Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Mercury Systems (NASDAQ:MRCY) presented its third-quarter fiscal year 2025 financial results on May 6, revealing a company in transition with improving operational metrics despite significant earnings challenges. The defense technology provider’s stock fell 1.43% in regular trading to $49.85 and continued declining in aftermarket trading, dropping an additional 6.57% to $47.10 following the release.

The presentation, delivered by Chairman and CEO Bill Ballhaus and CFO David Farnsworth, highlighted substantial improvements in cash flow and gross margins, even as the company posted a disappointing earnings per share (EPS) figure of -$0.33, significantly missing analyst expectations of $0.10.

Quarterly Performance Highlights

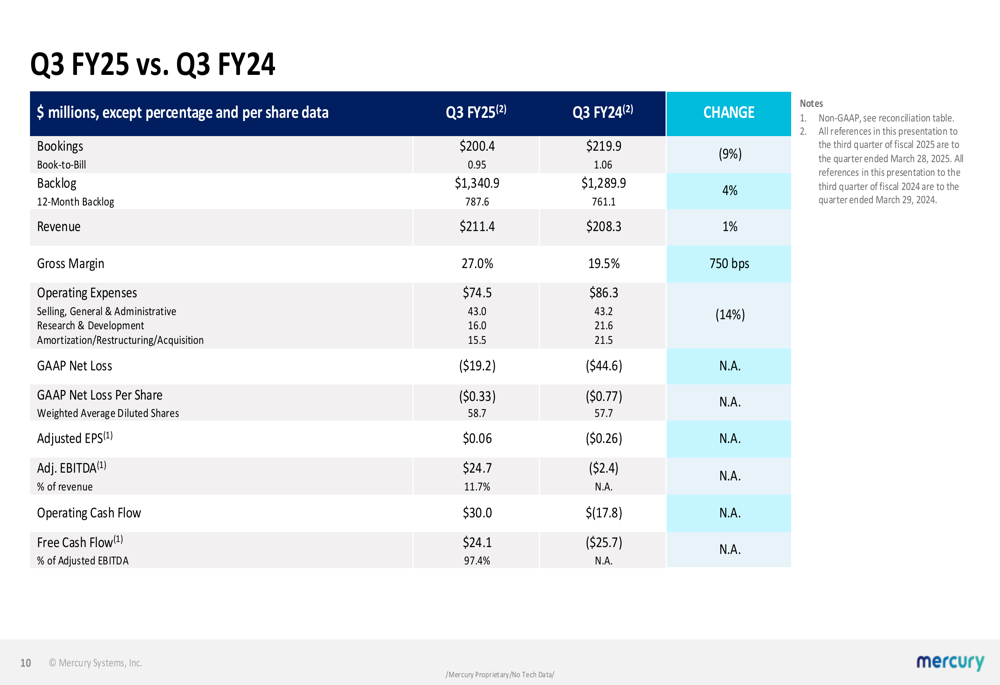

Mercury’s Q3 FY25 results showed modest top-line growth with revenue reaching $211.4 million, a 1% increase year-over-year, slightly exceeding analyst expectations of $205.88 million. The company reported bookings of $200.4 million, resulting in a book-to-bill ratio of 0.95 for the quarter, though the trailing twelve-month ratio remained positive at 1.1x.

The most notable improvement came in gross margin, which expanded to 27.0%, representing a substantial 750 basis point increase from the same period last year. This margin expansion, coupled with a 14% reduction in operating expenses, contributed to an adjusted EBITDA of $24.7 million (11.7% margin).

As shown in the following quarterly comparison:

Free cash flow emerged as a particular bright spot, with Mercury generating $24.1 million in Q3, a dramatic improvement from the negative $25.7 million reported in the same quarter last year. This cash flow improvement reflects the company’s focus on working capital optimization, which has reduced net working capital to its lowest level since Q2 FY22.

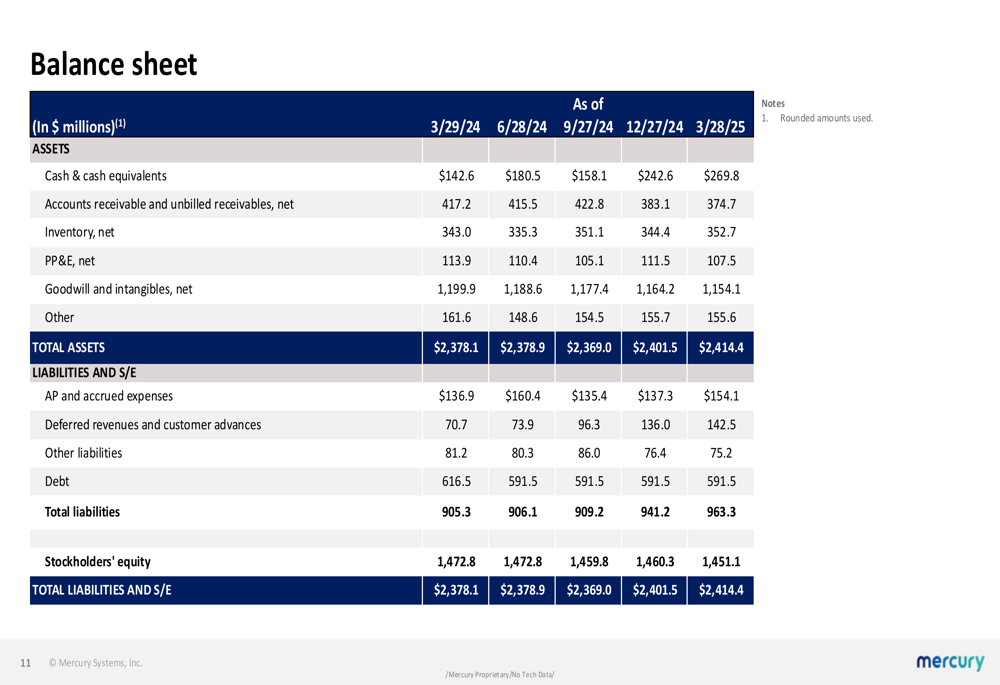

The balance sheet shows steady improvement over recent quarters:

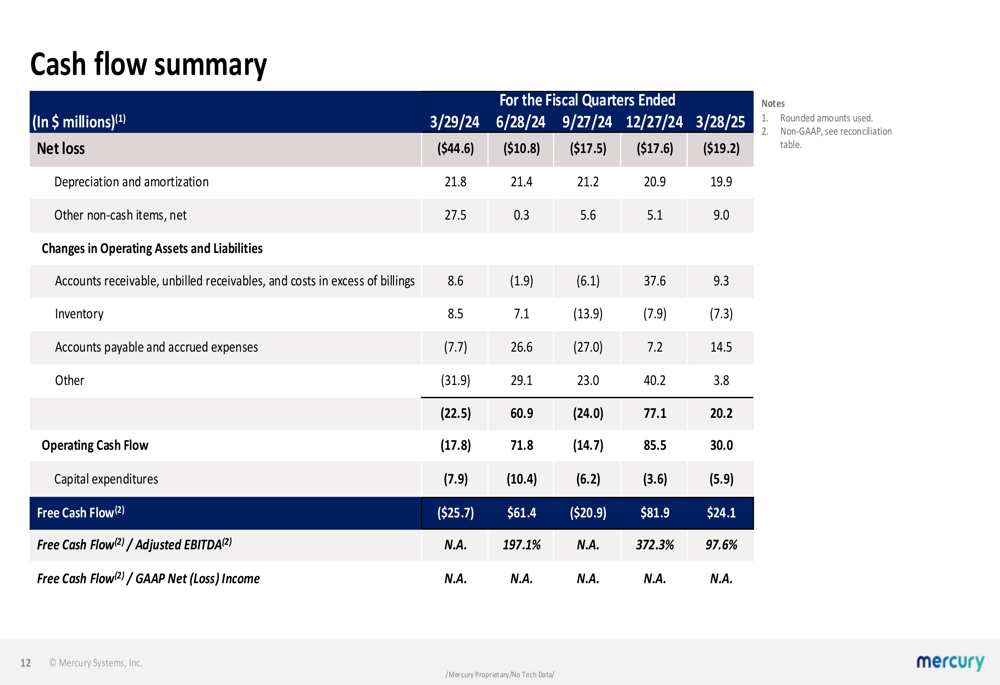

The cash flow summary further illustrates the company’s financial progress:

Strategic Initiatives

Mercury highlighted several strategic moves aimed at enhancing its competitive position. Early in Q4, the company completed the acquisition of Star Lab, which is expected to increase differentiation within its Common Processing Architecture products. Additionally, Mercury outsourced manufacturing operations in Switzerland to facilitate international growth through increased capacity and improved efficiency.

During the quarter, Mercury secured $40 million in production contracts for its Common Processing Architecture, and in April, the company announced a $20 million follow-on contract with an innovative space company, further strengthening its backlog, which stood at $1.34 billion at quarter-end (up 4% year-over-year).

CEO Bill Ballhaus expressed confidence in the company’s strategic direction, stating, "We delivered solid results in Q3 that were once again in line with or ahead of our expectations." However, this optimistic assessment contrasts with the significant EPS miss that concerned investors.

Detailed Financial Analysis

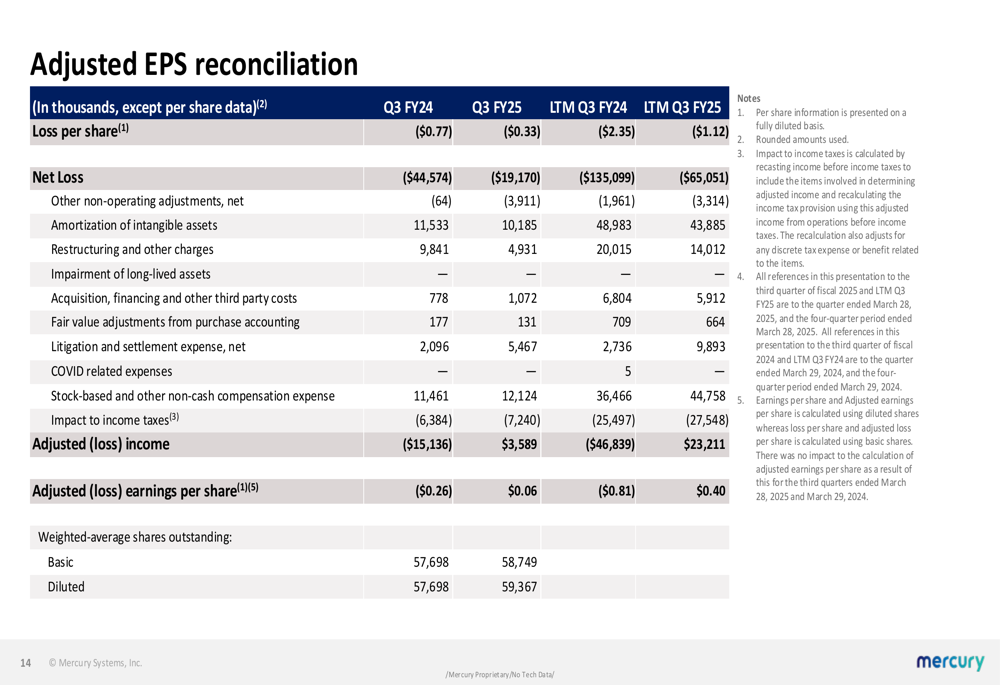

Despite the positive narrative around operational improvements, Mercury’s financial reconciliations reveal the complexity behind its reported figures. The adjusted EPS reconciliation shows the significant gap between GAAP and non-GAAP results:

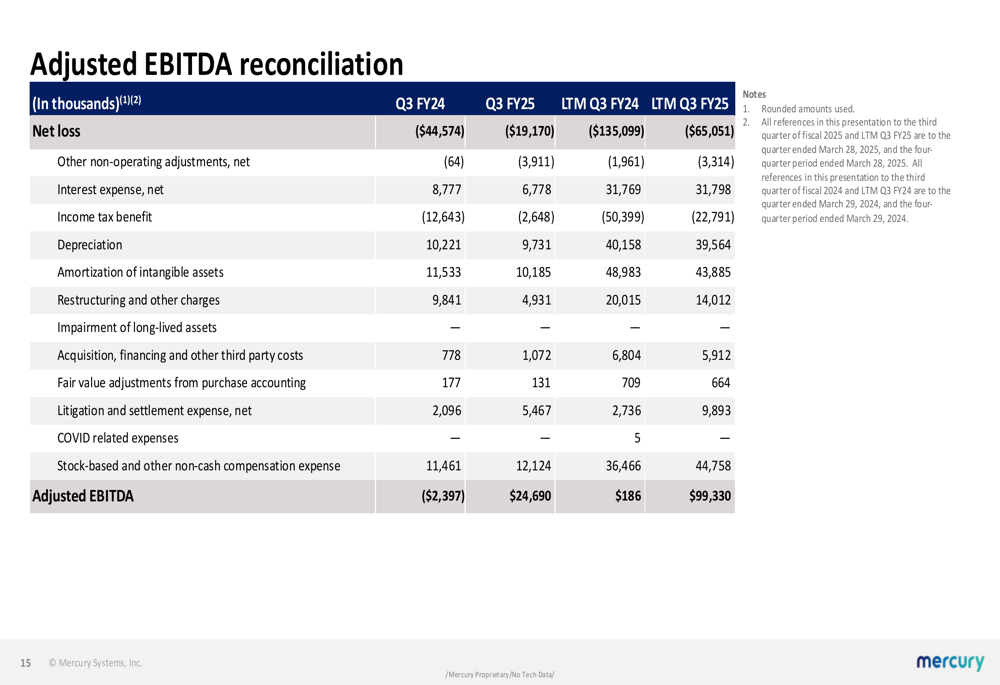

The adjusted EBITDA reconciliation similarly demonstrates the substantial adjustments made to arrive at the company’s preferred performance metrics:

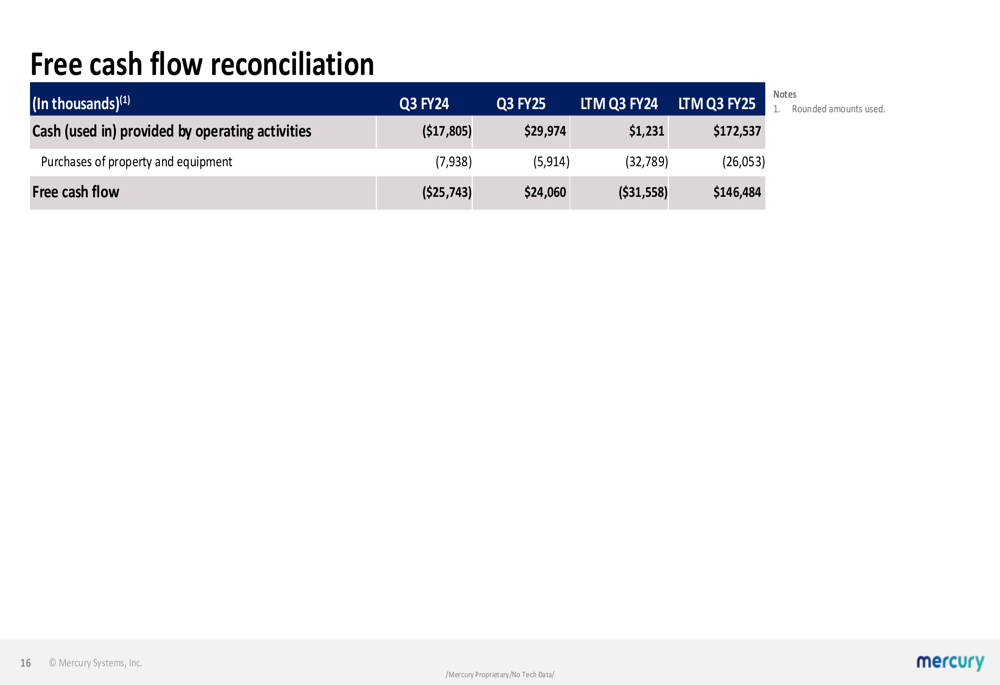

Free cash flow, a key focus area for management, showed remarkable improvement:

The company’s net debt has decreased to $322 million, its lowest level since Q1 FY22, providing Mercury with increased financial flexibility. With $270 million in cash on hand, the company appears well-positioned to continue its strategic initiatives while navigating operational challenges.

Forward-Looking Statements

Looking ahead, Mercury provided guidance that reflects cautious optimism. For fiscal year 2025, the company expects revenue growth approaching mid-single digits year-over-year, with low double-digit adjusted EBITDA margins overall. Management anticipates Q4 margins will approach mid-teens, representing the highest quarterly margins of the fiscal year.

The company’s long-term financial targets include above-market top-line growth, adjusted EBITDA margins in the low to mid-20% range, and free cash flow conversion of 50%. However, analysts at InvestingPro forecast an EPS of $0.41 for FY2025, suggesting continued profitability challenges despite operational improvements.

CFO Dave Farnsworth emphasized the company’s cash flow ambitions, noting, "We expect to get to a point where there’s a recurring 50% of EBITDA cash flow." This focus on cash generation appears to be gaining traction, with year-to-date free cash flow of $85 million already exceeding prior expectations, though Q4 free cash flow is expected to be around break-even.

As Mercury continues its transformation efforts, investors will be watching closely to see if operational improvements ultimately translate into bottom-line results that match the company’s optimistic outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.