Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

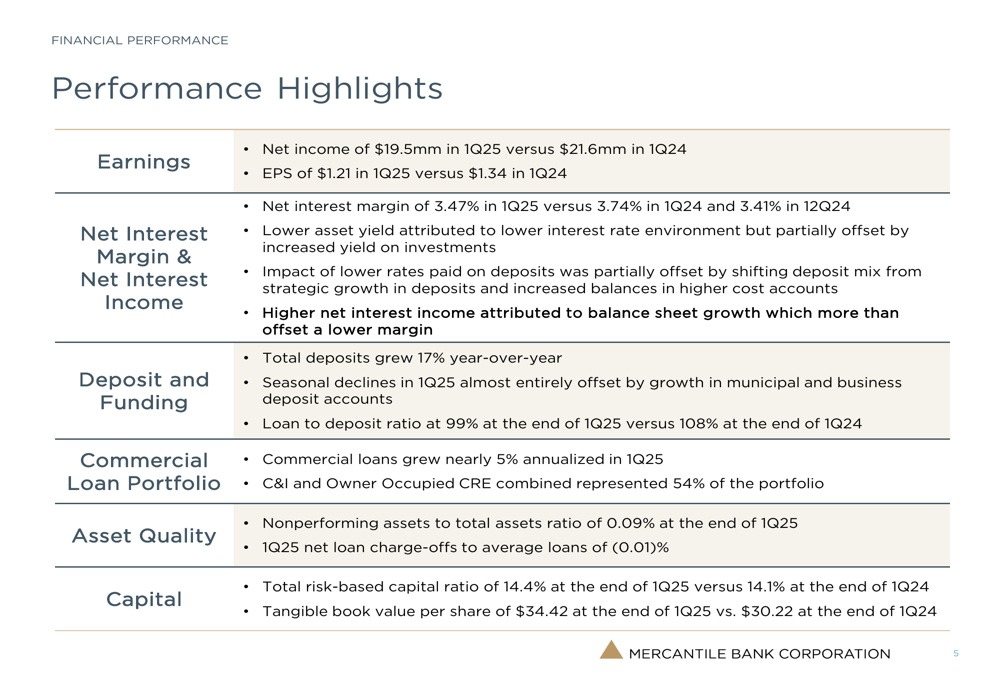

Mercantile Bank Corporation (NASDAQ:MBWM) released its first quarter 2025 investor presentation on April 22, highlighting continued execution of its strategic initiatives amid a changing interest rate environment. The Michigan-based bank reported net income of $19.5 million and earnings per share of $1.21, down from $21.6 million and $1.34 in the same period last year, as the bank prioritizes balance sheet improvement over short-term profitability.

Trading at $40.26 as of the presentation date, Mercantile’s stock remains below its 52-week high of $52.98, despite the bank’s outperformance against peers in key growth metrics. This valuation gap persists even as the bank demonstrates strong execution on its strategic priorities.

Quarterly Performance Highlights

Mercantile reported solid performance across key metrics for Q1 2025, with particular strength in deposit growth and asset quality. While net income and EPS declined year-over-year, the bank made significant progress in improving its balance sheet structure.

As shown in the following comprehensive performance summary:

Total (EPA:TTEF) deposits grew 17% year-over-year, significantly outpacing loan growth and reducing the loan-to-deposit ratio to 99% from 108% a year earlier. Commercial loans continued to grow at a healthy pace, increasing nearly 5% on an annualized basis in Q1 2025.

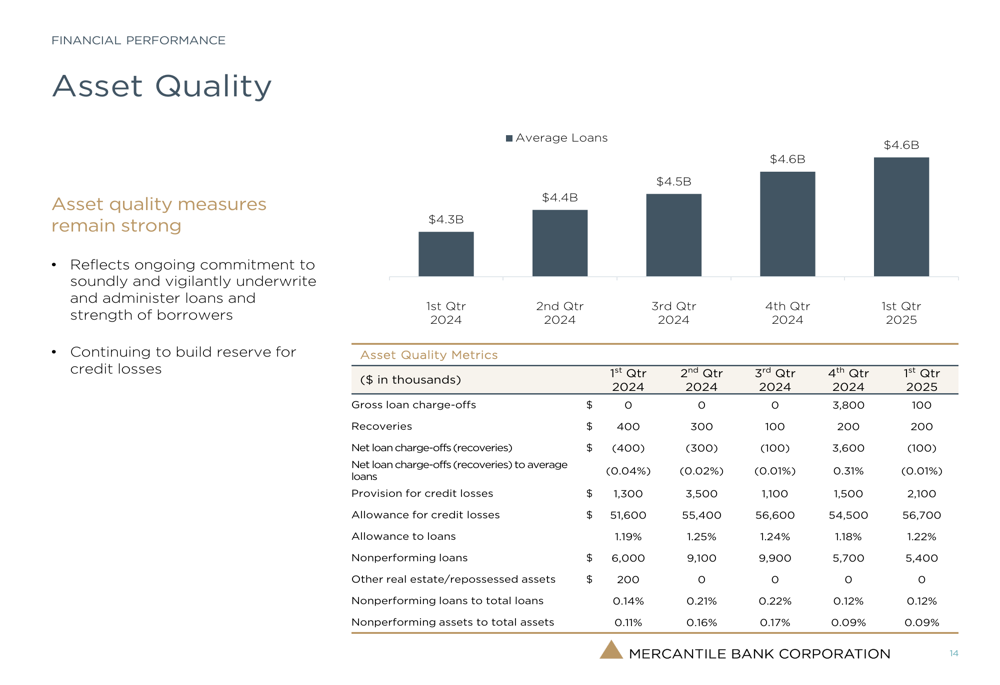

Asset quality remained exceptional, with nonperforming assets to total assets at just 0.09% and net loan recoveries (rather than charge-offs) of 0.01% of average loans. The bank’s capital position strengthened, with the total risk-based capital ratio improving to 14.4% from 14.1% a year earlier, while tangible book value per share grew to $34.42 from $30.22.

Strategic Initiatives

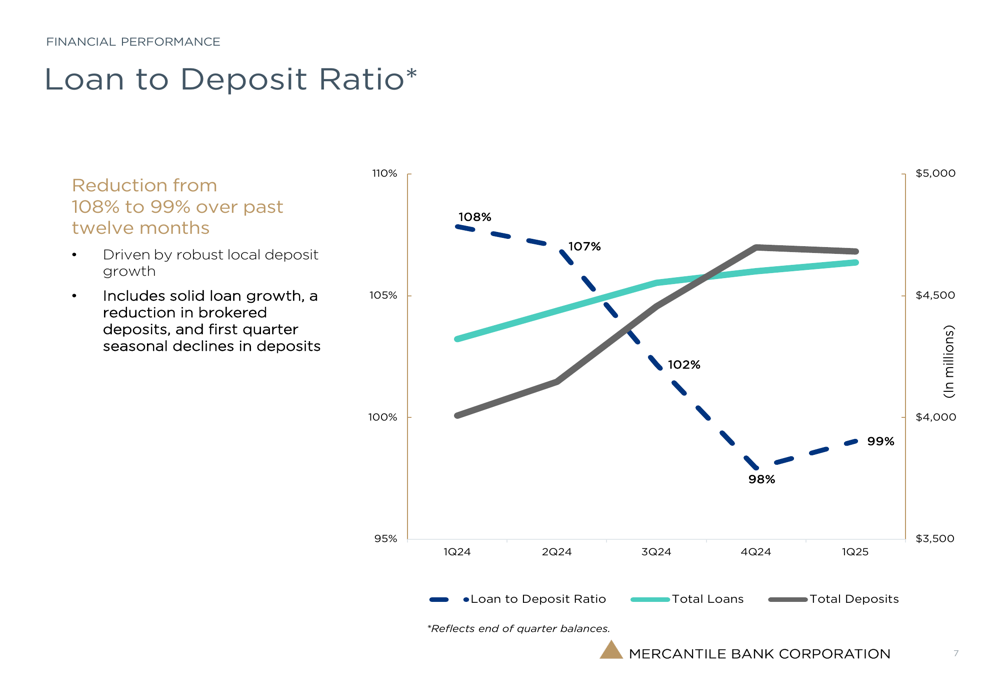

Mercantile’s primary strategic focus continues to be improving its loan-to-deposit ratio, which has successfully decreased from 108% in Q1 2024 to 99% in Q1 2025. This improvement reflects the bank’s emphasis on deposit gathering, particularly in business and municipal accounts, which has helped offset seasonal declines typically seen in the first quarter.

The following chart illustrates this positive trend over the past year:

The bank attributes this improvement to robust local deposit growth combined with solid loan growth and a reduction in brokered deposits. This strategic shift is positioning Mercantile for greater balance sheet flexibility and reduced funding costs over time.

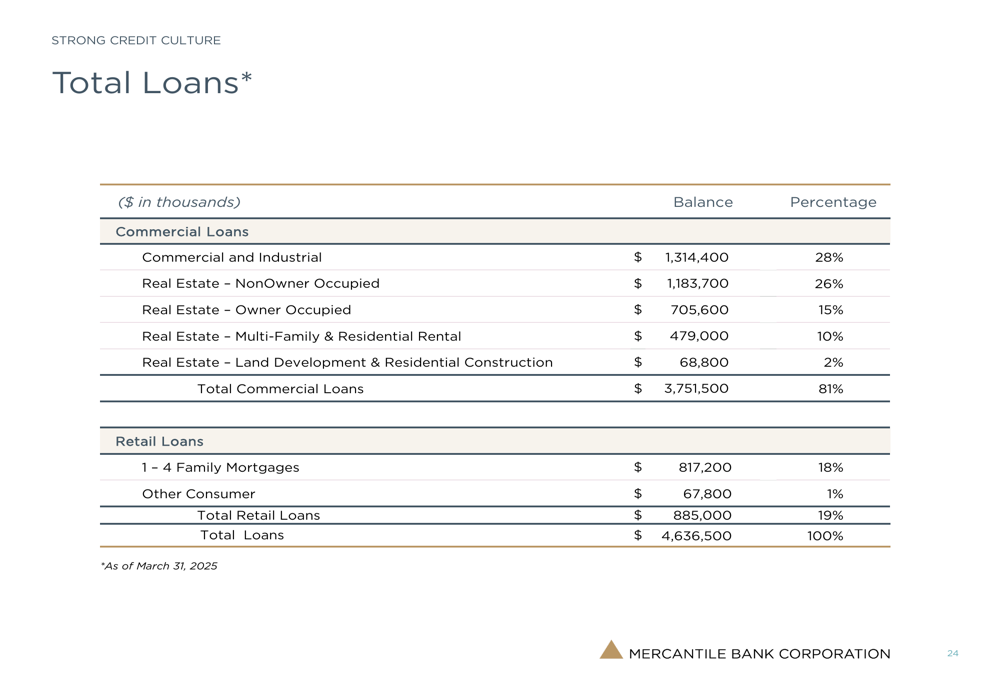

Mercantile has also maintained a disciplined approach to its loan portfolio composition, with a focus on commercial and industrial loans and owner-occupied commercial real estate, which together represent 54% of the portfolio. This emphasis on relationship-based lending supports the bank’s broader strategy of being a full-service partner to its business clients.

Detailed Financial Analysis

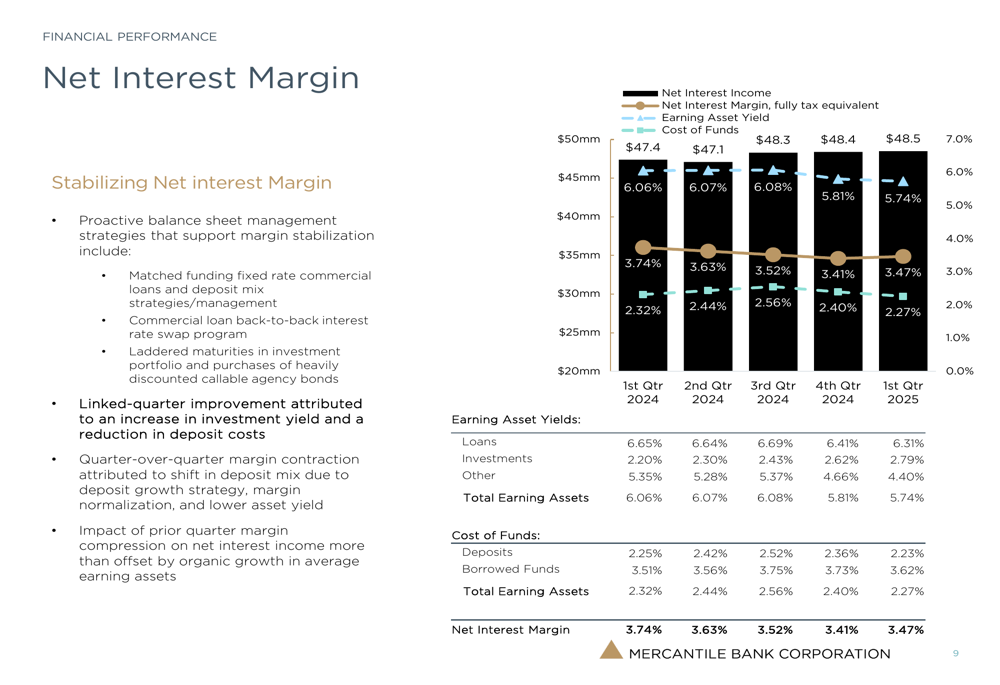

Despite pressure on its net interest margin, which declined to 3.47% in Q1 2025 from 3.74% a year earlier, Mercantile’s net interest income remained stable. This stability was achieved through balance sheet growth that offset the margin compression.

The following chart shows the trend in net interest income and margin:

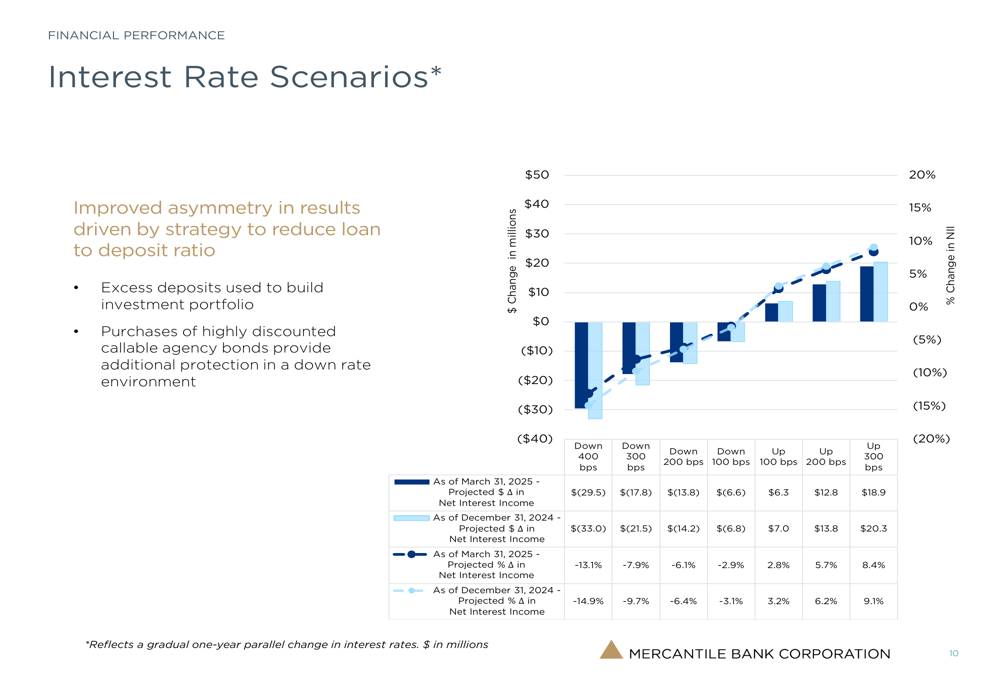

The bank’s proactive balance sheet management has improved its positioning for various interest rate scenarios. As shown in the following analysis, Mercantile has reduced its sensitivity to interest rate changes compared to the previous quarter:

This improved symmetry in results was driven by the strategy to reduce the loan-to-deposit ratio, with excess deposits used to build the investment portfolio. The purchase of highly discounted callable agency bonds provides additional protection in a declining rate environment.

Asset quality remains a significant strength for Mercantile, with consistently strong metrics across all categories:

The bank’s allowance for credit losses stands at $56.7 million, representing 1.22% of total loans, while nonperforming loans total just $5.4 million, or 0.12% of total loans.

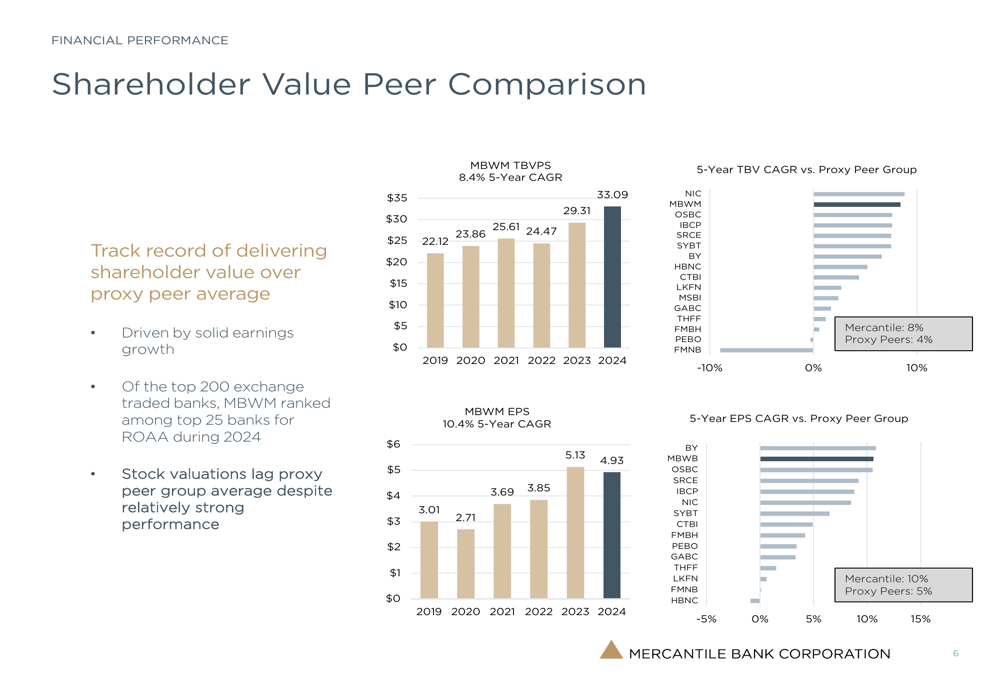

Shareholder Value Creation

Mercantile has consistently outperformed its peer group in key shareholder value metrics. The bank’s tangible book value per share has grown at a 5-year compound annual growth rate (CAGR) of 8.4%, double the 4% rate of its proxy peer group. Similarly, earnings per share have grown at a 10.4% CAGR over the same period, compared to 5% for peers.

The following comparison illustrates this outperformance:

Despite this strong relative performance, Mercantile’s stock continues to trade at a discount to its peer group, presenting a potential opportunity for investors who believe the bank’s strategic initiatives will continue to deliver superior results.

Loan Portfolio and Credit Quality

Mercantile maintains a diversified loan portfolio with a focus on commercial lending. Commercial loans represent 81% of the total portfolio, with residential mortgages and other consumer loans making up the remaining 19%.

The following breakdown shows the composition of the bank’s $4.64 billion loan portfolio:

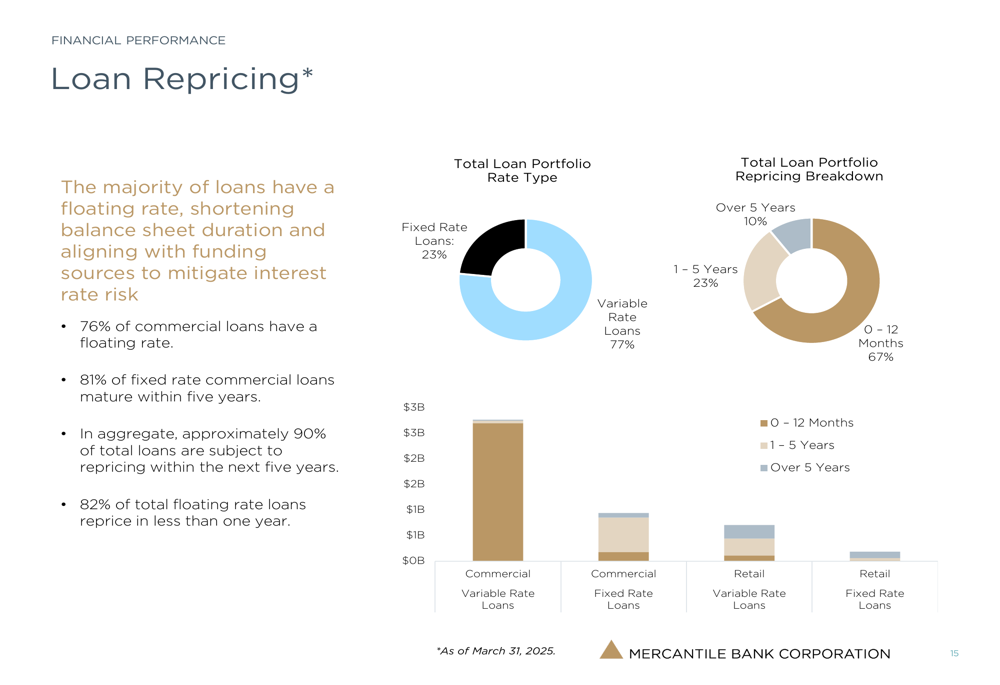

The bank’s loan portfolio is predominantly variable-rate (77%), providing flexibility in a changing rate environment. The majority of loans (67%) reprice within 12 months, with an additional 23% repricing within 1-5 years.

This repricing structure positions Mercantile well for potential interest rate changes, allowing the bank to adjust its asset yields relatively quickly as market conditions evolve.

Forward-Looking Statements

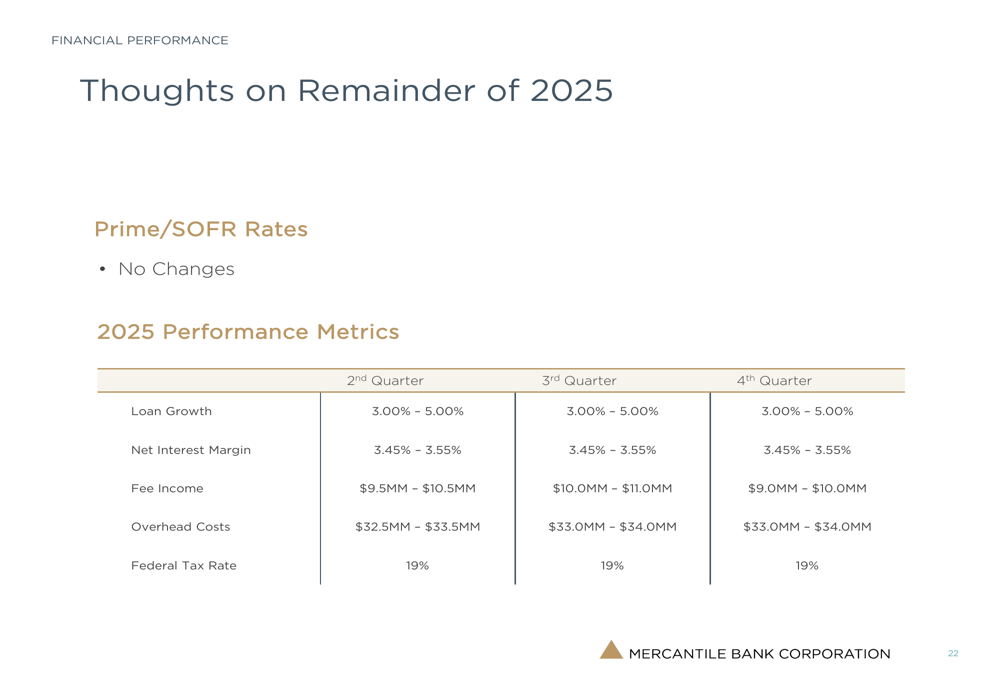

Looking ahead to the remainder of 2025, Mercantile management anticipates stable performance with continued execution of its strategic initiatives. The bank projects loan growth of 3-5% for each of the remaining quarters of 2025, with net interest margin expected to stabilize in the 3.45-3.55% range.

The bank expects fee income to range from $9.0-11.0 million per quarter, with overhead costs between $32.5-34.0 million. These projections assume no changes to the Prime/SOFR rates for the remainder of the year.

Management’s focus on relationship banking, deposit growth, and maintaining strong asset quality positions Mercantile well for continued success in 2025, despite ongoing challenges in the interest rate environment.

In conclusion, Mercantile Bank’s Q1 2025 presentation demonstrates continued progress on its strategic initiatives, with significant improvement in its loan-to-deposit ratio and strong performance in deposit growth and asset quality. While net income and EPS have declined year-over-year, the bank’s long-term positioning continues to strengthen, potentially setting the stage for improved performance as its balance sheet optimization strategy matures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.