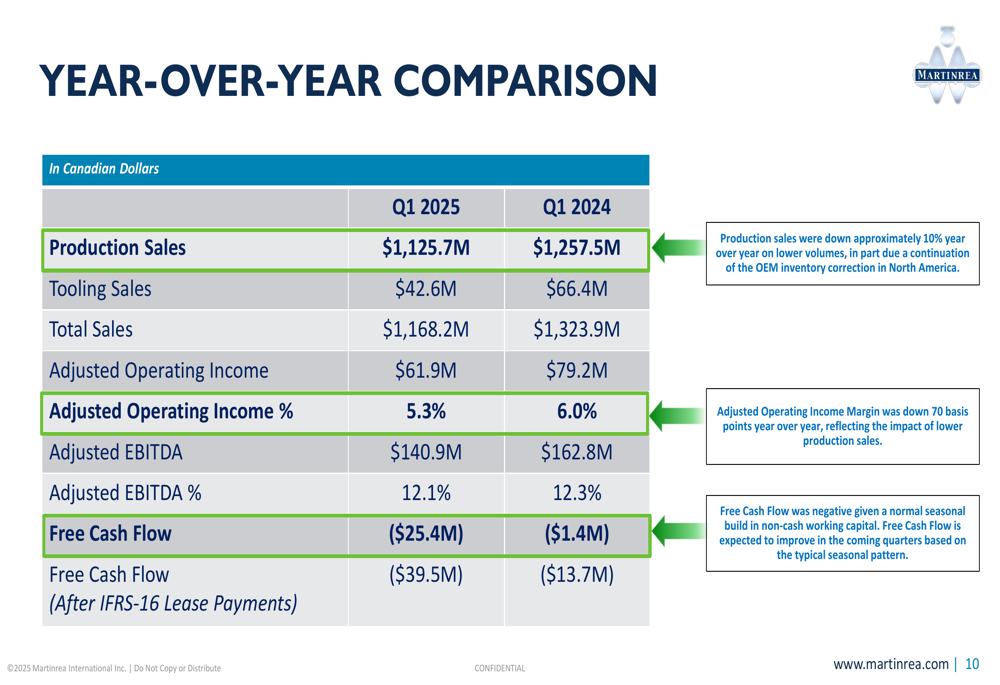

Martinrea reported total sales of $1,168.2 million for Q1 2025, representing an 11.8% decrease from $1,323.9 million in the same period last year. Production sales, which form the core of the company’s revenue, fell to $1,125.7 million from $1,257.5 million in Q1 2024.

As shown in the following financial highlights slide, the company maintained relatively stable margins despite the revenue decline:

Adjusted EBITDA came in at $140.9 million with a 12.1% margin, compared to $162.8 million and a 12.3% margin in Q1 2024. Adjusted operating income was $61.9 million (5.3% margin), down from $79.2 million (6.0% margin) a year earlier.

The year-over-year comparison reveals consistent pressure across all major financial metrics:

Notably, free cash flow deteriorated to negative $25.4 million, compared to negative $1.4 million in Q1 2024. This decline in cash generation reflects ongoing challenges in the operating environment and potentially higher working capital requirements.

Adjusted net earnings per share dropped to $0.41 from $0.62 in the prior-year period, representing a 33.9% decrease that outpaced the revenue decline, suggesting some margin compression and reduced operational leverage.

Regional Performance and New Business

According to the presentation, Martinrea’s regional performance showed mixed results. North American operations maintained strong margins despite challenges, while European operations improved significantly compared to the fourth quarter. The Rest of World segment also showed improvement both year-over-year and sequentially.

Fred Di Tosto, Martinrea’s President, emphasized the company’s execution capabilities, noting they were "executing well in a tough market."

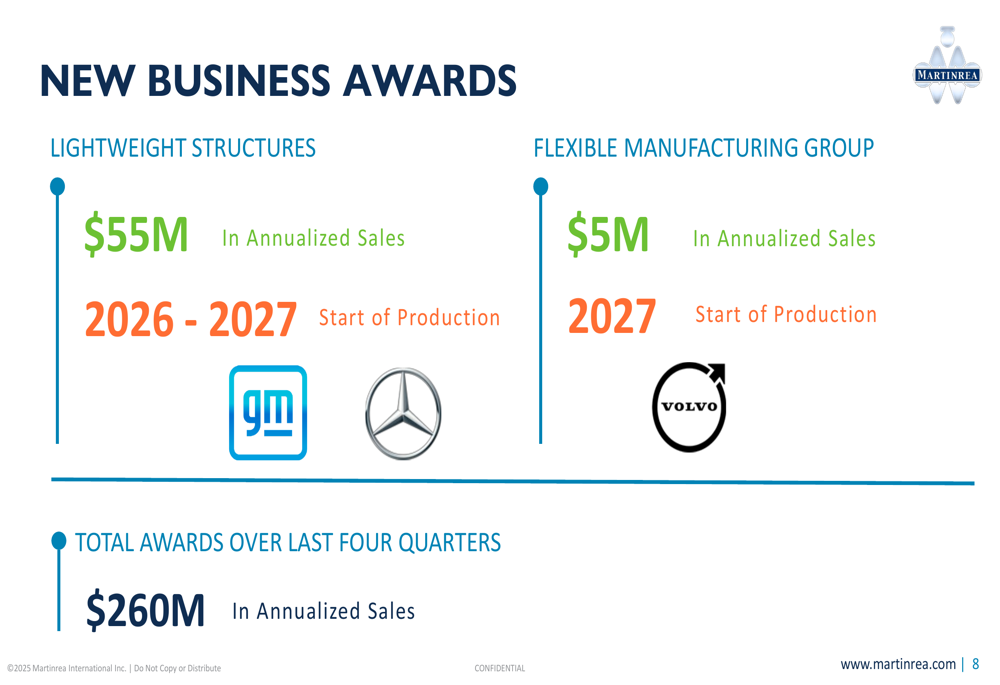

The company continues to secure new business, announcing awards worth $60 million in annualized sales during the quarter:

These new awards, primarily with major OEMs including GM, Mercedes, and Volvo (OTC:VLVLY), demonstrate Martinrea’s continued competitive position in the market. The company highlighted that over the past four quarters, it has secured a total of $260 million in annualized new business, providing a foundation for future growth despite current market challenges.

Financial Position and 2025 Outlook

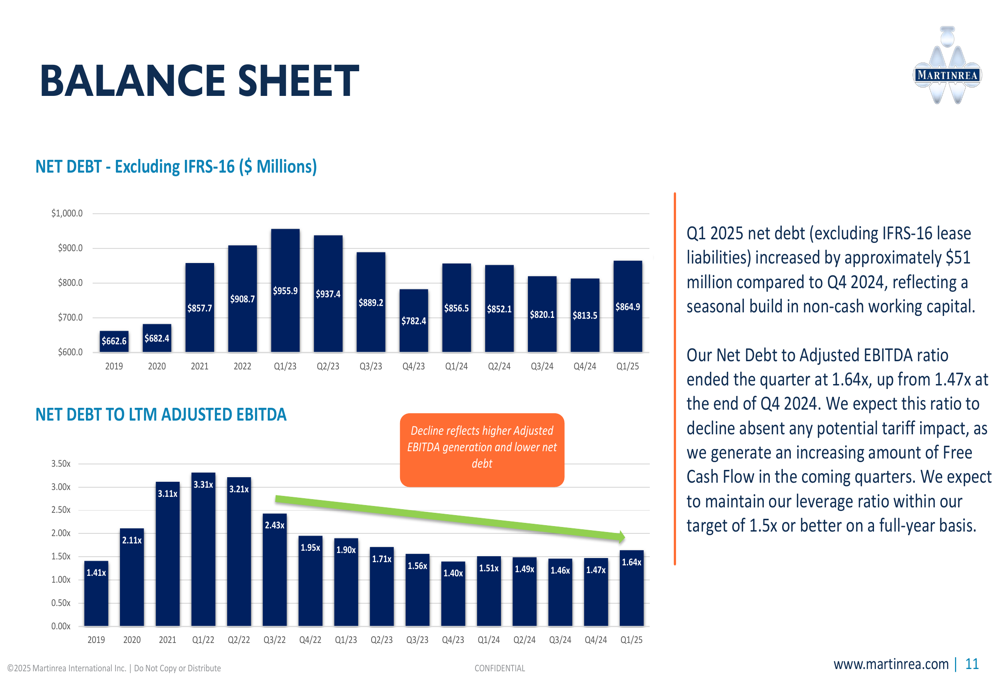

Martinrea’s balance sheet showed a slight increase in leverage, with net debt (excluding IFRS-16 lease liabilities) rising to $864.9 million and the net debt to adjusted EBITDA ratio increasing to 1.64x, as illustrated in the following slide:

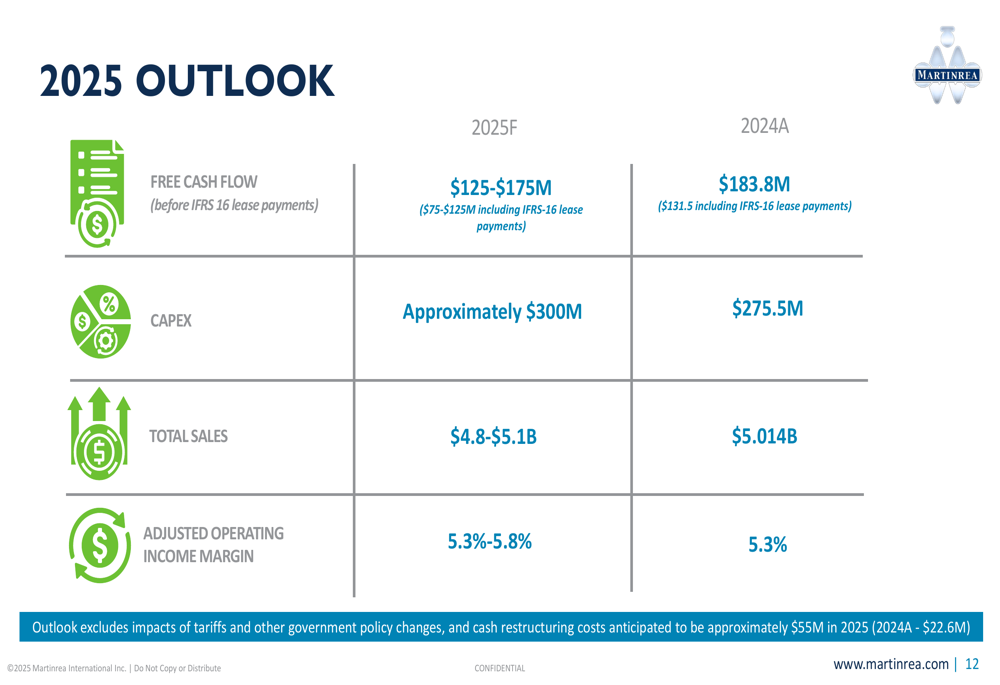

Looking ahead, the company provided a comprehensive outlook for 2025, projecting total sales between $4.8-$5.1 billion compared to $5.014 billion in 2024:

The 2025 guidance suggests Martinrea expects adjusted operating income margins to remain stable or potentially improve slightly to 5.3%-5.8%, compared to 5.3% in 2024. Free cash flow before IFRS 16 lease payments is projected at $125-$175 million, while capital expenditures are expected to increase to approximately $300 million from $275.5 million in 2024.

Importantly, the company noted that this outlook excludes potential impacts from tariffs and other government policy changes, as well as cash restructuring costs anticipated to be approximately $55 million in 2025.

Strategic Initiatives and Trade Policy

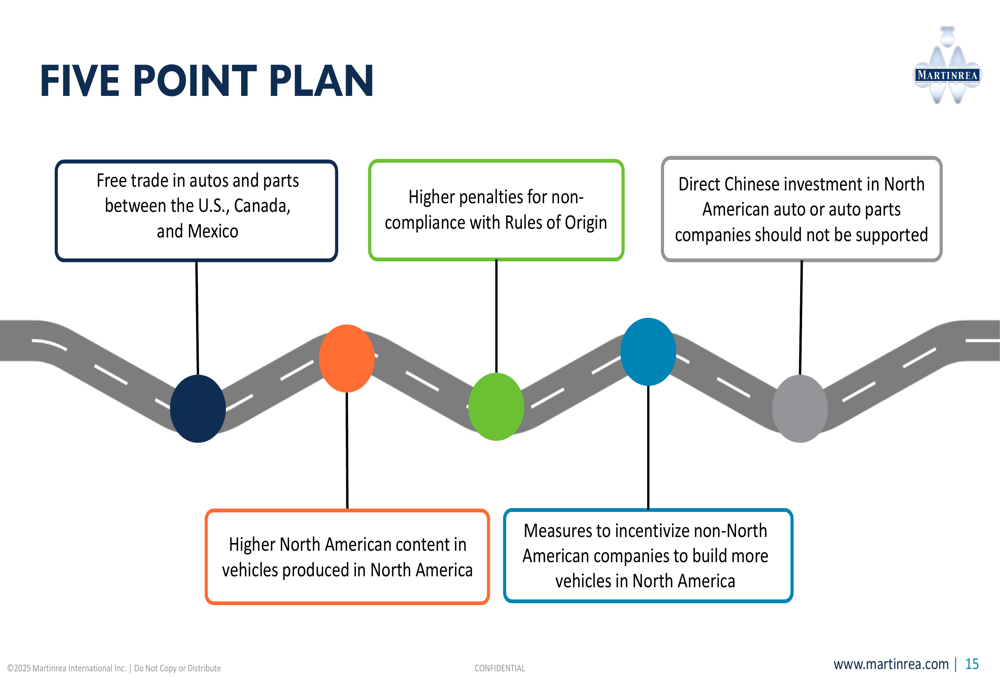

A significant portion of the presentation focused on trade and tariff issues, with Executive Chairman Rob Wildeboer outlining a five-point plan addressing North American automotive trade:

This strategic focus on trade policy reflects Martinrea’s positioning as a North American-centered manufacturer and its concerns about potential changes to trade agreements and tariff structures. The plan emphasizes free trade between the U.S., Canada, and Mexico while advocating for higher North American content requirements and restrictions on direct Chinese investment in the sector.

Conclusion

Martinrea’s Q1 2025 results reflect the challenging operating environment facing automotive suppliers, with declining revenues and profits compared to the prior year. However, the company has demonstrated resilience by maintaining relatively stable margins and securing new business that should support future growth.

The outlook for 2025 suggests management expects conditions to stabilize, with potential for modest margin improvement despite flat to slightly lower revenue projections. Increased capital expenditure indicates continued investment in future capabilities, while the focus on North American trade policy highlights the company’s strategic positioning in an evolving regulatory landscape.

Investors will likely watch closely for signs of market stabilization and the impact of potential trade policy changes on Martinrea’s competitive position in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.