United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Masco Corporation (NYSE:MAS) reported its first quarter 2025 results on April 23, showing revenue and profit declines amid challenging market conditions. The company has opted to withdraw its full-year guidance, citing macroeconomic and tariff uncertainties. Despite these headwinds, Masco maintained relatively strong margins and continued its share repurchase program, indicating confidence in its long-term strategy.

The company’s performance reflects broader challenges in the home improvement sector, with particular pressure on the Decorative Architectural segment. However, Masco continues to leverage its strong brands and introduce innovative products across its portfolio.

Quarterly Performance Highlights

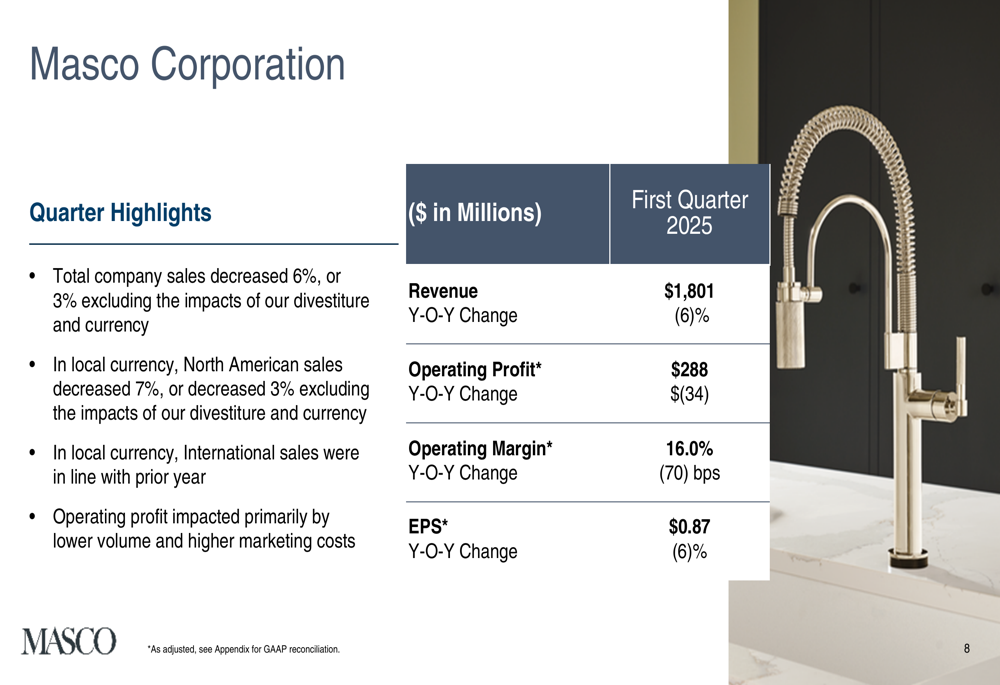

Masco reported first quarter revenue of $1,801 million, representing a 6% decrease year-over-year, or 3% excluding the impacts of divestitures and currency fluctuations. The company’s adjusted operating profit came in at $288 million, down $34 million from the prior year, with operating margin contracting 70 basis points to 16.0%. Adjusted earnings per share fell 6% to $0.87.

Despite the top-line pressure, Masco improved its adjusted gross margin by 20 basis points to 35.9%, demonstrating continued focus on operational efficiency and cost management. The company also repurchased 1.8 million shares for $130 million during the quarter, reinforcing its commitment to returning value to shareholders.

As shown in the following summary of quarterly performance:

Segment Analysis

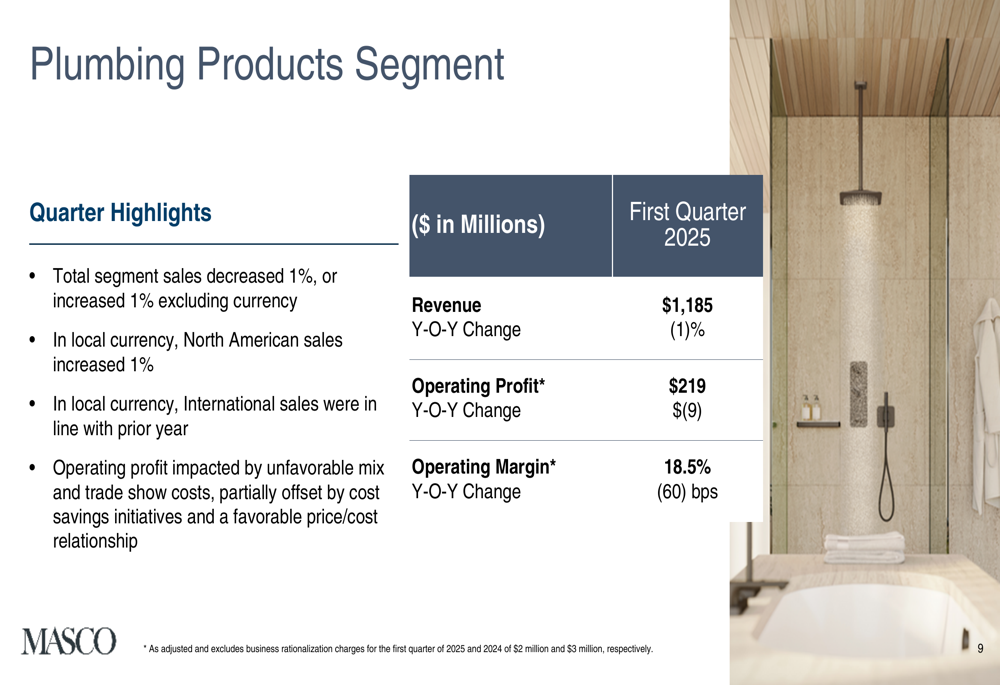

Masco’s Plumbing Products segment, which represents the larger portion of the company’s business, reported revenue of $1,185 million, a 1% decrease year-over-year, or a 1% increase excluding currency impacts. North American sales in this segment increased 1% in local currency, while International sales remained flat compared to the prior year. The segment’s operating profit decreased by $9 million to $219 million, with operating margin declining 60 basis points to 18.5%. These results were impacted by unfavorable mix and trade show costs, partially offset by cost savings initiatives and favorable price/cost relationships.

The segment details are illustrated in the following slide:

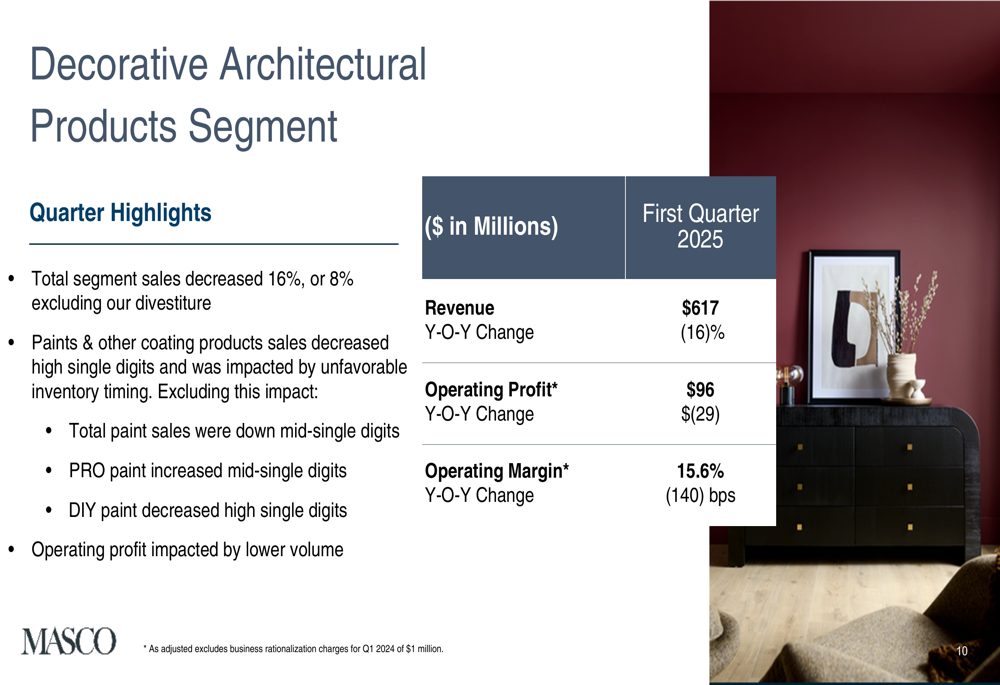

The Decorative Architectural Products segment faced more significant challenges, with revenue declining 16% to $617 million, or 8% excluding the impact of divestitures. Paint and other coating products sales decreased by high single digits, affected by unfavorable inventory timing. Within this category, professional paint sales increased by mid-single digits, while DIY paint sales decreased by high single digits. Operating profit for the segment fell by $29 million to $96 million, with operating margin contracting 140 basis points to 15.6%.

The performance of this segment is detailed in the following slide:

Balance Sheet and Capital Allocation

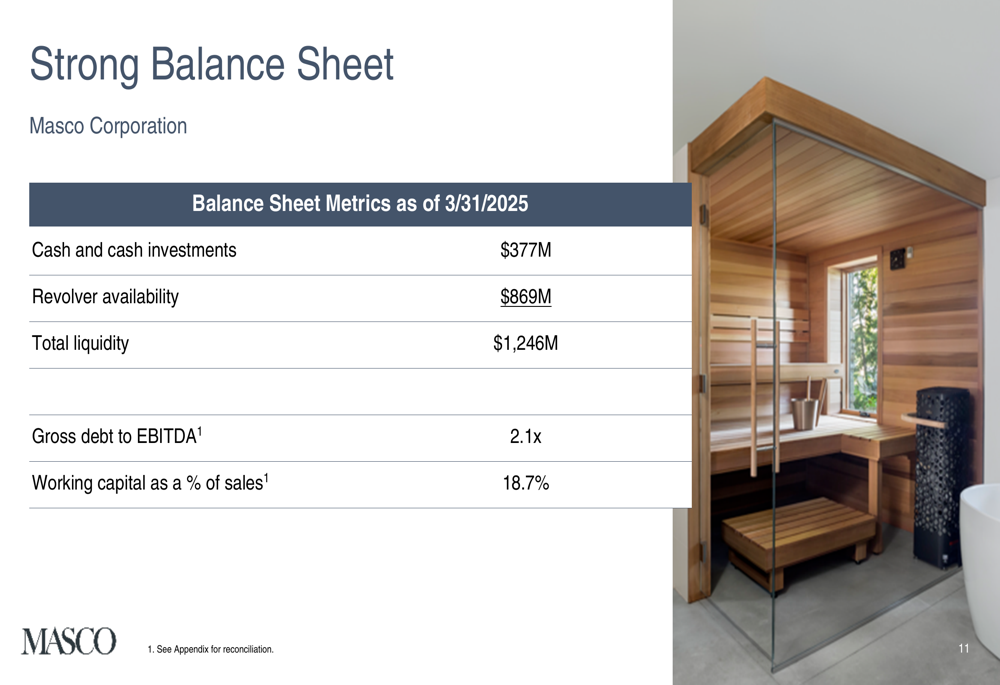

Despite the challenging operating environment, Masco maintained a strong financial position. As of March 31, 2025, the company reported $377 million in cash and cash investments, $869 million in revolver availability, and total liquidity of $1,246 million. Masco’s gross debt to EBITDA ratio stood at 2.1x, while working capital as a percentage of sales was 18.7%.

The company’s balance sheet strength is illustrated in this slide:

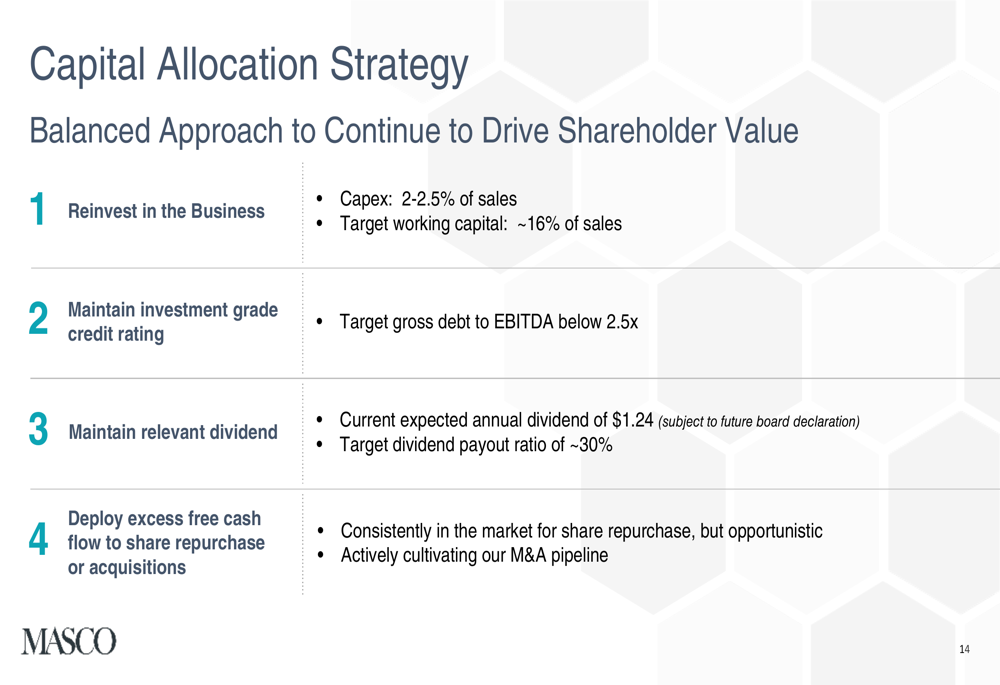

Masco’s capital allocation strategy remains focused on four key priorities: reinvesting in the business (with capital expenditures targeted at 2-2.5% of sales), maintaining an investment grade credit rating (targeting gross debt to EBITDA below 2.5x), providing a relevant dividend (with a current expected annual dividend of $1.24 and a target payout ratio of approximately 30%), and deploying excess free cash flow to share repurchases or acquisitions.

This disciplined approach to capital allocation is outlined in the following slide:

Strategic Initiatives and Product Innovation

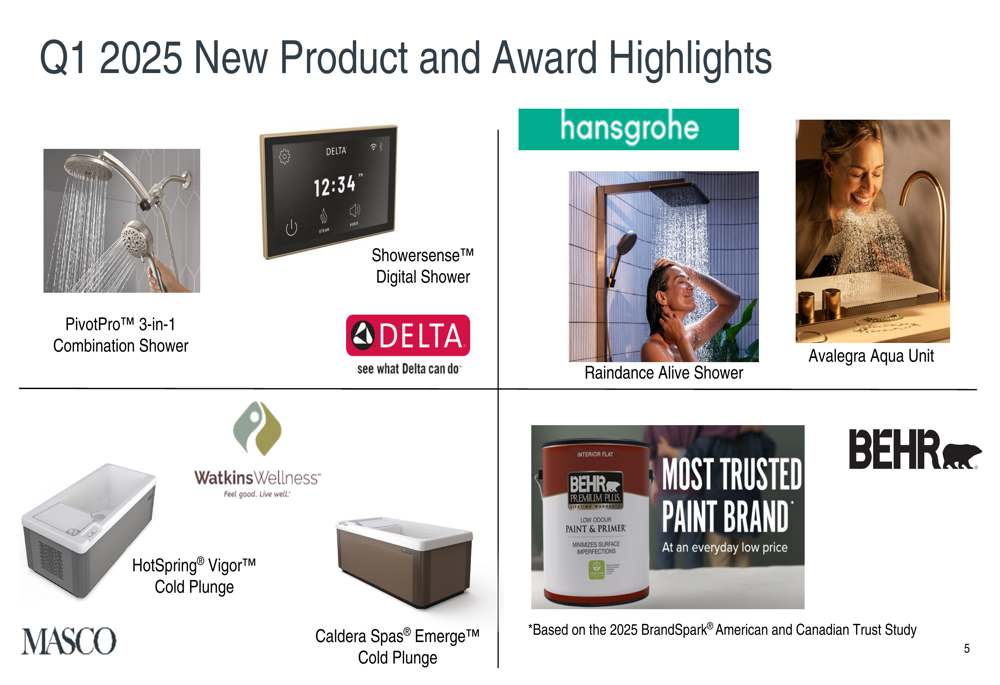

Despite the challenging market conditions, Masco continues to invest in product innovation across its portfolio. In the first quarter of 2025, the company introduced several new products, including the PivotPro™ 3-in-1 Combination Shower, Showersense™ Digital Shower (Delta), Raindance Alive Shower (Hansgrohe), Avalegra Aqua Unit, HotSpring® Vigor™ Cold Plunge, and Caldera Spas® Emerge™ Cold Plunge. Additionally, Behr was recognized as the "Most Trusted Paint Brand" based on the 2025 BrandSpark® American and Canadian Trust Study.

The company’s product innovation highlights are showcased in this slide:

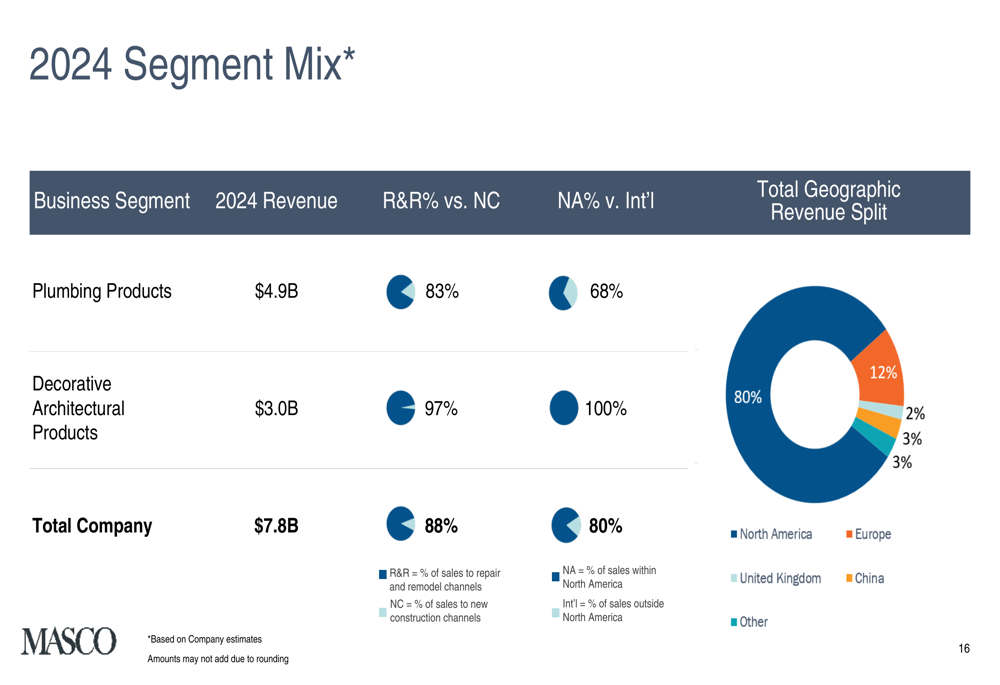

Masco’s business remains well-positioned in the repair and remodel (R&R) market, which provides greater stability through economic cycles compared to new construction. The company’s 2024 segment mix shows that Plumbing Products generated $4.9 billion in revenue (with 83% from R&R vs. new construction), while Decorative Architectural Products contributed $3.0 billion (with 97% from R&R).

The company’s segment mix and geographic diversification are illustrated in the following slide:

Outlook and Forward Guidance

In a significant development, Masco has opted not to provide full-year 2025 financial guidance at this time, citing tariff and macroeconomic uncertainty. This represents a shift from the company’s approach in previous quarters, reflecting increased caution about near-term market conditions.

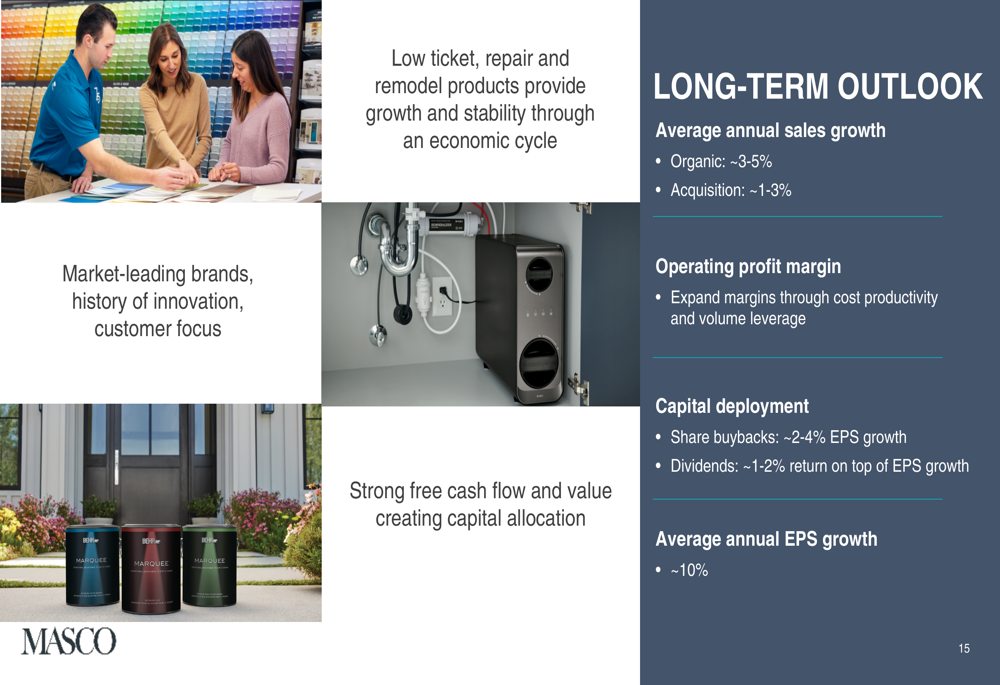

Despite this short-term uncertainty, Masco maintains a positive long-term outlook. The company continues to target average annual organic sales growth of 3-5%, with an additional 1-3% from acquisitions. Masco aims to expand operating profit margins through cost productivity and volume leverage, while deploying capital to generate 2-4% EPS growth from share buybacks and 1-2% return from dividends. Overall, the company’s long-term target for average annual EPS growth remains at approximately 10%.

The long-term outlook is detailed in the following slide:

Comparison to Previous Performance

Masco’s Q1 2025 results represent a notable shift from its Q3 2024 performance, when the company displayed resilience with stable net sales and an 8% increase in earnings per share to $1.08. In contrast, the current quarter shows a 6% revenue decline and a 6% decrease in EPS to $0.87.

The Plumbing segment, which showed 2% growth in Q3 2024, has now experienced a 1% decline in Q1 2025. Similarly, the Decorative Architectural segment has faced increased pressure, with sales declining 16% compared to a 3% decline in Q3 2024.

The decision to withdraw full-year guidance marks a significant change from Q3 2024, when the company projected adjusted EPS for 2024 between $4.05 and $4.15 and anticipated operating margins of approximately 17.5%.

Despite these challenges, Masco’s fundamentals remain strong, with the company maintaining its focus on operational efficiency, cost management, and strategic capital allocation to position itself for long-term growth when market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.