Asia FX muted, dollar fragile as CPI data boosts Sept rate cut bets

Introduction & Market Context

MaxCyte Inc. (NASDAQ:MXCT) presented its Strategic Platform License (SPL) portfolio overview on August 6, 2025, highlighting the company’s expanding partnerships in cell and gene therapy. The presentation comes amid challenging market conditions for the biotech sector, with MaxCyte’s stock trading at $2.06, down 36% year-to-date and near its 52-week low of $1.965, despite beating revenue expectations in its most recent quarterly results.

The company, which provides premier technology for ex vivo non-viral gene editing, emphasized its growing portfolio of partnerships and clinical programs as key drivers for future growth, even as current financial performance shows mixed results with core revenue growing only 1% year-over-year in Q1 2025.

SPL Portfolio Overview

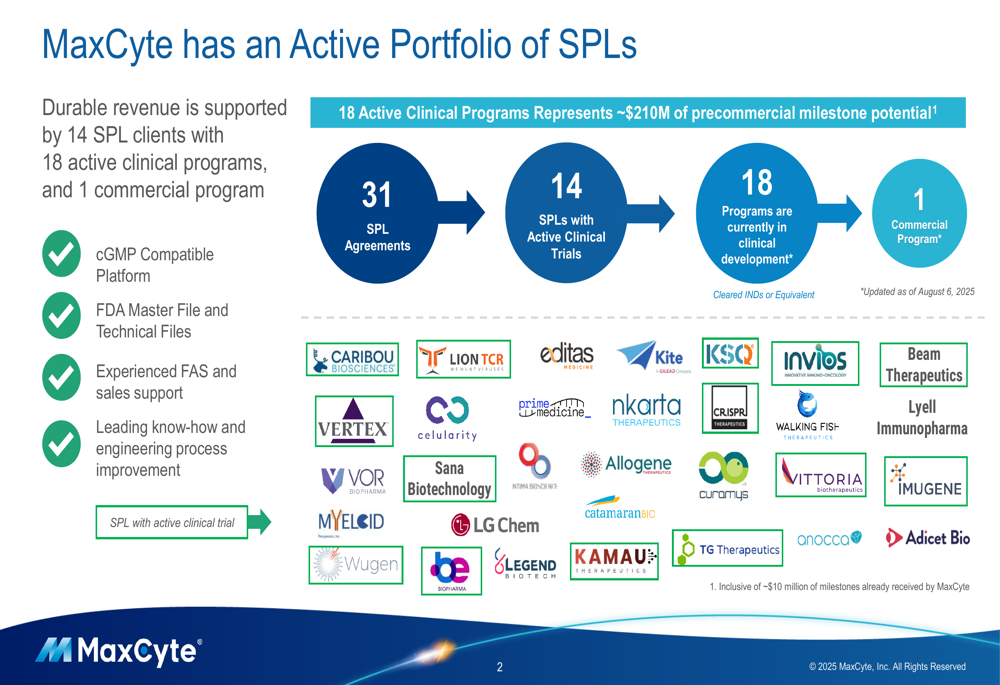

MaxCyte’s presentation highlighted its expanding portfolio of Strategic Platform Licenses, which now includes 14 SPL clients with 18 active clinical programs and one commercial program. The company has secured a total of 31 SPL agreements, providing a foundation for durable revenue through license fees, milestone payments, and potential royalties.

As shown in the following portfolio overview, MaxCyte’s platform offers CGMP compatibility, FDA Master File and Technical Files, experienced support teams, and leading know-how in engineering process improvement:

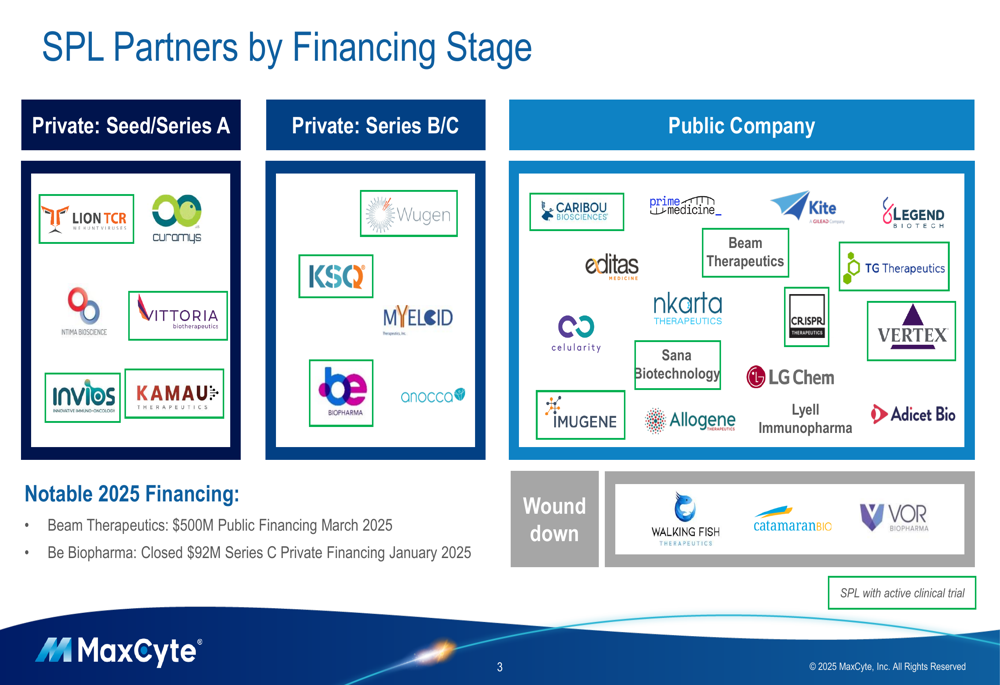

The company’s SPL partners span various financing stages, from early-stage private companies to established public corporations. Notable 2025 financing events among partners include Beam Therapeutics’ $500 million public financing in March 2025 and Be Biopharma’s $92 million Series C private financing in January 2025.

Clinical Pipeline and Therapeutic Areas

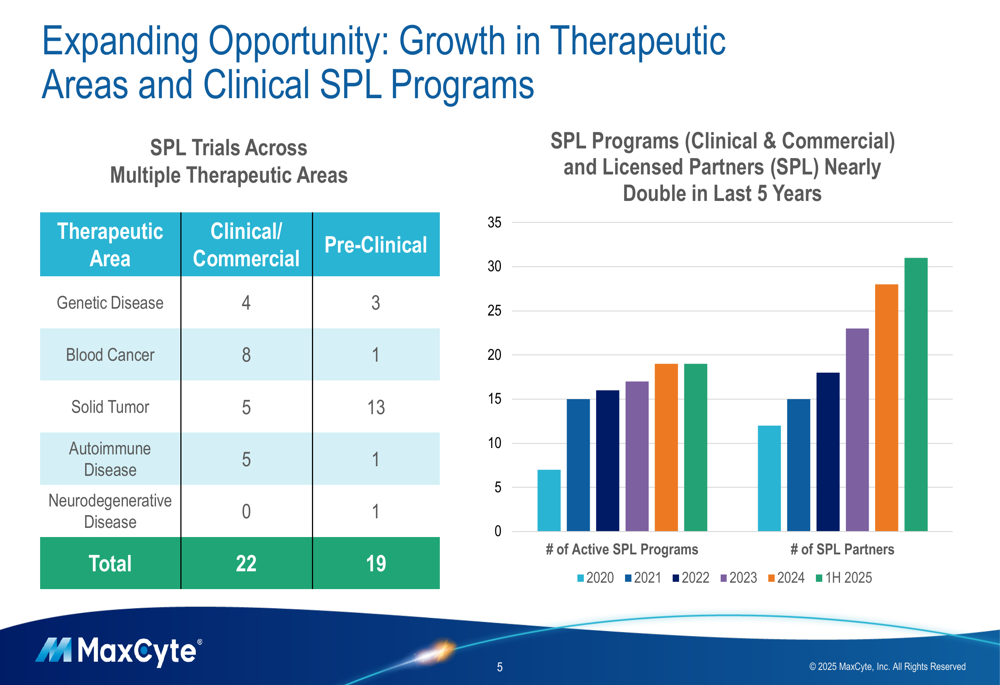

MaxCyte’s clinical pipeline has shown significant expansion across multiple therapeutic areas. The company now supports 22 active clinical trials spanning genetic diseases, blood cancers, solid tumors, and autoimmune diseases. The presentation revealed that both SPL programs and licensed partners have nearly doubled over the past five years (2020 to 1H 2025).

The following chart illustrates the growth in therapeutic areas and clinical SPL programs:

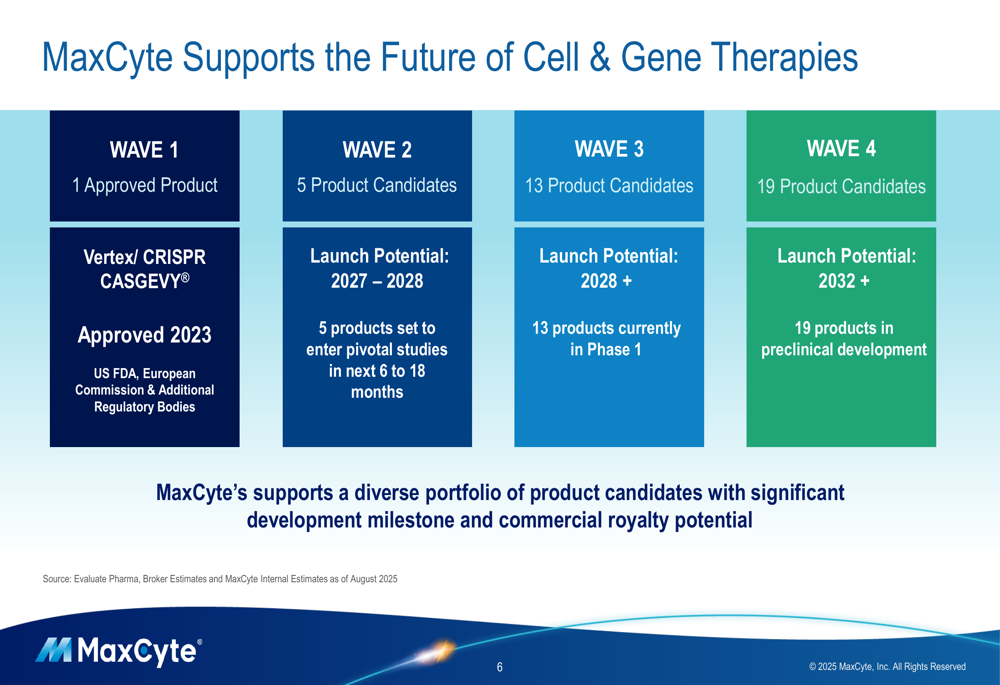

MaxCyte categorizes its product development pipeline into four "waves" of cell and gene therapies:

- Wave 1: One approved product (Vertex/CRISPR CASGEVY®, approved in 2023)

- Wave 2: Five product candidates with launch potential in 2027-2028

- Wave 3: Thirteen product candidates with launch potential in 2028 and beyond

- Wave 4: Nineteen product candidates in preclinical development with launch potential from 2032

The second wave of products, set to enter pivotal studies in the next 6-18 months, includes promising candidates targeting various hematologic malignancies. These candidates utilize different cell types and approaches, primarily focusing on T-cell therapies with both allogeneic and autologous approaches.

Revenue Model and Financial Performance

MaxCyte’s presentation outlined its revenue model for successful SPL programs, highlighting three key revenue streams: annual license fees of $0.25 million per GTx (genetic therapy), development and regulatory milestones averaging around $12 million, and potential royalty payments estimated at approximately $79 million for a successful program.

This forward-looking revenue model contrasts with the company’s current financial performance. In Q1 2025, MaxCyte reported revenue of $10.4 million, exceeding forecasts of $9.05 million, but still representing an 8% decline year-over-year. Core revenue showed modest growth of 1%, while the company reported an EPS of -$0.10, slightly better than the anticipated -$0.11.

The company maintains strong financial health with $174.7 million in cash and investments as of Q1 2025, and expects to end the year with approximately $160 million. Operating expenses have decreased to $21.2 million from $22.2 million year-over-year, indicating improved cost management.

Future Outlook and Challenges

MaxCyte’s presentation emphasized the long-term potential of its SPL portfolio, particularly highlighting the five product candidates expected to enter pivotal studies in the next 6-18 months. These candidates represent the "second wave" of potential commercial products following the success of Vertex/CRISPR’s CASGEVY®.

However, the company faces several challenges. Despite the positive outlook presented in the slides, MaxCyte’s stock has struggled, reflecting broader investor caution in the biotech sector. The company’s current revenue growth remains modest, with 2025 core revenue growth guidance of 8-15%, suggesting a significant gap between present performance and the ambitious future revenue projections from milestone payments and royalties.

CEO Maher Masud acknowledged these challenges in the Q1 earnings call, stating, "We are navigating a dynamic and evolving macro environment and remain on track to deliver on our 2025 goals." The company’s ability to convert its expanding SPL portfolio into sustainable revenue growth will be crucial for improving investor sentiment and stock performance in the coming quarters.

While MaxCyte’s presentation paints an optimistic picture of its long-term potential in the cell and gene therapy market, the company must navigate near-term market challenges and demonstrate progress in moving its partners’ programs through clinical development to realize the projected milestone and royalty revenues that form the core of its business model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.