U.S. stocks lower as investors rotate out of tech ahead of Jackson Hole

Introduction & Market Context

MEG Energy Corp (TSX:MEG) released its corporate presentation for November 2024, highlighting the company’s strong third-quarter performance and strategic shift toward enhanced shareholder returns. The Canadian oil sands producer has reached a significant milestone by achieving its US$600 million net debt target in Q3 2024, enabling the company to transition to returning 100% of free cash flow to shareholders starting in Q4.

The company operates in an improved market environment with the Trans Mountain Expansion (TMX) pipeline now in service, which has reduced Western Canadian Select (WCS) differential volatility and enhanced market access for Canadian heavy crude producers. MEG emphasized its strong position with approximately 80% of its production having firm service tidewater access.

Q3 2024 Performance Highlights

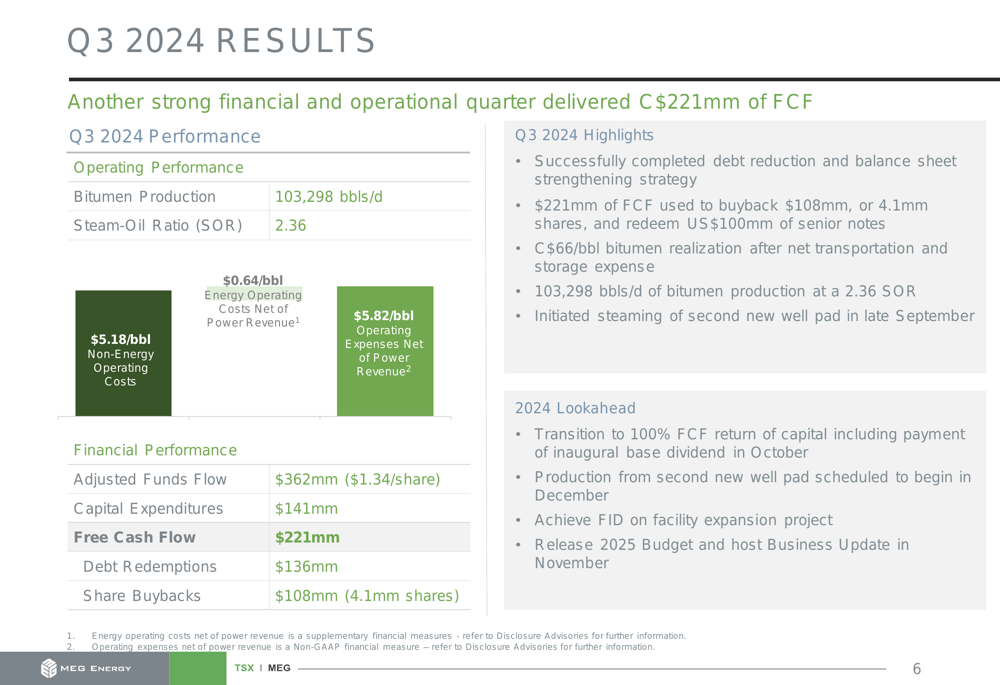

MEG Energy (OTC:MEGEF) delivered robust operational and financial results in the third quarter of 2024, generating C$221 million in free cash flow on bitumen production of 103,298 barrels per day. The company maintained a strong steam-oil ratio (SOR) of 2.36, demonstrating continued operational efficiency.

As shown in the following quarterly results summary:

Financial performance was equally strong, with adjusted funds flow reaching $362 million ($1.34 per share) against capital expenditures of $141 million. The company used its free cash flow to buy back $108 million of shares (4.1 million shares) and redeem US$100 million of senior notes during the quarter.

MEG achieved a bitumen realization of C$66 per barrel after net transportation and storage expenses, benefiting from improved market access and the narrowing WCS differential. The company also initiated steaming of its second new well pad in late September, with production expected to begin in December.

Strategic Initiatives & Capital Allocation

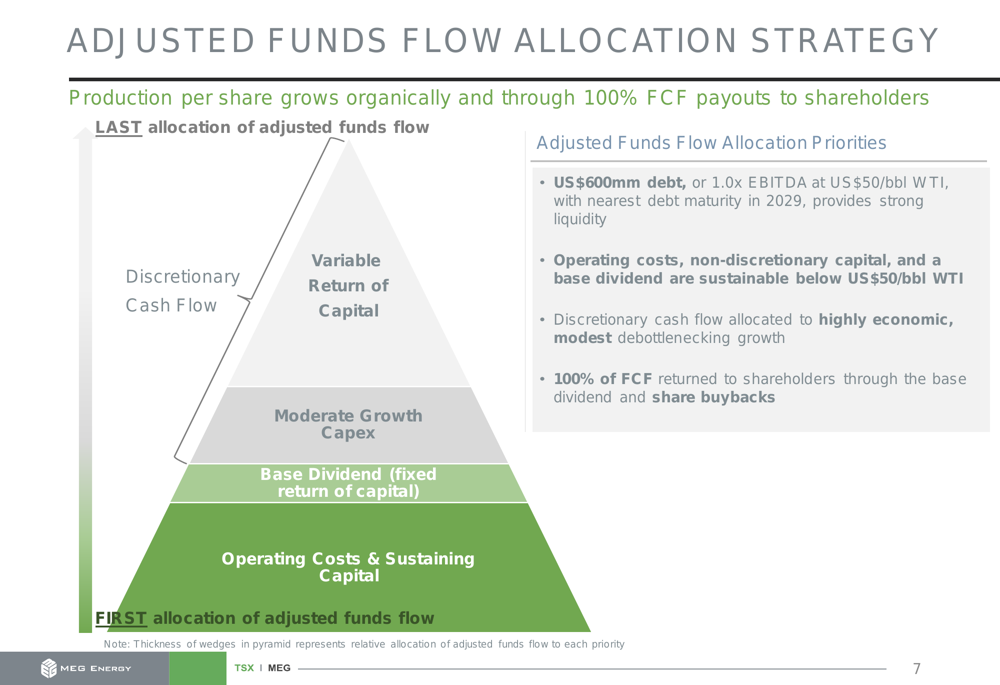

MEG Energy has successfully completed its debt reduction and balance sheet strengthening strategy, reaching the US$600 million net debt target in Q3 2024. This achievement marks a pivotal moment for the company’s capital allocation strategy, enabling the transition to returning 100% of free cash flow to shareholders.

The company’s adjusted funds flow allocation strategy is structured to prioritize operational sustainability while maximizing shareholder returns, as illustrated in the following pyramid:

MEG declared its inaugural quarterly base dividend of C$0.10 per share in Q3 2024, which was paid in October. This fixed return of capital complements the company’s robust share buyback program, which has repurchased approximately 50.7 million shares (17% of year-end 2021 outstanding balance) for $1.1 billion since April 2022.

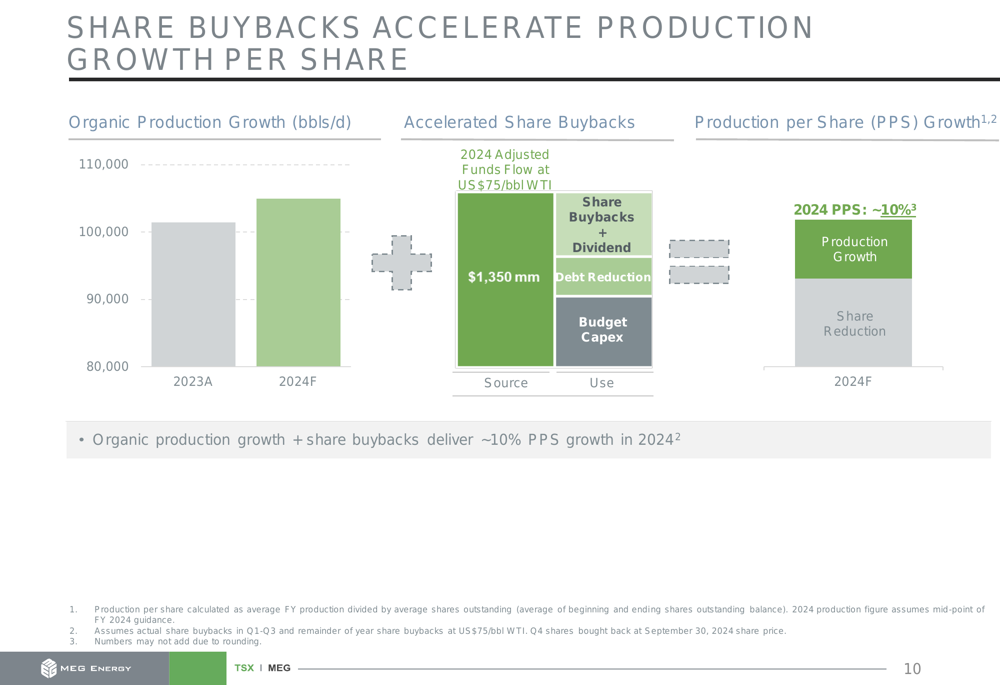

The company’s share buyback program, combined with organic production growth, is expected to deliver approximately 10% production per share growth in 2024, as shown in the following chart:

Financial Outlook & Sensitivity Analysis

MEG Energy provided a comprehensive overview of its 2024 budget guidance, projecting average bitumen production of 102,000-108,000 barrels per day with capital expenditures of $550 million. The capital budget allocates $450 million to sustaining capital and $100 million to modest debottlenecking growth initiatives.

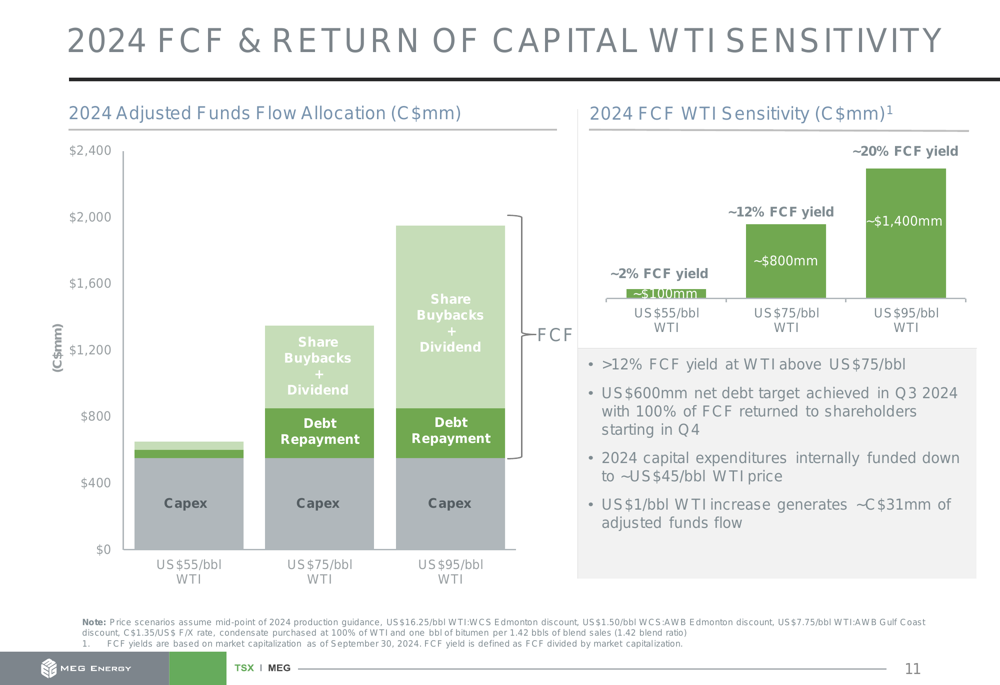

The company’s free cash flow generation demonstrates significant sensitivity to oil prices, with projected FCF yields of approximately 12% at US$75/bbl WTI and 20% at US$95/bbl WTI. This unhedged exposure to oil prices provides substantial upside potential in a strong price environment.

As shown in the following WTI sensitivity analysis:

MEG also highlighted its sensitivity to various market factors, noting that a US$1/bbl improvement in the WCS differential generates approximately C$47 million in additional adjusted funds flow, while a US$1/bbl increase in WTI adds approximately C$31 million.

Operational Excellence & Market Access

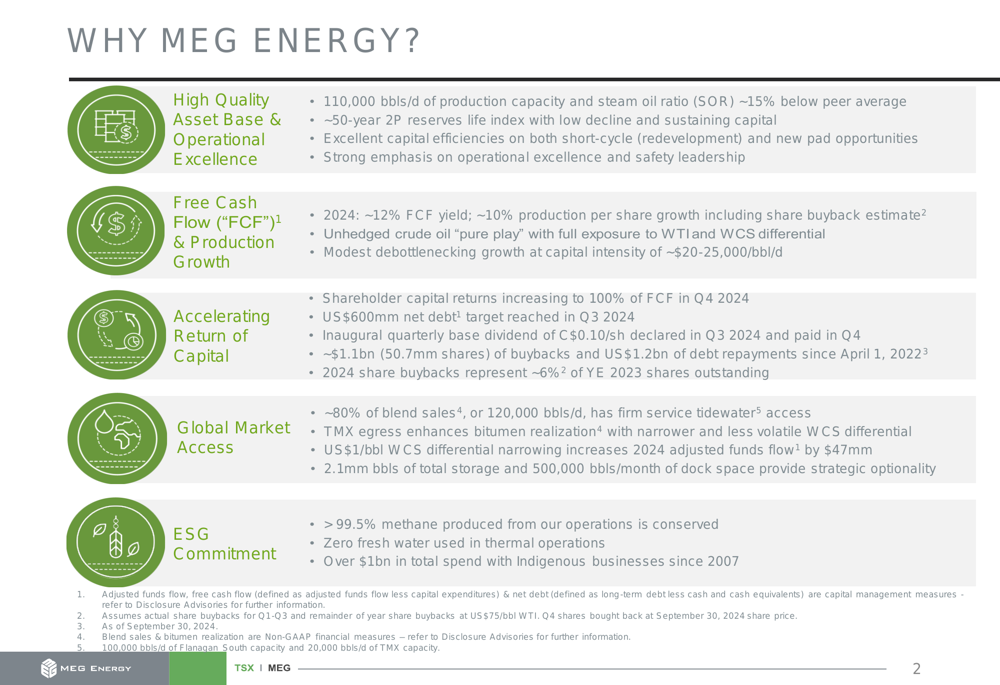

MEG Energy emphasized its continued focus on operational excellence, which has enabled the company to achieve production levels exceeding 100,000 barrels per day with top-tier non-energy operating costs. The company’s operating strategy includes enhanced completion designs, optimized well spacing, and effective steam allocation to maximize production and efficiency.

The company’s investment thesis is built on several key strengths, as outlined in the following overview:

A significant competitive advantage for MEG is its extensive tidewater access, with 120,000 barrels per day of capacity representing approximately 80% of production. This market access enhances bitumen realizations and provides strategic optionality in accessing global markets.

The company’s market access position has been further strengthened by the TMX pipeline coming into service, which has removed apportionment and reduced volatility in the WCS differential. MEG projects the WCS differential to trade in a US$10-15/bbl range, primarily driven by seasonal factors.

Forward-Looking Statements

Looking ahead, MEG Energy is transitioning to modest debottlenecking growth with highly economic facility expansion projects. The company is targeting 3-5% compound annual growth rate (CAGR) in production over the next five years, with capital intensity of approximately $20,000-25,000 per barrel per day.

MEG expects to achieve Final Investment Decision (FID) on its facility expansion project and release its 2025 budget in November. The company’s growth initiatives include a third processing train, skim tank, and steam optionality tie-ins, with $100 million allocated to these projects in the 2024 capital budget.

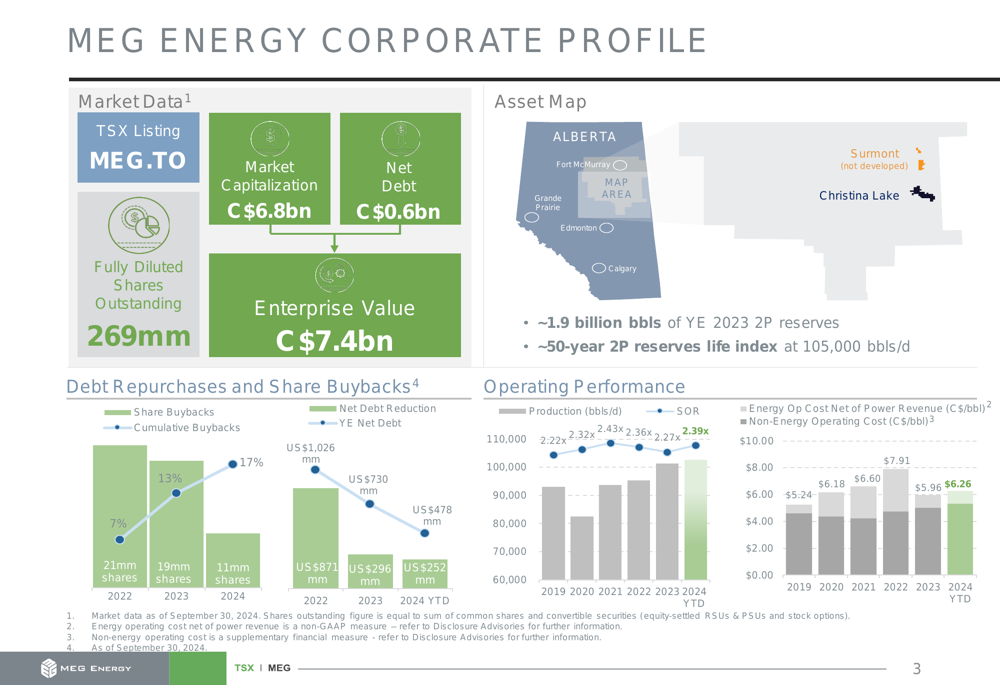

The company’s corporate profile demonstrates a strong foundation for future growth, with approximately 1.9 billion barrels of year-end 2023 2P reserves and a 50-year reserves life index at 105,000 barrels per day:

MEG Energy’s commitment to ESG principles remains a core focus, with over 99.5% of methane produced being conserved, zero fresh water used in thermal operations, and over $1 billion spent with Indigenous businesses since 2007. These initiatives support the company’s long-term sustainability and social license to operate.

With its strengthened balance sheet, operational excellence, and enhanced market access, MEG Energy is well-positioned to deliver sustainable production growth and substantial shareholder returns in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.