AZTR receives NYSE delisting warning over equity requirement

Introduction & Market Context

Mercedes-Benz (OTC:MBGAF) Group AG (XETRA:MBG) presented its Q2 2025 financial results on July 30, 2025, revealing a sharp decline in profitability despite relatively resilient cash flow generation. The luxury automaker’s stock closed at €53.03 on July 29, 2025, and has been trading between €45.99 and €63.71 over the past 52 weeks.

The company faced significant headwinds from tariffs on U.S. imports and challenging market conditions in China, resulting in a substantial compression of profit margins across its main business divisions.

Quarterly Performance Highlights

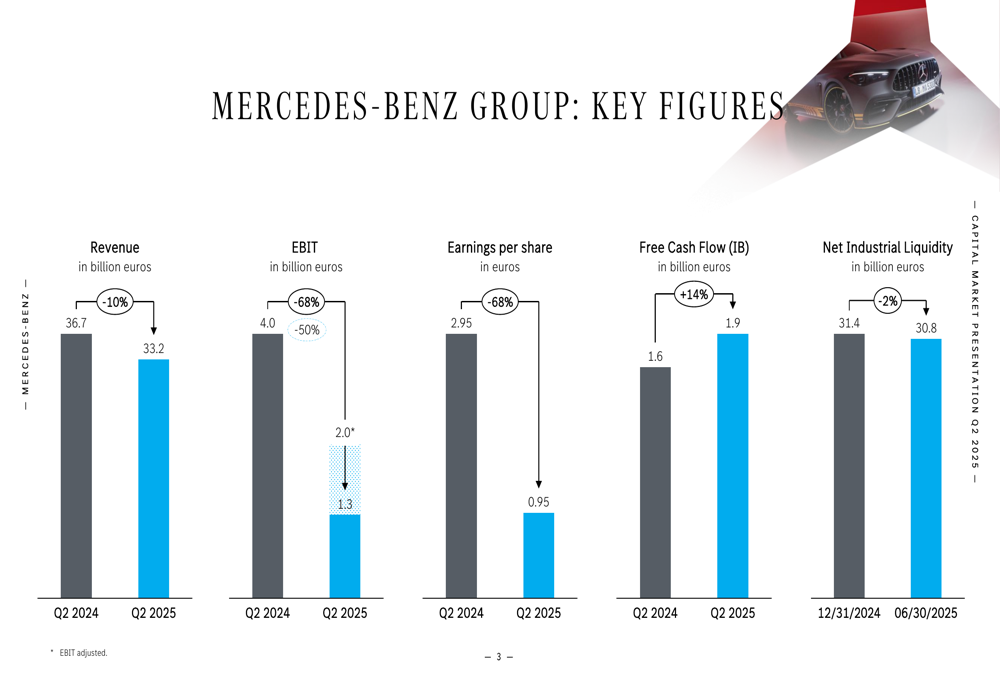

Mercedes-Benz reported revenue of €33.2 billion for Q2 2025, representing a 10% decline from €36.7 billion in the same period last year. More dramatically, EBIT plummeted 68% to €1.27 billion from €4.04 billion in Q2 2024. On an adjusted basis, EBIT fell 50% to €2.0 billion, with earnings per share dropping 68% to €0.95.

As shown in the following chart of key financial figures:

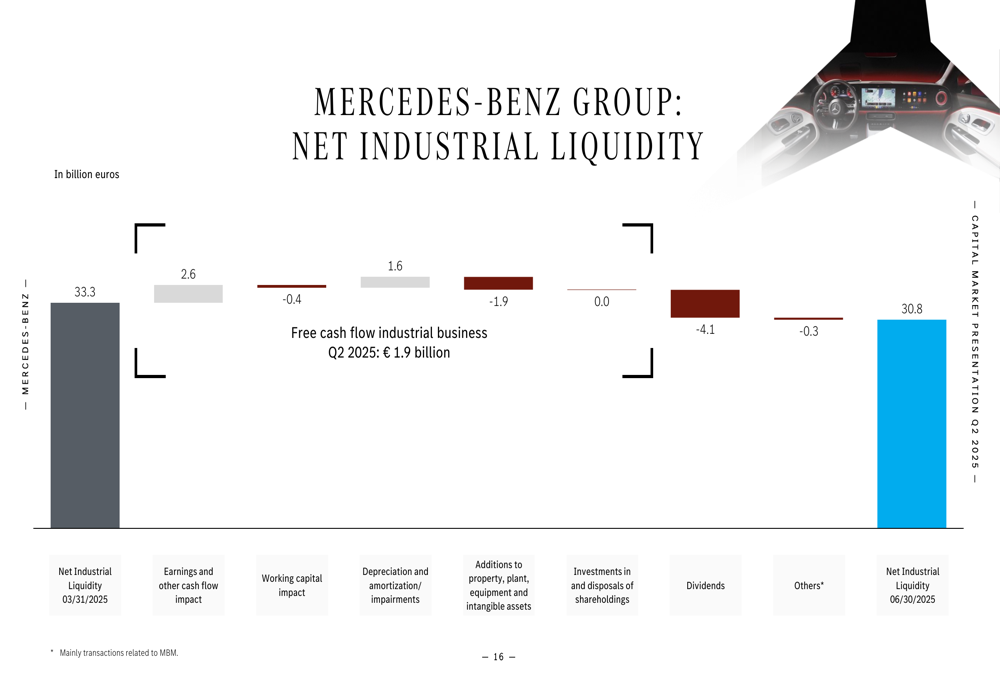

Despite the profit decline, the company managed to generate €1.9 billion in free cash flow from its industrial business, a 14% improvement compared to Q2 2024. Net industrial liquidity remained solid at €30.8 billion as of June 30, 2025, down slightly from €31.4 billion at the end of 2024.

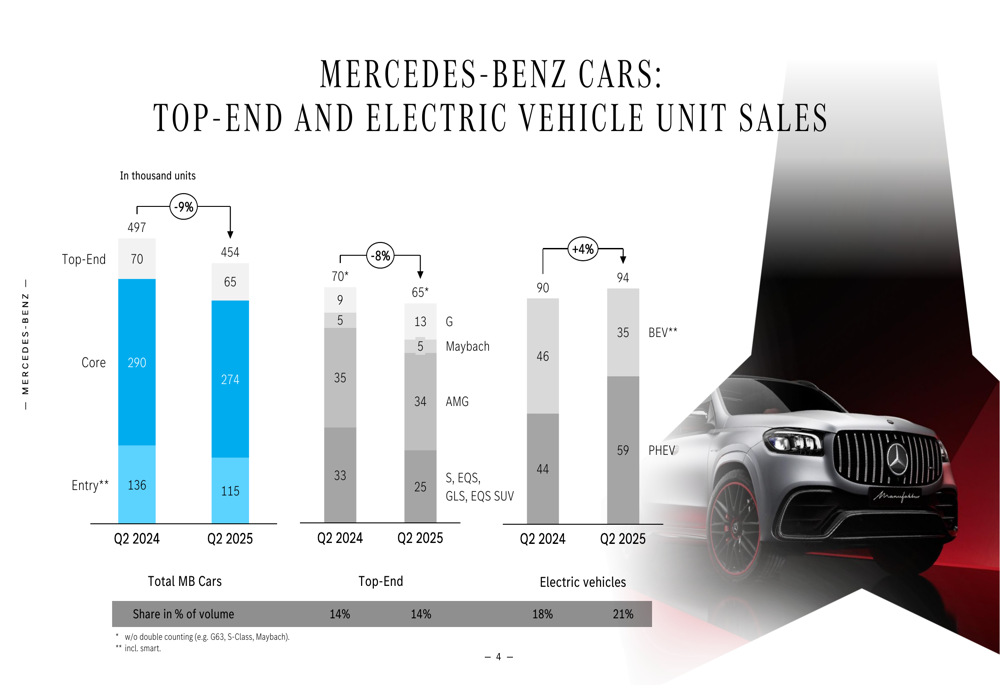

Total (EPA:TTEF) Mercedes-Benz car sales decreased by 9% to 454,000 units, while electric vehicle deliveries grew by 4% to 94,000 units, now representing 21% of total sales volume compared to 18% in Q2 2024.

The following chart illustrates the sales breakdown by segment and electric vehicle penetration:

Detailed Financial Analysis

Mercedes-Benz Cars

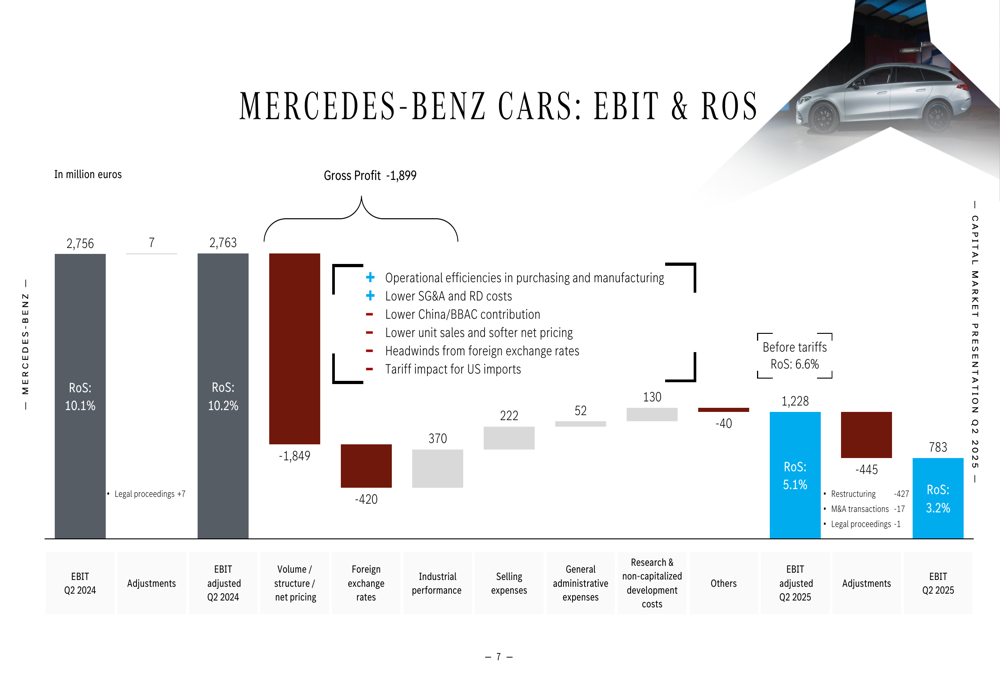

The Cars division was particularly hard hit, with adjusted EBIT falling 56% to €1.23 billion and adjusted return on sales dropping to 5.1% from 10.2% a year earlier. The division’s revenue declined 11% to €24.2 billion on 9% lower unit sales.

The following waterfall chart breaks down the factors affecting the Cars division’s EBIT performance:

Key negative factors included lower unit sales, softer net pricing, headwinds from foreign exchange rates, and notably, tariff impacts for U.S. imports. The company also cited lower contribution from its China operations and BBAC joint venture. These were partially offset by operational efficiencies in purchasing and manufacturing, as well as lower SG&A and R&D costs.

Mercedes-Benz Vans

The Vans division also experienced significant pressure, with adjusted EBIT falling 47% to €441 million and adjusted return on sales declining to 10.4% from 17.5% in Q2 2024. Revenue dropped 11% to €4.2 billion on a 10% decrease in unit sales.

Similar to the Cars division, the Vans segment faced challenges from significantly lower unit sales and negative net pricing, though this was partially offset by a healthy product mix and lower product-related expenses.

Mercedes-Benz Mobility

The Mobility division was a relative bright spot, with adjusted EBIT increasing 7% to €290 million and return on equity improving to 8.9% from 8.4% in Q2 2024. Contract volume stood at €128.8 billion as of June 30, 2025, down 4% from the end of March 2025.

Strategic Initiatives

Despite the challenging quarter, Mercedes-Benz highlighted several strategic initiatives in its presentation. The company announced the premiere of the CLA Shooting Brake and the start of production and deliveries of the CLA in July. It also reported successful long-distance testing of its VLE (Vision EQXX) technology demonstrator.

On the technology front, Mercedes-Benz showcased the AMG GT XX as a preview of future performance capabilities and demonstrated point-to-point driving assistance in China. The company also opened its first Maybach brand center in Seoul, reinforcing its luxury positioning.

The growing share of electric vehicles in the company’s sales mix indicates continued progress in its electrification strategy. Electric vehicle sales for Mercedes-Benz Vans grew even more impressively, increasing 32% to 7,000 units, now representing 7% of total van sales compared to 5% a year earlier.

Forward-Looking Statements

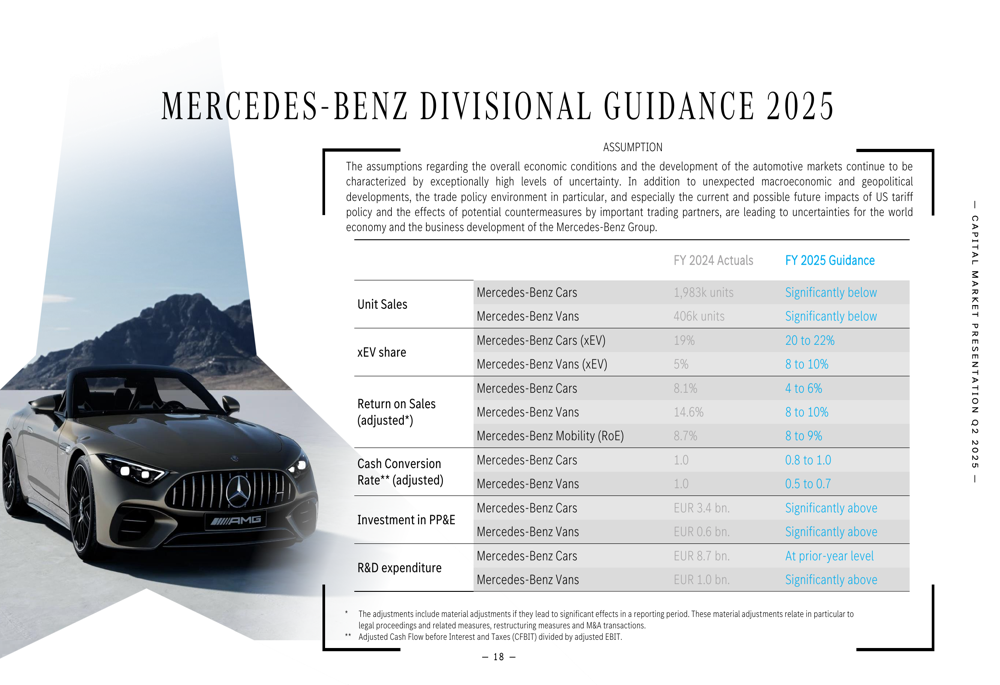

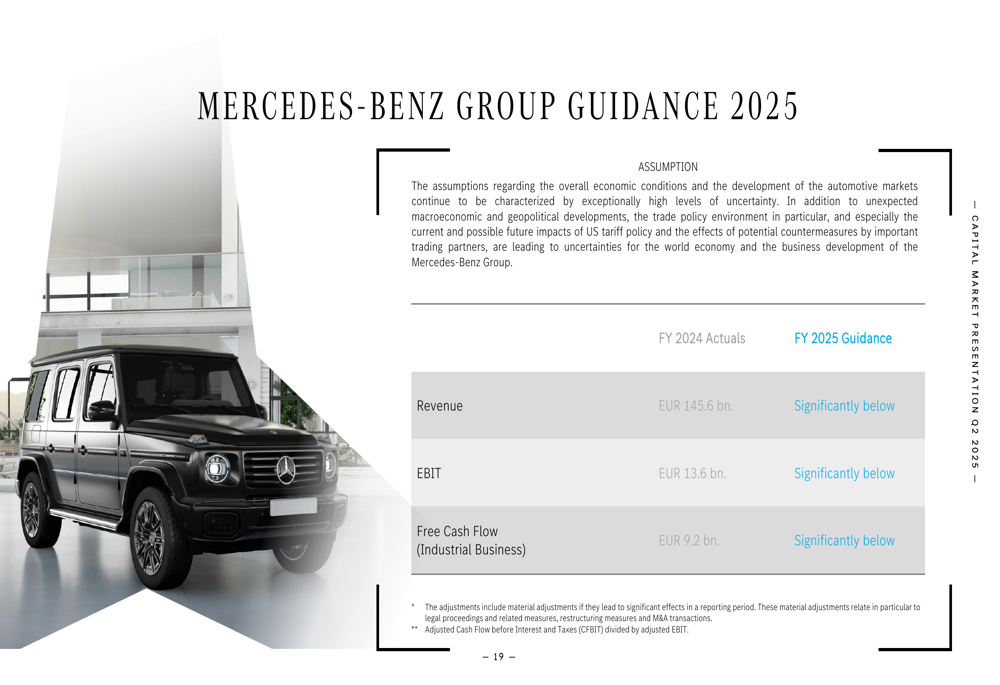

Mercedes-Benz provided a sobering outlook for the remainder of 2025, as shown in the following divisional guidance:

For Mercedes-Benz Cars, the company expects unit sales to be significantly below the prior year, with an electric vehicle share of 20-22% and return on sales between 4-6%. The Vans division is projected to achieve 8-10% return on sales with unit sales significantly below the previous year.

The overall group guidance paints a challenging picture for the full year:

Revenue, EBIT, and free cash flow from the industrial business are all expected to be significantly below prior-year levels. According to the company’s guidance definitions, "significantly below" indicates a decline of more than 7.5% for revenue, more than 15% for EBIT, and more than 25% for free cash flow.

Competitive Industry Position

Despite the profit decline, Mercedes-Benz maintained its focus on the premium segment, with Top-End vehicle sales declining less severely (-8%) than overall sales (-9%). The company’s cash generation capabilities remain intact, with €4.2 billion cash generated in the first half of 2025.

The company’s net industrial liquidity position provides a buffer against market uncertainties, as illustrated in this chart:

However, the significant dividend payment of €4.1 billion reduced the net industrial liquidity from €33.3 billion at the end of March to €30.8 billion by the end of June 2025.

Looking ahead, Mercedes-Benz is preparing for the IAA Mobility 2025 event, which will showcase its next major product launch program. The company’s ability to navigate the current headwinds while continuing to invest in future technologies and products will be crucial for its long-term competitive positioning in the premium automotive market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.