Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Masimo Corporation (NASDAQ:MASI) released its first quarter 2025 earnings presentation on May 6, revealing strong financial performance across key metrics, but the stock fell 7.1% in aftermarket trading to $150, likely due to concerns about significant tariff headwinds that could impact future results.

The healthcare technology company reported substantial growth in both revenue and profitability, continuing the momentum seen in its previous quarter. However, newly implemented tariffs are expected to significantly impact the company’s cost structure throughout 2025, potentially eroding some of the operational gains achieved.

Quarterly Performance Highlights

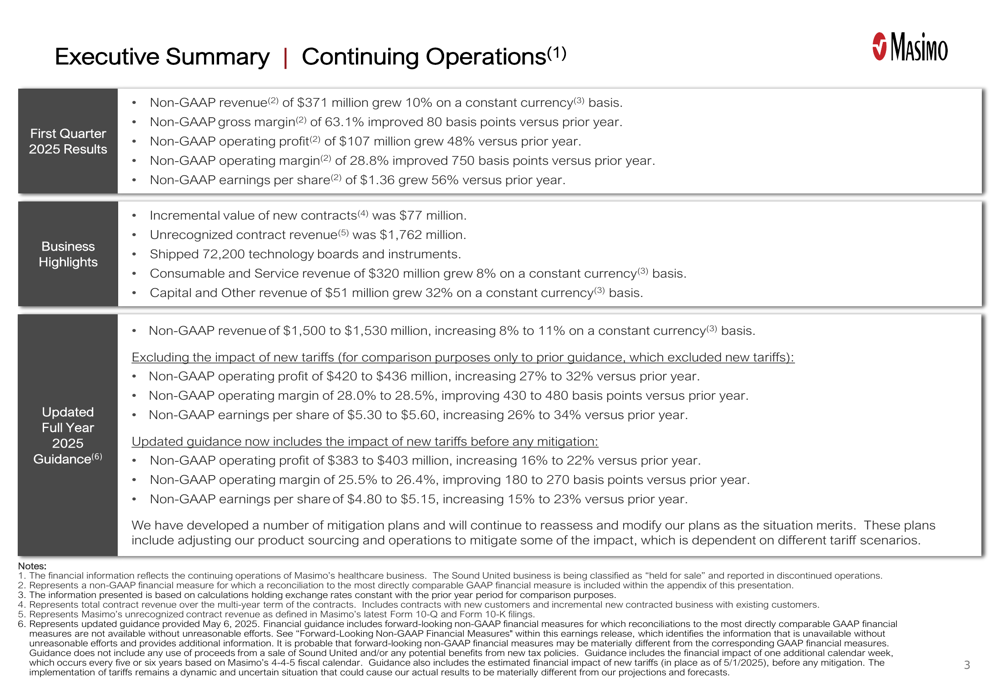

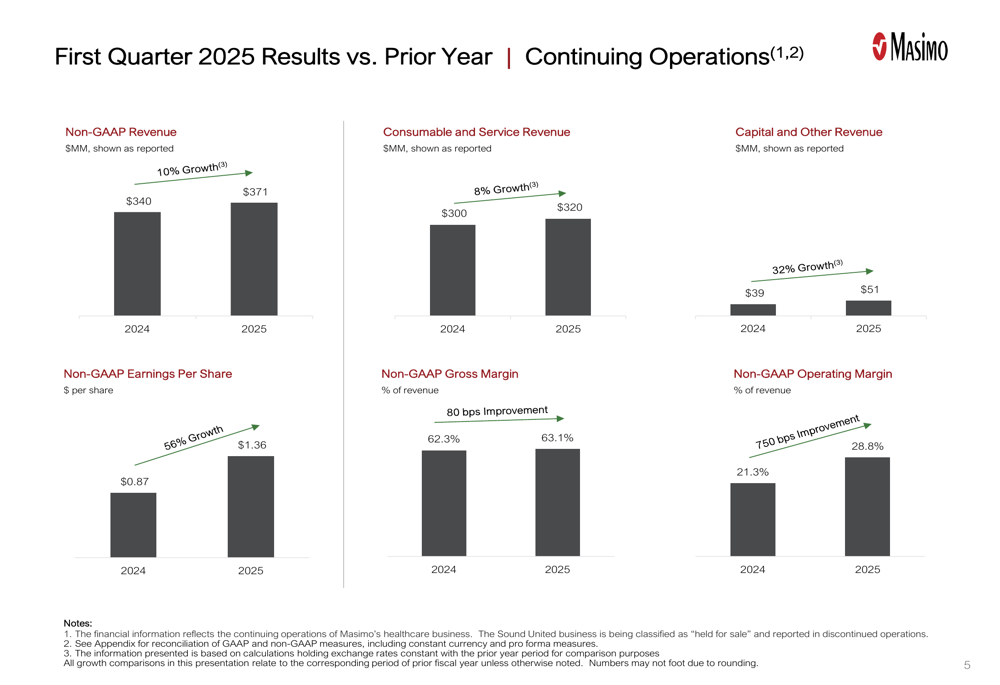

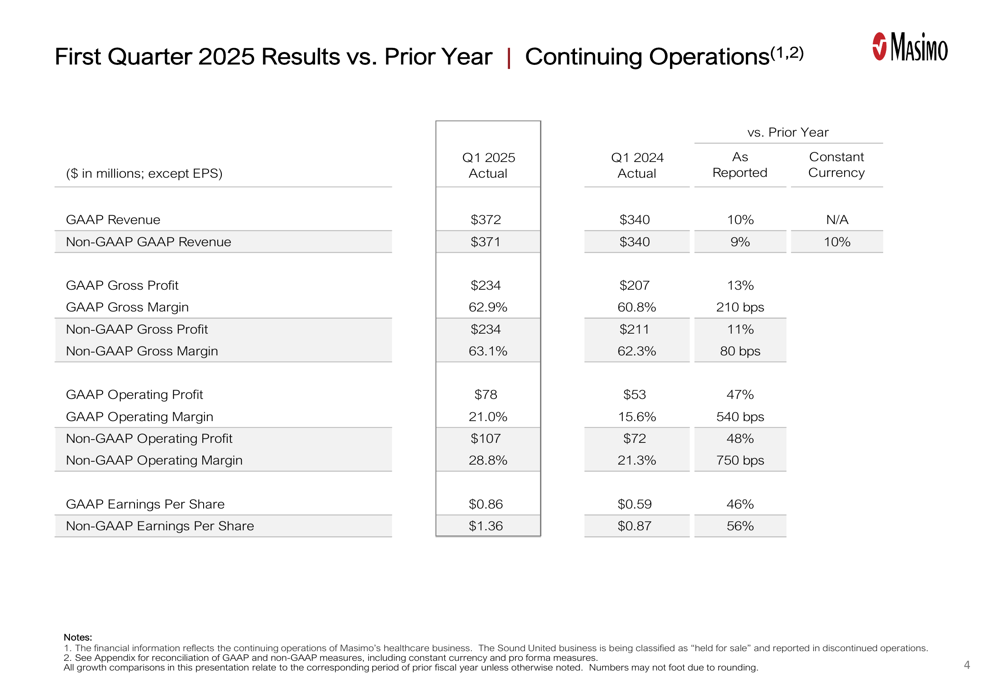

Masimo delivered impressive first quarter results, with non-GAAP revenue reaching $371 million, representing a 10% increase on a constant currency basis compared to the same period last year. The company’s profitability metrics showed even stronger improvement, with non-GAAP operating profit surging 48% to $107 million and non-GAAP earnings per share jumping 56% to $1.36.

As shown in the following comprehensive results summary:

The company’s performance was driven by growth across both its consumables and capital equipment segments. Consumable and service revenue, which represents the majority of Masimo’s business at $320 million, grew 8% on a constant currency basis. Meanwhile, capital and other revenue showed particularly strong momentum, increasing 32% to $51 million.

The following chart illustrates the year-over-year growth across key financial metrics:

Detailed Financial Analysis

Masimo’s margin performance was particularly noteworthy in Q1 2025. The company achieved a non-GAAP gross margin of 63.1%, an improvement of 80 basis points from the prior year. Even more impressive was the expansion in operating margin, which increased 750 basis points to 28.8%, reflecting the company’s operational efficiency and scaling benefits.

The detailed comparison between GAAP and non-GAAP results provides further insight into the company’s performance:

The company also reported strong business momentum with the incremental value of new contracts reaching $77 million during the quarter. Unrecognized contract revenue stood at $1,762 million, providing visibility into future revenue streams. Additionally, Masimo shipped 72,200 technology boards and instruments during the quarter, indicating healthy demand for its monitoring technologies.

Tariff Impact Analysis

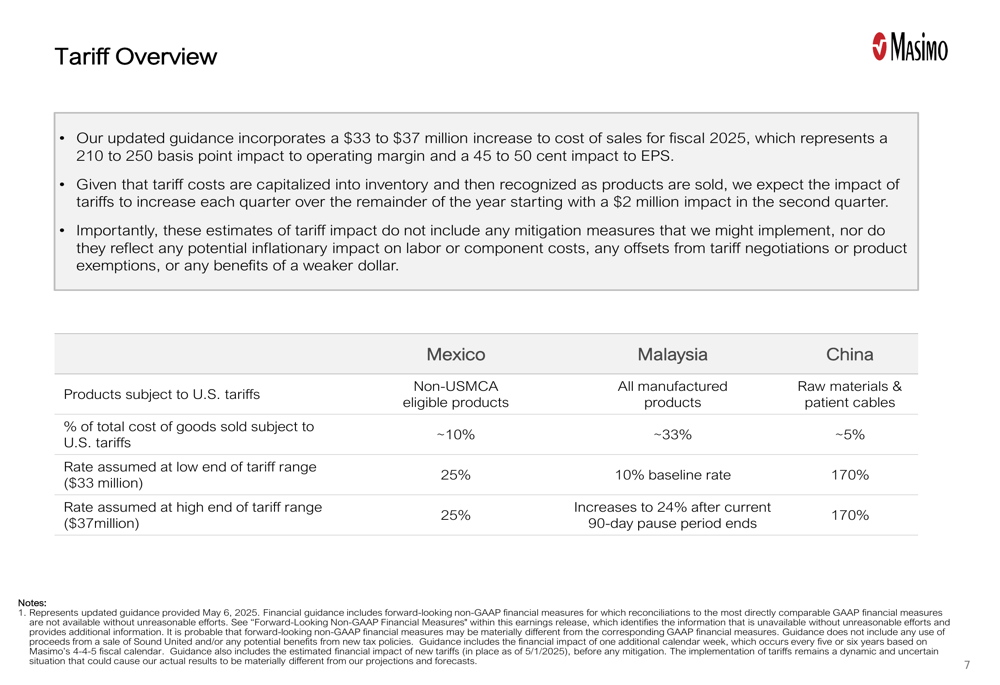

Despite the strong operational performance, Masimo’s presentation highlighted significant challenges from newly implemented tariffs that will impact its cost structure throughout 2025. The company expects these tariffs to increase its cost of sales by $33 to $37 million for the fiscal year, representing a 210 to 250 basis point impact to operating margin and a 45 to 50 cent impact to earnings per share.

The following slide details the specific tariff impacts by country:

The tariff impact is expected to escalate throughout the year, starting with a $2 million impact in the second quarter. Notably, approximately 10% of Masimo’s total cost of goods sold is subject to US tariffs on non-USMCA eligible products from Mexico at a 25% rate, while about 33% is subject to tariffs on manufactured products from Malaysia at rates that will increase from 10% to 24% after a 90-day pause.

Forward-Looking Statements

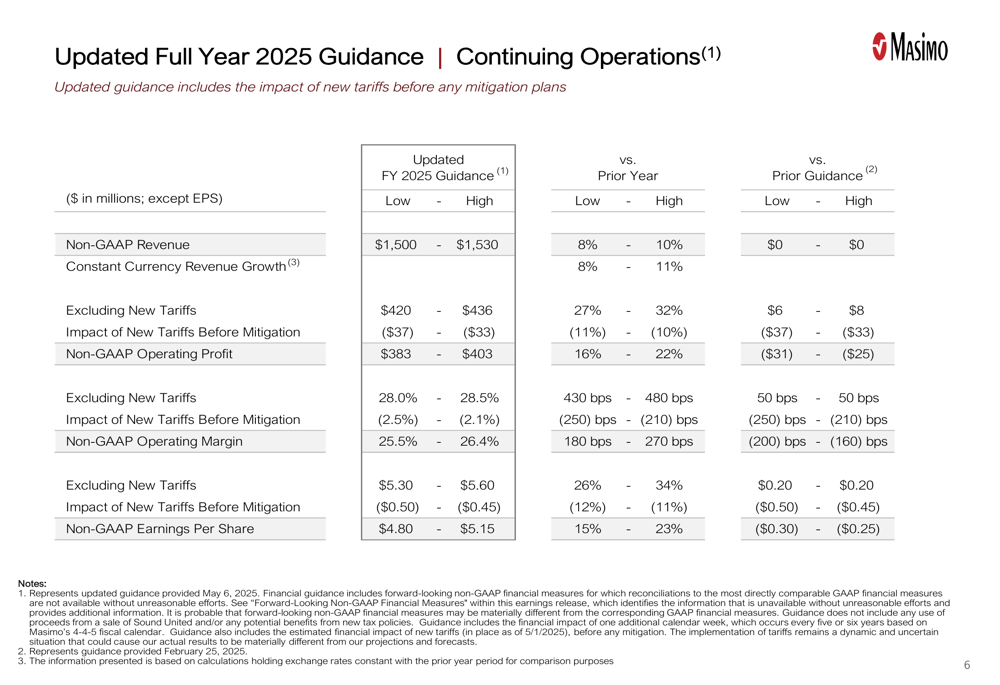

Despite the tariff headwinds, Masimo provided an updated full-year 2025 guidance that shows continued growth. The company expects non-GAAP revenue of $1,500 to $1,530 million, representing 8% to 11% growth on a constant currency basis.

The guidance includes two scenarios - one excluding the impact of new tariffs and one including them:

Excluding tariffs, Masimo actually raised its operating profit guidance by $6 to $8 million above prior projections, demonstrating confidence in its underlying business performance. However, when including the tariff impact, the company expects non-GAAP operating profit of $383 to $403 million (16% to 22% year-over-year growth) and non-GAAP earnings per share of $4.80 to $5.15 (15% to 23% growth).

The negative market reaction following the presentation suggests investors are focusing more on the tariff headwinds than the strong underlying performance and raised guidance (excluding tariffs). Management did not provide specific details on potential mitigation strategies for the tariff impact, which may have contributed to investor concerns.

As Masimo navigates these tariff challenges, the company’s ability to maintain its operational efficiency and potentially adjust its supply chain will be critical factors for investors to monitor throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.