S&P 500 climbs, but Nvidia slip keeps lid on gains

Matrix Service Company (NASDAQ:MTRX) presented its first quarter fiscal 2026 results on November 6, 2025, highlighting significant revenue growth, improving margins, and a robust project backlog. The company's shares rose 9.29% in premarket trading, reflecting investor optimism about the company's recovery trajectory after disappointing fourth-quarter results.

Quarterly Performance Highlights

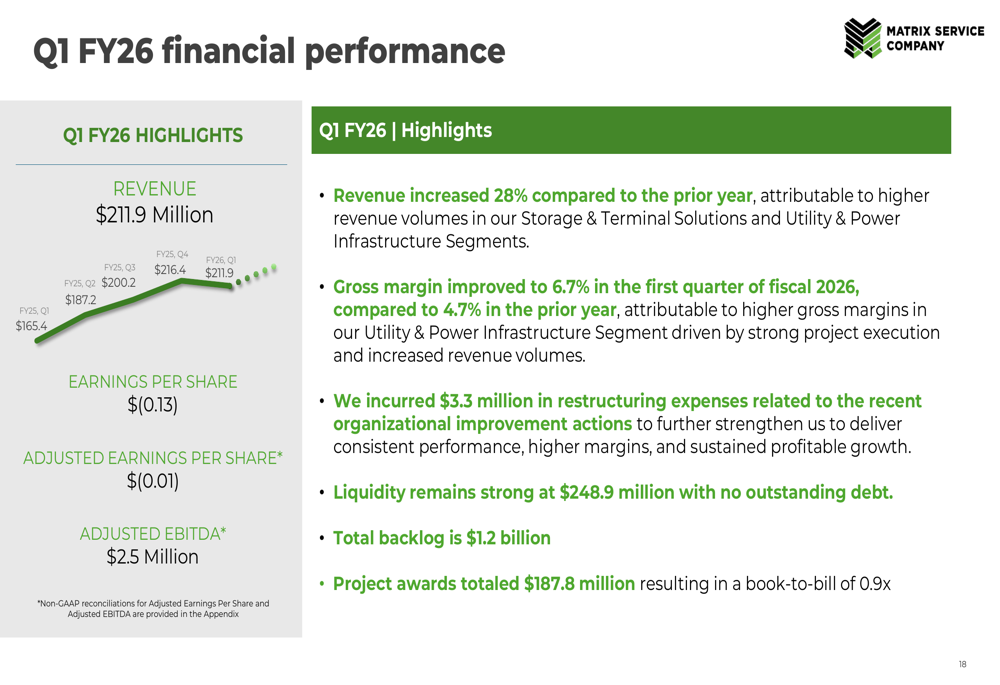

Matrix Service reported Q1 FY26 revenue of $211.9 million, representing a 28% increase compared to $165.6 million in the same period last year. Gross margin improved to 6.7%, up from 4.7% in Q1 FY25, while SG&A expenses decreased to $16.3 million from $18.6 million year-over-year.

The company posted an adjusted net loss per share of $0.01, a substantial improvement from the $0.33 loss per share in the prior-year quarter. Adjusted EBITDA turned positive at $2.5 million, compared to negative $5.9 million in Q1 FY25.

As shown in the following chart of quarterly financial performance, Matrix has demonstrated consistent revenue growth over the past five quarters:

Despite the improved performance, the company incurred $3.3 million in restructuring costs during the quarter. These costs are part of Matrix's efforts to streamline operations and improve profitability, which appears to be yielding results as evidenced by the narrowing operating loss percentage (-2.6% vs -6.5% year-over-year).

Strategic Initiatives

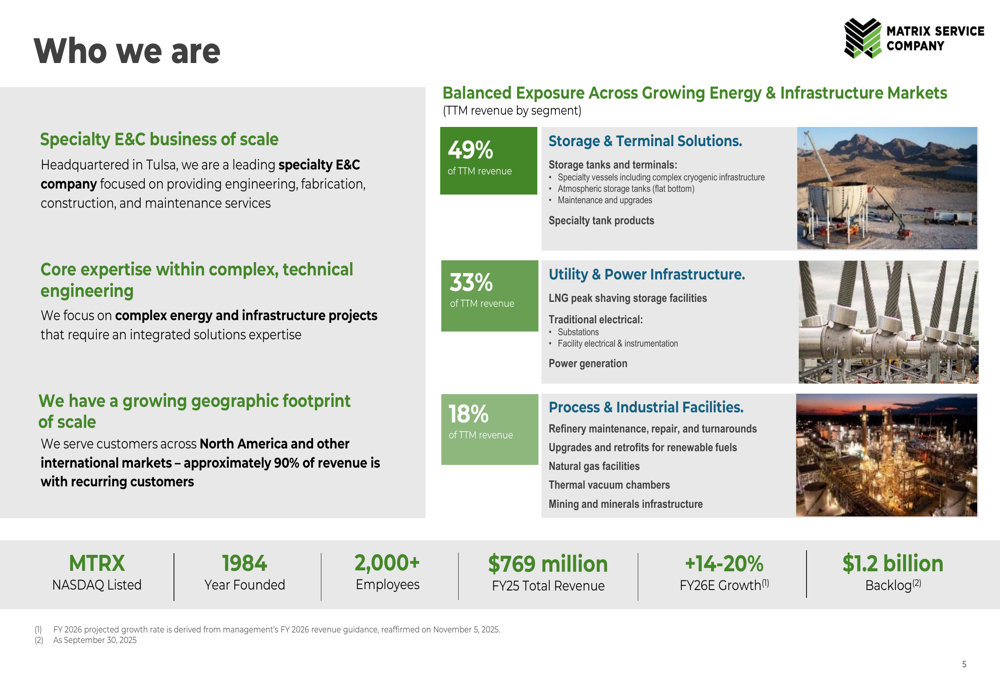

Matrix Service is positioning itself across three core business segments, with Storage & Terminal Solutions representing the largest portion at 49% of trailing twelve-month revenue, followed by Utility & Power Infrastructure at 33% and Process & Industrial Facilities at 18%.

The company is leveraging its 40+ year track record in specialty engineering and construction to expand into high-growth markets while maintaining its presence in traditional sectors. This strategic approach is illustrated in the company's market sector focus:

Matrix is particularly targeting expansion into data centers, semiconductors, advanced manufacturing, and power generation—sectors experiencing significant investment growth. The company offers full lifecycle solutions across planning, construction, and asset service phases, providing an integrated approach to complex energy and infrastructure projects.

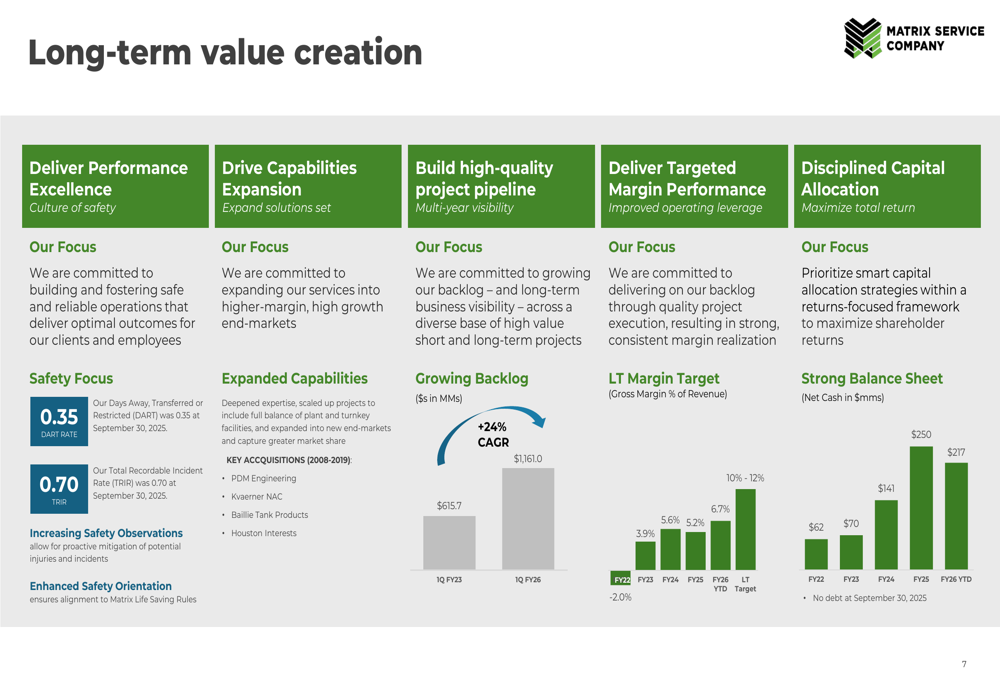

The company's long-term value creation strategy focuses on four key pillars as shown below:

Forward-Looking Statements

Matrix Service reaffirmed its fiscal 2026 revenue guidance of $875-925 million, representing 14-20% growth over fiscal 2025. This guidance is supported by a strong backlog of $1.2 billion and Q1 project awards totaling $187.8 million.

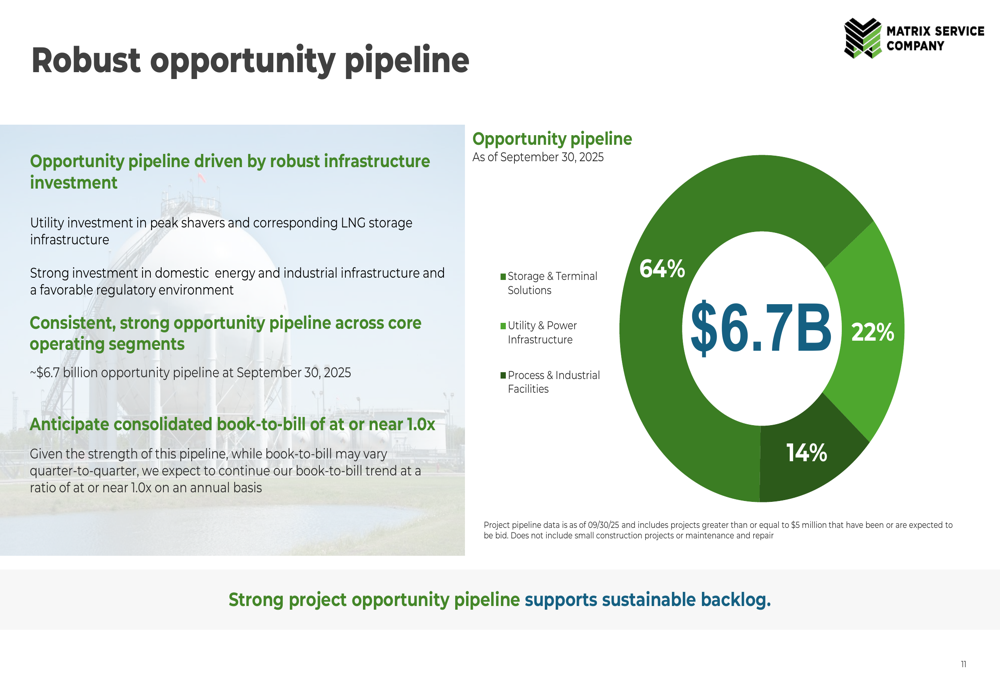

The company's opportunity pipeline stands at an impressive $6.7 billion, driven by utility investment, strong domestic energy and industrial infrastructure spending, and a favorable regulatory environment. The breakdown of this pipeline is visualized below:

Management expects to achieve a book-to-bill ratio at or near 1.0x, indicating continued strong project awards that should sustain the company's growth trajectory.

Detailed Financial Analysis

Matrix Service's backlog composition demonstrates strength across all segments, with Storage & Terminal Solutions leading at $796.7 million, followed by Utility & Power Infrastructure at $262.3 million and Process & Industrial Facilities at $101.9 million. This diverse backlog provides revenue visibility and stability.

The following chart details the company's project awards and backlog by segment:

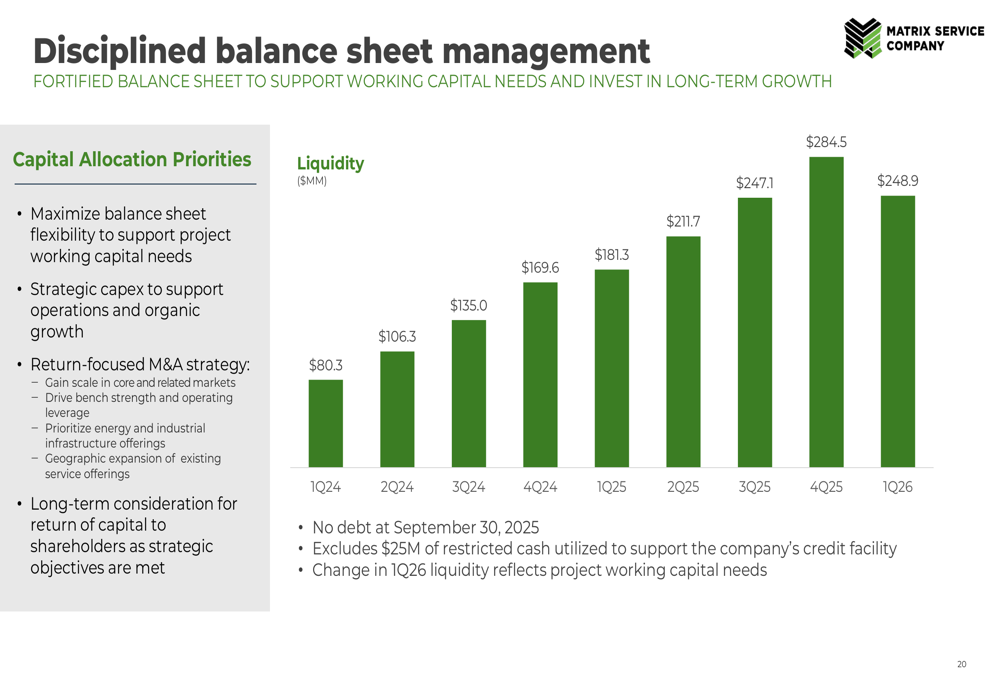

From a balance sheet perspective, Matrix Service maintains a strong financial position with $248.9 million in liquidity and no outstanding debt. This represents a significant improvement from $181.3 million in Q1 FY25, though it decreased slightly from $284.5 million in Q4 FY25 due to project working capital needs.

Investment Outlook

Matrix Service's Q1 FY26 results mark a significant improvement from its Q4 FY25 performance, where the company reported a disappointing $0.28 loss per share and saw its stock drop 15.58% following the announcement. The current quarter's results suggest the company is making progress on its turnaround strategy.

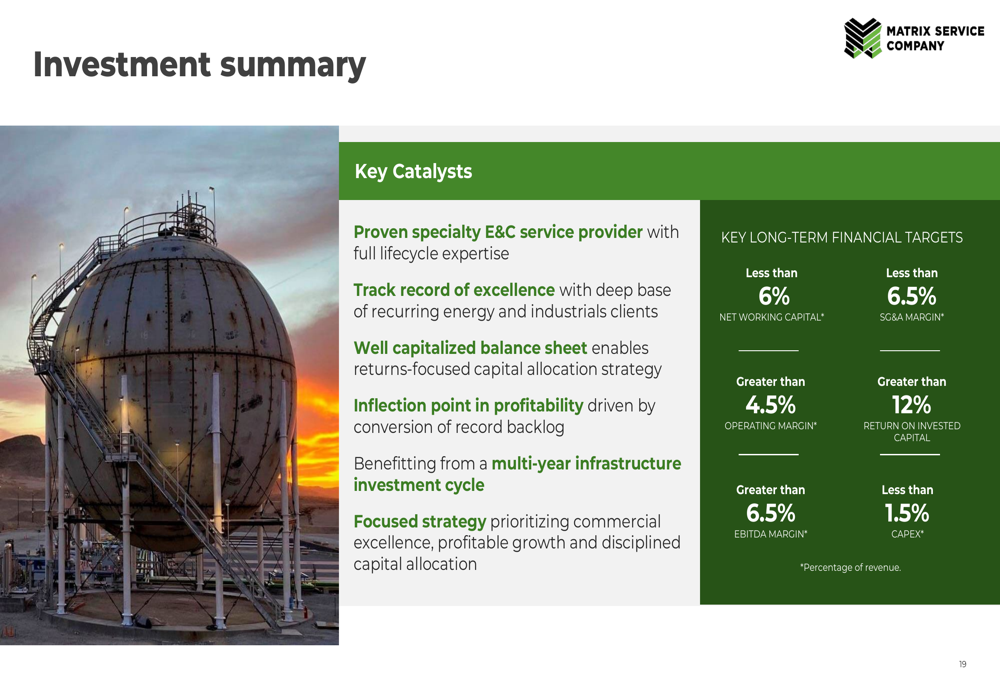

The company has established clear long-term financial targets, including gross margins in the 10-12% range, SG&A below 6.5% of revenue, operating margins above 4.5%, and return on invested capital exceeding 12%.

With approximately 90% recurring customer revenue and a strong balance sheet, Matrix Service appears well-positioned to capitalize on growing infrastructure investment across its target markets. However, investors should note that while the company has shown improvement, it still reported a net loss for the quarter, indicating that the path to consistent profitability remains a work in progress.

As Matrix Service continues executing its strategic framework focused on winning new projects, safe and reliable execution, and delivering sustainable performance, the coming quarters will be crucial in determining whether this positive momentum can be maintained and accelerated.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.