S&P 500 hits a fresh record high on stronger economic growth, Nvidia pares losses

Introduction & Market Context

mBank SA (WSE:MBK) presented its second quarter 2025 results on July 31, showcasing significant profit growth and accelerated business expansion amid a favorable Polish economic environment. The bank reported substantial increases in both loan portfolio and deposit base, each growing by approximately 10% year-over-year, while simultaneously reducing its exposure to Swiss franc mortgage loans.

Poland’s macroeconomic outlook remains positive, with GDP growth projected to reach 3.8% in 2025, supported by increasing private consumption and investment. Inflation is expected to decline to 2.6% by year-end, creating a stable environment for banking operations.

Quarterly Performance Highlights

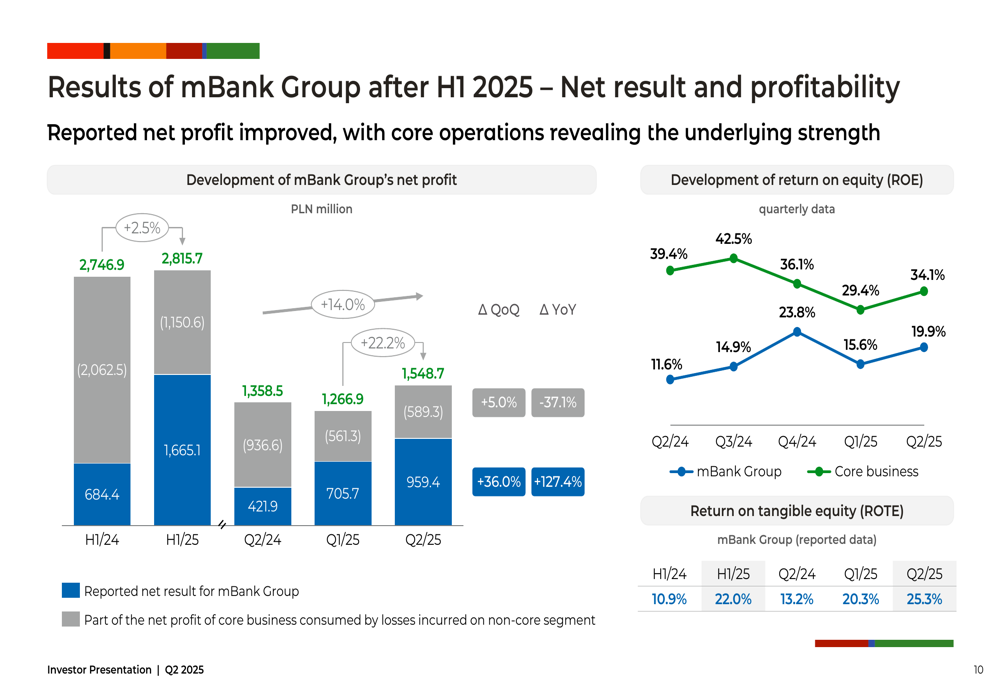

mBank reported a net profit of PLN 959.4 million for Q2 2025, a significant increase from PLN 705.7 million in Q1 2025 and more than double the PLN 421.9 million recorded in Q2 2024. For the first half of 2025, the bank’s total net profit reached PLN 1,665.1 million, compared to PLN 684.4 million in H1 2024.

The bank’s profitability metrics showed impressive results, with Return on Equity reaching 29.4% in Q2 2025 for the Group, while the core business achieved 19.9%. The Cost/Income ratio remained excellent at 28.2% in Q2 2025, demonstrating the bank’s operational efficiency.

As shown in the following chart of net profit and return on equity development:

Total (EPA:TTEF) income for H1 2025 reached PLN 6,202.6 million, with net interest income contributing PLN 4,936.0 million and net fee and commission income adding PLN 1,085.2 million. The bank’s net interest margin stood at 4.16% in Q2 2025, showing a slight decline from 4.27% in Q1 2025 but remaining well above the bank’s strategic target of 3.0%.

Loan and Deposit Growth

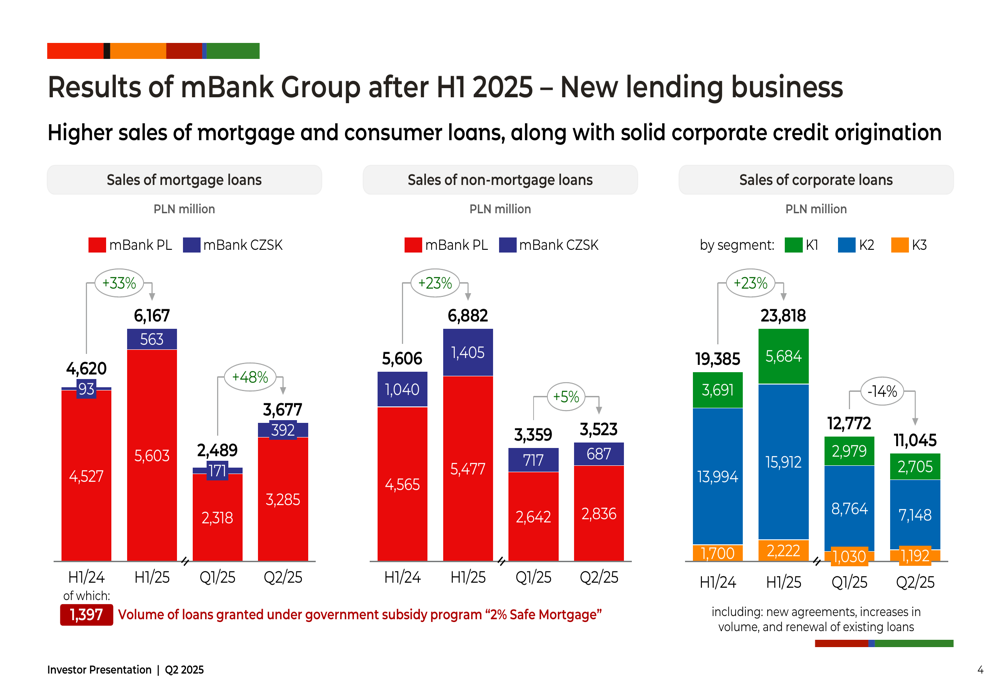

mBank demonstrated strong growth in its lending business across all segments. Mortgage loan sales in Poland reached PLN 3,677 million in Q2 2025, up from PLN 2,489 million in Q1 2025. Corporate loan sales were particularly impressive at PLN 12,772 million in Q2 2025, more than doubling from PLN 5,684 million in Q1 2025.

The following chart illustrates the bank’s new lending business results:

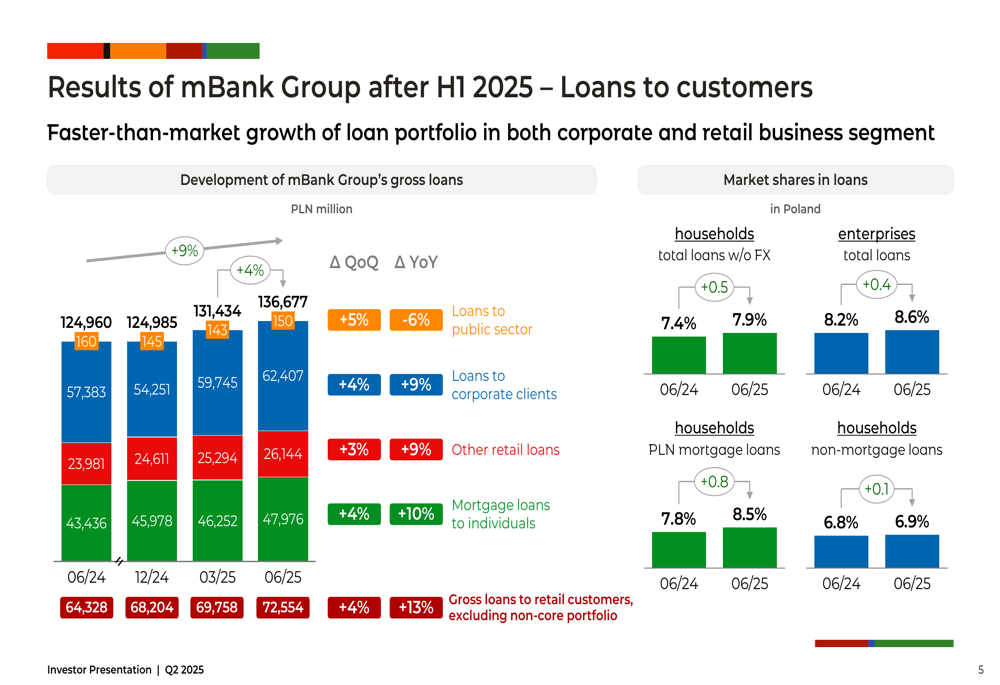

The bank’s gross loan portfolio expanded to PLN 136,677 million as of June 2025, up from PLN 124,960 million a year earlier. This growth helped mBank increase its market share in Poland across key segments, with total loans to households (excluding FX) rising from 7.4% to 7.9% and loans to enterprises increasing from 8.2% to 8.6% year-over-year.

The development of the loan portfolio and market shares is shown in this chart:

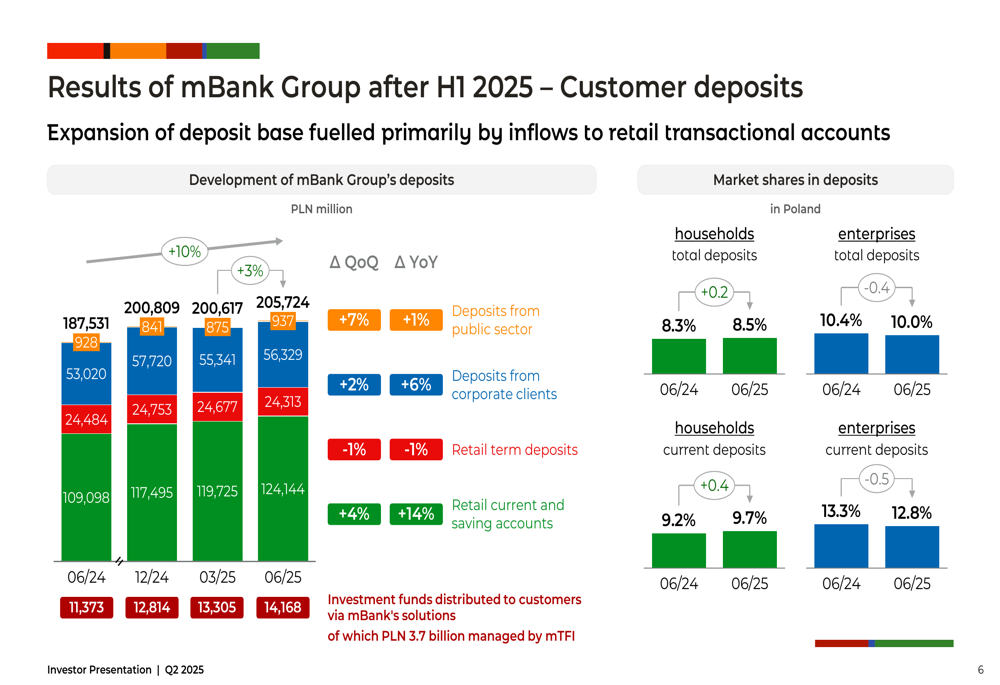

Customer deposits also showed strong growth, reaching PLN 205,724 million in June 2025, compared to PLN 187,531 million a year earlier. Retail current and savings accounts grew particularly well, increasing to PLN 124,144 million from PLN 109,098 million in June 2024.

The following chart details the development of customer deposits and market shares:

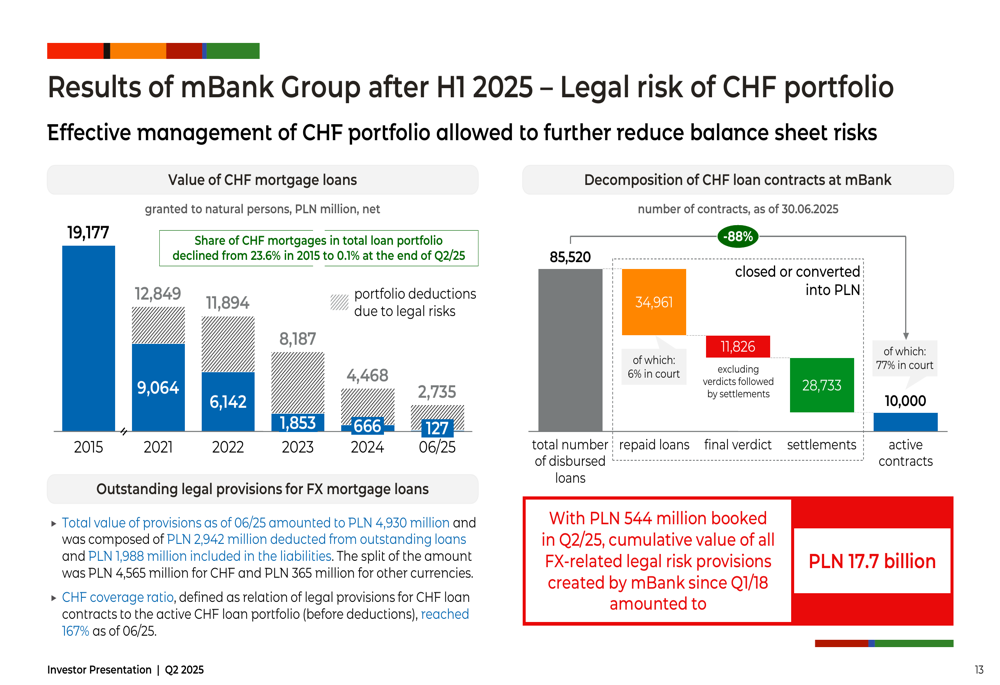

CHF Portfolio Risk Reduction

mBank has made significant progress in reducing its exposure to Swiss franc mortgage loans and the associated legal risk. The value of CHF mortgage loans decreased to PLN 4,468 million as of June 2025, a dramatic reduction from PLN 19,177 million in 2015 and PLN 6,142 million at the end of 2024.

The bank has successfully concluded 28,733 settlements with CHF loan customers as of June 2025, up from 17,016 a year earlier. New CHF-related court cases have been declining steadily, with only 202 cases involving active contracts in Q2 2025, compared to 1,006 in Q2 2024.

The following chart illustrates the reduction in the CHF portfolio and the bank’s provisioning:

Total provisions for legal risk related to foreign currency loans stood at PLN 4,930 million as of June 2025, providing a CHF coverage ratio of 167%. The bank booked PLN 544 million in FX-related legal risk provisions in Q2 2025, bringing the cumulative value of all such provisions since Q1 2018 to PLN 17.7 billion.

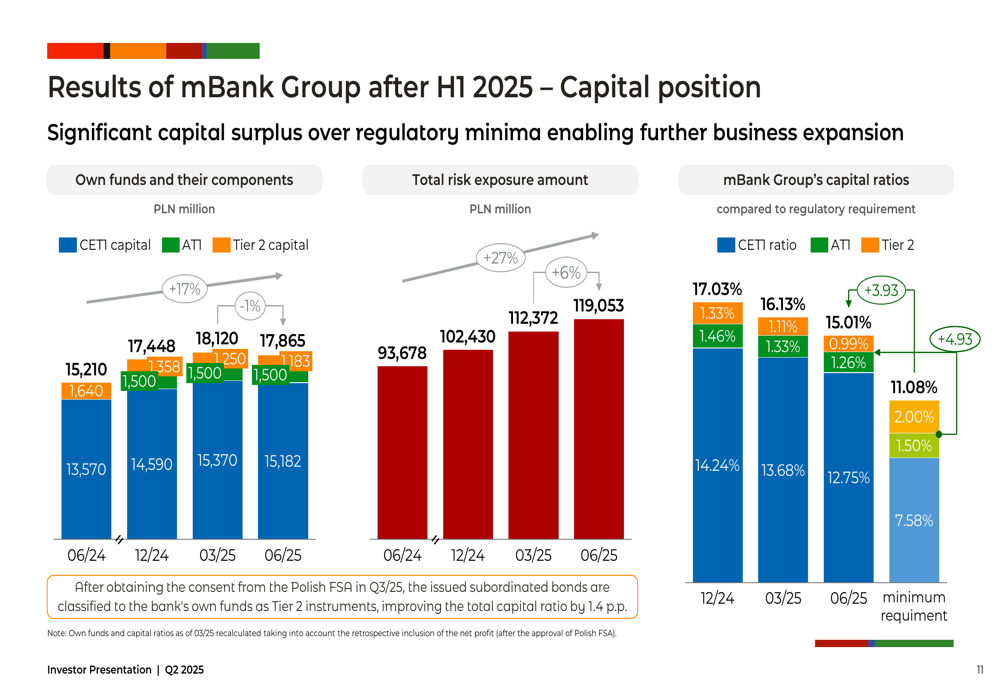

Capital Position and Strategic Achievements

mBank maintained a strong capital position with a CET1 ratio of 12.75% as of June 2025, well above the minimum requirement of 7.58%. The bank’s total capital ratio stood at 15.01%, supported by the issuance of EUR 400 million in Tier 2 subordinated bonds in the quarter.

The capital position is illustrated in the following chart:

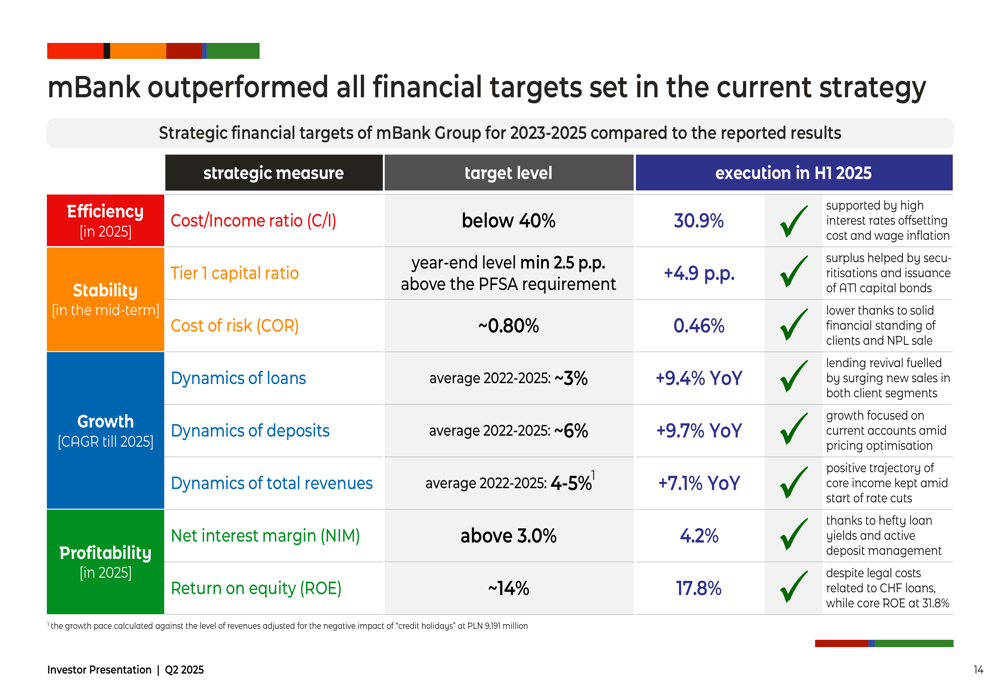

The bank has outperformed all its strategic financial targets for 2023-2025, including Cost/Income ratio (target:below 40%, actual: 30.9%), cost of risk (target:~0.80%, actual: 0.46%), and Return on Equity (target:~14%, actual: 17.8%).

The following chart shows mBank’s performance against its strategic targets:

Outlook and Guidance

Looking ahead, mBank expects its total revenues to exceed PLN 12 billion in 2025, surpassing the level reported for 2024. The bank anticipates continued strong growth in both corporate and retail loan portfolios, outpacing the market.

Capital and MREL (Minimum Requirement for own funds and Eligible Liabilities) buffers are expected to remain sound thanks to strong profit generation, complemented by the recent Tier 2 issuance and a new securitization transaction.

The bank expects that legal risk costs related to FX mortgage loans will materially burden the financial results for the last time in 2025, suggesting a resolution to this long-standing issue is approaching.

Poland’s economic outlook remains supportive, with GDP growth projected at 3.8% in 2025 and 3.5% in 2026, providing a favorable environment for the bank’s continued expansion and profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.