Stock market today: Stocks fall as investors rotate out of tech into Jackson Hole

Introduction & Market Context

Matrix Service Company (NASDAQ:MTRX) presented its Q3 FY25 results on May 8, 2025, highlighting significant revenue growth and a record backlog that positions the company for continued expansion. As a specialty engineering and construction company with over 40 years of experience, Matrix Service focuses on supporting energy and utility infrastructure customers across North America and select international markets.

The company operates in a favorable market environment with multi-industry tailwinds driving sustainable growth. These include increasing data center energy demand, low-cost feedstock availability, low-carbon infrastructure development, industrial and manufacturing resurgence, oil and gas demand, and grid reliability needs. Collectively, these sectors represent a total addressable market exceeding $2 trillion.

As shown in the following chart detailing the company’s multi-industry growth drivers:

Quarterly Performance Highlights

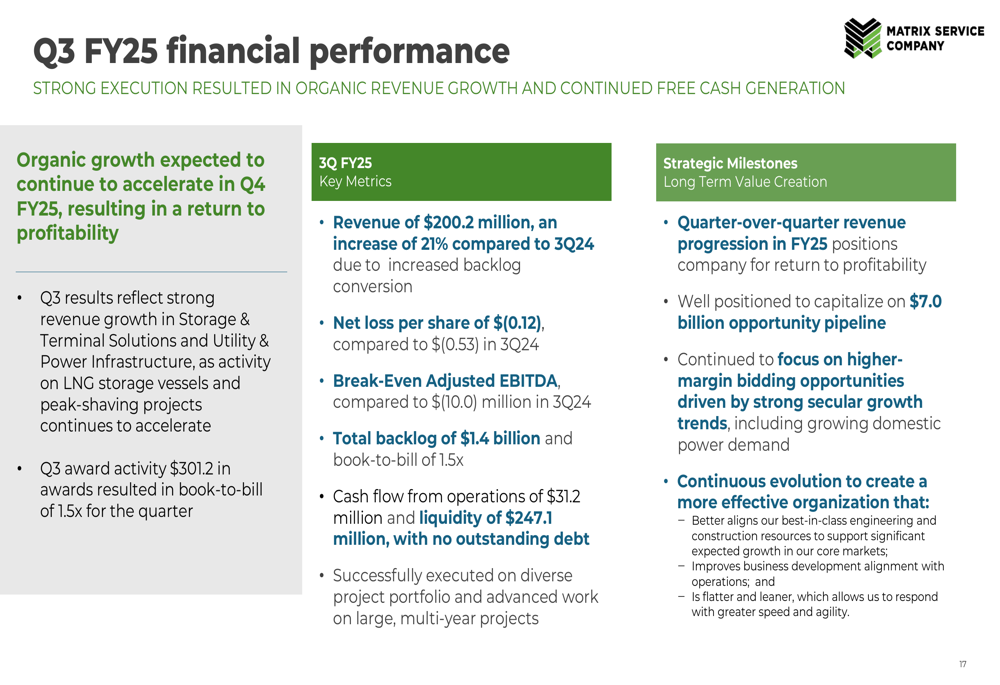

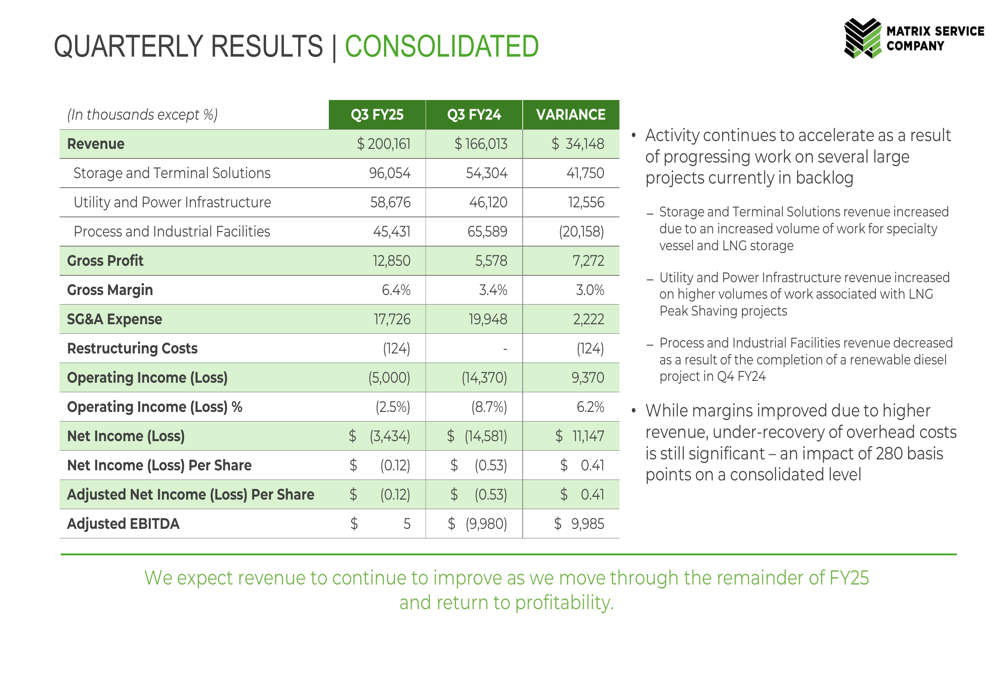

Matrix Service reported Q3 FY25 revenue of $200.2 million, representing a 21% increase compared to Q3 FY24. Despite this strong top-line growth, the company posted a net loss per share of $(0.12) and break-even Adjusted EBITDA. However, gross margin improved significantly to 6.4% in Q3 FY25 from 3.4% in the same period last year, indicating progress toward the company’s profitability goals.

The quarter also saw strong cash generation, with cash flow from operations reaching $31.2 million. The company maintained a robust liquidity position of $247.1 million with no outstanding debt, providing financial flexibility to support growth initiatives.

The following slide summarizes the key financial metrics for Q3 FY25:

A more detailed breakdown of the quarterly results shows improvement across several key metrics:

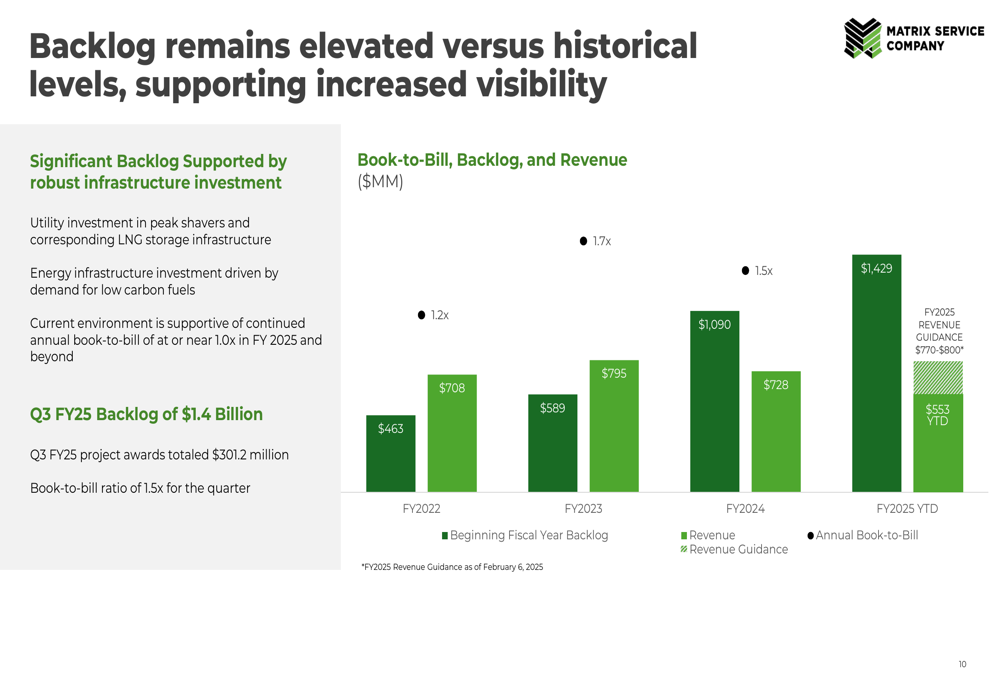

Backlog and Revenue Visibility

One of the most significant highlights from the presentation was Matrix Service’s record backlog of $1.4 billion, which provides multi-year visibility for profitable growth. The company has achieved consistent backlog growth with book-to-bill ratios exceeding 1.0x for three consecutive fiscal years: 1.2x in FY2022, 1.7x in FY2023, and 1.5x in FY2024.

This strong backlog is supported by robust infrastructure investment, particularly in utility investments for peak shavers and corresponding LNG storage infrastructure, as well as energy infrastructure investments driven by demand for low-carbon fuels. Management expects the current environment to support continued annual book-to-bill ratios at or near 1.0x in FY2025 and beyond.

The following chart illustrates the company’s backlog and revenue trends:

Beyond the current backlog, Matrix Service has identified an opportunity pipeline of approximately $7.0 billion as of March 31, 2025. This pipeline is heavily weighted toward the Storage & Terminal Solutions segment (60%), followed by Process & Industrial Facilities (23%) and Utility & Power Infrastructure (17%).

Strategic Initiatives

Matrix Service is implementing a strategic roadmap focused on profitable growth and execution excellence. The company’s value creation framework centers on three key components: winning market share in existing and high-value end markets, executing projects safely and efficiently, and delivering commercial, operational, and financial excellence.

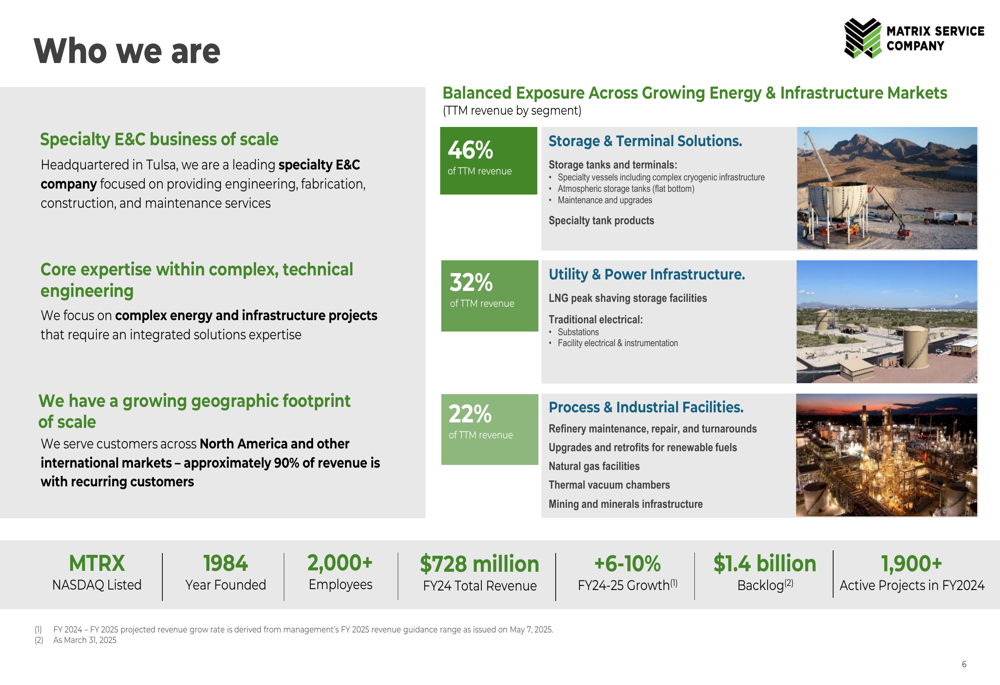

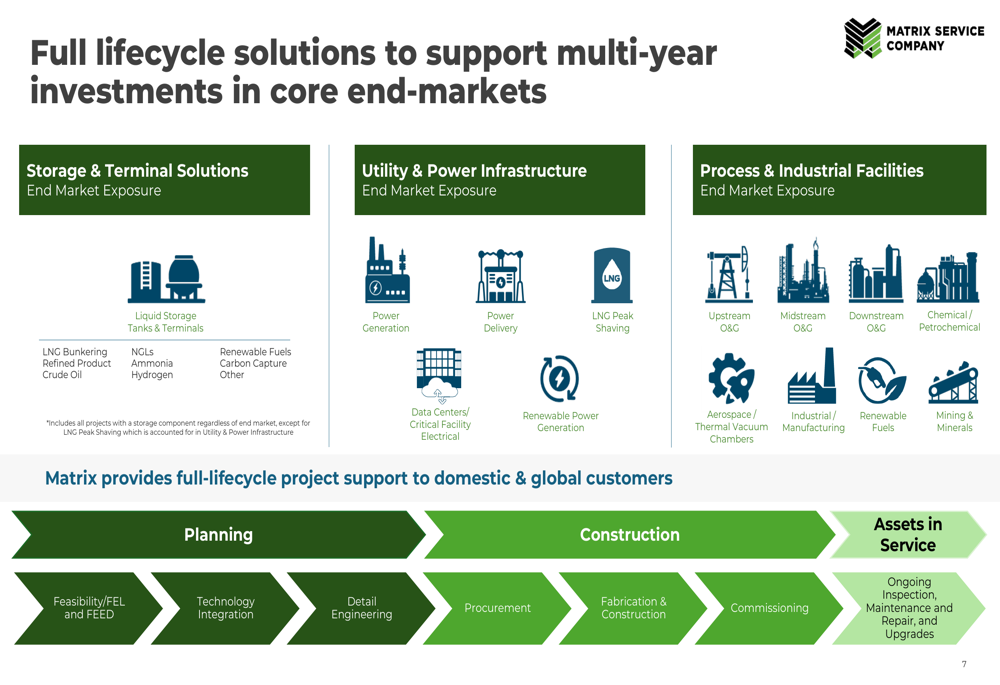

The company provides full lifecycle solutions across its three business segments: Storage & Terminal Solutions (46% of TTM revenue), Utility & Power Infrastructure (32%), and Process & Industrial Facilities (22%). These solutions span from planning and feasibility studies through construction, commissioning, and ongoing maintenance and repairs.

As illustrated in the following overview of the company’s capabilities and market exposure:

Matrix Service’s full lifecycle approach enables it to support customers throughout their infrastructure investments:

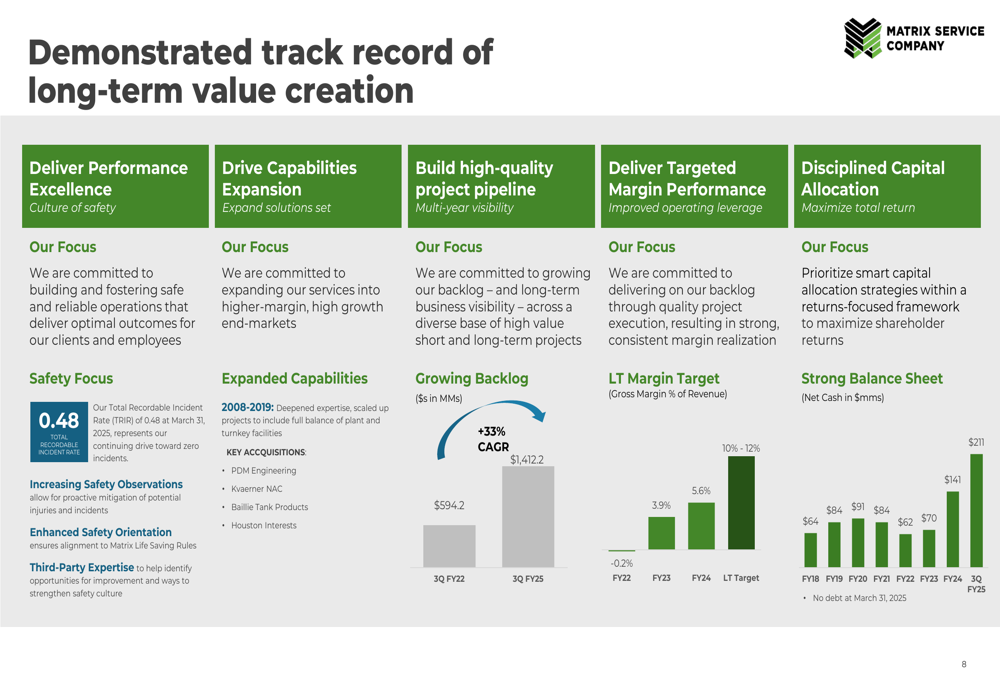

The company has demonstrated a track record of long-term value creation through performance excellence, capabilities expansion, high-quality project pipeline development, targeted margin performance, and disciplined capital allocation. Notably, Matrix Service has achieved a 33% CAGR in backlog from Q3 FY22 to Q3 FY25 while maintaining a strong balance sheet with no debt.

Forward-Looking Statements

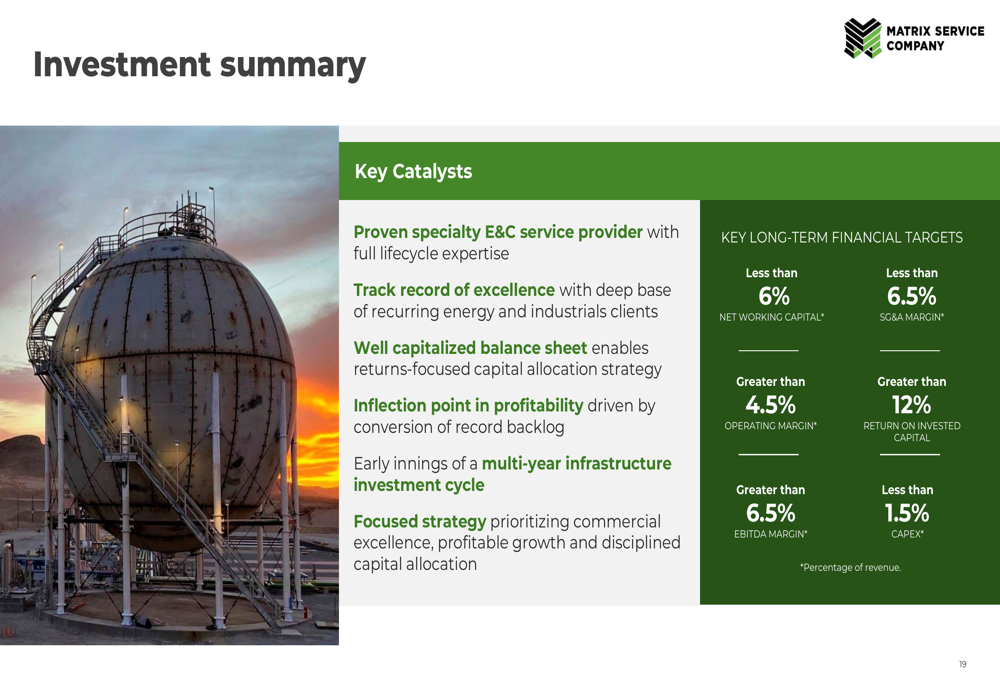

Looking ahead, Matrix Service has established clear long-term financial targets, including:

- Net working capital less than 6% of revenue

- Operating margin greater than 4.5% of revenue

- EBITDA margin greater than 6.5% of revenue

- SG&A margin less than 6.5% of revenue

- Return on invested capital greater than 12%

- CAPEX less than 1.5% of revenue

The company reaffirmed its FY25 revenue guidance of $770-$800 million, which represents continued growth from FY24 revenue of $708 million. Management believes Matrix Service is at an inflection point in profitability, driven by the conversion of its record backlog into revenue.

The investment thesis for Matrix Service centers on its proven specialty E&C service capabilities, track record of excellence with recurring clients, well-capitalized balance sheet, and positioning to benefit from the early stages of a multi-year infrastructure investment cycle.

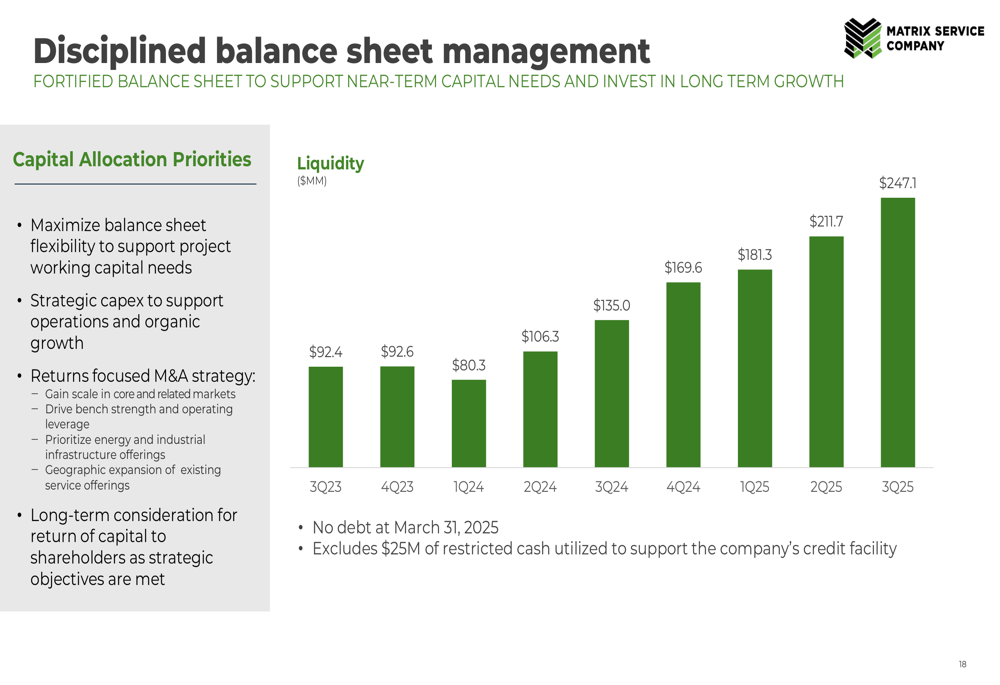

With its disciplined balance sheet management approach, Matrix Service is focused on maximizing financial flexibility to support near-term capital needs and invest in long-term growth. The company’s liquidity has steadily increased over the past two years, reaching nearly $250 million by Q3 FY25, with no debt outstanding.

As Matrix Service continues to execute its strategic roadmap, the company appears well-positioned to capitalize on the growing demand for energy and utility infrastructure services, potentially delivering improved profitability and shareholder returns in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.