Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

mBank SA (WSE:MBK) released its Q1 2025 financial results on April 30, 2025, highlighting continued positive trends across key performance indicators. The Polish banking group reported accelerating loan portfolio growth, maintained strong revenues, and significantly reduced legal provisions related to foreign exchange loans.

The presentation comes amid a stabilizing macroeconomic environment in Poland, characterized by steady consumption, low unemployment, and expectations for declining inflation throughout 2025. The bank also received credit rating upgrades from all three major agencies, reflecting improved profitability, solvency, and reduced legal risks.

Quarterly Performance Highlights

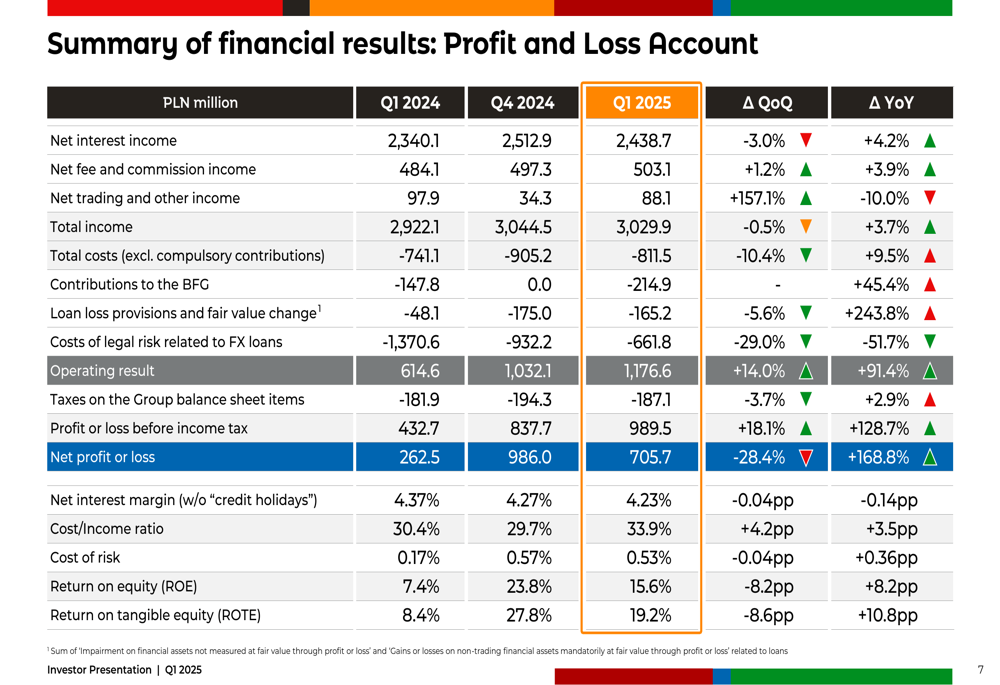

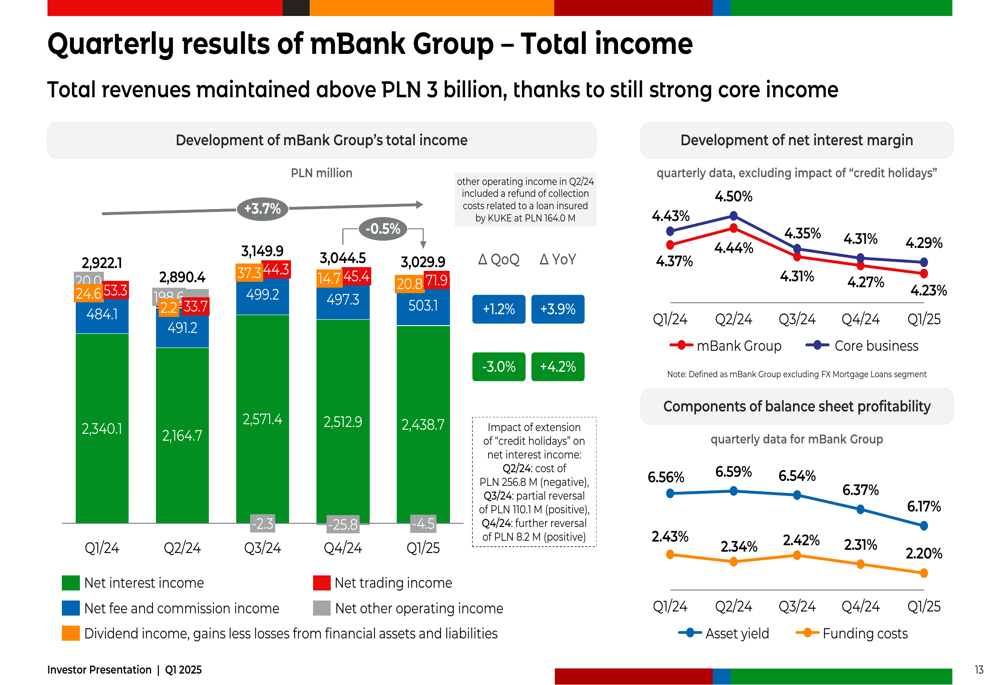

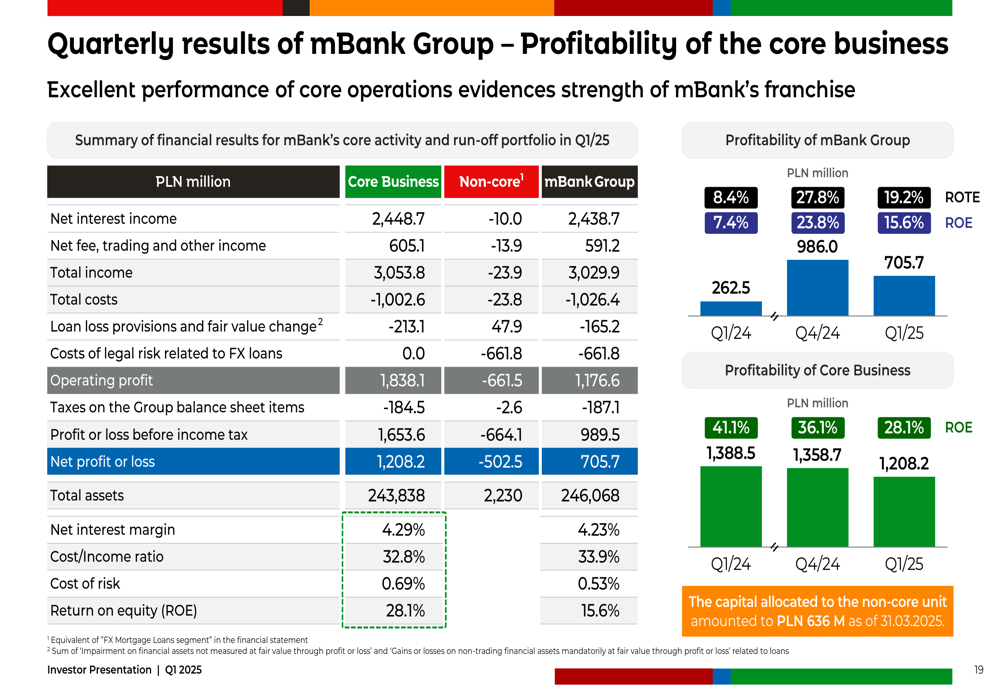

mBank reported a net profit of PLN 705.7 million for Q1 2025, a substantial increase from PLN 262.5 million in Q1 2024. The bank’s core business demonstrated strong performance with total revenues maintained above PLN 3 billion, reaching PLN 3,029.9 million, up 3.7% year-over-year.

As shown in the following summary of financial results, the bank achieved a return on equity (ROE) of 15.6%, more than doubling from 7.4% in the same period last year, while return on tangible equity (ROTE) improved to 19.2% from 8.4% in Q1 2024:

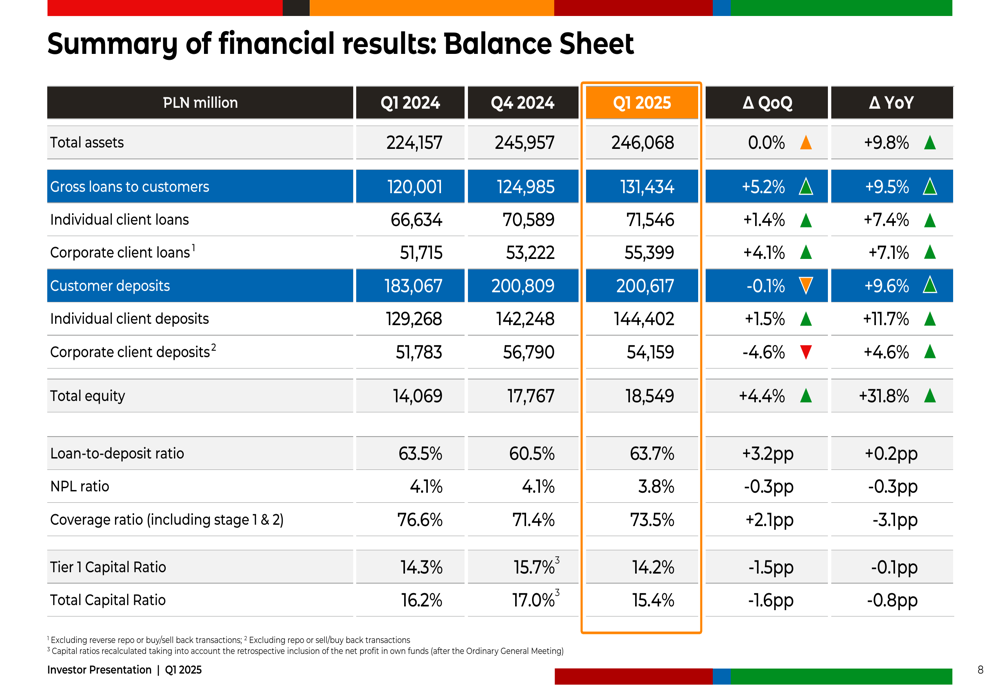

The bank’s balance sheet continued to strengthen, with total assets reaching PLN 246,068 million, up from PLN 224,157 million in Q1 2024. Gross loans to customers increased to PLN 131,434 million, while customer deposits remained stable at PLN 200,617 million:

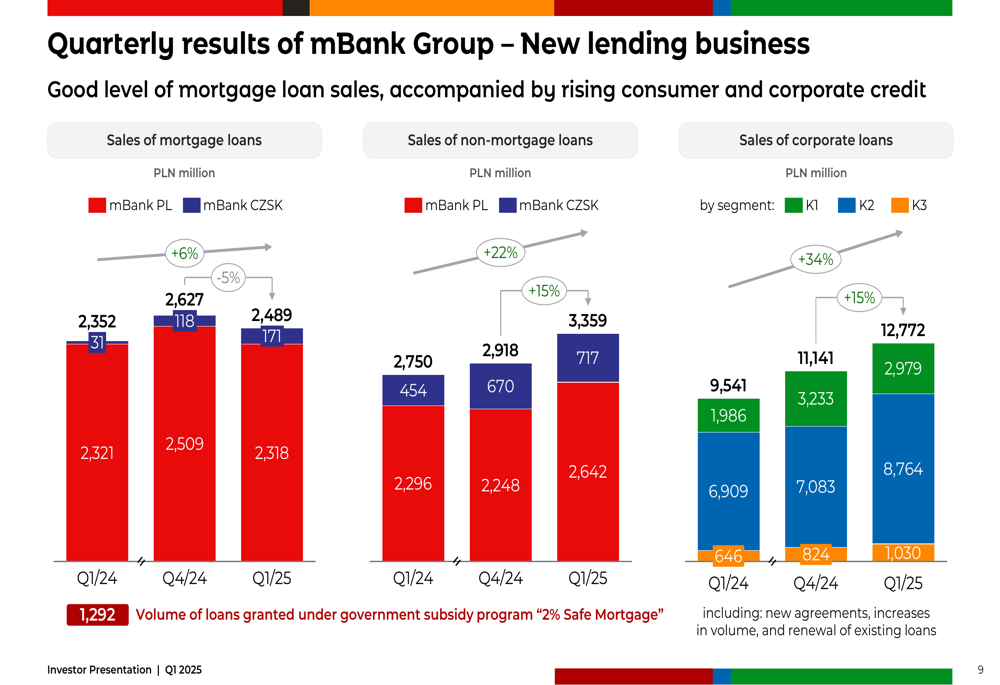

A key driver of mBank’s performance was the accelerating growth in its loan portfolio, which increased by 9.0% year-over-year. The presentation highlighted strong new lending activity across mortgage, non-mortgage, and corporate segments:

Detailed Financial Analysis

mBank maintained its total income above PLN 3 billion in Q1 2025, supported by strong core income despite a slight decrease in net interest margin to 4.23% from 4.37% in Q1 2024:

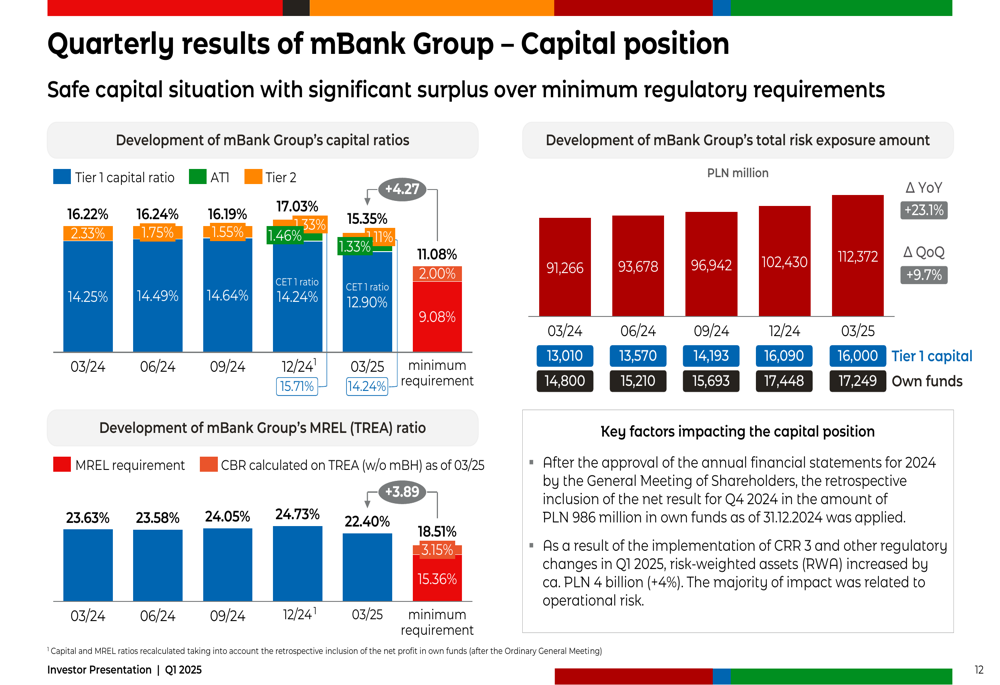

The bank’s capital position remained solid, with a Tier 1 Capital Ratio of 14.24% as of March 2025, though slightly down from 15.71% at the end of 2024. The implementation of CRR3 and other regulatory changes in Q1 2025 increased risk-weighted assets by approximately PLN 4 billion (+4%), primarily related to operational risk:

Operating costs increased marginally to PLN 919.3 million in Q1 2025 from PLN 888.9 million in Q1 2024, while the normalized cost/income ratio rose to 29.1% from 26.6% a year earlier. Despite this increase, mBank maintained its position as one of the most efficient banks in Poland.

The bank’s loan portfolio quality continued to improve, with the NPL ratio decreasing to 3.8% in Q1 2025 from 4.1% in Q1 2024, reflecting prudent risk management and favorable economic conditions.

Strategic Initiatives and Risk Management

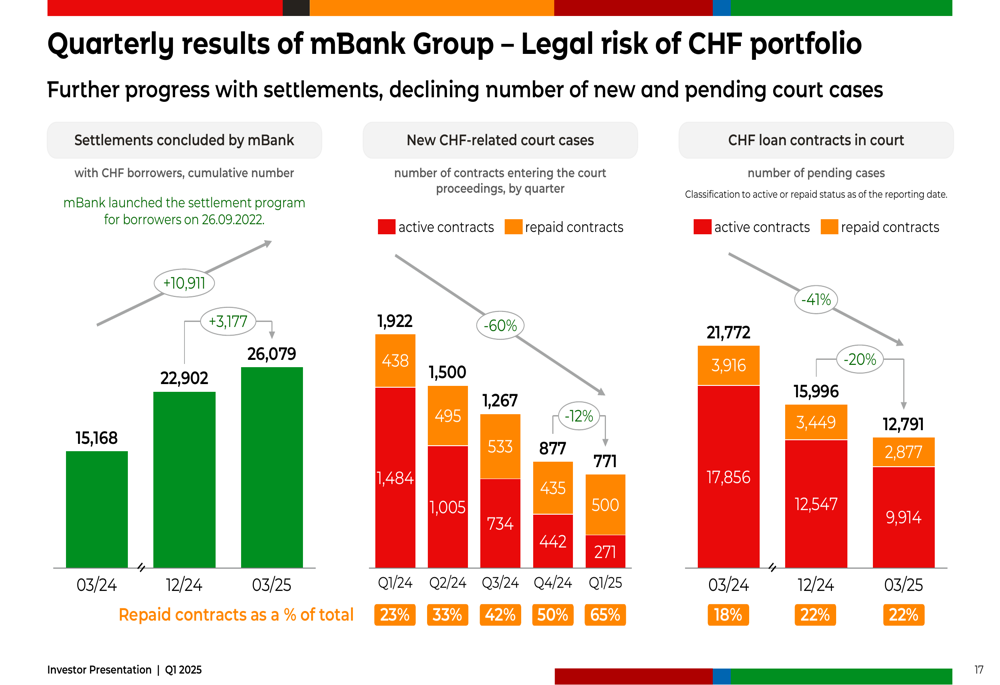

A significant development for mBank has been the progress in resolving legal risks associated with its Swiss franc (CHF) mortgage portfolio. The costs of legal risk related to FX loans decreased by 52%, falling to PLN 662 million in Q1 2025 from PLN 1,371 million in Q1 2024.

The bank has substantially increased settlements with CHF loan borrowers, with the number of settlements rising to 26,079 by March 2025, while the number of active contracts continued to decline:

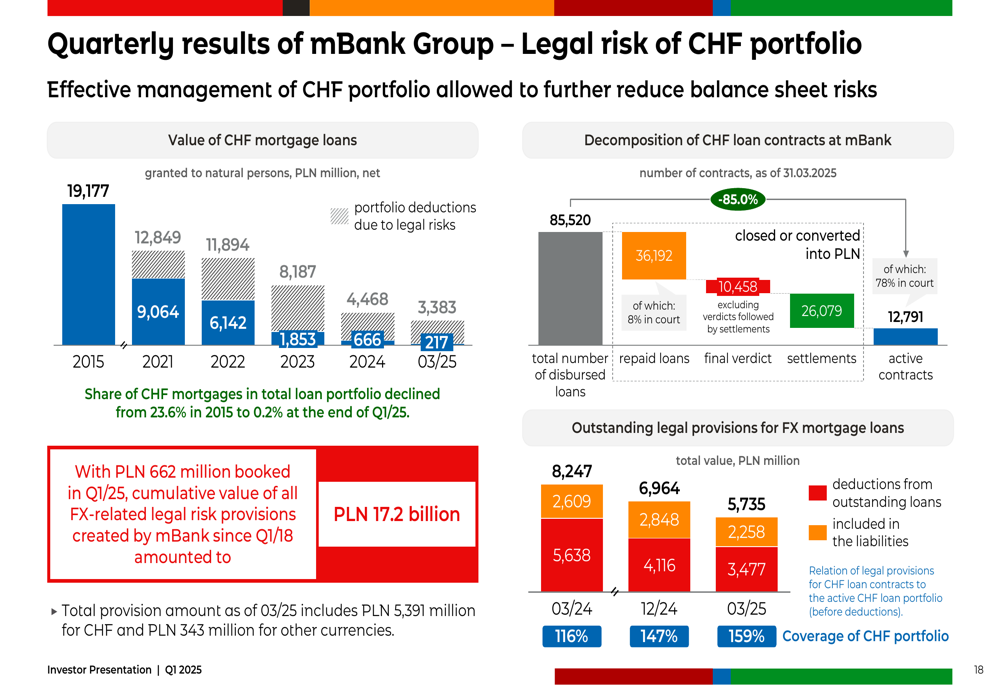

The share of CHF mortgages in mBank’s total loan portfolio has dramatically decreased from 23.6% in 2015 to just 0.2% at the end of Q1 2025, with legal provisions for CHF loan contracts now representing 159% of the active CHF loan portfolio:

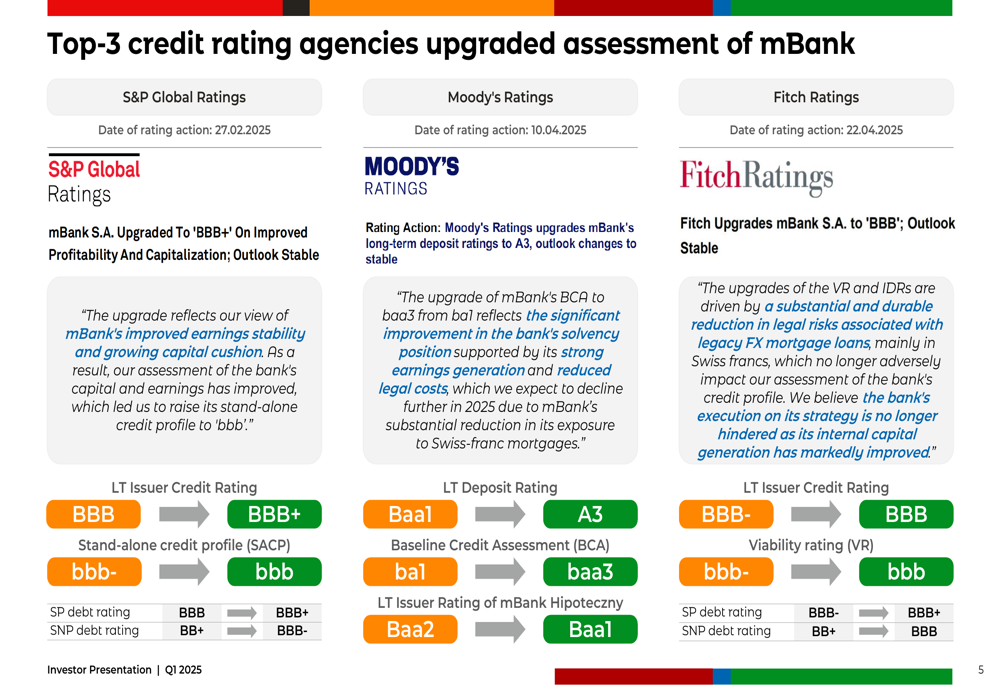

This progress in addressing legacy issues has contributed to credit rating upgrades from all three major agencies. S&P Global Ratings upgraded mBank to ’BBB+’ on February 27, 2025, Moody’s Ratings issued an upgrade on April 10, 2025, and Fitch Ratings upgraded the bank to ’BBB’ on April 22, 2025:

Forward-Looking Statements

Looking ahead, mBank expects to maintain its strong performance throughout 2025. The bank anticipates continued growth in its loan portfolio, particularly in the corporate segment, and stable total revenues. Management also projects further reductions in legal risk costs associated with the CHF portfolio.

The bank’s profitability metrics demonstrate the strength of its core business, with normalized ROE expected to remain in the mid-teens range:

mBank’s outlook is supported by favorable macroeconomic forecasts for Poland, including expected GDP growth of 3.0% in 2025, investment growth of 9.8%, and continued expansion of the banking sector with corporate loans projected to increase by 4.9% and household loans by 2.9%.

The bank remains committed to its ESG strategy, which includes transforming its loan portfolio to reach net-zero by 2050 and providing PLN 10 billion in green financing by the end of 2025.

In conclusion, mBank’s Q1 2025 results reflect a financial institution that has successfully navigated past challenges and is now positioned for sustainable growth, with improving asset quality, strong capital ratios, and reduced legal risks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.