Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Medallion Financial Corp. (NASDAQ:MFIN) released its first quarter 2025 earnings presentation on April 30, showcasing continued growth in its loan portfolio and improved financial performance. The company, which has transformed from its original taxi medallion lending focus to a diversified consumer and commercial lender, reported a 20% year-over-year increase in net income and announced a dividend increase.

In after-hours trading following the presentation, Medallion’s stock rose 1.7% to $8.95, building on its regular session closing price of $8.85. The stock has been trading in a range between its 52-week high of $10.50 and low of $6.48.

Quarterly Performance Highlights

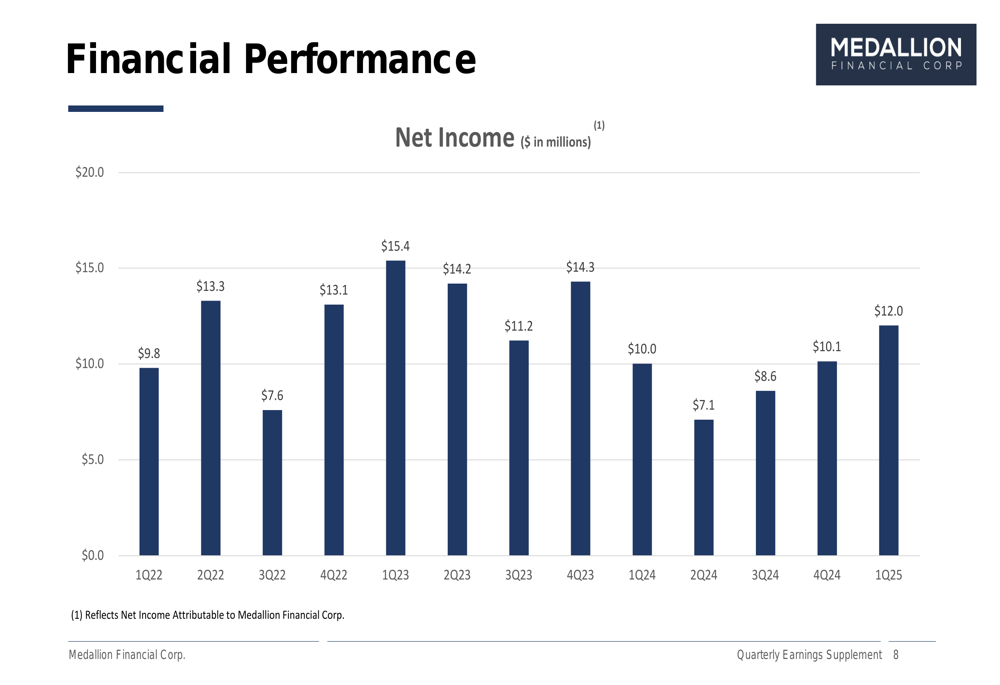

Medallion Financial reported net income of $12.0 million for Q1 2025, up from $10.0 million in Q1 2024, representing a 20% year-over-year increase. Net interest income grew to $51.4 million, compared to $47.9 million in the same period last year.

The company’s return on common equity stood at 12.96%, reflecting its improved profitability. In a move that signals confidence in its financial position, Medallion announced a dividend increase to $0.12 per share per quarter beginning May 2025, up from the previous $0.11 quarterly dividend.

As shown in the following chart of quarterly net income performance, the company has demonstrated a recovery trend in recent quarters:

Loan Portfolio Analysis

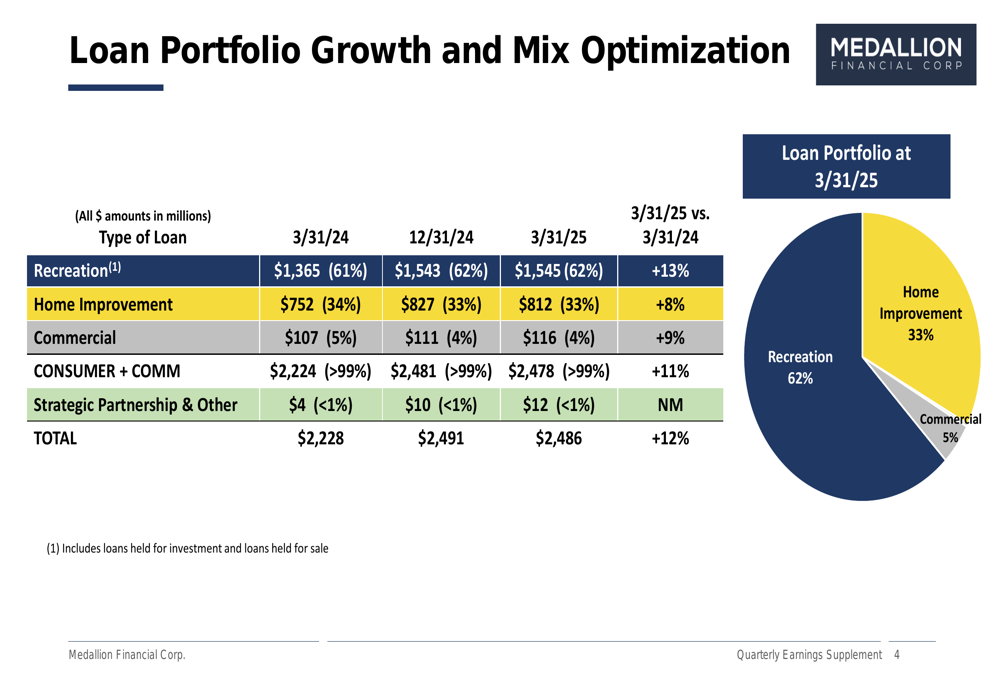

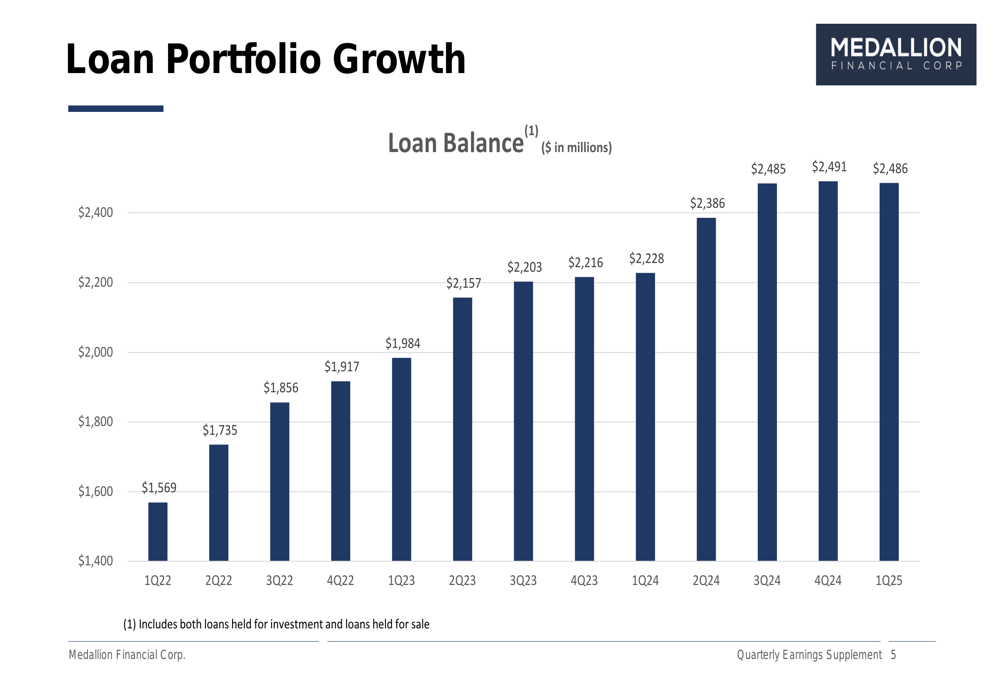

Medallion Financial’s total loan portfolio reached $2.486 billion as of March 31, 2025, representing a 12% increase from $2.228 billion a year earlier. The portfolio remains primarily focused on consumer lending, with recreation loans comprising 62% of the portfolio, home improvement loans accounting for 33%, and commercial lending making up the remaining 5%.

The following chart illustrates the company’s loan portfolio composition and year-over-year growth by segment:

The company’s loan portfolio has shown consistent growth over the past three years, as demonstrated in this quarterly progression:

Recreation lending continues to be the largest segment with $1.545 billion in loans and an average interest rate of 15.01% at quarter-end. This segment targets consumers with an average FICO score of 685 and is distributed through approximately 3,300 dealers and financial service providers.

Home improvement lending, which targets higher credit quality borrowers with an average FICO score of 781, totaled $812.4 million with an average interest rate of 9.83%. Commercial lending, the smallest segment, stood at $116.1 million with an average interest rate of 13.14%.

Financial Performance Details

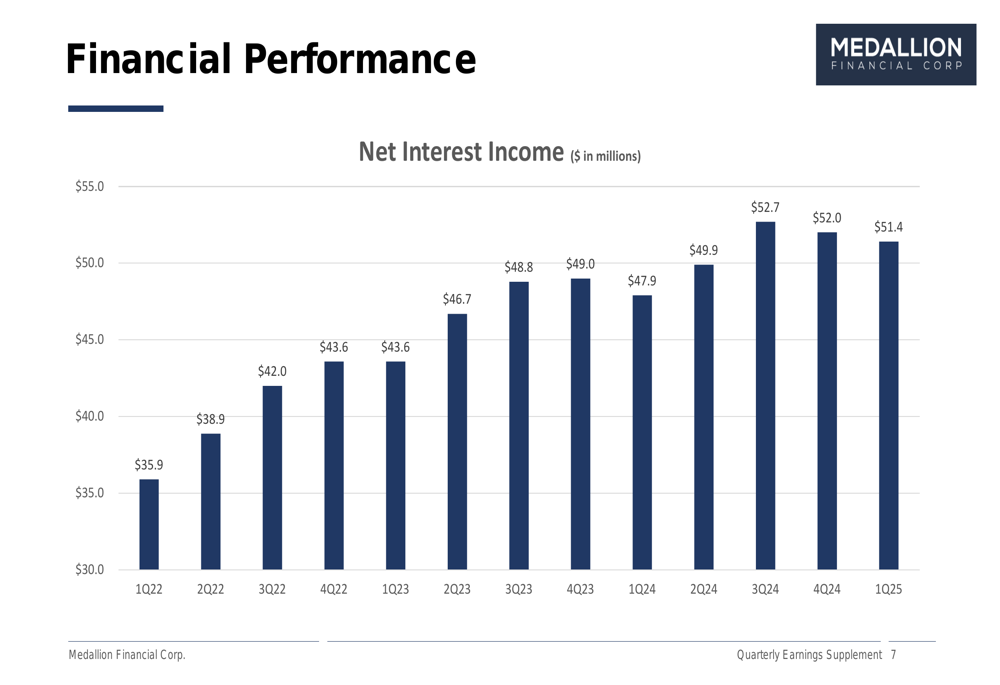

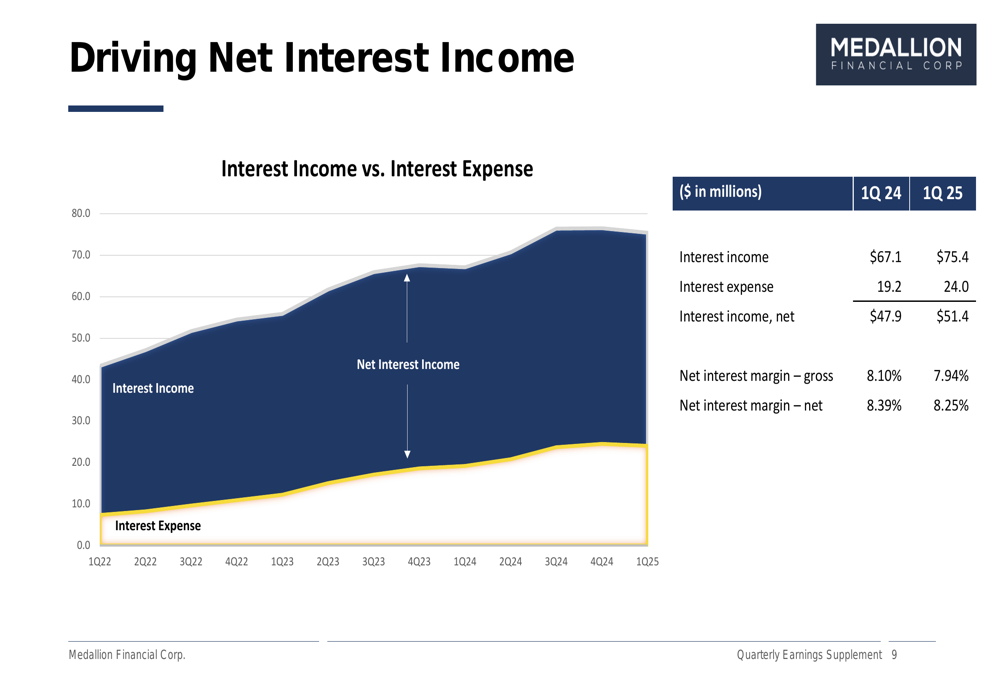

Medallion’s net interest income has shown steady growth over time, reaching $51.4 million in Q1 2025. This represents a 7.3% increase from the $47.9 million reported in Q1 2024.

The following chart demonstrates the company’s consistent net interest income growth trajectory:

However, the company’s net interest margin showed a slight compression, with the margin on gross loans decreasing to 7.94% in Q1 2025 from 8.10% in Q1 2024. Similarly, the net interest margin on net loans declined to 8.25% from 8.39% in the same period.

The following chart breaks down the components driving net interest income:

Net charge-offs as a percentage of the total portfolio improved slightly to 3.1% in Q1 2025 from 3.2% in Q1 2024. Recreation loans continued to have the highest charge-off rate at 4.7%, up from 4.4% a year earlier, while home improvement loans improved to 1.6% from 2.1%.

Operating Efficiency and Capital Structure

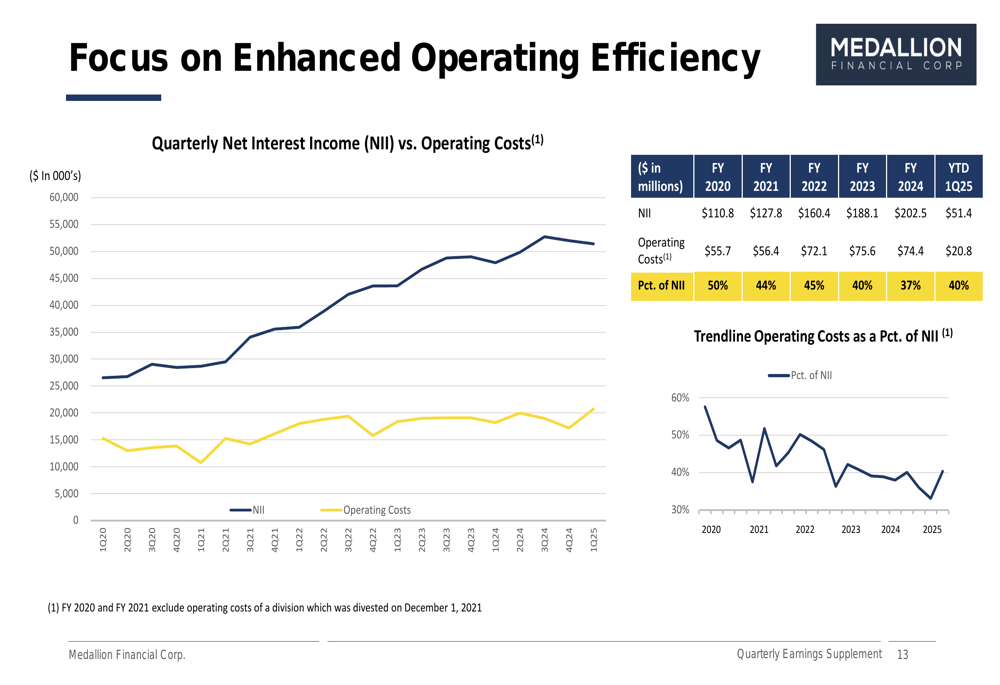

Medallion Financial has made significant strides in improving its operating efficiency over the years. Operating costs as a percentage of net interest income stood at 40% in Q1 2025, compared to 50% in fiscal year 2020. However, this represents a slight increase from the 37% reported for fiscal year 2024.

The following chart illustrates the company’s focus on enhanced operating efficiency:

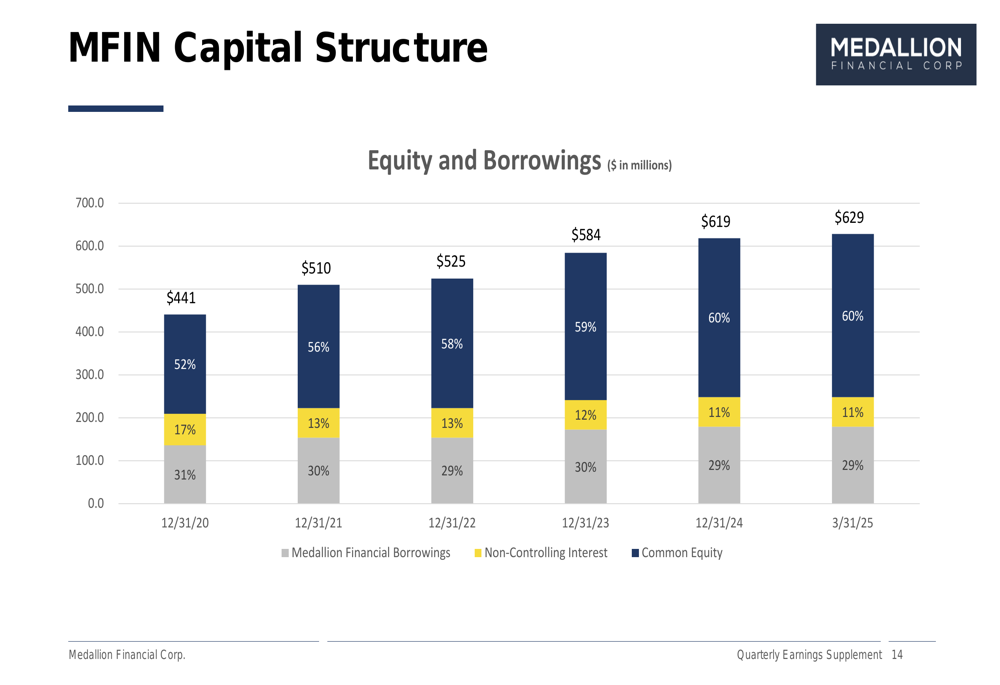

The company’s capital structure has remained relatively stable, with Medallion Financial borrowings accounting for 60% of the total capital structure as of March 31, 2025, common equity at 29%, and non-controlling interest at 11%. Total (EPA:TTEF) capital reached $629 million, up from $441 million at the end of 2020.

Medallion has also been active in returning capital to shareholders through its share repurchase program, having purchased 60,185 shares at an average cost of $8.83 per share, with $14.9 million remaining in the repurchase plan.

Forward Outlook

While the presentation did not provide explicit forward guidance, Medallion Financial’s increased dividend and ongoing share repurchase program suggest management’s confidence in the company’s future performance. The company’s diversified lending portfolio, with its focus on higher-yielding recreation and home improvement loans, positions it to continue generating solid returns.

The slight compression in net interest margin and the uptick in operating costs as a percentage of net interest income will be areas to watch in coming quarters. Additionally, the increase in net charge-offs in the recreation segment, while still within historical norms, bears monitoring in the context of broader economic conditions.

Medallion’s strategic shift away from taxi medallion lending (now representing just $6.8 million in net assets) to consumer and commercial lending has transformed the company into a more diversified financial institution with improved stability and growth prospects. The company’s ability to maintain this growth trajectory while managing credit quality will be key to its continued success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.