Aston Martin cuts 2025 volume and profit guidance amid weak demand, tariff risks

Introduction & Market Context

MC Group PCL (SET:MC) presented its FY2025 results on September 2, 2025, highlighting a year of modest overall growth and significant digital channel expansion. The presentation comes after the company’s disappointing Q4 performance, where it missed revenue expectations by 30.73%, reporting $925.41 million against forecasts of $1.336 billion.

The Thai apparel retailer, known for its flagship Mc Jeans brand which has operated for over 49 years, has been strategically pivoting from a denim-focused company to a broader lifestyle brand. This transformation continues despite recent revenue challenges, with the stock trading at 10.90 baht as of the presentation date.

Financial Performance Highlights

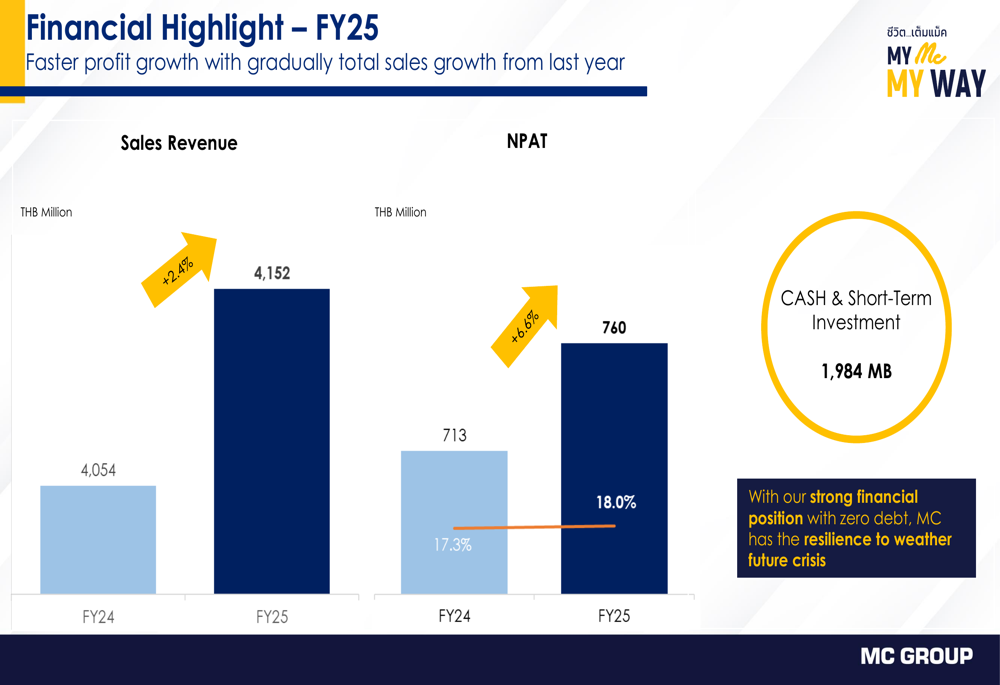

MC Group reported full-year sales revenue of 4,152 million baht for FY2025, representing a 2.4% increase from the previous year. Net profit after tax (NPAT) grew more substantially at 6.6% to reach 760 million baht, with net margin improving to 18.0% from 17.3% in FY2024.

As shown in the following financial highlights chart:

The company maintains a strong financial position with 1,984 million baht in cash and short-term investments, emphasizing its "zero debt" status as a key strength for weathering potential future crises. This solid foundation exists despite the significant Q4 revenue shortfall revealed in recent earnings reports.

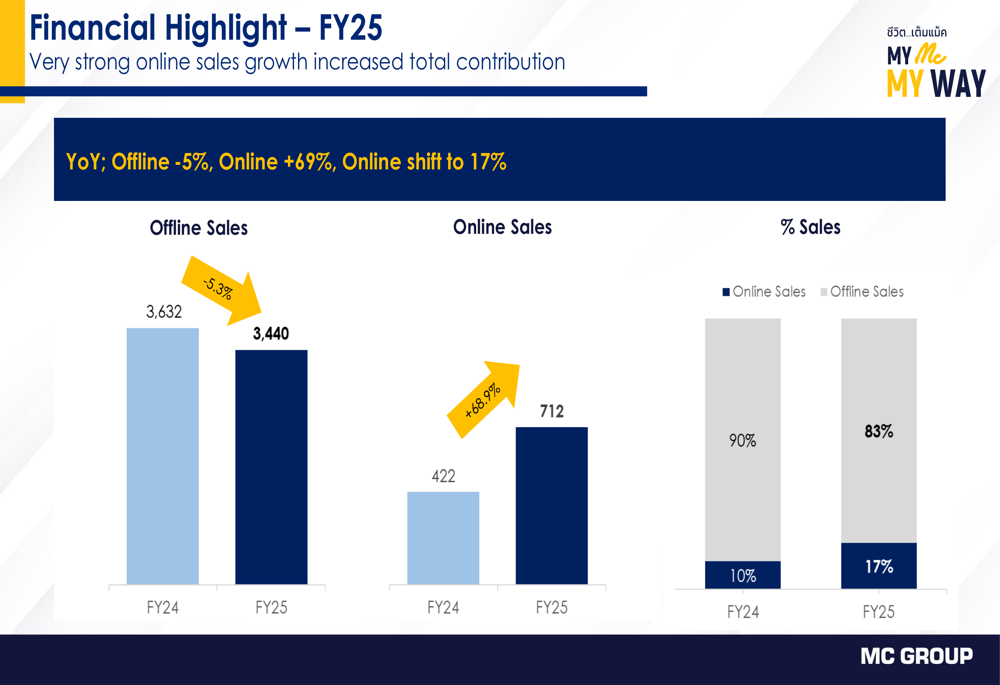

One of the most notable developments has been the dramatic shift in sales channels. Online sales surged by 69% year-over-year, now representing 17% of total sales compared to just 10% in FY2024. Meanwhile, offline sales declined by 5%, highlighting the company’s accelerating digital transformation.

This channel shift appears to be a strategic response to changing consumer behavior and may help explain some of the revenue volatility experienced in Q4. The company’s gross profit increased marginally by 2.0% to 2,655 million baht, maintaining a healthy gross margin of 63.9%, slightly down from 64.2% in the previous year.

Strategic Initiatives

MC Group’s presentation outlined four key strategic pillars: expanding product categories, growing distribution channels, enhancing customer experiences, and improving margins and productivity.

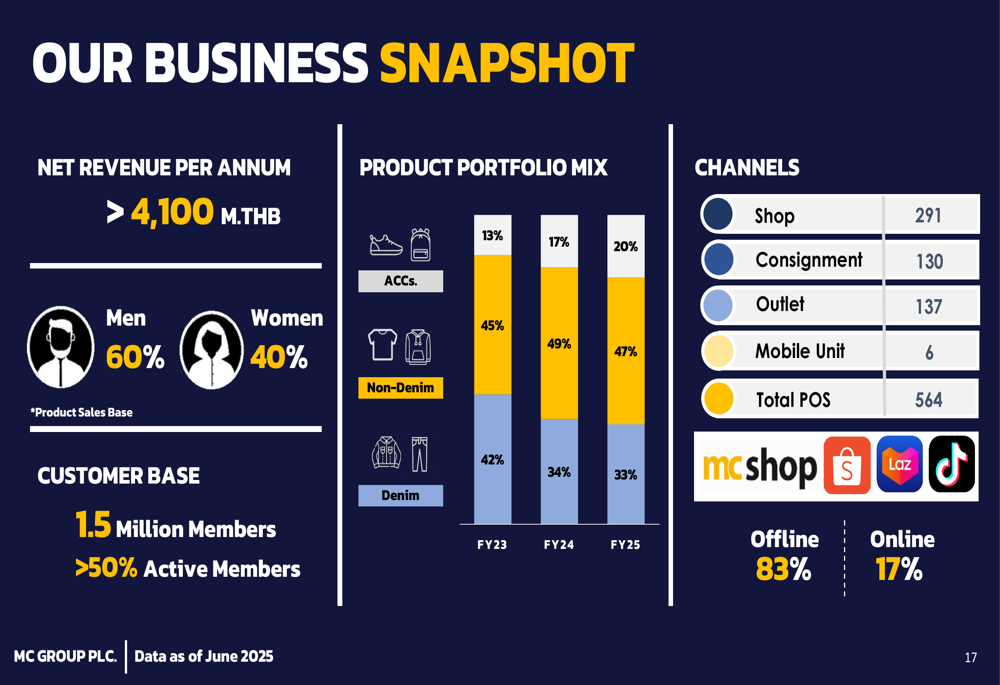

The company’s business snapshot reveals a significant transformation in its product portfolio, with denim products now accounting for only 33% of sales (down from 42% in FY2023), while non-denim items contribute 47% and accessories 20%. This diversification represents a deliberate shift toward becoming a comprehensive lifestyle brand.

The company operates through 564 points of sale nationwide, including 291 shops, 130 consignment locations, 137 outlets, and 6 mobile units. With 1.5 million loyalty program members and over 50% active participation, MC Group is leveraging its customer relationships to drive growth.

Store productivity improvement initiatives are underway, with projects designed to increase display capacity by 24% and enhance traffic flow, conversion rates, and average transaction values. The company is also investing in its CRM capabilities as both a profit center and sales driver, noting that members generate 70% of sales with 40% repeat purchases and 50% higher average transaction values.

Financial Position & Dividend Policy

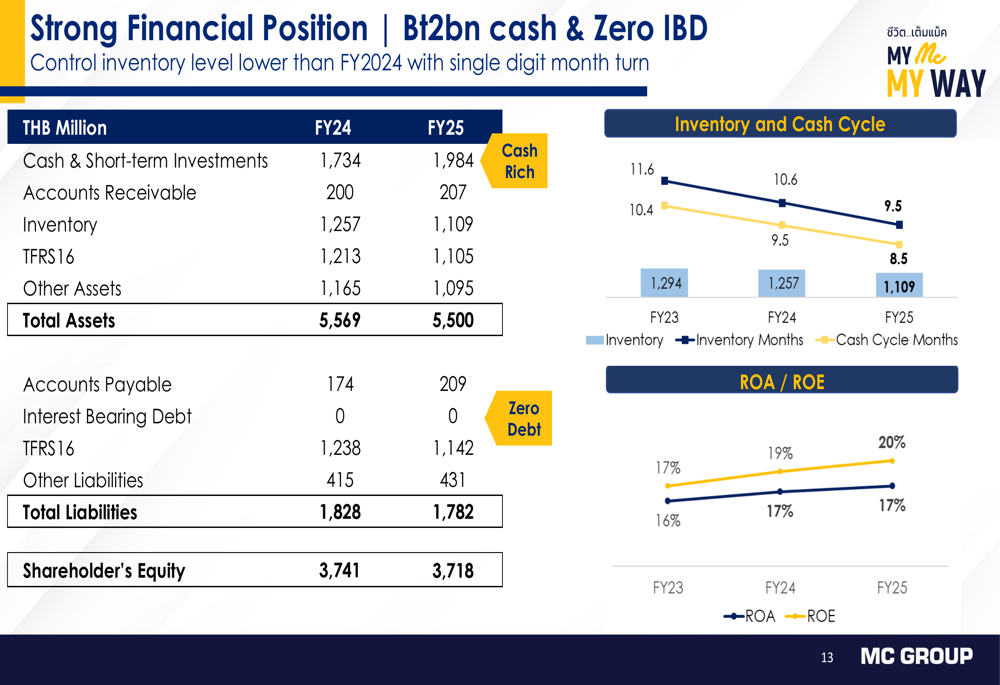

MC Group’s financial strength remains a cornerstone of its investor proposition, with the presentation highlighting its zero-debt position and substantial cash reserves. The company’s return on equity improved from 19% to 20%, while inventory levels decreased and cash cycle improved from 10.6 to 9.5 months.

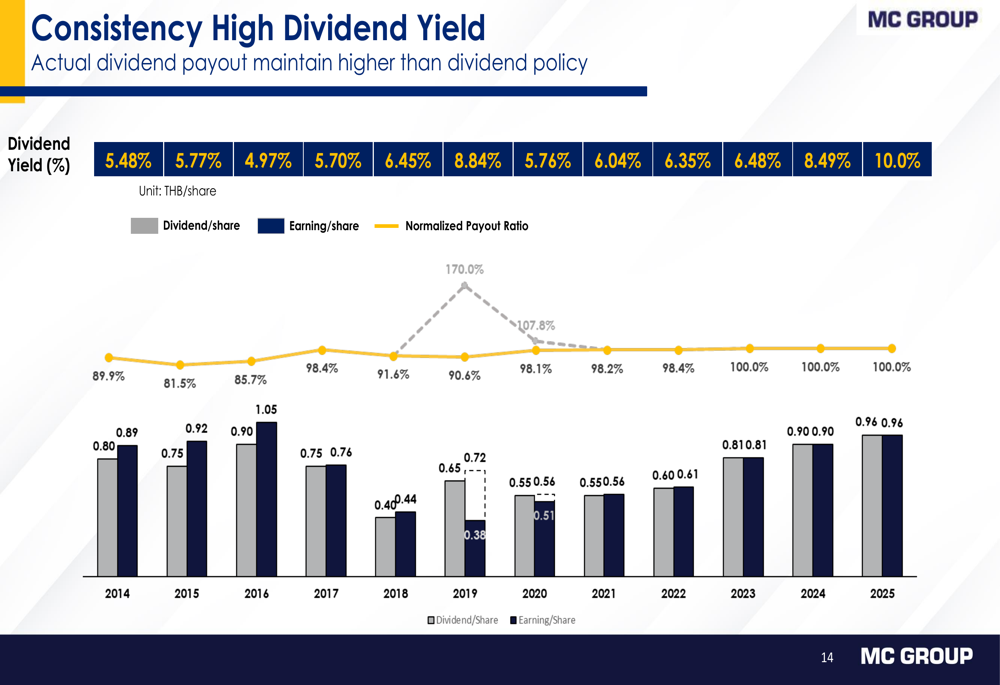

Particularly noteworthy is MC Group’s dividend policy, which has delivered consistently high yields. The dividend yield for 2025 stands at an impressive 10.0%, continuing an upward trend from 5.48% in 2014. This generous shareholder return policy appears sustainable given the company’s strong cash position, though investors may question its long-term viability if revenue challenges persist.

Challenges & Outlook

While the presentation focused primarily on positive developments, the recent earnings report revealed significant challenges, particularly the 30.73% revenue miss in Q4. This discrepancy raises questions about the sustainability of the company’s growth trajectory and the effectiveness of its strategic initiatives.

The presentation’s emphasis on online growth aligns with statements in the earnings report about expanding digital and omnichannel strategies. However, the earnings report mentioned maintaining a 5% net profit margin, which contrasts with the 18.0% net margin highlighted in the presentation, suggesting potential differences in calculation methodology or forward-looking projections versus current performance.

MC Group summarized its competitive strengths and market positioning as follows:

Looking forward, the company expects to maintain its growth momentum through continued product diversification, channel expansion, and customer experience enhancements. The earnings report indicates revenue forecasts of $1.45 billion for fiscal year 2025 and $1.721 billion for 2026, suggesting confidence in overcoming current challenges.

Conclusion

MC Group’s FY2025 presentation portrays a company in transition, successfully pivoting toward digital channels and lifestyle products while maintaining strong profitability and financial discipline. The 69% surge in online sales represents a bright spot amid otherwise modest growth figures and a disappointing Q4 revenue performance.

Investors will likely focus on whether the company can leverage its zero-debt position, strong brand equity, and customer relationships to address revenue challenges while continuing to deliver exceptional dividend yields. The contrast between the optimistic tone of the presentation and the significant Q4 revenue miss highlights the challenges of navigating retail transformation in a competitive market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.