Asia FX muted, dollar fragile as CPI data boosts Sept rate cut bets

Mercantile Bank Corporation (NASDAQ:MBWM) shares rose 0.65% to $49.07 on Tuesday, with premarket gains of 2.56%, as the Michigan-based regional bank released its second quarter 2025 investor presentation highlighting solid financial performance and a stable outlook for the remainder of the year.

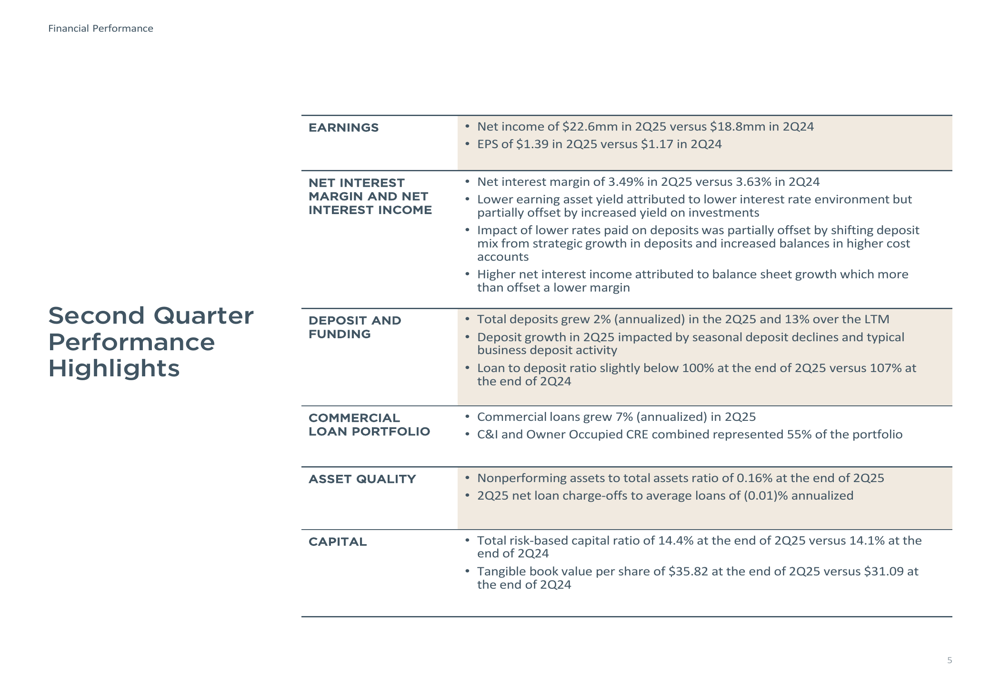

Quarterly Performance Highlights

Mercantile reported net income of $22.6 million for the second quarter of 2025, representing a substantial 20.2% increase from $18.8 million in the same period last year. Earnings per share reached $1.39, up 18.8% from $1.17 in Q2 2024, continuing the momentum from Q1 2025 when the bank reported EPS of $1.21.

The bank’s net interest margin was 3.49% in Q2 2025, showing a slight compression from 3.63% in Q2 2024, but remaining within management’s target range. This performance came despite challenges in the interest rate environment, with the bank effectively managing its balance sheet to mitigate margin pressure.

As shown in the following quarterly performance highlights, Mercantile demonstrated strength across multiple financial metrics:

The bank has consistently outperformed its peer group in key shareholder value metrics. Mercantile’s tangible book value per share reached $35.82 at the end of Q2 2025, a significant improvement from $31.09 at the end of Q2 2024, representing a 15.2% year-over-year increase. The company’s 5-year compound annual growth rate (CAGR) for tangible book value per share stands at 8.4%, while its EPS 5-year CAGR is 10.4%, both metrics outperforming its proxy peer group.

Loan and Deposit Composition

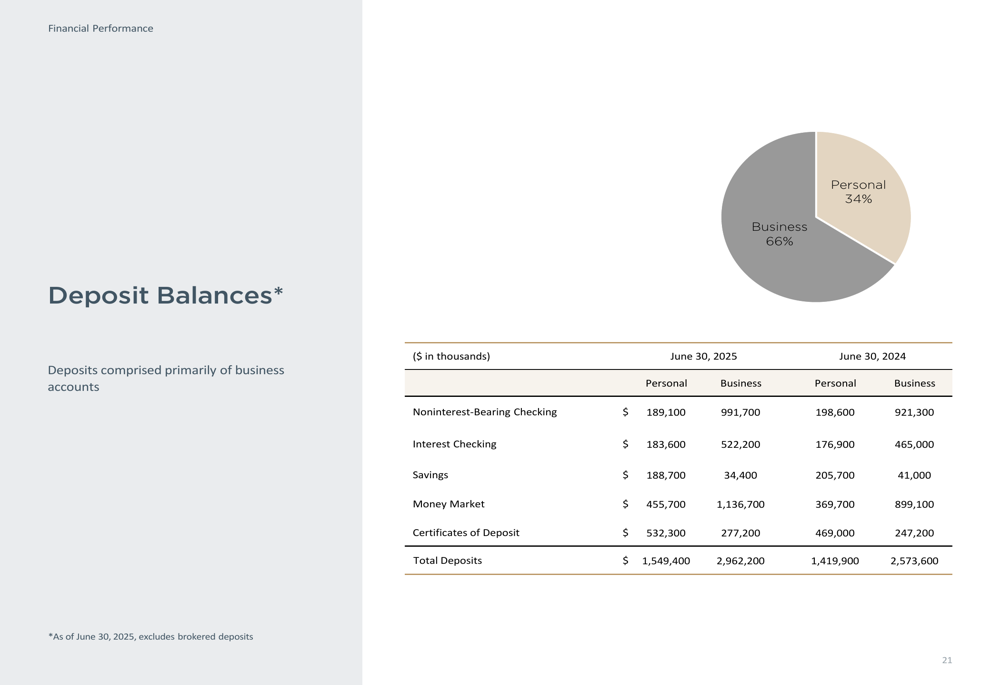

Mercantile’s loan-to-deposit ratio improved to just below 100% at the end of Q2 2025, down from 107% in Q2 2024, reflecting the bank’s successful efforts to grow deposits faster than loans. Total (EPA:TTEF) deposits grew by 2% (annualized) in Q2 2025 and 13% over the last twelve months, providing a stable funding base for the bank’s operations.

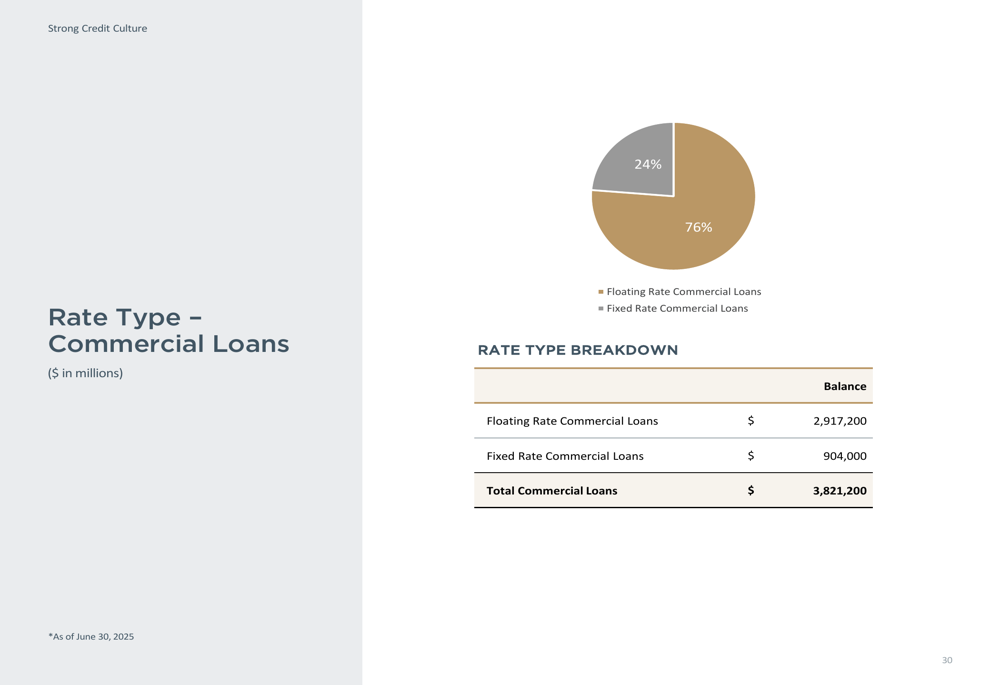

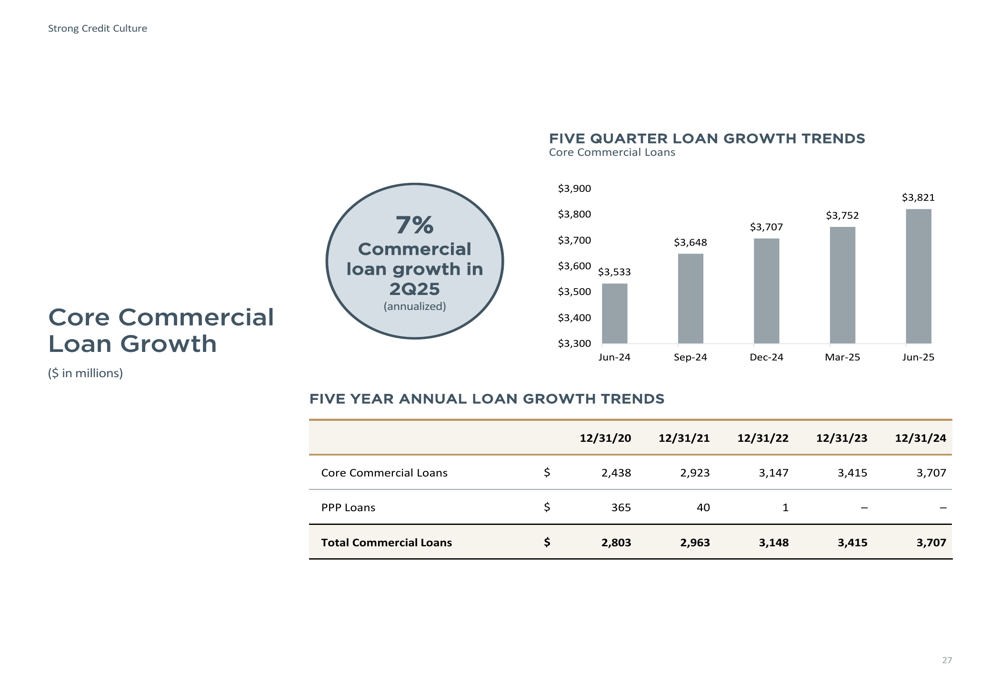

Commercial loans, which represent 81% of the total loan portfolio, grew at an annualized rate of 7% in Q2 2025. The bank maintains a well-diversified loan portfolio with a focus on commercial and industrial (C&I) loans and owner-occupied commercial real estate, which together represent 55% of the portfolio.

The following chart illustrates the bank’s loan portfolio structure by rate type, showing that 76% of commercial loans have floating rates, which positions the bank favorably in the current interest rate environment:

This rate structure provides flexibility and helps mitigate interest rate risk, as 83% of total floating rate loans reprice in less than one year, and 91% of total loans are subject to repricing within the next five years.

Deposit composition remains favorable with business deposits accounting for 66% and personal deposits 34% of the total deposit base:

The bank has maintained stable relationships with large depositors, with 80 relationships aggregating $1.5 billion as of June 30, 2025. Of the 59 relationships with over $5 million in deposits five years ago, 41 still maintain deposits over $5 million, demonstrating strong customer retention.

Asset Quality and Capital Position

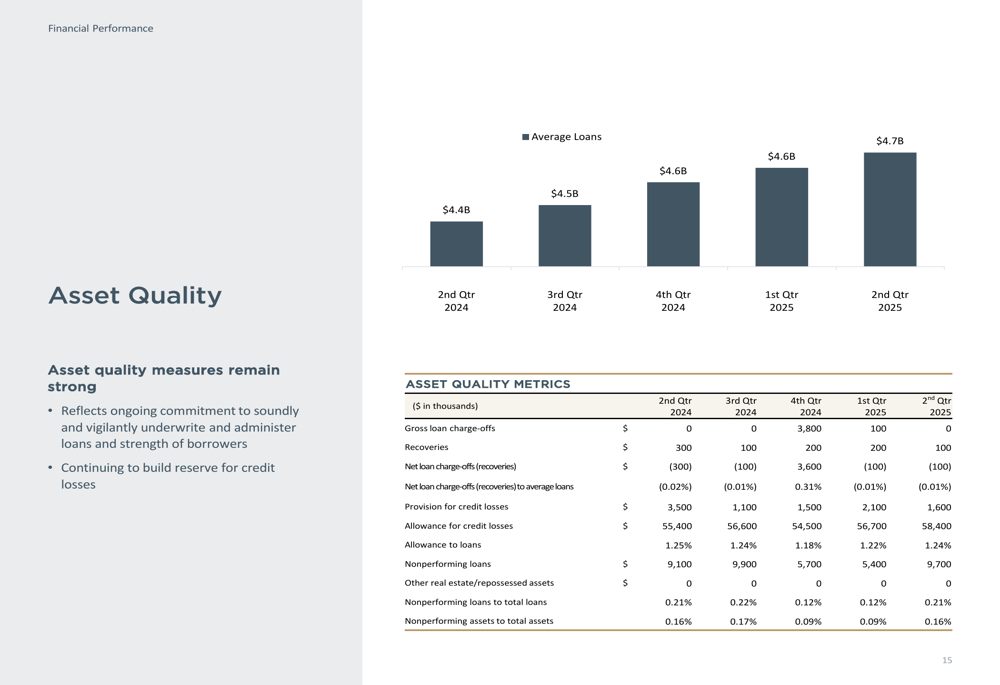

Mercantile continues to demonstrate strong asset quality metrics, with nonperforming assets to total assets ratio at a low 0.16% at the end of Q2 2025. The bank reported net loan charge-offs to average loans of -0.01% (annualized) for Q2 2025, indicating net recoveries for the period.

The following asset quality metrics highlight the bank’s strong credit culture:

The bank’s capital position remains robust, with a total risk-based capital ratio of 14.4% at the end of Q2 2025, up from 14.1% at the end of Q2 2024. This strong capital base provides flexibility for future growth opportunities and shareholder returns.

Commercial loan growth has been consistent, with core commercial loans increasing by 7% over the past year:

Strategic Initiatives

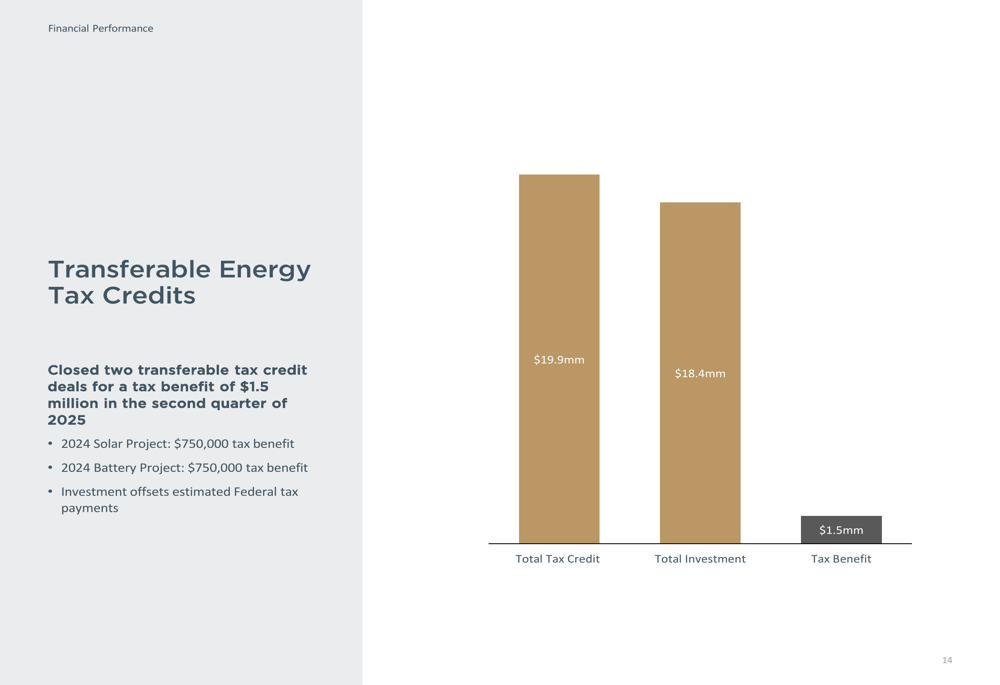

During Q2 2025, Mercantile closed two transferable tax credit deals for a combined tax benefit of $1.5 million. These deals included a 2024 Solar Project and a 2024 Battery Project, each providing a $750,000 tax benefit. This initiative represents a strategic approach to managing the bank’s tax liability while supporting renewable energy projects.

As shown in the following chart, these tax credit investments are part of the bank’s broader strategy:

The bank continues to focus on maintaining a strong credit culture with diversified lending, as evidenced by its low nonperforming assets and well-structured loan portfolio. The majority of loans have floating rates, which shortens balance sheet duration and aligns with funding sources to mitigate interest rate risk.

Forward-Looking Statements

For the remainder of 2025, Mercantile provided the following guidance:

- Loan growth of 1-2%

- Net interest margin of 3.50-3.60%

- Fee income of $9.0-10.0 million

- Overhead costs of $32.5-33.5 million

- Federal tax rate of 16%

This outlook suggests a stable operating environment for the second half of the year, with continued focus on maintaining asset quality and managing the balance sheet efficiently. The projected loan growth represents a slight moderation from the current pace, likely reflecting a cautious approach amid economic uncertainties.

The bank’s strong performance in the first half of 2025, with EPS of $1.21 in Q1 and $1.39 in Q2, positions it well to meet or exceed full-year expectations. With a current stock price of $49.07, up from the $40.26 reported after Q1 earnings, the market appears to be recognizing Mercantile’s consistent performance and solid fundamentals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.