Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Mattel Inc . (NASDAQ:MAT) presented its second quarter 2025 earnings results on July 23, 2025, revealing a mixed performance characterized by declining sales but improved profit margins. The toy maker reported that while net sales fell 6% year-over-year, adjusted gross margin expanded by 200 basis points to 51.2%. Following the earnings release, Mattel’s stock rose 1.56% in aftermarket trading to $20.06, suggesting investors were encouraged by the company’s ability to maintain profitability despite revenue challenges.

The presentation highlighted that the global toy industry continued to grow through June 2025 according to Circana data, with Mattel’s point-of-sale (POS) metrics increasing in all regions during both Q2 and the first half of the year. However, the company faced headwinds in the U.S. market, which it attributed to "global trade dynamics" – likely referring to tariff impacts.

Quarterly Performance Highlights

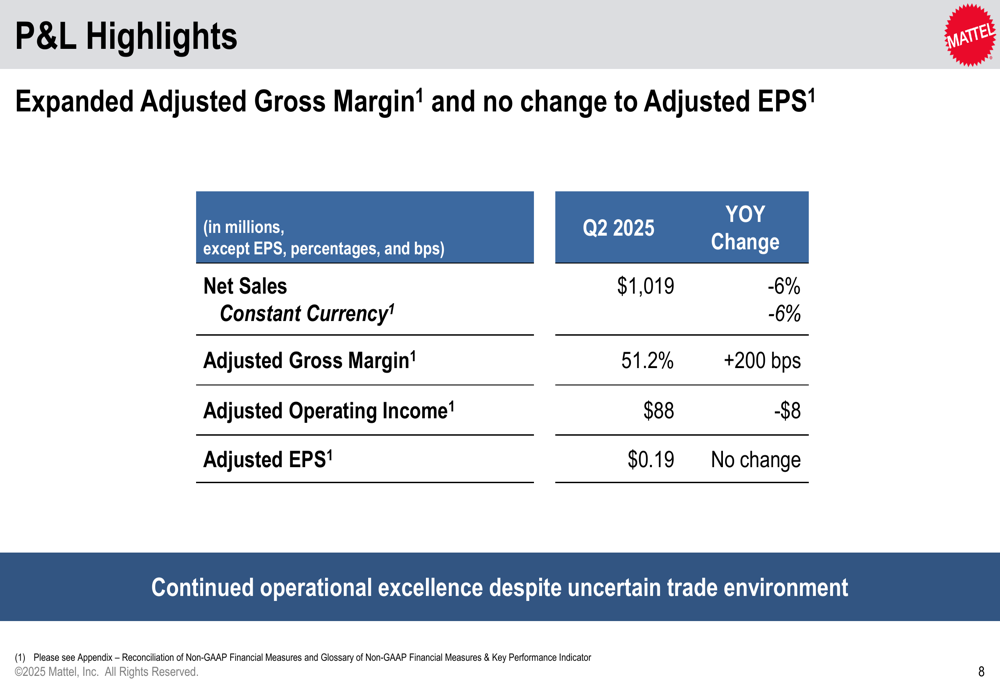

Mattel reported Q2 2025 net sales of $1.019 billion, representing a 6% decline both as reported and in constant currency compared to the same period last year. Despite this top-line pressure, the company maintained its adjusted earnings per share at $0.19, unchanged from Q2 2024, exceeding analyst expectations of $0.16 per share.

As shown in the following financial highlights slide, the company achieved adjusted gross margin expansion while maintaining stable EPS despite sales challenges:

The company’s adjusted operating income was $88 million, down $8 million from the prior year, while adjusted EBITDA remained nearly flat at $170 million, just $1 million below Q2 2024. These results reflect Mattel’s focus on operational efficiency and cost management in a challenging environment.

Geographic and Category Performance

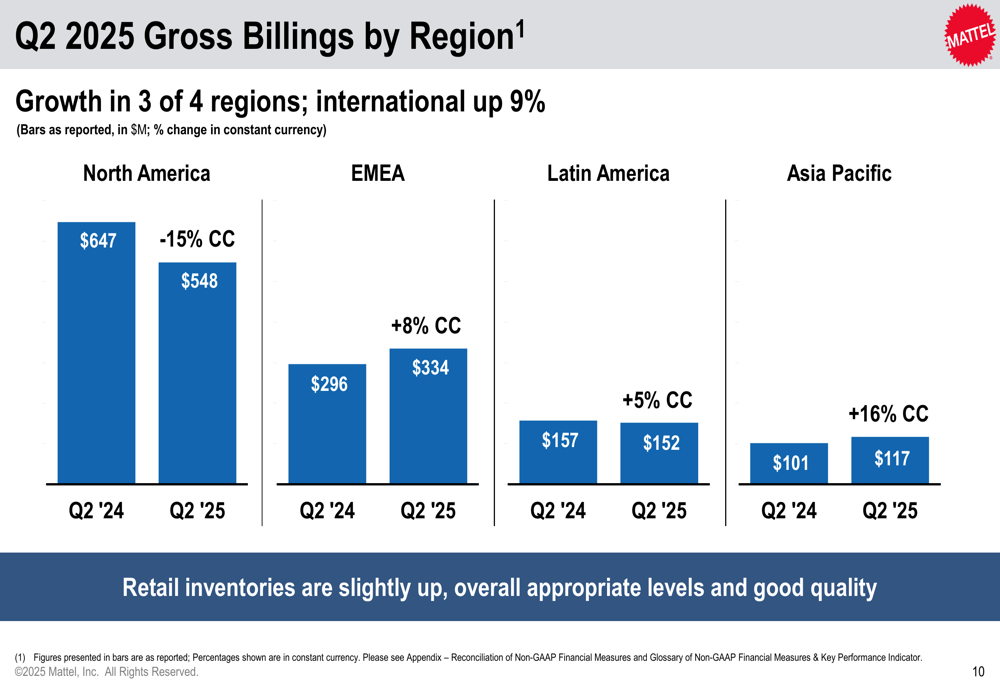

Mattel’s international business showed strong momentum, with overall international gross billings increasing 9% in constant currency. This growth helped offset a significant 15% decline in North America, which the company attributed to global trade dynamics affecting the U.S. market.

The following chart illustrates the regional performance divergence, with growth in three of four regions:

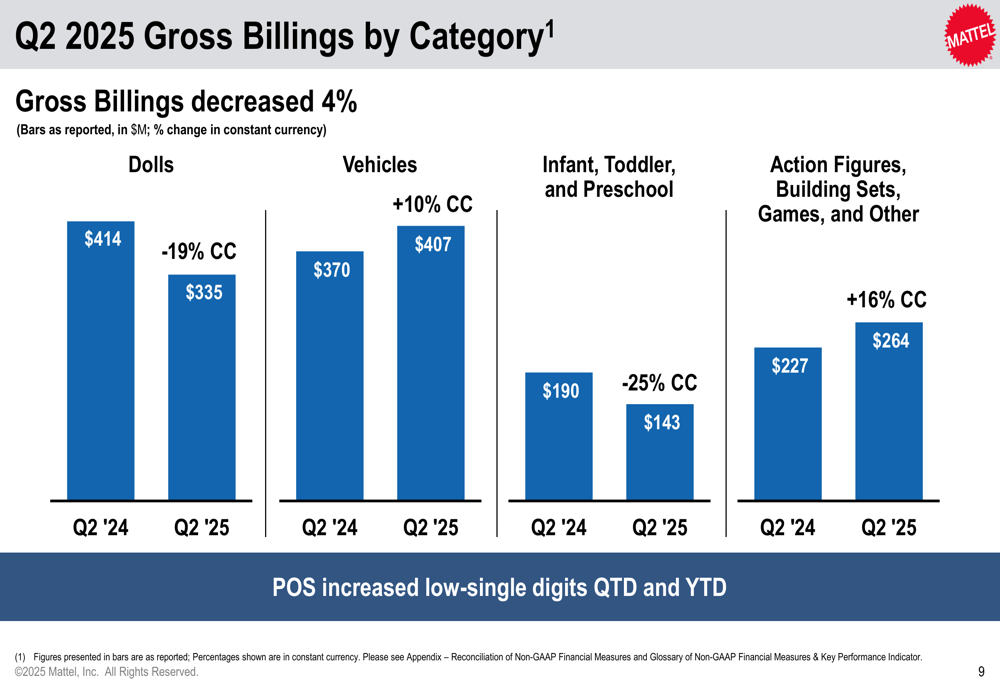

Product category performance was similarly mixed. The Vehicles category, led by Hot Wheels, delivered 10% growth in constant currency. Action (WA:ACT) Figures, Building Sets, Games, and Other grew an impressive 16%, benefiting from strong performance in tentpole movie properties and evergreen brands. However, the Dolls category, which includes Barbie, declined 19%, while the Infant, Toddler, and Preschool category fell 25%, with Fisher-Price particularly impacted by U.S. market challenges.

The following chart breaks down gross billings by product category:

The company noted that it is exiting certain Baby Gear lines and Power Wheels products, likely contributing to the decline in the Infant, Toddler, and Preschool category.

Margin Expansion and Cost Management

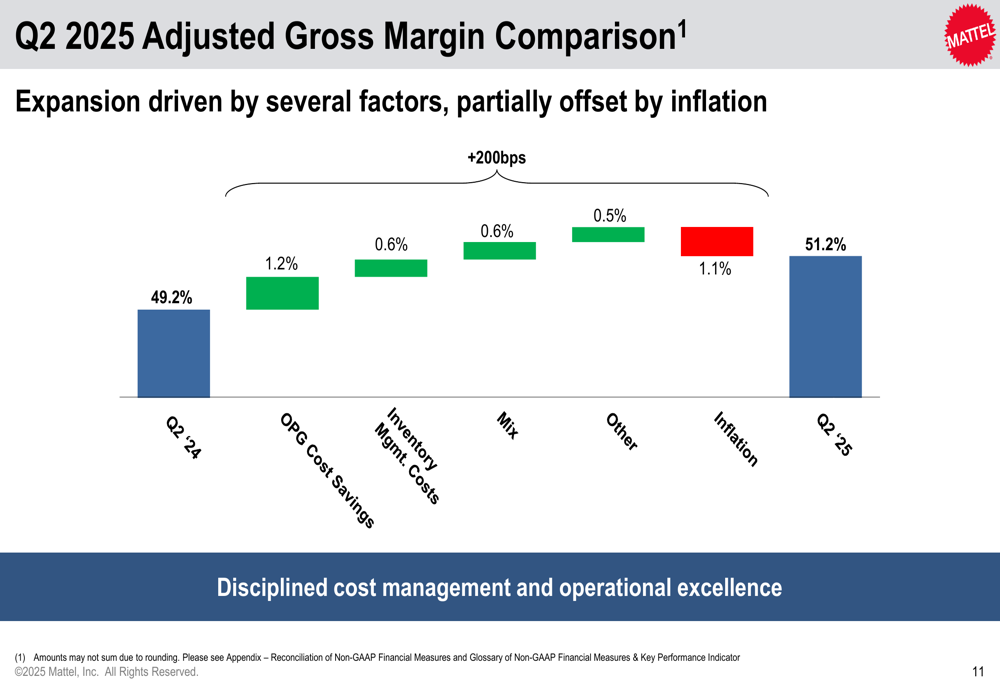

A key bright spot in Mattel’s Q2 results was the 200 basis point expansion in adjusted gross margin to 51.2%. This improvement came despite inflationary pressures, highlighting the company’s effective cost management.

The following waterfall chart breaks down the factors contributing to margin expansion:

Mattel’s "Optimizing for Profitable Growth" (OPG) program delivered $23 million in savings during Q2 and $42 million year-to-date. Since launching the program in 2024, the company has achieved $126 million in cumulative savings and remains on track to reach its target of $200 million by 2026.

The company also strengthened its balance sheet, increasing its cash position to $870 million from $722 million in Q2 2024, while maintaining a healthy leverage ratio of 2.2x (down from 2.3x). Mattel repurchased $50 million worth of shares during the quarter and $210 million year-to-date, demonstrating confidence in its long-term prospects.

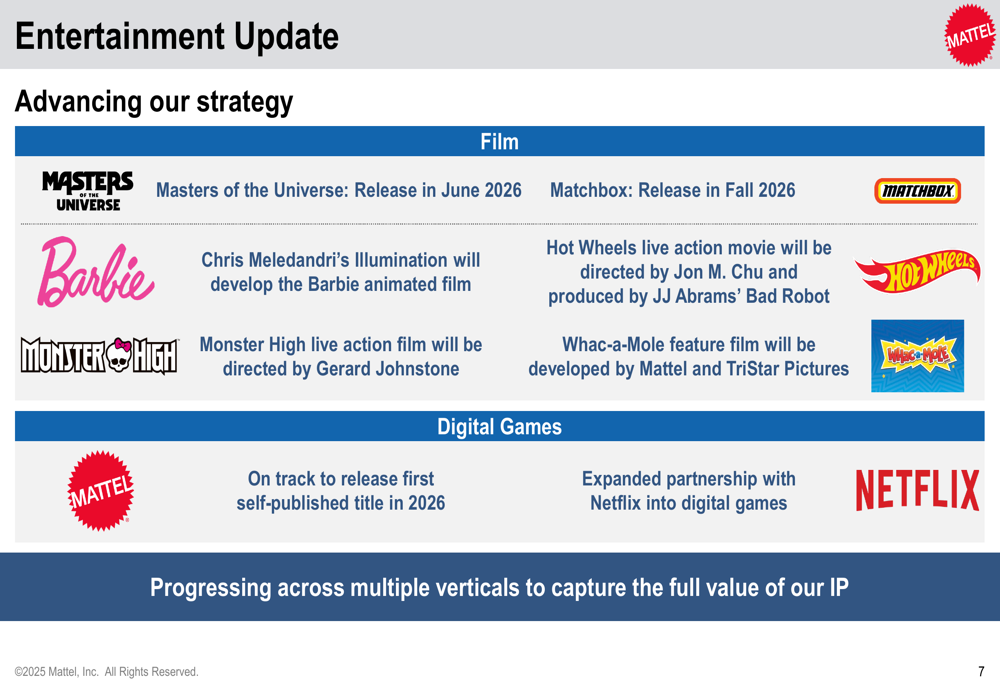

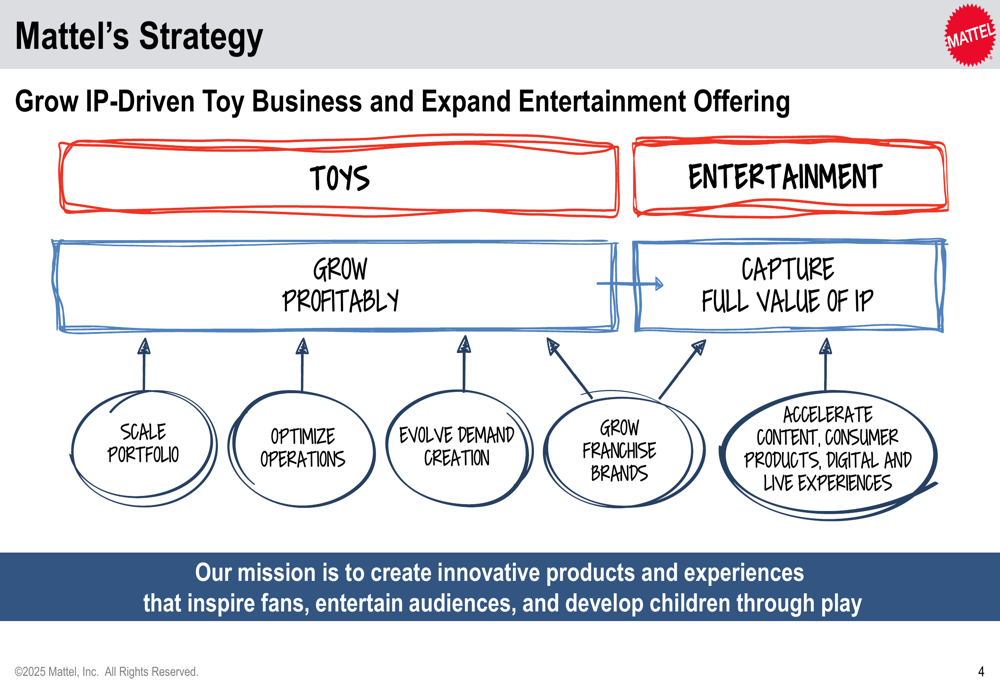

Entertainment and Digital Strategy

Mattel continued to advance its strategy of expanding beyond traditional toys into entertainment and digital gaming. The presentation highlighted significant progress in developing film projects based on the company’s iconic brands.

As shown in the following entertainment update slide, Mattel has secured impressive partnerships for upcoming films:

Key entertainment initiatives include a Masters of the Universe film slated for June 2026, a Matchbox movie for Fall 2026, and partnerships with major studios and directors. Chris Meledandri’s Illumination will develop an animated Barbie film, while Jon M. Chu will direct a Hot Wheels live action movie produced by JJ Abrams’ Bad Robot. The company is also expanding into digital gaming, with plans to release its first self-published title in 2026 and an expanded partnership with Netflix (NASDAQ:NFLX).

This entertainment push aligns with Mattel’s broader strategy to capture the full value of its intellectual property beyond traditional toy sales:

The company is also embracing new technologies, including artificial intelligence, to develop innovative products and experiences based on its brands.

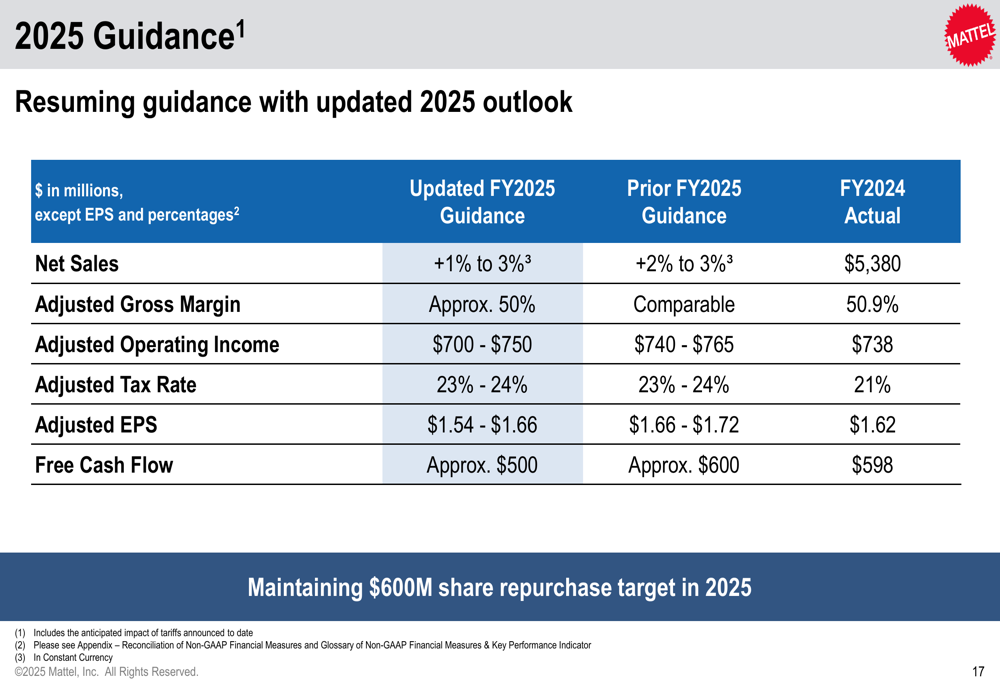

Updated 2025 Guidance

In light of its Q2 performance, Mattel updated its full-year 2025 guidance. The company now expects net sales growth of 1% to 3%, down slightly from its previous forecast of 2% to 3%. Adjusted EPS guidance was revised to $1.54-$1.66, compared to the prior range of $1.66-$1.72.

The following slide details the revised outlook across key metrics:

Despite the modest downward revision, Mattel maintained its target of $600 million in share repurchases for 2025, signaling continued confidence in its long-term strategy and financial position.

Executive Commentary

Ynon Kreiz, Mattel’s Chairman and CEO, emphasized the company’s operational excellence and strategic execution in his closing remarks:

"Our second quarter performance reflects operational excellence in the current macroeconomic environment as we continue to execute our strategy to grow Mattel’s IP-driven toy business and expand our entertainment offering. We achieved meaningful gross margin expansion, grew internationally, and further progressed our entertainment slate. We are embracing technology and collaborating with world-class partners to bring our iconic brands to life in new ways to position Mattel for long-term success."

The executive’s comments highlight Mattel’s dual focus on operational efficiency and strategic growth initiatives, particularly in entertainment and digital, as the company navigates a challenging but evolving toy market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.